- Non-food Packaging

- Metal Packaging Market

Metal Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Metal Packaging Market by Material (Aluminum, Steel, Others), Product Type (Containers & Cans, Caps & Closures, Others), Application, and Regional Analysis for 2026 - 2033

Metal Packaging Market Size and Trends Analysis

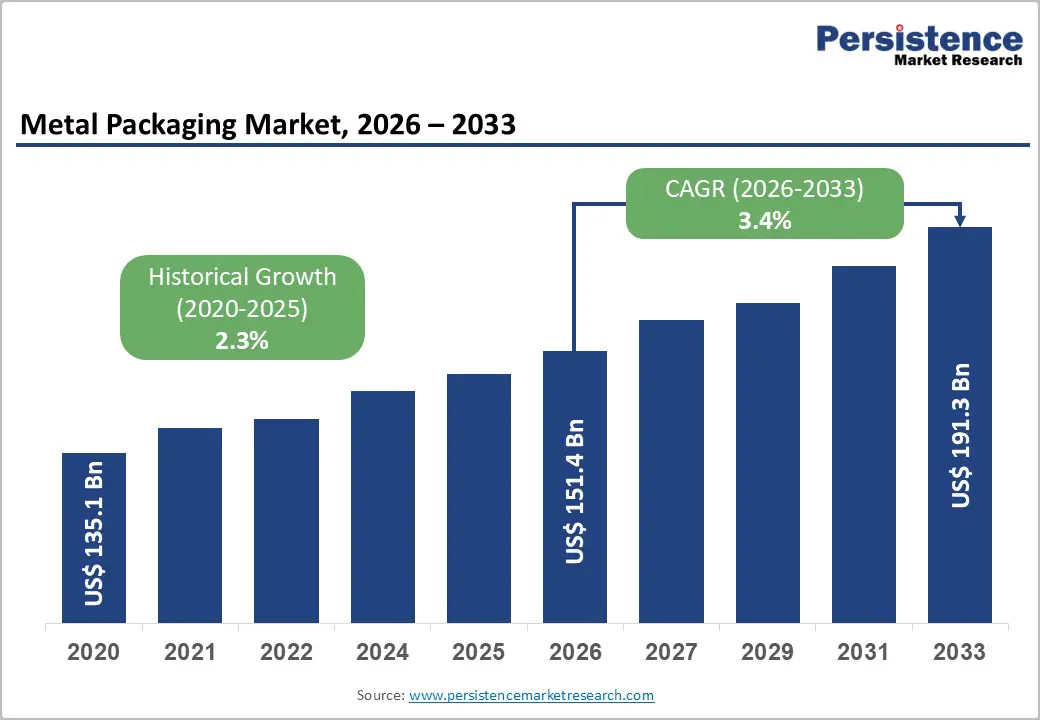

The global metal packaging market size is likely to be valued at US$151.4 billion in 2026 and is expected to reach US$191.3 billion by 2033, growing at a CAGR of 3.4% between 2026 and 2033, driven by sustained demand from food & beverage packaging, industrial chemicals, and pharmaceutical products, all of which require high-barrier and durable packaging formats. Rising substitution of plastic packaging with infinitely recyclable metal materials, particularly aluminum and steel, is reinforcing the industry’s long-term sustainability positioning.

Key Industry Highlights:

