- Technology

- Motherboard Market

Motherboard Market Size, Share, and Growth Forecast, 2026 – 2033

Motherboard Market by CPU Platform (AMD, Intel, ARM-based, Others), Sales Channel (Offline Retail, Online Retail), Application (Desktop PCs, Servers, Industrial & IoT), and Regional Analysis 2026 – 2033

Motherboard Market Size and Trends Analysis

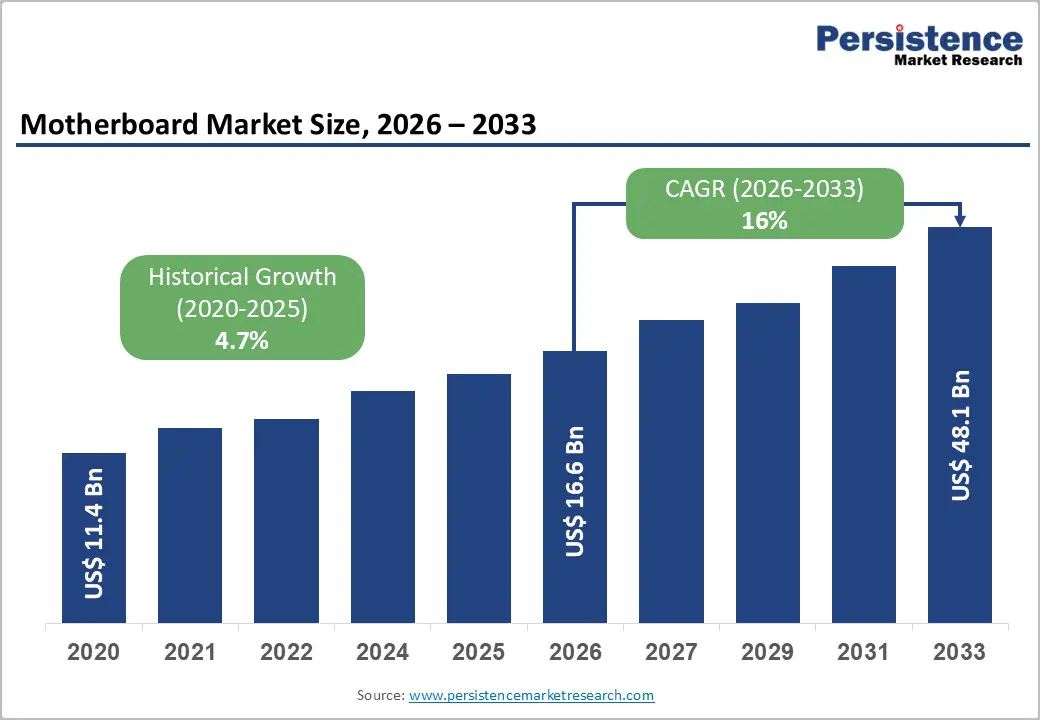

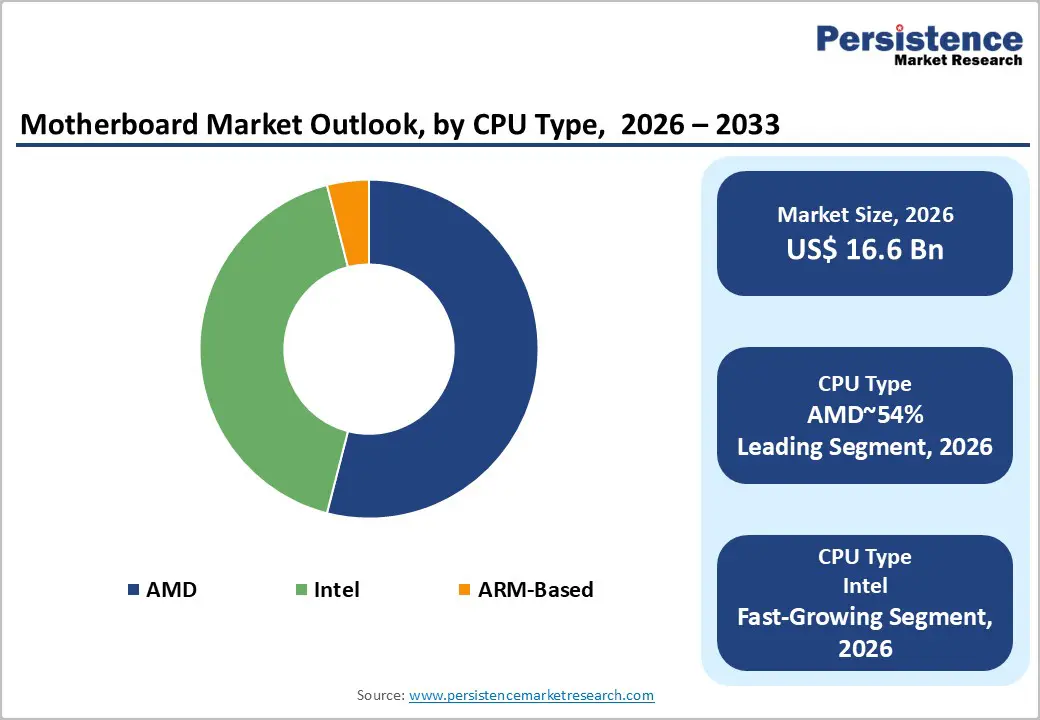

The global motherboard market size is likely to be valued at US$16.6 billion in 2026 and is expected to reach US$48.1 billion by 2033, growing at a CAGR of 16% during the forecast period from 2026 and 2033, driven by the convergence of high-performance computing (HPC) and primarily catalyzed by the mass adoption of AI-capable hardware and the "Edge AI" revolution. Growth is further sustained by a robust upgrade cycle in the consumer desktop segment, fueled by next-generation gaming requirements and the transition to DDR5 memory standards. The rising demand for high-performance computing in gaming, AI, and industrial applications, alongside AMD platform dominance and ARM-based expansions.

Key Industry Highlights:

- Leading CPU Platform: AMD is anticipated to remain the leading CPU platform in the global single-board computer and embedded computing market, holding around 54% share, as its performance-per-dollar advantage, strong multi-core architectures, and expanding ecosystem support adoption across desktop-class embedded systems and server-grade edge deployments.

- Leading Sales Channel: Offline retail is expected to continue as the dominant sales channel for motherboards, representing approximately 55% of the global market, driven by consumers’ preference for hands-on purchasing when assembling complex PC builds.

