- Beverages

- Non-Alcoholic Beer Market

Non-Alcoholic Beer Market Size, Share, and Growth Forecast, 2026 - 2033

Non-Alcoholic Beer Market by Packaging Type (Cans, Glass Bottles, PET Bottles, Kegs), Product Type (Lager, Ale, Stout, Wheat Beer), Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Bars & Restaurants, Online Retail), and Regional Analysis for 2026 - 2033

Non-Alcoholic Beer Market Share and Trends Analysis

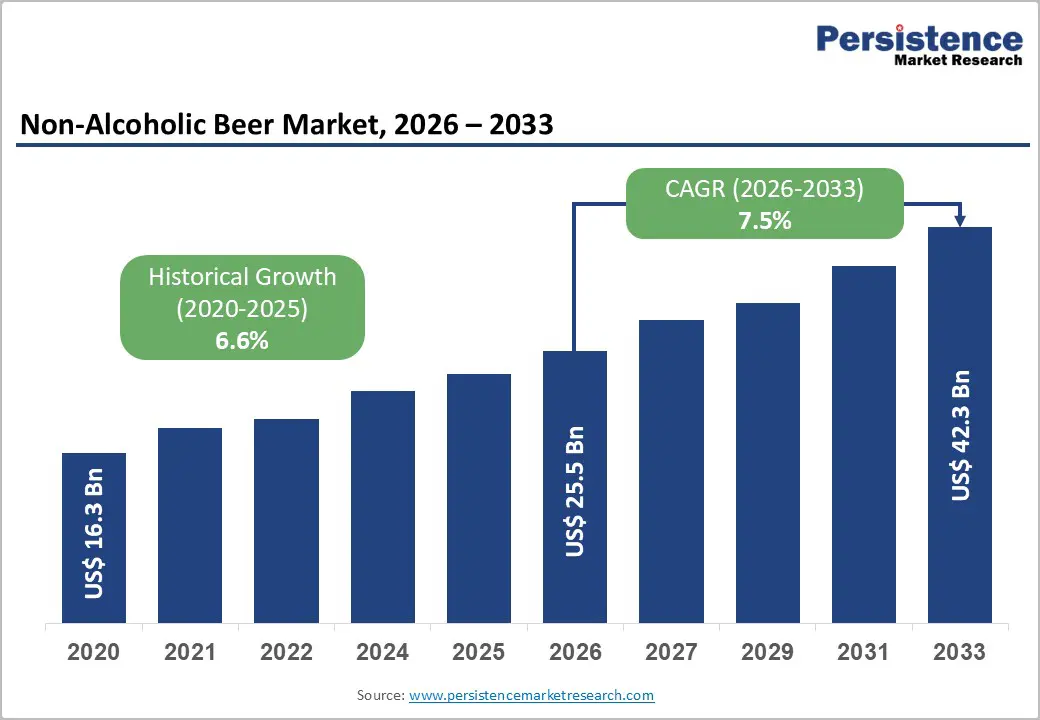

The global non-alcoholic beer market size is likely to be valued at US$ 25.5 billion in 2026, and is projected to reach US$ 42.3 billion by 2033, growing at a CAGR of 7.5% during the forecast period 2026−2033. The market is registering steady expansion as consumers are shifting toward low- and zero-alcohol beverages while maintaining traditional beer consumption occasions.

Breweries are adopting advanced dealcoholization methods such as vacuum distillation and reverse osmosis to retain aroma compounds and preserve flavor integrity. Producers are also introducing premium variants that replicate established beer styles while aligning with health awareness and regulatory expectations. The World Health Organization (WHO) and several national health authorities are intensifying alcohol risk awareness campaigns, which are influencing consumer choices and encouraging breweries to expand alcohol-free product portfolios.

Market demand is strengthening as younger demographics are prioritizing moderation and wellness-oriented consumption. Governments are introducing stricter alcohol taxation policies and advertising controls, which are encouraging beverage producers to diversify into alcohol-free offerings that maintain brand relevance.