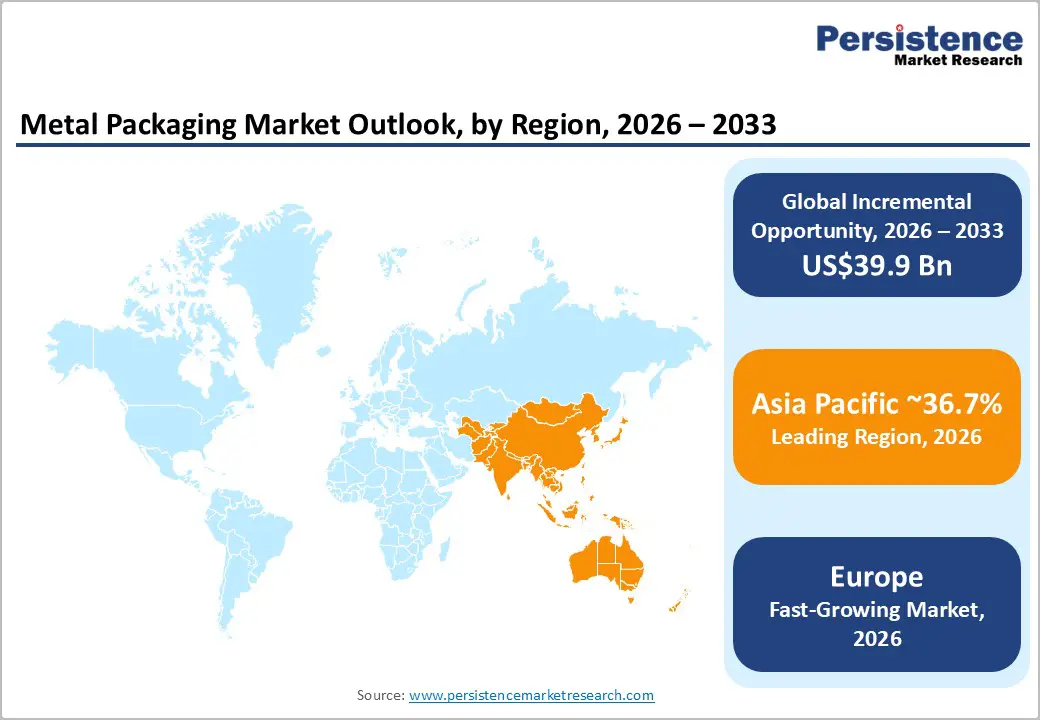

- Leading Region: Asia Pacific is projected to lead the market, accounting for approximately 36.7% of market share, supported by strong manufacturing capacity in China, Japan, and India along with rising consumption of packaged beverages and processed foods across emerging economies.

- Fastest-growing Region: Europe is projected to be the fastest-growing regional market, driven by strict sustainability regulations, high recycling rates for aluminum and steel packaging, and increasing adoption of metal cans by beverage brands transitioning toward circular packaging solutions.

- Investment Plans: Major packaging companies including Ball Corporation, Crown Holdings, and CANPACK Group are expanding aluminum can production facilities and upgrading automated manufacturing lines to support rising demand for canned beverages and sustainable packaging formats.

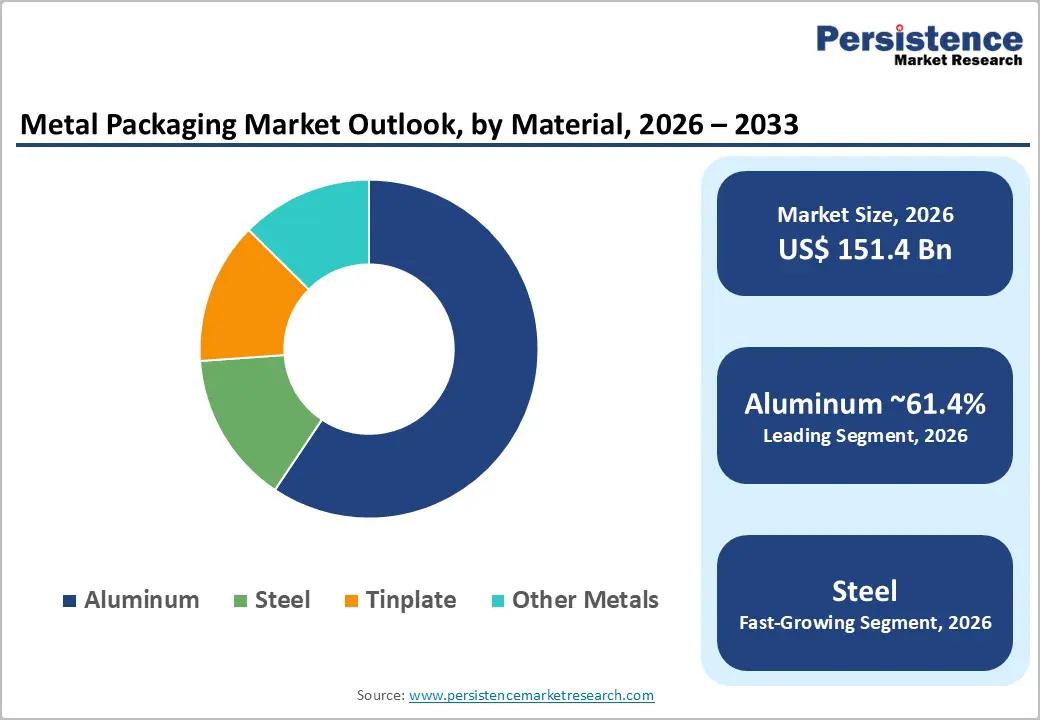

- Dominant Material: Aluminum is anticipated to represent around 61.4% of the market share, driven by lightweight properties, high recyclability, corrosion resistance, and widespread use in beverage cans and aerosol containers.

