- Hardware & Software IT Services

- Mobile Analytics Market

Mobile Analytics Market Size, Share, and Growth Forecast 2026 - 2033

Mobile Analytics Market by Solution (Application Performance Analytics, Mobile Marketing/Advertising Analytics, In-app Analytics), by Deployment Type (On-premise, Cloud), by Industry (BFSI, Transportation & Logistics, e-Commerce & Retail, Hospitality, Media & Entertainment, Healthcare, Others), by Regional Analysis, 2026-2033

Mobile Analytics Market Size and Trend Analysis

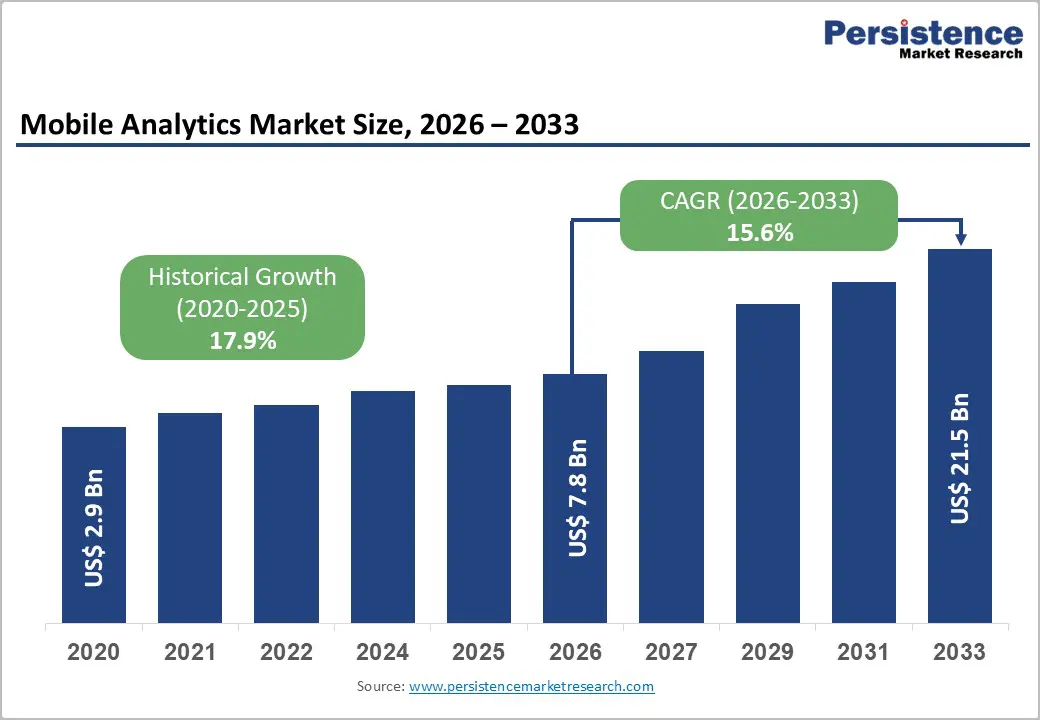

The global mobile analytics market size is expected to be valued at US$ 7.8 billion in 2026 and projected to reach US$ 21.5 billion by 2033, growing at a CAGR of 15.6% between 2026 and 2033.

This expansion reflects the central role of mobile applications, mobile web, and connected devices in how consumers bank, shop, communicate, and consume content. Enterprises are rapidly embedding advanced analytics into their mobile channels to understand user behavior, optimize engagement, and connect marketing investments to measurable outcomes. Supported by rising global smartphone penetration, 5G rollouts, and the surge in mobile advertising expenditure, mobile analytics has become a foundational capability for digital transformation strategies across sectors such as BFSI, e-Commerce & Retail, Media & Entertainment, and Healthcare.