Large brewers are scaling distribution through supermarkets, convenience stores, and digital commerce channels to increase accessibility. Europe is maintaining strong market penetration due to established alcohol-free beer traditions, while Asia Pacific and Latin America are generating new demand as urban populations expand and disposable incomes rise. These structural shifts are positioning non-alcoholic beer as a strategic growth category within the global brewing industry.

Key Industry Highlights

- Product Type Leadership: Lager is expected to lead with an estimated 52% revenue share in 2026, while ale-based variants are projected to grow the fastest through 2033 as craft brewing innovations attract premium consumers.

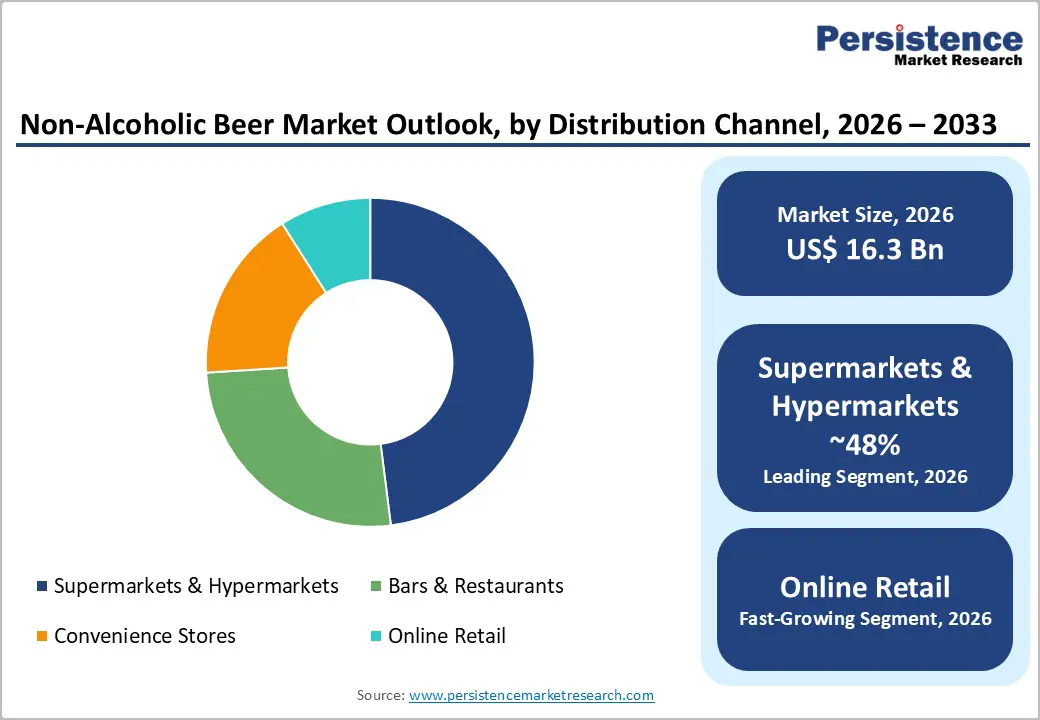

- Distribution Channel Dynamics: Supermarkets and hypermarkets are projected to dominate, with approximately 48% revenue share in 2026, whereas online retail platforms are anticipated to expand the fastest at roughly 11.2% CAGR through 2033, driven by the widening adoption of direct-to-consumer (D2C) models.