- Leading Product Type: Containers and cans are estimated to account for approximately 45.7% market share, primarily supported by strong global demand for canned beverages, processed foods, and ready-to-drink products.

| Key Insights | Details |

|---|---|

| Metal Packaging Market Size (2026E) | US$151.4 Bn |

| Market Value Forecast (2033F) | US$191.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Sustainability Regulations and Recycling Economics Driving Material Adoption

Global regulatory frameworks and corporate sustainability commitments are accelerating the transition from single-use plastics toward highly recyclable metal packaging solutions. Aluminum and steel maintain their material integrity during repeated recycling cycles, allowing manufacturers to establish closed-loop supply systems that significantly reduce environmental impact. Many governments have implemented extended producer responsibility frameworks and waste-reduction targets, encouraging consumer brands to adopt recyclable packaging alternatives. Beverage and food manufacturers increasingly prefer metal containers because they combine sustainability credentials with strong barrier protection. The long-term market implication is a structural increase in metal packaging demand, particularly in beverage cans and food containers. Companies that integrate recycling operations and secondary metal sourcing gain strategic advantages through improved cost efficiency and environmental compliance.

Growth of Ready-to-Drink Beverages and Packaged Food Consumption

The global expansion of ready-to-drink (RTD) beverages, craft beer, energy drinks, and canned cocktails continues to strengthen demand for aluminum and steel containers. Metal cans offer superior product protection, extended shelf life, and convenient portability compared with alternative packaging formats. High-speed filling lines and improved printing technologies have also enhanced branding opportunities for beverage producers, making cans a preferred format for premium beverage launches. Urbanization and rising disposable income levels are simultaneously driving consumption of processed foods and convenience meals, many of which rely on durable metal packaging. As beverage and food manufacturers diversify their product portfolios, packaging conversion from plastic and glass into aluminum cans is increasing global metal packaging penetration.

Manufacturing Investments and Regional Capacity Expansion

Major packaging manufacturers are expanding production capacity to meet rising global demand for metal containers and closures. Investments in new manufacturing facilities, production line upgrades, and automation technologies are increasing throughput and improving operational efficiency. Regional capacity expansions in emerging economies enable manufacturers to reduce transportation costs, strengthen supply chain resilience, and better serve local consumer markets. These investments also support innovation in lightweight materials and advanced coatings that enhance corrosion resistance and product shelf life. The result is improved cost competitiveness for metal packaging compared with alternative materials, supporting steady market growth over the forecast period.

Barrier Analysis - Raw Material Price Volatility

Metal packaging production depends heavily on aluminum and steel, both of which are subject to significant price fluctuations driven by global commodity markets, trade policies, and energy costs. Rapid shifts in metal prices can place pressure on packaging manufacturers that operate under fixed supply contracts with food and beverage companies. Historically, a double-digit fluctuation in aluminum prices can significantly affect converter margins unless companies have strong hedging strategies or pricing adjustment mechanisms in place. Smaller packaging companies may face greater financial exposure because they lack long-term procurement contracts or integrated recycling systems.

Regulatory Compliance and Coating Technology Costs

Food-contact regulations require packaging manufacturers to meet strict safety standards regarding coatings, linings, and material migration limits. Metal containers often require specialized internal coatings to prevent corrosion and preserve product quality. Reformulating these coatings to meet evolving regulatory requirements involves extensive testing, certification processes, and research investment. Compliance costs can raise production expenses, particularly for smaller manufacturers that lack dedicated research facilities. These regulatory challenges may slow the adoption of new packaging technologies and create entry barriers for smaller converters attempting to compete in high-value packaging segments.

Opportunity Analysis - Emerging Market Expansion and Urban Consumption Growth

Developing economies across Asia, Latin America, and Africa present substantial opportunities for metal packaging manufacturers. Rapid urbanization, growing middle-class populations, and expanding retail infrastructure are increasing demand for packaged beverages and processed foods. Local production facilities allow companies to reduce transportation costs while securing supply contracts with regional beverage and food producers. Strategic partnerships and joint ventures with local manufacturers can help international companies expand market presence and access high-growth consumer markets.