Key Industry Highlights

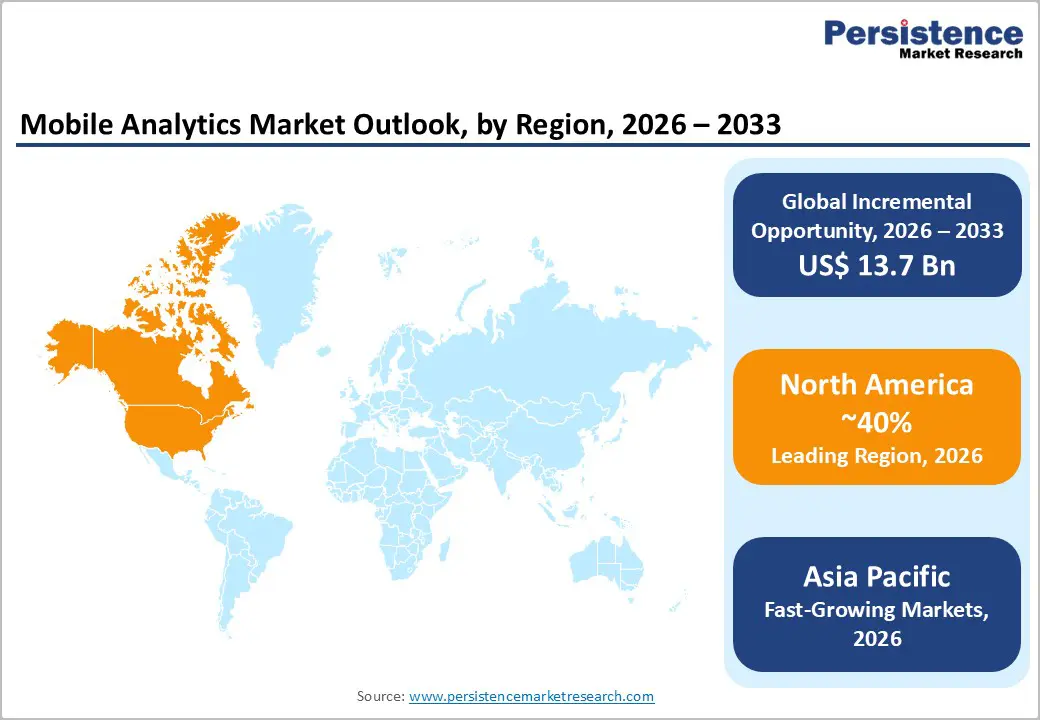

- Leading Region: North America leads the mobile analytics market with an estimated 40% revenue share in 2025, driven by strong cloud adoption, a highly developed app economy, and deep investments in mobile-first customer experience and digital advertising.

- Fastest-Growing Region: Asia Pacific is projected to be the fastest-growing region through 2033, supported by rapid smartphone penetration, digital payments expansion, and high engagement with super-apps and mobile commerce across China, India, and ASEAN economies.

- Dominance Segment: Mobile marketing and advertising analytics solutions hold around 40% market share, reflecting growing global mobile ad spend exceeding US$ 400 billion, and advertisers’ dependence on analytics to optimize campaigns and manage privacy-driven measurement challenges.

- Fastest-Growing Segment: Cloud-based mobile analytics deployments account for roughly 75% of implementations and are expanding fastest, as organizations leverage elastic infrastructure, rapid deployment, and integrated AI services from providers like Google, Microsoft, and SAP.

- Key Opportunity: AI- and ML-enabled mobile analytics represent the key opportunity, enabling predictive churn modeling, real-time personalization, and privacy-preserving attribution that help enterprises maintain performance despite signal loss and regulatory constraints.

| Global Market Attributes | Key Insights |

|---|---|

| Mobile Analytics Market Size (2026E) | US$ 7.8 billion |

| Market Value Forecast (2033F) | US$ 21.5 billion |

| Projected Growth CAGR (2026-2033) | 15.6% |

| Historical Market Growth (2020-2025) | 17.9% |

Mobile Analytics Market Dynamics

Market Growth Drivers

Explosive Growth in Mobile Usage, App Economy, and Digital Engagement

The primary growth driver for the mobile analytics market is the explosive growth in mobile device usage and app-driven engagement across all demographics. Global smartphone users surpassed 6.9 billion recently, and mobile apps now account for more than 50% of total internet traffic in many regions. App stores collectively generate annual revenues exceeding US$ 500 billion, heavily skewed toward in-app purchases and in-app advertising.

At the same time, mobile advertising spending is projected to cross US$ 400 billion globally in the mid-2020s, with more than 80% channeled into in-app formats. Brands can no longer afford to operate mobile channels without granular analytics on installs, retention, lifetime value, churn, and in-app behavior. Mobile analytics platforms help enterprises translate raw event streams into insights that drive funnel optimization, personalized engagement, and higher return on mobile marketing investments.

Shift to Data-Driven Mobile Experiences and Real-Time Application Performance Monitoring

A second major growth driver is the shift from static, content-centric mobile applications to data-driven, continuously optimized mobile experiences. Users expect mobile apps to load in under 3 seconds, maintain near-perfect uptime, and deliver contextually relevant content. Studies show that even a 1-second delay in mobile page load time can reduce conversions by 7-10%, while crash rates above 1% drastically reduce user retention.