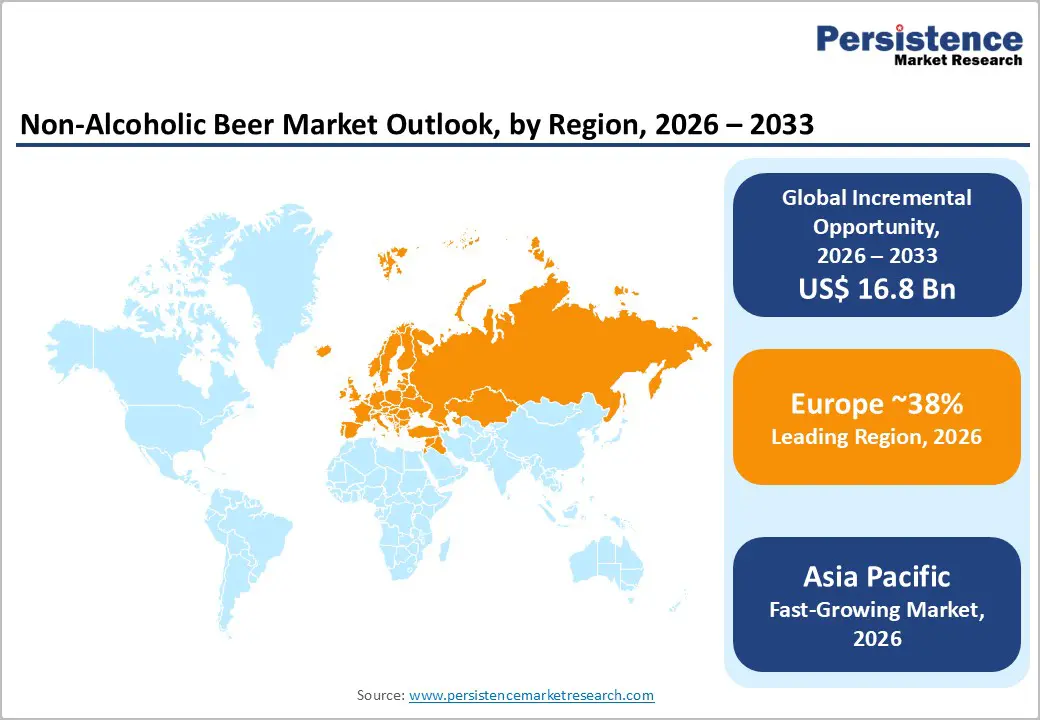

- Regional Leadership: Europe is expected to command around 38% in 2026, supported by well-established brewing infrastructure across Germany, Spain, and the Netherlands.

- Fastest-Growing Market: The Asia Pacific market is forecast to register the highest growth through 2033, driven by an increasing demand for moderated drinking alternatives across Japan, China, and India.

- Technology Catalyst: Advances in vacuum distillation, reverse osmosis, and specialized yeast fermentation technologies are improving flavor retention in alcohol-free beer, enabling brewers to achieve taste parity with conventional beer.

- Strategic Opportunity: The emergence of functional and premium non-alcoholic beer formulations, including electrolyte-enhanced and craft-style variants, is creating new high-margin product segments.

- December 2025: Athletic Brewing partnered with OpenTable during its “Athletic January” campaign to help diners locate restaurants serving its non-alcoholic beers through an interactive map.

| Key Insights | Details |

|---|---|

|

Non-Alcoholic Beer Market Size (2026E) |

US$ 25.5 Bn |

|

Market Value Forecast (2033F) |

US$ 42.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Moderation Culture and Sober-Curious Consumer Demographics

Global alcohol consumption patterns are shifting toward moderation, which is accelerating adoption of non-alcoholic beer. Public health institutions are strengthening awareness campaigns about the long-term health risks linked with excessive alcohol intake. The WHO estimates that harmful drinking is causing nearly three million deaths annually, which is prompting governments to promote responsible consumption policies. Countries such as the United Kingdom, Canada, and Australia are expanding national health communication programs that encourage reduced alcohol intake, particularly among younger adults. These initiatives are influencing beverage companies to diversify product portfolios and introduce alcohol-free alternatives that align with emerging health priorities.