Premium Packaging and Value-Added Design Capabilities

Consumer brands increasingly view packaging as a key component of product differentiation. Advanced metal decoration techniques such as embossing, matte finishes, and digitally printed designs enable companies to create distinctive packaging that enhances brand visibility. Integration of smart packaging technologies, including QR codes and product traceability systems, further strengthens marketing capabilities. Packaging suppliers that offer design, finishing, and branding services alongside manufacturing can capture higher margins while building stronger relationships with consumer product companies.

Category-wise Analysis

Material Insights

Aluminum is anticipated to account for approximately 61.4% of the market share in 2026, making it the dominant material segment. The material’s leadership is primarily driven by its lightweight structure, excellent corrosion resistance, and strong barrier protection for beverages and food products. Aluminum cans are extensively used in the beverage industry because they preserve product freshness while allowing efficient high-speed filling, stacking, and transportation. Another advantage is aluminum’s exceptional recyclability, which allows it to be reused repeatedly without losing its structural integrity.

Recycling aluminum also consumes significantly less energy compared with primary metal production, making it attractive for companies pursuing sustainability objectives and circular economy goals. The dominance of aluminum is particularly evident in the carbonated beverage and energy drink industries, where aluminum cans are the preferred packaging format due to their portability and shelf stability. For instance, major global beverage brands such as Coca-Cola, PepsiCo, and Red Bull widely utilize aluminum cans for flagship products to improve logistics efficiency and support recyclability targets. Aluminum is also commonly used in aerosol packaging for personal care products, including deodorants and hair sprays, as well as in lightweight trays for ready-to-eat meals.

Steel is anticipated to be the fastest-growing material segment in the market. Steel containers offer superior strength, rigidity, and durability, making them particularly suitable for industrial packaging applications such as chemical drums, paint containers, and large storage tins. In the food sector, steel cans provide excellent barrier protection and mechanical strength, allowing packaged goods to withstand long transportation cycles and extended storage conditions without compromising product quality.

Steel packaging is widely used in canned food products such as vegetables, soups, and seafood, where durability and long shelf life are critical. For example, many global food brands package canned tuna, tomato products, and ready-to-cook soups in steel cans to maintain product safety and freshness. In industrial markets, steel drums are commonly used for lubricants, solvents, and construction chemicals due to their ability to safely store hazardous or heavy materials. Advances in lightweight steel technology, improved corrosion-resistant coatings, and enhanced internal linings are expanding the range of steel packaging applications.

Product Type Insights

Containers and cans are anticipated to account for approximately 45.7% of the market share in 2026, making them the largest product segment. This segment is strongly influenced by the global beverage industry, which relies heavily on aluminum and steel cans for packaging carbonated soft drinks, energy beverages, beer, and ready-to-drink products. The popularity of canned beverages continues to grow due to convenience, portability, rapid cooling capability, and strong product protection against light and oxygen exposure.

Technological advancements in can manufacturing have also improved printing resolution, embossing capabilities, and decorative finishes, allowing beverage companies to use cans as effective branding and marketing tools. For example, beverage producers frequently launch limited-edition printed cans for seasonal campaigns or sports sponsorships, helping brands stand out on retail shelves. Automated filling and sealing technologies have reduced production costs while enabling high-speed packaging operations. In addition to beverages, metal containers are widely used in processed food packaging, including canned vegetables, soups, sauces, and seafood products, further reinforcing the segment’s dominant market share.

Caps and closures are anticipated to be the fastest-growing product segment. Demand for these components is increasing due to rising consumption of bottled beverages, pharmaceutical liquids, and specialty packaged products. Metal closures offer superior sealing performance, durability, and tamper-evident protection, ensuring product safety throughout transportation and storage. In the beverage sector, metal caps are commonly used in glass bottled beverages such as beer, carbonated soft drinks, and flavored sparkling water, where secure sealing is essential to maintain carbonation.

Pharmaceutical packaging also relies heavily on precision metal closures for syrups, injectable vials, and medicinal containers, where contamination prevention is critical. Manufacturers are continuously developing innovative closure designs that support easy opening, resealing functionality, and enhanced leak prevention. Precision engineering, improved sealing liners, and automated production technologies are enabling packaging companies to produce highly reliable closures suitable for a wide range of industries, contributing to the segment’s rapid growth.