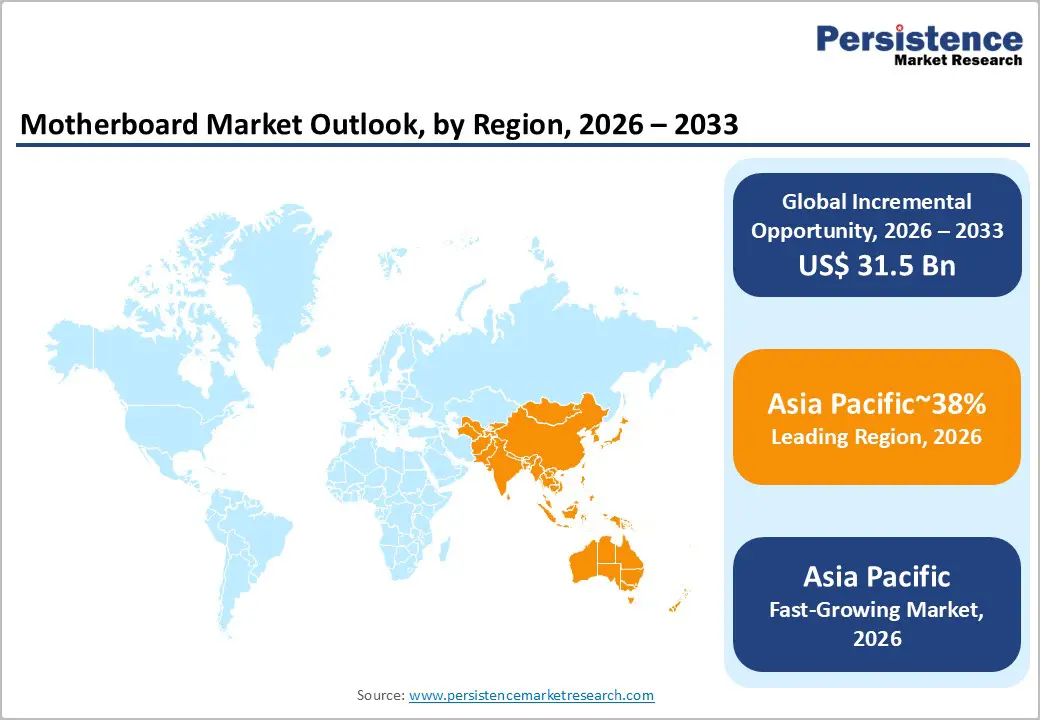

- Leading and the Fastest-growing Region: Asia Pacific is anticipated to lead the global market with approximately 38% share, supported by large-scale electronics manufacturing ecosystems, strong developer adoption, and high-volume deployment of embedded computing platforms across industrial automation and smart infrastructure projects.

| Key Insights | Details |

|---|---|

|

Motherboard Market Size (2026E) |

US$16.6 Bn |

|

Market Value Forecast (2033F) |

US$48.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

16% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Explosion of AI-Integrated Personal Computing

NPU integration forces accelerated refresh cycles across PCs, workstations, and edge devices. AI workloads require higher power delivery and tighter signal integrity constraints. Legacy motherboard designs increasingly fail under sustained AI inference demands. Power phase limitations constrain stability during mixed CPU, GPU, and NPU loads. High-speed interconnect routing imposes stricter PCB material performance thresholds. OEMs redesign platforms around higher phase-count, advanced VRM architectures. Legacy motherboards with limited phases and VRMs increasingly fail sustained on-device workloads. OEMs redesign platforms using higher phase-count networks, upgraded regulators, and advanced PCB materials.

NPU adoption increases bill-of-materials intensity across critical motherboard subsystems. Advanced PCB laminates and power ICs capture higher content per unit. Enterprises accelerate endpoint replacements to support local AI inference workloads. Thermal management complexity rises under continuous AI compute utilization profiles. Vendors differentiate through firmware optimization, stabilizing heterogeneous power draw. Hardware stack pricing increases amid shortened refresh cycles in premium segments. Collectively, the shift toward AI-native personal computing increases average selling prices across the PC hardware stack, shortens refresh intervals in performance-oriented segments, and creates a durable demand tailwind for suppliers positioned in high-reliability PCB materials, power electronics, and system-level power integrity solutions.

Surge in High-Fidelity Gaming and Esports Ecosystems

The gaming motherboard segment expands, driven by rising esports and high-fidelity demand. Market value increases reflect sustained investment in performance-centric computing platforms. Competitive gaming elevates requirements for low latency and high processing throughput. Streaming ecosystems reinforce consumer preference for premium, customizable hardware configurations. Performance-oriented builds increasingly displace mainstream, cost-optimized PC system designs. High-end gaming workloads intensify motherboard specification requirements across multiple subsystems. Vendors prioritize differentiation through feature density and premium component integration. Segment growth supports incremental pricing power across enthusiast motherboard product tiers.

Modern esports workloads necessitate advanced connectivity, storage bandwidth, and power delivery. Wi-Fi 7 and multi-gigabit Ethernet reduce competitive network latency constraints. PCIe 5.0 adoption enables higher throughput for next-generation graphics and storage. Expanded VRM phase counts stabilize sustained overclocking under peak gaming loads. DDR5 memory support improves frame stability and overall system responsiveness. Premium models concentrate flagship features targeting high-end enthusiast demand segments. Platform diversity across Intel and AMD sustains competitive vendor positioning strategies.