As a result, organizations are deploying application performance analytics and mobile app performance monitoring (APM) to track latency, crash rates, API response times, and user flows in real time. Vendors such as Google LLC, Microsoft Corporation, SAP SE, and IBM Corporation are integrating advanced analytics, AI, and observability capabilities to help clients detect anomalies proactively and correlate technical performance with business KPIs. This convergence of performance monitoring, behavioral analytics, and marketing attribution capabilities substantially expands enterprise investments in mobile analytics.

Market Restraints

Data Privacy Regulations, Platform Restrictions, and Identity Signal Loss

Stringent data protection regulations such as GDPR in Europe and CCPA in California, together with platform-level changes like Apple’s App Tracking Transparency (ATT) framework and restrictions on third-party cookies, have created significant constraints for mobile analytics implementation. These rules limit the use of device identifiers and reduce deterministic user-level tracking, particularly for mobile marketing and advertising analytics. Many advertisers have seen addressable audiences and signal quality drop by more than 40% after ATT enforcement, forcing a shift to aggregated and probabilistic models. Compliance requirements increase implementation complexity and legal risk for analytics deployments, especially across jurisdictions, and some enterprises slow rollout while legal and security teams re-architect data flows.

Shortage of Analytics Talent and Implementation Complexity

A second barrier is the complexity of deploying cross-platform mobile analytics stacks and the shortage of skilled professionals capable of turning data into action. Integrating SDKs across iOS, Android, mobile web, and emerging device types, while harmonizing event taxonomies and ensuring low-latency processing at scale, remains non-trivial for many organizations. Enterprises often juggle several tools for product analytics, marketing attribution, crash reporting, and APM, creating silos and inconsistent metrics. Without strong data governance and analytical talent, organizations struggle to fully utilize advanced features such as cohort analysis, pathing, and predictive modeling, limiting return on analytics investments.

Market Opportunities

Expansion of AI-Driven Analytics, Predictive Insights, and Privacy-Preserving Measurement

One of the most significant opportunities for mobile analytics vendors and enterprises lies in integrating artificial intelligence (AI) and machine learning (ML) to deliver predictive and prescriptive insights. Rather than only describing historical user behavior, AI-enabled mobile analytics can predict churn risk, identify high-value user segments, and recommend optimal actions in real time.

For example, anomaly detection algorithms automatically flag unusual crash spikes or revenue drops, while recommendation engines power personalized offers based on real-time in-app behavior. AI-powered attribution and incremental measurement are becoming critical in mobile marketing analytics as deterministic identifiers weaken. Vendors such as Adobe, Salesforce.com, Inc., Oracle Corporation, and SAS Institute Inc. are embedding AI-driven analytics into their mobile analytics suites, opening opportunities for enterprises to automate optimization and scale experimentation.

Growth in Vertical-Specific Mobile Analytics in BFSI, Retail, and Healthcare

A second major opportunity stems from the growth of vertical-specific mobile analytics solutions tailored to industries such as BFSI, e-Commerce & Retail, and Healthcare. In banking and financial services, mobile channels now dominate customer touchpoints, with some banks reporting over 70% of customer interactions via mobile apps. Mobile analytics supports fraud detection, personalized product recommendations, and regulatory reporting.

In e-commerce and retail, mobile commerce accounts for over 70% of total digital transactions in leading markets, and retailers rely on in-app analytics to optimize product discovery, promotions, and cart recovery flows. In healthcare, the rise of telemedicine and remote patient monitoring apps has created demand for analytics to track patient engagement, adherence, and clinical outcomes. Industry-specific regulations, such as HIPAA in the U.S., encourage the development of compliant analytics solutions with strong data governance. Vendors that build deep vertical functionality and integrations will capture disproportionate value.

Category-wise Insights

Solution Analysis

Within the mobile analytics market, Mobile Marketing/Advertising Analytics is the leading solution segment, accounting for an estimated 40% share of global revenues in 2025. This dominance is closely correlated with the surge in global mobile advertising spend, which exceeded US$ 400 billion in 2024, with in-app advertising representing more than 80% of that total. Advertisers and app publishers rely on marketing analytics to attribute installs, optimize campaigns across channels, and measure return on ad spend (ROAS).

As privacy regulations and platform changes reduce deterministic identifiers, advertisers are shifting to modeled attribution and incrementality testing, further increasing dependence on advanced analytics platforms. At the same time, In-app Analytics is the fastest-growing solution subsegment for 2026-2033, expected to grow at a higher-than-average CAGR as product teams seek to understand in-app journeys, feature adoption, and retention through event-level analysis and session replay.