Regional Insights

North America Metal Packaging Market Trends - Beverage Can Innovation and Recycling-Driven Demand

North America represents one of the most mature and technologically advanced markets. The U.S. dominates regional demand due to its large beverage industry, extensive food processing sector, and well-established packaging manufacturing infrastructure. Aluminum beverage cans account for a significant share of packaging consumption in the region, particularly in carbonated drinks, beer, hard seltzers, and energy beverages. The strong presence of major packaging manufacturers such as Ball Corporation, Crown Holdings, and Silgan Holdings has helped maintain a highly developed supply chain for aluminum cans, steel food containers, and specialty closures.

The increasing popularity of canned ready-to-drink beverages and craft beer has further reinforced the role of metal packaging across the U.S. beverage market. Canada and Mexico also contribute meaningfully to regional market expansion. Canada has experienced increasing demand for premium canned beverages, including craft beer and ready-to-drink cocktails, where aluminum cans offer branding flexibility and improved recyclability. Meanwhile, Mexico’s growing manufacturing sector and expanding packaged food industry have supported demand for steel drums, food cans, and aerosol containers. Strong recycling infrastructure across North America further strengthens the competitiveness of metal packaging by enabling efficient recovery of aluminum and steel. For instance, beverage companies such as Coca-Cola and PepsiCo have expanded initiatives to increase recycled aluminum content in their packaging, reinforcing the role of metal containers within circular packaging systems.

Several factors continue to support market growth across the region. High consumption of packaged beverages, continued innovation in packaging technologies, and investments in sustainable manufacturing practices all contribute to steady industry expansion. Major beverage brands have increasingly shifted certain product lines from plastic bottles to aluminum cans to improve recyclability and reduce environmental impact. For example, several beverage producers have introduced aluminum can formats for bottled water and flavored sparkling beverages, reflecting growing consumer preference for sustainable packaging.

Major packaging manufacturers are also investing heavily in production upgrades and facility expansions. Companies such as Ball Corporation and Crown Holdings have announced investments in new can manufacturing lines and modernization of existing plants in the United States and Mexico. These investments increase production capacity, improve energy efficiency, and support growing demand from beverage companies launching new canned products. The expansion of manufacturing capabilities across the region ensures stable supply for large beverage brands while strengthening North America’s role as a major hub for advanced metal packaging technology.

Europe Metal Packaging Market Trends - Sustainability Regulations and Circular Packaging Adoption

Europe represents a major market for metal packaging, characterized by strong regulatory oversight, advanced recycling systems, and high consumer demand for sustainable packaging solutions. Countries such as Germany, the United Kingdom, France, and Spain play significant roles in regional production and consumption. Europe’s focus on environmental sustainability and circular economy practices has accelerated the adoption of recyclable metal packaging materials, particularly aluminum beverage cans and steel food containers.

Germany serves as one of the leading manufacturing hubs for metal packaging in Europe, supported by a strong industrial base and advanced materials engineering capabilities. Major packaging companies such as Ardagh Group and CANPACK Group operate large production facilities in the country and supply packaging solutions to beverage and food companies across the continent. The United Kingdom has witnessed strong growth in canned craft beverages and ready-to-drink alcoholic drinks, with many independent breweries shifting from glass bottles to aluminum cans for improved portability and shelf life.

Europe’s regulatory environment strongly encourages the use of recyclable packaging materials. Policies focused on packaging waste reduction, recycling targets, and environmental sustainability encourage manufacturers and consumer brands to adopt metal packaging solutions. These policies frequently require higher recycled content and improved recovery rates, which favor aluminum and steel due to their high recyclability. Beverage companies such as Carlsberg and Heineken have introduced sustainability programs that include increasing the recycled content in aluminum cans and reducing packaging weight, further supporting metal packaging demand.

Manufacturers across Europe are also investing in advanced technologies to improve production efficiency and packaging aesthetics. Companies are introducing digital printing technologies, lightweight aluminum can designs, and advanced coating solutions that reduce environmental impact while enhancing product appearance. For example, packaging producers have expanded decorative printing capabilities for limited-edition beverage packaging, allowing brands to launch promotional campaigns using customized cans.