Barrier Analysis – Rising Bill of Materials (BOM) and Consumer Price Sensitivity

Interface transitions inflate the motherboard BOM through higher copper grades and impedance control. Advanced assembly processes increase material intensity across multilayer PCB stack configurations. Compliance with power integrity standards elevates VRM, re-timer, and connector content. Manufacturing complexity raises baseline costs even for entry-tier platform designs. Average production cost curves shift upward across mainstream motherboard portfolios. Cost inflation compresses vendor pricing headroom within highly competitive value segments. Vendors face structural margin pressure from mandatory feature adoption requirements.

Rising low-end ASPs intersect with pronounced price sensitivity across developing markets. Budget constraints extend upgrade cycles and lengthen platform replacement intervals. Consumers increasingly defer purchases or shift toward refurbished alternatives. Demand elasticity constrains unit volumes across cost-sensitive regional markets. OEMs absorb margin trade-offs to preserve competitive entry-level pricing. Pricing floors narrow the addressable base for first-time and value-tier buyers. Premium segments absorb inflation while mainstream volumes face structural growth limits.

Opportunity Analysis – Edge AI & IoT Gateway Expansion

Rising cloud operating costs accelerate enterprise migration toward localized edge computing architectures. On-device inference reduces latency, bandwidth consumption, and centralized infrastructure dependence. Edge deployments require compact motherboards optimized for constrained thermal envelopes. Mini-ITX and SBC form factors gain relevance for distributed AI gateway implementations. Embedded accelerators become essential for sustained inference at acceptable power budgets. System designers prioritize power efficiency, footprint minimization, and deployment scalability. Edge AI adoption expands the addressable demand for specialized motherboard platforms.

Pre-integrated AI SDKs lower deployment friction and shorten enterprise integration cycles. Dedicated tensor accelerators improve deterministic performance for edge inference workloads. Software-hardware co-design enhances platform stickiness within industrial IoT ecosystems. Turnkey edge platforms reduce total integration costs for system integrators. Reference designs accelerate time-to-market across vertical-specific edge deployments. Ecosystem partnerships strengthen vendor positioning within distributed AI infrastructure markets. Value capture concentrates among suppliers, enabling rapid, low-friction edge AI adoption.

Sustainable Tech Convergence

Sustainable motherboard strategies integrate circularity, energy efficiency, and bio-based material adoption principles. Green technology penetration is projected to expand gradually. Manufacturers transition from linear disposal toward orchestrated eco-technology integration models at scale. Recyclable substrates enable component recovery, reducing waste and improving materials circularity outcomes. Secondary material usage lowers virgin metal demand across soldering and copper supply. Energy-optimized designs extend component lifecycles through improved thermals and monitoring capabilities broadly. Sustainability commitments increasingly influence OEM procurement, compliance, and product differentiation strategies decisions.

E-waste management markets expand as corporate recovery mandates intensify globally across regions. Regional policies stimulate localized recycling capacity and formalized recovery infrastructure investment pipelines. High precious-metal densities elevate economic incentives for the adoption of advanced PCB reclamation technologies. AI-driven sorting improves material purity, throughput, and end-of-life recovery yields materially today. Hydrometallurgical processes reduce emissions while maximizing precious-metal extraction efficiency at an industrial scale. Robotics automation lowers labor intensity and variability across disassembly operations at scale. Converged recovery technologies strengthen circular supply chains and resilience outcomes across ecosystems.

Category–wise Analysis

CPU Platform insights

AMD is projected to lead the CPU platform segment, accounting for approximately 54% share in 2026, underpinned by a large installed base across gaming desktops, creator workstations, and enterprise refresh cycles. Adoption remains anchored by strong performance per dollar, platform longevity around the AM5 ecosystem, and predictable upgrade paths that extend motherboard lifecycles into upcoming Zen generations. Giants such as ASUS are expanding premium X870-class offerings such as the ROG Maximus X870E Hero to lock in overclocking-centric workflows, while MSI scales thermally optimized midrange designs for high-volume system integrators. This combination of mature ecosystem depth, software-optimized silicon, and repeatable upgrade economics sustains AMD’s dominance across standardized DIY and OEM deployment models.