Deployment Type Analysis

Cloud-based deployment is the dominant and fastest-growing deployment model in the mobile analytics market, representing roughly 75% of total deployments in 2025. Cloud-native analytics platforms offered by providers such as Google LLC, Microsoft Corporation, Amazon Web Services, and SAP SE allow organizations to ingest billions of events per day with elastic scaling and pay-as-you-go economics. Cloud deployment also accelerates time-to-value by reducing the need for on-premise infrastructure, manual updates, and capacity planning.

This is especially critical for businesses with volatile traffic patterns, such as e-commerce, media streaming, and gaming. While On-premise deployments continue to hold a meaningful share, around 25%, in highly regulated sectors like government and critical financial services, most new implementations are cloud-first or hybrid architectures, where sensitive data remains on-premise but anonymized behavioral signals are processed in the cloud for advanced modeling.

Industry Analysis

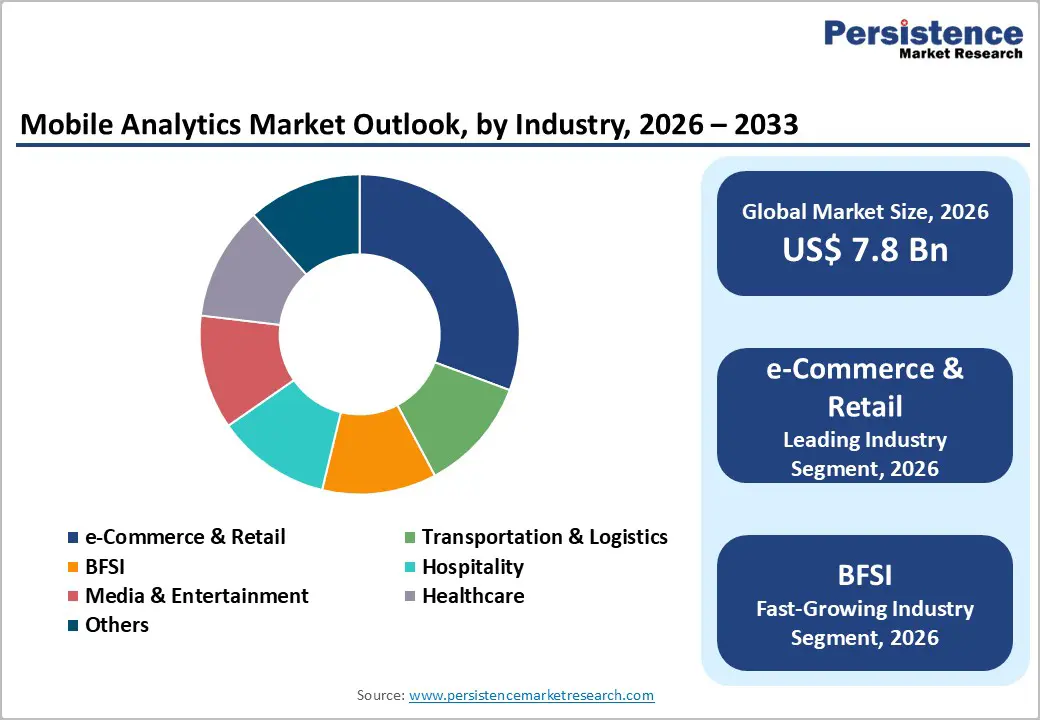

The e-Commerce & Retail segment is the leading industry vertical for mobile analytics, with an estimated 27% share of market revenues in 2025. Mobile commerce’s share of total e-commerce has surpassed 70% in markets such as China, and global consumers increasingly research, compare, and purchase products within mobile apps. Retailers leverage mobile analytics to optimize acquisition channels, personalize product recommendations, refine search and merchandising, and orchestrate omnichannel journeys connecting mobile with stores.

At the same time, the BFSI segment is among the fastest-growing industry verticals for mobile analytics during 2026-2033, as digital-only banks, insurance platforms, and investment apps scale rapidly. Banks use mobile analytics for customer segmentation, credit scoring enhancement, risk monitoring, and regulatory reporting, while also tracking critical metrics like login frequency, feature usage, and cross-sell conversion.

Regional Insights

North America Mobile Analytics Market Trends and Insights

North America is the leading regional market for mobile analytics, accounting for an estimated 40% of global revenues in 2025. The United States leads in both adoption and innovation, supported by high smartphone penetration, mature cloud infrastructure, and some of the world’s largest mobile-first enterprises across technology, retail, banking, and media. The region also hosts many of the premier analytics and cloud providers, including Google LLC, Microsoft Corporation, Adobe, and Oracle Corporation, which continuously extend their mobile analytics capabilities. Strong mobile advertising and in-app monetization ecosystems further reinforce the need for granular analytics and attribution. Regulatory frameworks such as CCPA, sector-specific rules in BFSI and Healthcare, and evolving guidance on algorithmic transparency are driving investment in privacy-preserving analytics architectures.