Asia Pacific Metal Packaging Market Trends-Rapid Urbanization and Expanding Packaged Beverage Consumption

Asia Pacific leads the market regionally, holding approximately 36.7% of the market share in 2026. Rapid economic growth, increasing urbanization, and expanding consumer markets continue to drive strong demand for packaged food and beverages across the region. As disposable incomes rise and urban lifestyles become more prevalent, consumers are increasingly purchasing convenience foods and ready-to-drink beverages that rely heavily on durable metal packaging. China remains the largest market in the region, supported by its extensive manufacturing infrastructure and massive consumer base. The country has seen strong growth in aluminum beverage cans and aerosol containers used for food, personal care, and household products.

Several global packaging companies have expanded manufacturing operations in China to serve domestic demand and regional export markets. Meanwhile, Japan maintains a mature but highly innovative packaging industry, with strong demand for premium canned beverages such as ready-to-drink coffee and specialty teas. Beverage companies in Japan frequently use advanced aluminum can designs, including resealable lids and heated beverage cans sold through vending machines.

India represents one of the fastest-growing markets in Asia Pacific due to rising disposable incomes, rapid urbanization, and expanding retail distribution networks. The growing popularity of packaged foods, energy drinks, and carbonated beverages is increasing demand for aluminum cans and steel food containers. Global beverage brands such as Coca-Cola, PepsiCo, and local beverage producers are expanding canned beverage offerings in the country, which in turn supports the growth of domestic packaging manufacturers.

Manufacturing advantages in Asia Pacific include relatively lower production costs, access to raw materials, and government initiatives that encourage industrial development. Several governments across the region are promoting local manufacturing and packaging industries through infrastructure investment and industrial incentives. As a result, many global packaging companies have established regional production hubs to serve domestic markets and export to other regions. These investments are expected to further strengthen Asia Pacific’s position as the leading global center for metal packaging production and consumption over the coming decade.

Competitive Landscape

The global metal packaging market demonstrates a moderately consolidated structure, with several multinational corporations dominating high-volume beverage can production while numerous regional manufacturers supply niche and industrial packaging products. Leading companies operate large-scale manufacturing facilities and maintain global distribution networks that allow them to serve multinational food and beverage companies. At the same time, smaller regional players focus on specialized products such as industrial drums, food cans, and customized packaging formats. This mix of large multinational producers and regional specialists creates a competitive environment characterized by both consolidation and product differentiation. Leading metal packaging companies are focusing on capacity expansion, recycling integration, lightweight material development, and premium packaging innovations to strengthen market competitiveness. Many firms are also investing in sustainable manufacturing practices and digital printing technologies to enhance product differentiation and meet evolving consumer brand requirements.

Key Industry Developments:

- In March 2025, Ball Corporation announced the formation of a joint venture with Ayna.AI for its Ball Aluminum Cup business, transferring a majority stake in the aluminum cup portfolio to the new entity. The partnership aims to accelerate innovation and expand the adoption of reusable aluminum cups as sustainable alternatives to single-use plastic packaging in foodservice and beverage markets.

Companies Covered in Metal Packaging Market

- Ball Corporation

- Crown Holdings, Inc.

- Ardagh Metal Packaging S.A.

- CANPACK S.A.

- Silgan Holdings Inc.

- Toyo Seikan Group Holdings, Ltd.

- CPMC Holdings Limited

- Kian Joo Can Factory Berhad

- Showa Aluminum Can Corporation

- Envases Universales Group

- Tata Steel Packaging

- Massilly Holding S.A.S.

- BWAY Corporation

- Nampak Limited

- Hindustan Tin Works Ltd.

- Orora Limited

Frequently Asked Questions

The global metal packaging market is estimated to be valued at US$151.4 billion in 2026.

The global metal packaging market is projected to reach US$191.3 billion by 2033.

Key trends include the growing adoption of aluminum beverage cans, increasing focus on recyclable and circular packaging materials, lightweight metal packaging innovations, and rising demand for ready-to-drink beverages and packaged foods. Companies are also investing in advanced printing technologies and automated manufacturing to enhance production efficiency.

Aluminum is the leading material segment, accounting for around 61.4% of the market share, driven by its lightweight properties, corrosion resistance, and high recyclability, particularly in beverage can production.

The metal packaging market is projected to grow at a CAGR of 3.4% between 2026 and 2033.

Some of the major companies include Ball Corporation, Crown Holdings, Ardagh Metal Packaging, Silgan Holdings, and CANPACK Group.