Demographic dynamics are reinforcing these behavioral transitions. Research from the International Alliance for Responsible Drinking (IARD) shows that Generation Z consumers are consuming less alcohol than earlier cohorts while still participating in social occasions involving beer. Breweries are responding by launching non-alcoholic variants that replicate popular beer styles such as lagers and India pale ales (IPAs). This strategy is preserving brand engagement while addressing evolving consumer preferences. Producers are positioning alcohol-free beer as a parallel offering within their portfolios, enabling consumers to participate in social rituals without alcohol exposure while sustaining long-term category demand.

Technological Advancements in Dealcoholization Processes

Brewing technology advancements are improving the sensory quality of alcohol-free beer and strengthening consumer acceptance. Earlier alcohol removal processes often eliminated aromatic compounds along with ethanol, which resulted in weaker flavor profiles. Modern methods such as vacuum distillation, reverse osmosis membrane filtration, and specialized yeast fermentation are preserving volatile aroma components while selectively removing alcohol. These techniques are enabling brewers to produce alcohol-free variants that closely resemble traditional beer styles in taste and aroma, which is improving product credibility among mainstream consumers.

Industry data from the Brewers Association indicates that craft breweries are increasingly adopting low-temperature dealcoholization processes to reduce flavor degradation during production. Large multinational brewers are investing in dedicated alcohol-free brewing lines to improve operational efficiency and scale manufacturing capacity. Producers are also deploying genetically optimized yeast strains that naturally generate lower alcohol during fermentation, which reduces reliance on post-processing technologies. These technical improvements are stabilizing production costs and enhancing flavor consistency, which is strengthening adoption across both mature beer markets and rapidly developing regions.

High Production Costs and Technical Complexity

Producing non-alcoholic beer involves additional processing stages compared with conventional brewing, which is increasing operational expenditure. Alcohol removal technologies such as vacuum distillation and membrane filtration require specialized equipment and significant energy input. The European Brewery Convention (EBC) reports that these processes are raising manufacturing costs by roughly 20% to 40% compared with standard beer production. These technical requirements are making alcohol-free brewing more capital intensive, which is affecting pricing strategies and profit margins across the industry.

Cost pressure is also erecting significant barriers for small and medium-sized breweries that lack large-scale production infrastructure. Craft producers often face difficulty investing in dedicated alcohol removal systems while maintaining competitive retail prices. As a result, non-alcoholic beer frequently enters the market at a higher price than conventional beer despite lower alcohol content. This pricing imbalance is limiting consumer adoption in price-sensitive regions such as Latin America and Southeast Asia. To address this constraint, breweries are forming contract production partnerships and using shared brewing facilities to reduce capital investment and improve manufacturing efficiency.

Regulatory Classification and Labeling Complexity

Regulatory definitions for non-alcoholic beer differ significantly across jurisdictions, which is creating compliance complexity for global producers. In the United States, beverages containing up to 0.5% alcohol by volume (ABV) qualify for non-alcoholic labeling, while several Middle Eastern markets require certification at 0.0% ABV. In parts of the European Union (EU), the European Commission (EC) permits the alcohol-free designation only when alcohol content remains below 0.05% ABV. These regulatory thresholds are shaping formulation standards and influencing product classification across international markets.

Such regulatory divergence is requiring breweries to adjust recipes, labeling practices, and certification processes for each export destination. Compliance costs are increasing when producers are entering regions with strict religious or cultural restrictions related to alcohol consumption. Marketing regulations are also limiting promotional claims associated with health or wellness attributes, which is narrowing communication strategies for beverage companies. These regulatory conditions are raising administrative expenses and slowing international expansion, particularly for small and medium-sized breweries with limited regulatory resources.

Expansion of Non-Alcoholic Beer in Emerging Urban Markets

Rapid urbanization across Asia Pacific and Latin America is expanding the demand potential for non-alcoholic beer. The United Nations Department of Economic and Social Affairs (UN DESA) estimates that about 68% of the global population will reside in urban areas by 2050, with significant growth occurring in emerging economies. Urban consumers are adopting global lifestyle patterns that emphasize moderated alcohol intake and wellness-focused beverage choices. This shift is encouraging breweries to position alcohol-free beer as a practical alternative within social drinking occasions.