Europe Mobile Analytics Market Trends and Insights

Europe represents the second-largest mobile analytics market, holding approximately 27% of global revenues in 2025. Countries such as Germany, the U.K., France, and Spain are at the forefront of adoption, particularly in sectors like automotive, retail, travel, and financial services. The GDPR regulatory regime has reshaped how companies implement analytics, with stronger requirements around consent, data minimization, and user rights. This has accelerated demand for analytics platforms that support anonymization, on-device processing, and aggregated reporting while still delivering actionable insights. European enterprises are also advancing in mobile app quality and user experience, investing in application performance analytics and end-to-end observability. As 5G coverage expands and digital public services mature, mobile analytics will increasingly underpin smart city applications, mobility services, and digital identity solutions across the European Union.

Asia Pacific Mobile Analytics Market Trends and Insights

The Asia Pacific region is the fastest-growing mobile analytics market globally, expected to record the highest CAGR from 2026-2033. Rapid smartphone adoption, affordable mobile data, and the dominance of super-app ecosystems in countries such as China, India, Indonesia, and other ASEAN economies are driving extraordinary mobile engagement volumes. China’s mobile app economy alone accounts for hundreds of billions of dollars in annual gross merchandise value, and domestic vendors heavily leverage in-app analytics to drive engagement and monetization. In India, low-cost data, the expansion of UPI-based digital payments, and explosive growth in fintech and e-commerce apps are fueling adoption of mobile analytics for fraud detection, personalization, and customer lifecycle optimization. Japan, South Korea, and Singapore lead in advanced use cases such as real-time APM for high-availability financial trading platforms and media streaming services. With regional enterprises rapidly embracing cloud and AI, Asia Pacific is expected to outpace other regions in advanced mobile analytics deployments.

Competitive Landscape

The mobile analytics market exhibits a moderately consolidated structure, combining large enterprise software providers, cloud-native platforms, and niche analytics specialists competing across functionality, scale, and integration depth. Leading participants benefit from broad product portfolios that bundle mobile analytics with marketing automation, cloud infrastructure, and enterprise data platforms, creating high switching costs for customers. Smaller and mid-sized vendors compete by offering specialized capabilities such as product analytics, user behavior tracking, attribution modeling, and real-time performance monitoring.

Key competitive strategies center on embedding artificial intelligence and machine learning to enable predictive insights, automation, and personalization, while simultaneously adopting privacy-by-design frameworks to comply with evolving data protection regulations. Vendors are increasingly developing industry-specific solutions tailored to retail, media, banking, and gaming use cases to improve relevance and monetization. Strategic partnerships with cloud service providers, mobile app developers, ad-tech ecosystems, and system integrators play a critical role in expanding market reach, accelerating deployment, and positioning analytics platforms as core components of broader digital transformation initiatives.

Key Developments

- March, 2025, Segwise launched a Creative Analytics AI Agent powered by multimodal AI, enabling mobile game and app publishers to analyze ad creatives, identify performance drivers, optimize campaigns, and maximize return on ad spend across major ad networks.

- April, 2024, Adjust unveiled InSight, an AI and machine learning-powered mobile analytics solution that enables marketers to measure campaign incrementality, assess marketing actions' impact on ROI, and make privacy-first, data-driven decisions for better optimization.

Companies Covered in Mobile Analytics Market

- Teradata Corporation

- Micro Focus

- Comscore, Inc.

- Salesforce.com, Inc.

- IBM Corporation

- Adobe

- AT Internet

- Google LLC

- SAS Institute Inc.

- SAP SE

- Microsoft Corporation

- TIBCO Software Inc.

- Microstrategy Incorporated

- Oracle Corporation

- Splunk Inc.

- AppsFlyer Ltd.

- Amplitude, Inc.

- Mixpanel, Inc.

- UXCam

- AppDynamics

Frequently Asked Questions

The global mobile analytics market is expected to reach about US$ 7.8 billion by 2026.

Key drivers include rising mobile app usage, higher mobile ad spending, 5G rollout, and demand for real-time, data-driven insights.

North America leads the market, accounting for roughly 40–45% of global revenue.

AI-driven and privacy-focused mobile analytics represents the most significant growth opportunity.

Major players include Google, Adobe, Salesforce, Microsoft, IBM, Oracle, SAP, and specialized firms such as AppsFlyer, Amplitude, and Mixpanel.