- Pharmaceuticals

- Non-Melanoma Skin Cancer Market

Non-Melanoma Skin Cancer Market Size, Share, Trends, Growth, and Regional Forecasts, 2025 - 2032

Non-Melanoma Skin Cancer Market By Indication (Basal Cell Carcinoma, Squamous Cell Carcinoma, Merkel cell carcinoma, and Others), Treatment (Surgery, Radiotherapy, Photodynamic Therapy, and Chemotherapy), End-user, and Regional Analysis from 2025 - 2032

Non-melanoma Skin Cancer Market Share and Trends Analysis

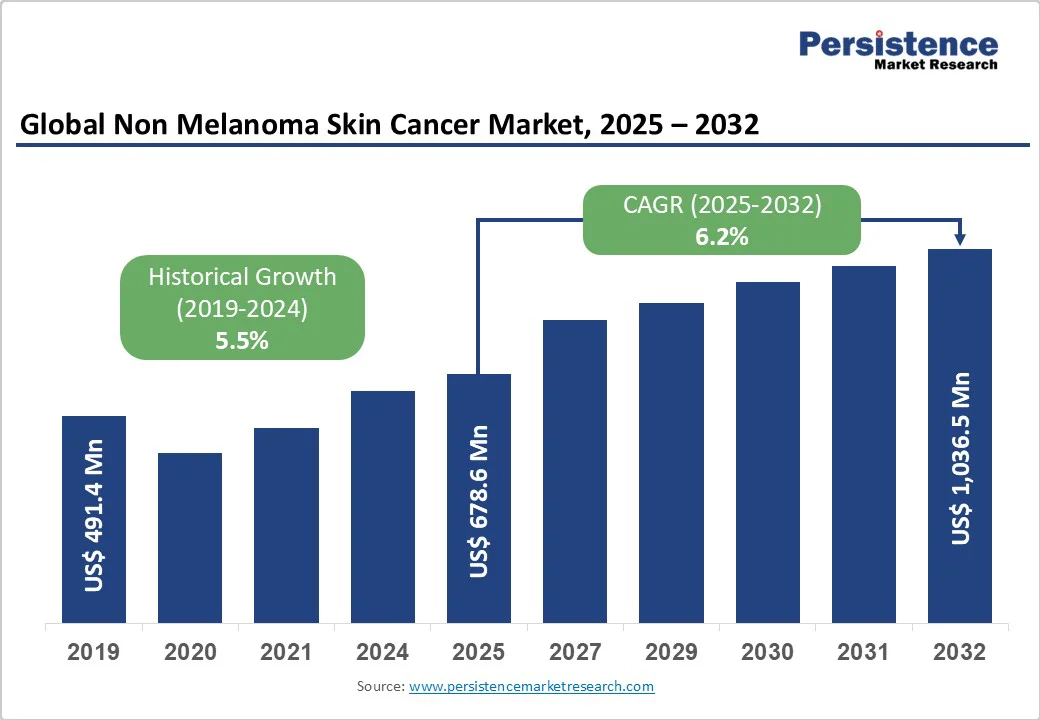

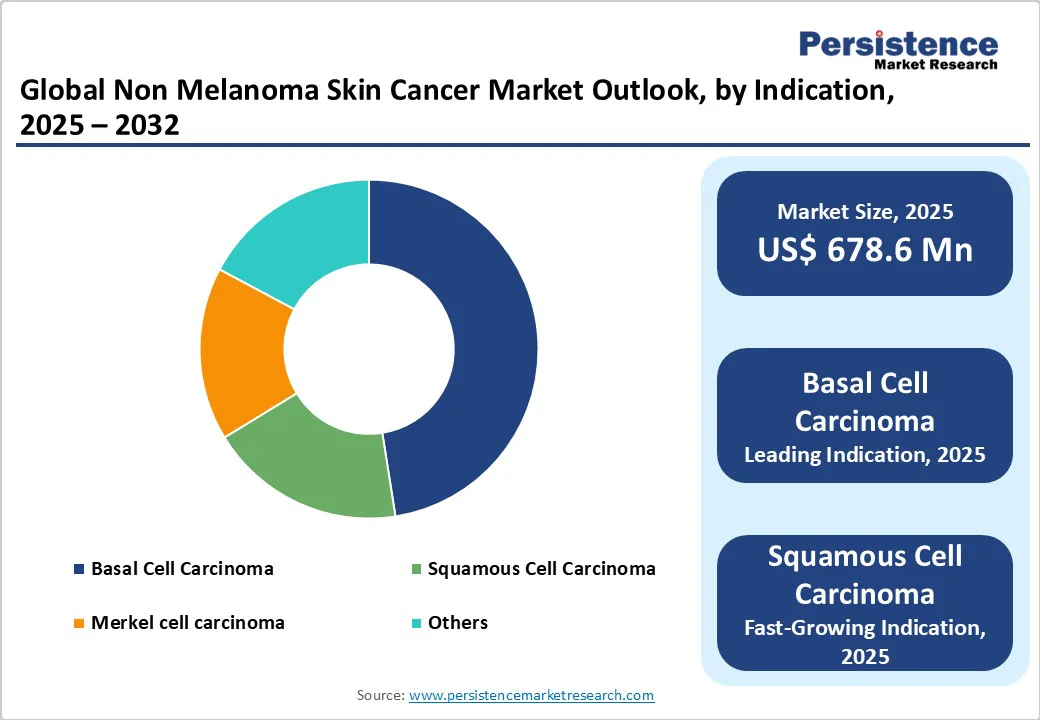

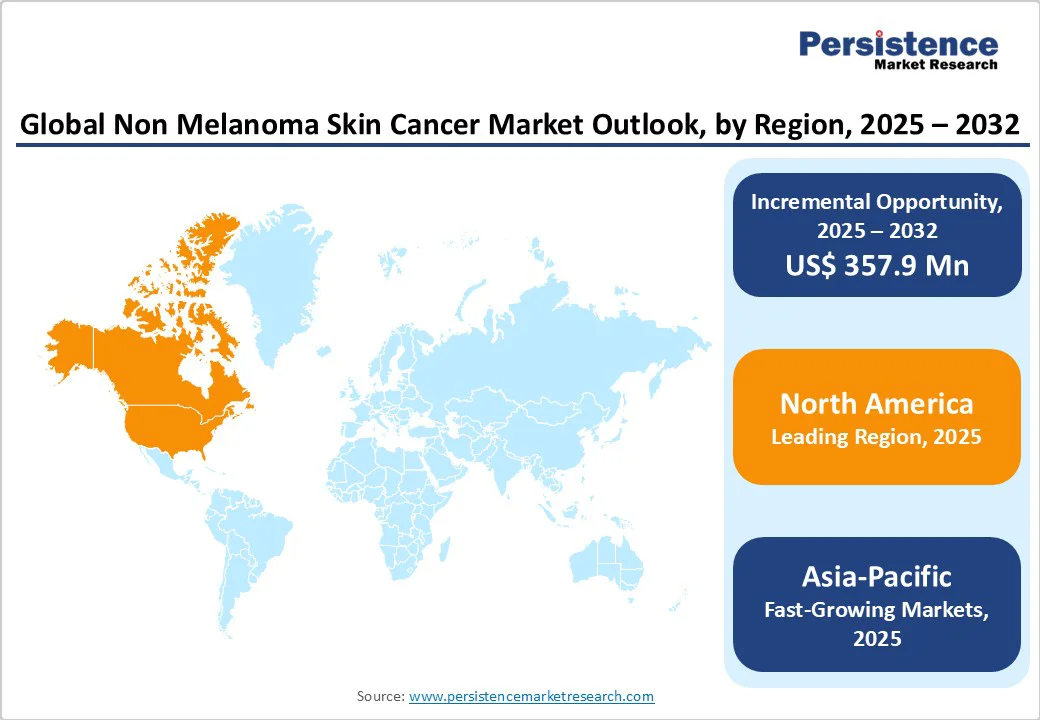

The global non melanoma skin cancer market size is likely to value at US$ 678.6 million in 2025 and is projected to reach US$ 1,036.5 million by 2032, growing at a CAGR of 6.2% during the forecast period from 2025 to 2032. Global demand for non-melanoma skin cancer (NMSC) is rising as awareness of skin cancer prevention, early diagnosis, and advanced treatment options increases across hospitals, dermatology clinics, and specialized cancer centers. Additionally, expansion in healthcare infrastructure, rise in skin cancer incidences, government screening programs, and investments in oncology facilities in developing regions are enhancing product availability and adoption, further fueling market growth.