In markets such as India, Thailand, and Brazil, alcohol regulations often restrict advertising or consumption in certain public settings. Non-alcoholic beer is allowing consumers to participate in social gatherings without breaching regulatory limitations. These regions also present strong growth potential because per capita alcohol consumption remains lower than levels observed in Europe and North America. Multinational brewers are expanding local production facilities and distribution partnerships to strengthen market access. As these supply networks are expanding, alcohol-free beer is gaining a larger share within regional beer portfolios.

Functional and Premium Non-Alcoholic Beer Innovation

Product innovation is creating premium segments within the non-alcoholic beer category as breweries incorporate functional ingredients such as electrolytes, adaptogens, and vitamins. These formulations are positioning alcohol-free beer as a wellness-oriented beverage that appeals to athletes and health-conscious consumers seeking alternatives to conventional sports drinks. The International Food Information Council (IFIC) reports that more than 52% of consumers globally are seeking functional beverages that support hydration and recovery, which is shaping product development strategies within the brewing industry.

Breweries are responding by introducing isotonic alcohol-free beers designed for post-exercise consumption and active lifestyles. Craft producers are also developing premium variants featuring specialty hops, barrel aging, and experimental fermentation processes to enhance flavor complexity. These innovations are enabling manufacturers to differentiate their portfolios and justify higher price positioning within the beverage market. As product quality and consumer awareness are improving, premium alcohol-free beer is generating incremental revenue opportunities and strengthening the strategic value of this category for global brewers.

Category-Wise Analysis

Product Type Insights

Lager is poised to hold the leading position in 2026 with an estimated 52% of the non-alcoholic beer market revenue share. This leadership is rooted in strong consumer familiarity with lager profiles and the technical compatibility of lager fermentation with alcohol removal processes. Lager brewing typically produces a clean and balanced flavor profile, which allows brewers to preserve taste quality during dealcoholization. Major producers such as Heineken N.V. and Anheuser-Busch InBev SA/NV are prioritizing alcohol-free lager variants because these products replicate flagship beer offerings that consumers already recognize. This strategy is helping breweries maintain brand continuity while addressing shifting consumption patterns toward moderated alcohol intake.

Ale-style non-alcoholic beer is expected to register the highest CAGR of approximately 8.5% between 2026 and 2033. Demand for this variant is increasing among consumers who are seeking distinctive flavor profiles associated with craft brewing traditions. Breweries are introducing alcohol-free adaptations of well-known ale styles such as IPA and pale ale to replicate the aromatic intensity and bitterness that hop-forward beers typically deliver. These offerings are appealing to experienced beer drinkers who are reducing alcohol intake but still expecting complexity in taste and aroma. This shift is encouraging brewers to diversify their portfolios and address evolving consumer expectations within the premium beverage segment. Producers are also investing in advanced fermentation processes and yeast strain optimization to retain volatile hop compounds while limiting alcohol formation during brewing. These innovations are allowing brewers to maintain the sensory depth of traditional ale products while achieving regulatory compliance for alcohol-free labeling.

Distribution Channel Insights

Supermarkets and hypermarkets are anticipated to capture about 48% of the non-alcoholic beer market share in 2026. Large retail chains are providing extensive shelf space and efficient supply networks that enable breweries to reach a broad consumer base. These retail environments are supporting high product visibility because alcohol-free beer is often placed near conventional beer categories, which encourages trial purchases among regular beer consumers. Retailers are also allocating dedicated sections for alcohol-free beverages as consumer demand for moderated drinking options is strengthening. This retail strategy is improving product discoverability while reinforcing the category’s presence within mainstream beverage aisles. Retail chains are simultaneously expanding private label portfolios in the alcohol-free segment to address price-sensitive consumers and increase category accessibility.