ARM-based boards are expected to be the fastest-growing segment, driven by unmet needs for energy-efficient compute, integrated AI acceleration, and lower total cost of ownership across laptops, edge gateways, and hyperscale nodes. Growth is being catalyzed by architectural gains in Armv9-class cores, heterogeneous compute pairing with NPUs, and modular chiplet approaches that improve performance density while constraining power envelopes. Accelerating adoption is supported by maturing application compatibility on Windows and Linux, cloud-native toolchains, and converged AI stacks that reduce integration friction for first-time adopters. Qualcomm is scaling Windows on ARM platforms around Snapdragon X Elite designs for thin-and-light systems, while NVIDIA advances Grace-based boards for AI-first server deployments.

Sales Channel Insights

Offline retail is projected to remain the leading sales channel for motherboards, accounting for roughly 55% of the global market share, supported by high-touch purchase behavior for complex PC builds. Physical outlets retain relevance because buyers seek hands-on validation of form factor, VRM build quality, and socket compatibility, alongside immediate technical support for BIOS flashing and assembly. Channel differentiation is shifting toward experience-led formats, including demo zones, gaming lounges, and configuration counters that compress decision cycles for premium rigs. Within this channel, ASUS is anchoring premium walk-in traffic through curated ROG experience zones featuring boards such as the X870E Hero, while Advantech sustains B2B demand via industrial-grade boards distributed through specialist resellers that bundle lifecycle support and compliance documentation.

Online e-commerce is expected to be the fastest-growing sales channel, propelled by AI-assisted configurators, D2C storefronts, and rapid fulfillment across Tier II and Tier III cities. Growth is further reinforced by inventory transparency during supply volatility, bank-linked promotions that compress effective pricing, and live commerce that converts influencer-led builds into instant transactions. Qualcomm-powered Windows on ARM systems and Grace-class server boards are increasingly procured through online channels for institutional buyers, while Gigabyte’s AORUS ecosystem leverages authorized e-tail partnerships to scale community-led discovery without fragmenting channel integrity.

Regional Insights

Asia Pacific Motherboard Market Trends

Asia Pacific is anticipated to remain the leading regional market for motherboards, accounting for about 38% of global demand and anchoring both volume manufacturing and design iteration. Urban digitization expands edge computing across manufacturing, automotive, and public sectors. Sustainability mandates influence procurement toward efficient layouts and recyclable substrates. Hardware security requirements tighten across regulated industry deployment environments. Low-latency processing and ruggedization become baseline specifications for edge deployments. Manufacturing diversification reduces sourcing risk and improves regional assembly resilience.

Asia Pacific is also expected to be the fastest-growing regional market, underpinned by rising gaming intensity, IoT proliferation, and the decentralization of computing to the edge. India is strengthening local PCBA capacity and shortening supply lead times. Asia Pacific acts as the primary global hub for both production and consumption. ASUS ROG and MSI MPG series boards anchor the premium gaming channel, while Gigabyte AORUS and ASRock industrial lines scale adoption in performance desktops and embedded systems. Taiwan-based manufacturers alone produce approximately 90% of the world's server boards. 5G-ready boards accelerate logistics and urban infrastructure modernization programs.

North America Motherboard Market Trends

North America continues to represent a mature and highly sustainable segment of the market, driven by advanced technological infrastructure and deep integration across high-performance computing, AI, and enterprise data centers. Leading vendors such as ASUS, Gigabyte, MSI, and ASRock dominate consumer segments. Enterprise and server boards are supplied by Intel, HP, Dell, EVGA, and Supermicro. R&D ecosystems focus on multi-core optimization, thermal management, and AI system utilities. Next-generation standards such as PCIe 5.0, DDR5, and high-speed networking improve competitiveness. Partnership ecosystems strengthen resilience across enterprise and industrial deployment models.

Green design adoption supports long-term market stability and competitive differentiation. Technological depth combined with diversified vendor presence reinforces North America’s leadership. Sustainability and innovation together underpin ongoing regional prominence in the global motherboard market. Companies such as ASUS, MSI, Gigabyte, and Intel are increasingly adopting eco-conscious manufacturing processes and green design principles to meet both corporate ESG targets and operational efficiency goals. The region’s market is anchored by well-established players such as ASUS, Gigabyte, MSI, and ASRock, which dominate consumer and gaming boards, alongside Intel, HP, Dell, EVGA, and Supermicro, which provide enterprise and server-grade motherboards.