Key Industry Highlights:

- Leading Region: North America leads globally with a 35.5% share, supported by advanced healthcare infrastructure, high awareness of skin cancer screening, and the presence of major pharmaceutical and biotech companies.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by rising skin cancer incidence, growing awareness of early detection, expanding healthcare facilities, and increasing adoption of advanced therapies.

- Leading Indication Category: Basal cell carcinoma (BCC) is projected to dominate with 43.7% share, due to due to its high prevalence among non-melanoma skin cancers, increasing awareness and early diagnosis, and strong adoption of advanced targeted therapies.

- Fastest-Growing Indication Category: Growing demand for squamous cell carcinoma treatment is gaining traction, driven by rising incidence rates, increased adoption of immune checkpoint inhibitors, and growing demand for effective therapies in advanced or high-risk cases.

| Key Insights | Details |

|---|---|

|

Non Melanoma Skin Cancer Market Size (2025E) |

US$ 678.6 Mn |

|

Market Value Forecast (2032F) |

US$ 1,036.5 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

6.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.5% |

Market Dynamics

Driver - Rising Incidence Linked to Chronic Immunosuppression and Technological Advancements in Non-Invasive Diagnostics

The growing number of organ transplant recipients and patients on long-term immunosuppressive therapy significantly elevates the risk of non-melanoma skin cancer (NMSC). Transplant recipients are 65–250 times more likely to develop squamous cell carcinoma than the general population.

For instance, in April 2023, according to a study published in the National Library of Science, NMSC incidence among transplant patients reaches 82% in Australia, 35% in the U.S., and 10–15% in Southern Europe over ten years. This rising burden highlights the need for early dermatologic surveillance, advanced diagnostic imaging, and teledermatology solutions to enable timely detection and management.

The adoption of advanced diagnostic tools such as confocal microscopy, optical coherence tomography (OCT), and AI-driven lesion analysis is transforming the early detection of non-melanoma skin cancer. These innovations enable clinicians to visualize skin architecture at near-histological resolution, facilitating precise diagnoses without the need for invasive biopsies. The integration of machine learning algorithms further enhances diagnostic accuracy by identifying subtle morphological changes invisible to the human eye.

Restraints - High Cost and Access Barriers to Advanced Therapies and Recurrence-Related Treatment Limitations

The high prices of targeted therapies and immunotherapies, often several times more expensive than conventional treatments, pose a significant barrier to widespread adoption, particularly in low- and middle-income countries.

Limited insurance coverage and reimbursement policies further restrict patient access, even though these therapies demonstrate superior clinical outcomes and reduced recurrence rates. Additionally, the requirement for specialized healthcare infrastructure and trained personnel to administer these advanced treatments compounds accessibility challenges, creating disparities in care.

High-risk squamous cell carcinoma (SCC) cases exhibit high recurrence rates, presenting significant challenges for clinical management. Such frequent relapses complicate long-term treatment planning and increase the need for ongoing monitoring, multiple interventions, and combination therapies. Moreover, resistance to conventional treatments can reduce overall effectiveness, necessitating more aggressive or novel therapeutic approaches.

Opportunity - Advancements in Targeted Therapies and AI-Enabled Teledermatology Solutions

The growing focus on targeted small-molecule inhibitors presents a significant opportunity in the non-melanoma skin cancer market. Novel agents such as Silmitasertib (CX-4945), a casein kinase 2 (CK2) inhibitor, are demonstrating strong clinical potential in advanced BCC cases where standard treatments fail.