Online retail is slated to grow the fastest at an estimated CAGR of 11.2% during the 2026-2033 forecast period. Digital commerce platforms are enabling breweries to expand market reach without relying exclusively on conventional retail networks. Online grocery services and direct-to-consumer websites are allowing producers to sell alcohol-free beer directly to households, which is improving accessibility and reducing intermediary costs. Subscription-based beverage programs are also attracting consumers who prefer scheduled home delivery and curated product selections. Digital channels are proving particularly valuable for small and independent breweries that have limited access to large retail distribution networks. Online platforms are also providing national and international visibility for niche brands, which is strengthening competitive diversity within the market.

Regional Insights

North America Non-Alcoholic Beer Market Trends

North America is likely to account for an approximate 26% of the non-alcoholic beer market value in 2026, and the market here is projected to expand at a steady CAGR between 2026 and 2033. Demand is rising as consumers across the United States and Canada are prioritizing healthier lifestyles and moderated alcohol intake. The United States is serving as the primary revenue contributor because of strong interest in craft alcohol-free beer and functional beverage alternatives. Breweries are launching new product lines that target fitness-focused consumers and individuals seeking beverages with reduced alcohol exposure while maintaining traditional beer flavors.

Regulatory developments are also shaping regional market expansion. Several United States jurisdictions are revising distribution frameworks to allow alcohol-free beer sales through a wider range of retail outlets such as grocery stores and convenience retailers. This regulatory flexibility is increasing consumer accessibility and encouraging product experimentation within the beverage sector. Investment activity is also intensifying as venture capital firms are funding startups that specialize in alcohol-free fermentation technology and advanced brewing methods. These investments are enabling new producers to introduce premium alcohol-free beer variants and compete with multinational brewing companies across specialized market niches.

Europe Non-Alcoholic Beer Market Trends

Europe is forecast to become the largest regional market for non-alcoholic beer with an estimated global share of about 38% in 2026, showcasing a moderate CAGR through 2033. Germany, Spain, and the Netherlands are maintaining strong consumption levels because alcohol-free beer has long been integrated into mainstream drinking culture. Industry data indicates that alcohol-free variants already represent a notable share of total beer sales in several European markets. This established consumer familiarity is enabling brewers to scale production and introduce new alcohol-free formulations across both premium and mainstream beer categories. Regulatory frameworks promoting responsible alcohol consumption are also shaping market expansion across the region.

A growing number of national governments within the EU are enforcing strict drink-driving regulations and higher alcohol taxation policies, which are encouraging consumers to select alcohol-free beverage options during social occasions. Large brewing companies headquartered in Europe are investing in advanced dealcoholization processes and modern fermentation techniques to improve product quality and expand export capabilities. These strategic investments are strengthening manufacturing capacity and enabling European brewers to supply growing international demand for alcohol-free beer products across emerging markets.

Asia Pacific Non-Alcoholic Beer Market Trends

The market for non-alcoholic beer in Asia Pacific is expected to register the highest 2026-2033 CAGR at an estimated 9.2%. Rapid urban expansion and rising disposable income levels are increasing consumer spending on premium beverage categories. Countries such as Japan and Australia already possess well-developed alcohol-free beer markets with established consumer acceptance. Emerging economies such as India and China are presenting strong growth potential as urban middle-class populations are expanding and younger consumers are adopting moderated drinking behaviors. Cultural norms and regulatory structures are also supporting adoption across several Asian markets.

In several countries across Asia, alcohol consumption is restricted in certain public environments or during religious observances, which is encouraging the demand for alcohol-free alternatives that allow participation in social occasions without breaching cultural expectations. Multinational brewing companies are investing in regional production facilities and localized supply chains to reduce import dependency and improve distribution efficiency. These investments are strengthening manufacturing capacity and enabling producers to respond more effectively to rising consumer demand across the highly diverse Asia Pacific market.