Europe Motherboard Market Trends

The Europe motherboard market is defined by a focus on sustainability, industrial reliability, and high-efficiency designs, particularly in the industrial & embedded and server segments. Industrial & embedded and server segments drive demand for long-life, high-efficiency platforms. Regional brands emphasize operational stability and eco-conscious manufacturing practices. Europe has cultivated a strong ecosystem of brands and manufacturers that emphasize long-term operational stability and eco-conscious production. Edge-AI adoption in micro-data centers drives Mini-ITX and Micro-ATX board demand.

Advanced thermal and reliability features meet deployment requirements for distributed computing nodes. Regional integration of brands, standards, and industrial focus ensures long-term market stability. The market also benefits from the rise of edge-AI deployments in micro-data centers across the U.K., Poland, and Germany, fueling demand for Mini-ITX and Micro-ATX boards with advanced thermal and reliability features. Collectively, this network of brands, standards, and industrial focus ensures Europe’s motherboard market maintains resilience, technological sophistication, and long-term sustainability.

Competitive Landscape

The global motherboard market is a high-barrier oligopoly dominated by four major players. ASUS, MSI, Gigabyte, and ASRock collectively control roughly 75% of the consumer share. ASUS leads premium segments with nearly 40% market share through its ROG ecosystem. Market dynamics are shifting toward specialized dominance across DIY, Edge-AI, and IoT sectors. AMD surpasses Intel with 54% share in the enthusiast DIY platform segment. Advantech and Kontron capture high-margin industrial, Edge-AI, and IoT deployments globally. Competitiveness increasingly relies on ecosystem lock-in and integrated AI utility platforms. Geopolitical shifts and regulatory frameworks drive production decentralization to Vietnam, Thailand, and India.

Key Industry Highlights:

- In January 2026, MSI outlined a playbook for India, which prioritized local manufacturing and Edge AI integration to become a leading premium PC brand in the region. This shift aims to align with India’s growing hardware ambitions, potentially lowering costs for premium components through domestic production.

- In September 2025, GIGABYTE launched X870E AORUS X3D motherboards for North America. Optimized for Ryzen X3D with EZ installation and Wi-Fi drivers, it simplifies builds and upgrades, boosting gaming performance and user accessibility in the region.

- In October 2024, Gigabyte launched its Z890 series motherboards, with the flagship AORUS XTREME being among the first to feature Thunderbolt 5 support. Thunderbolt 5 provides significantly higher bandwidth (up to 120Gbps), enabling faster data transfer and support for multiple high-resolution displays.

Companies Covered in Motherboard Market

- ASUS (ASUSTeK)

- MSI (Micro-Star)

- Gigabyte Technology

- Lenovo

- HP

- Dell

- SECO

- Beckhoff

- Intel

- AMD

- Colorful

- EVGA

- Sapphire

- Biostar

- SECO

Frequently Asked Questions

The motherboard market is projected to be valued at US$16.6 billion in 2026 and is expected to reach US$48.1 billion by 2033, driven by the mass adoption of AI-capable hardware and a robust upgrade cycle in consumer gaming and desktop PCs.

The integration of Neural Processing Units (NPUs) forces accelerated refresh cycles, as legacy motherboard designs fail under sustained AI inference workloads, driving OEMs to redesign platforms with advanced power delivery and materials, which increases average selling prices and creates durable demand.

The motherboard market is forecast to grow at a CAGR of 16% from 2026 to 2033, reflecting the radical transformation driven by high-performance computing and AI adoption.

Asia Pacific is the leading regional market, accounting for approximately 38% share, supported by its large-scale electronics manufacturing ecosystem, high-volume deployment in industrial automation, and strong demand from gaming and edge computing.

The motherboard market is a high-barrier oligopoly dominated by four major players: ASUS, MSI, Gigabyte, and ASRock, which collectively control roughly 75% of the consumer segment. ASUS leads the premium segment market share through its ROG ecosystem.