For instance, in April 2025, Senhwa Biosciences, Inc. completed a Phase 1/Dose Expansion Trial of Silmitasertib, reporting positive outcomes. Specifically, three patients achieved over 30% tumor reduction, and two exhibited progression-free survival beyond 21 months. These promising results highlight growing opportunities for next-generation targeted and precision therapies in the market.

The integration of AI-powered image recognition with teledermatology platforms is revolutionizing non-melanoma skin cancer (NMSC) screening, particularly in underserved or remote regions. By enabling rapid, accurate assessment of suspicious lesions without the need for in-person visits, these technologies can bridge gaps in access to dermatologic care. This approach not only accelerates early detection and referral but also reduces healthcare costs and patient travel burden.

Category-wise Analysis

By Indication, Basal Cell Carcinoma Dominates Globally Due to its Slow-Growing Nature and Frequent Occurrence in Sun Exposed Areas

The basal cell carcinoma (BCC) segment is projected to lead the global non melanoma skin cancer market with 72.4% in 2025. The segment’s strong performance is driven by its high prevalence, particularly among populations with fair skin and chronic UV exposure, coupled with the aging global population. Additionally, the relatively slow-growing nature of BCC facilitates early detection and treatment, supporting widespread adoption of both surgical and non-invasive therapies.

For instance, according to the Cancer Council, around 1,664 people were diagnosed with non-melanoma skin cancer in 2024, with basal cell carcinoma (BCC) accounting for around 70% of cases. BCC originates in the lower layer of the epidermis and can develop anywhere on the body, though it most commonly appears on areas exposed to frequent or intermittent sunlight, such as the head, face, neck, shoulders, and back.

By Treatment, Surgery Dominates Due to High Cure Rates and Low Recurrence for Localized Lesions

The surgery segment is expected to dominate the global non melanoma skin cancer market in 2025 with a revenue share of 44.7%. This is due to its high cure rates and low recurrence, particularly for localized lesions. The widespread adoption of Mohs micrographic surgery and other advanced surgical techniques, along with increasing early diagnosis and growing patient awareness, further drives demand for surgical interventions over non-surgical treatments such as radiotherapy, photodynamic therapy, or chemotherapy.

By End-user, Hospitals Segment Leads Due to High Surgical Volume and Advanced Infrastructure

The hospitals segment is projected to hold 48.1% of the global non melanoma skin cancer market in 2025 due to their ability to provide comprehensive care, including surgical interventions, radiotherapy, and advanced diagnostic services. Hospitals also manage high-risk and complex cases, offer access to multidisciplinary teams, and have the infrastructure for follow-up and recurrence management, making them the preferred choice for both patients and clinicians.

Regional Analysis

North America Non Melanoma Skin Cancer Market Trends

The North America market is expected to dominate globally with a value share of 41.1% in the 2025, with the U.S. leading the region. This dominance is due to the high prevalence of NMSC among the population, particularly due to widespread UV exposure and an aging demographic.

For instance, according to The Skin Cancer Foundation, around 90% of non-melanoma skin cancers are linked to ultraviolet (UV) radiation from the sun. Basal cell carcinoma (BCC) is the most common type, with an estimated 3.6 million cases diagnosed annually in the U.S. alone.

The region benefits from advanced healthcare infrastructure, including well-equipped hospitals, specialized dermatology clinics, and access to advanced diagnostic and treatment technologies. Additionally, rapid adoption of innovative therapies, such as immunotherapies, targeted treatments, and minimally invasive surgical techniques, supports market growth.

Europe Non Melanoma Skin Cancer Market Trends

Europe is projected to experience steady growth, supported by rising awareness of skin cancer prevention, increasing adoption of advanced diagnostic and therapeutic technologies, a growing geriatric population, and government initiatives promoting early detection and treatment of non-melanoma skin cancers.

In Germany, a nationwide skin cancer screening program has been implemented, entitling all individuals with statutory health insurance aged 35 and above to undergo a full-body visual skin examination every two years. Additionally, the presence of well-established healthcare infrastructure and increasing investment in dermatology clinics and outpatient services further drives market growth across the region.