Competitive Landscape

The global non-alcoholic beer market structure is exhibiting moderate concentration, with multinational brewers controlling a large share of industry revenue. The five largest companies – Anheuser-Busch InBev, Heineken, Carlsberg, Asahi Group, and Kirin Holdings –collectively control approximately 48% of global sales, supported by their extensive distribution infrastructure, established brand portfolios, and strong research and development capabilities. These firms are leveraging existing brewing expertise and global supply networks to scale alcohol-free production while maintaining operational efficiency. Their financial resources are enabling sustained investment in product development, technology upgrades, and international market expansion.

Leading brewers are introducing alcohol-free variants of flagship brands to preserve consumer loyalty while addressing evolving drinking preferences. Craft breweries are also entering the category with premium offerings that emphasize distinctive flavor profiles and artisanal brewing practices. Competitive intensity is increasing as beverage companies from adjacent sectors such as soft drinks and functional beverages are developing beer-inspired alcohol-free products aimed at wellness-focused consumers. In response, brewers are strengthening marketing strategies that position alcohol-free beer as a lifestyle beverage suitable for social occasions, fitness-oriented consumption, and responsible drinking environments.

Key Industry Developments

- In March 2026, Heineken launched Heineken 0.0 Ultimate, a new alcohol-free beer formulated with zero alcohol, zero calories, and zero sugar, targeting consumers seeking healthier beverage options without compromising taste. The product will debut in markets such as the United States, the Netherlands, and Poland, expanding the company’s alcohol-free portfolio amid rising demand for mindful drinking alternatives.

- In February 2026, AB InBev India unveiled Corona Cero, the zero-alcohol variant of its Corona brand, priced at INR 120 and distributed through modern retail outlets, e-commerce platforms, and select on-premise venues across the country. The launch expands the company’s alcohol-free portfolio as India’s non-alcoholic beer segment has recorded around 25% annual growth, reflecting rising demand for mindful drinking options.

- In September 2025, Ironhill Brewery brought out its first non-alcoholic beer, Zero Gravity AF, marking the entry of India’s largest microbrewery chain into the alcohol-free segment. The wheat beer is brewed to deliver the sensory profile of traditional craft beer with citrus and tropical notes while containing minimal alcohol. The product uses a specialized yeast strain that naturally stops fermentation at around 0.5% ABV, preserving aroma, body, and flavor without dilution.

Companies Covered in Non-Alcoholic Beer Market

- Anheuser-Busch InBev SA/NV

- Heineken N.V.

- Carlsberg A/S

- Asahi Group Holdings, Ltd.

- Kirin Holdings Company, Limited

- Molson Coors Beverage Company

- Diageo plc

- Suntory Holdings Limited

- Athletic Brewing Company LLC

- Big Drop Brewing Company Ltd

- Clausthaler (Radeberger Gruppe KG)

- BrewDog plc

- Erdinger Weißbräu Werner Brombach GmbH

- Krombacher Brauerei Bernhard Schadeberg GmbH

Frequently Asked Questions

The global non-alcoholic beer market is projected to reach US$ 25.5 billion in 2026.

Behavioral shift among consumers toward low- and zero-alcohol beverages while maintaining traditional beer consumption occasions and introduction of premium variants by producers that replicate established beer styles while aligning with health awareness and regulatory expectations are fueling market growth.

The market is poised to witness a CAGR of 7.5% from 2026 to 2033.

Growing adoption of dealcoholization methods such as vacuum distillation and reverse osmosis by breweries, intensification of alcohol risk awareness campaigns by national and international health bodies, prioritization of moderation and wellness-oriented consumption among young consumers, and implementation of stricter alcohol taxation policies and advertising controls by governments are opening new market opportunities.

Anheuser-Busch InBev, Heineken, Carlsberg, and Asahi Group Holdings are some of the key players in the market.