Asia and Pacific Non Melanoma Skin Cancer Market Trends

Asia Pacific is expected to register a relatively higher CAGR of around 8.2% between 2025 and 2032, driven by the increasing prevalence of NMSC, resulting from factors such as higher UV exposure, aging populations, and lifestyle changes. Public awareness campaigns and educational programs are promoting early detection and preventive behaviors, encouraging more individuals to undergo regular dermatologic check-ups. The region is also seeing significant investments in healthcare infrastructure, including modern hospitals, specialty dermatology clinics, and telemedicine platforms, which enhance access to diagnosis and treatment services.

Additionally, supportive government policies and initiatives aimed at expanding dermatology services and improving cancer care are fostering market growth. Rapid urbanization, increasing disposable incomes, and higher healthcare spending are enabling more patients to access quality dermatologic care, while rising demand for minimally invasive procedures and targeted therapies is further boosting market growth in the region.

Competitive Landscape

The global non melanoma skin cancer market is highly competitive, with major players such as Pfizer Inc, F. Hoffmann-La Roche Ltd., Merck & Co., Inc., and Novartis AG dominating the market through a combination of product innovation, strategic partnerships, mergers and acquisitions, and geographic expansion. These companies are consistently investing in research and development of advanced therapies, including immune checkpoint inhibitors, hedgehog pathway inhibitors, and topical treatments, to improve clinical outcomes and patient safety. Additionally, they have robust distribution networks and regulatory expertise to expand their presence in emerging regions.

Key Industry Developments:

- In October 2025, Regeneron Pharmaceuticals announced that the U.S. FDA approved the PD-1 inhibitor Libtayo (cemiplimab-rwlc) as an adjuvant treatment for adults with high-risk cutaneous squamous cell carcinoma (CSCC) following surgery and radiation. The FDA granted Priority Review, highlighting its potential to significantly enhance efficacy and safety for this serious condition.

- In January 2024, Medison Pharma announced an exclusive multi-national agreement with Regeneron Ireland DAC, a subsidiary of Regeneron Pharmaceuticals, Inc., to commercialize Libtayo (cemiplimab) in select European and other international markets. Libtayo is a fully human monoclonal antibody that targets the PD-1 immune checkpoint receptor on T cells, enhancing the immune system’s ability to recognize and attack cancer cells

- In May 2023, Sun Pharmaceutical Industries announced a licensing agreement with Philogen SpA, a Swiss-Italian biopharmaceutical company, to commercialize an investigational skin cancer therapy across Europe, Australia, and New Zealand. The partnership focuses on Nidlegy, Philogen’s anti-cancer biopharmaceutical currently in Phase III clinical trials, developed for the treatment of both melanoma and non-melanoma skin cancers.

Companies Covered in Non-Melanoma Skin Cancer Market

- Pfizer Inc

- F. Hoffmann-La Roche Ltd.

- Merck & Co., Inc.

- Novartis AG

- Viatris Inc.

- Sun Pharmaceutical Industries Ltd.

- Sanofi

- Regeneron Pharmaceuticals Inc.

- Almirall S.A.

- Senhwa Biosciences, Inc

- Sirnaomics

- OncoBeta

- Verrica Pharmaceuticals.

- Medivir AB

- Checkpoint Therapeutics, Inc.

Frequently Asked Questions

The global non melanoma skin cancer market is projected to be valued at US$ 678.6 Mn in 2025.

Rising incidence of non-melanoma skin cancers and increasing demand for advanced targeted and immunotherapy treatments are driving market growth.

The global non melanoma skin cancer market is poised to witness a CAGR of 6.2% between 2025 and 2032.

Development of targeted therapies, immune checkpoint inhibitors, and RNA-based drugs, along with the growing adoption of advanced topical and photodynamic therapies, is creating significant opportunities.

Pfizer Inc, F. Hoffmann-La Roche Ltd., Merck & Co., Inc., and Novartis AG are key players.