- Beauty & Personal Care

- Medical Specialty Bags Market

Medical Specialty Bags Market Size, Share, and Growth Forecast 2026 - 2033

Medical Specialty Bags Market by Bag Type (IV Bags, Blood Bags, Urine Collection Bags), by Material (Polypropylene, Polyethylene, Polyvinyl Chloride), by End User (Hospitals, Research Centres, Pharmaceutical Companies), by Regional Analysis, 2026 - 2033

Medical Specialty Bags Market Size and Trend Analysis

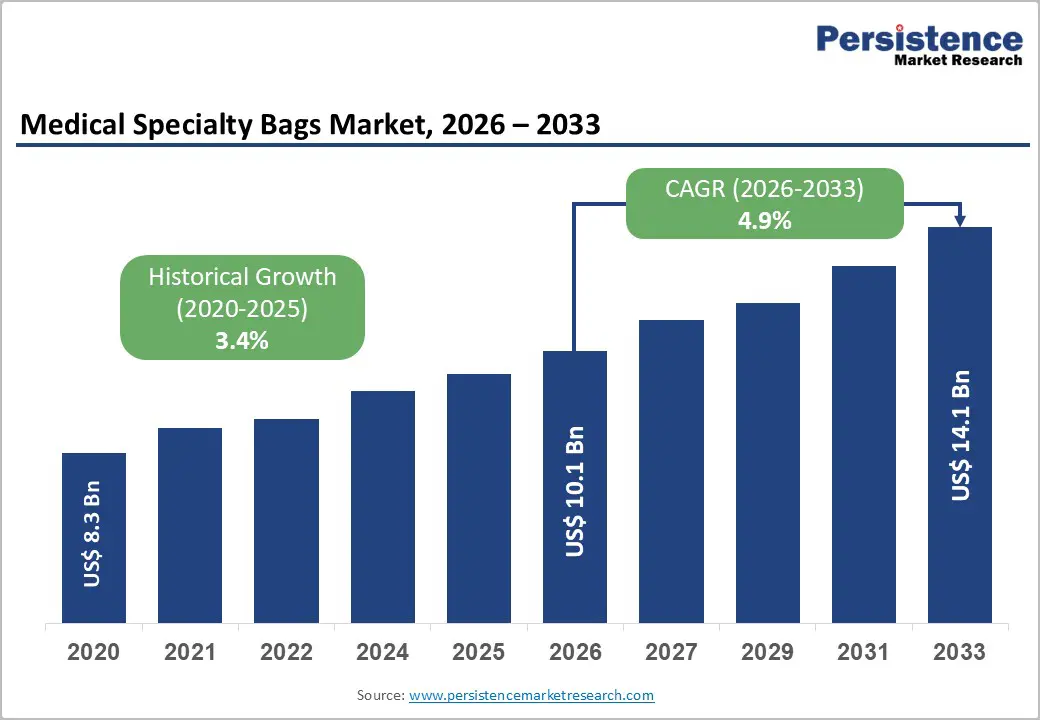

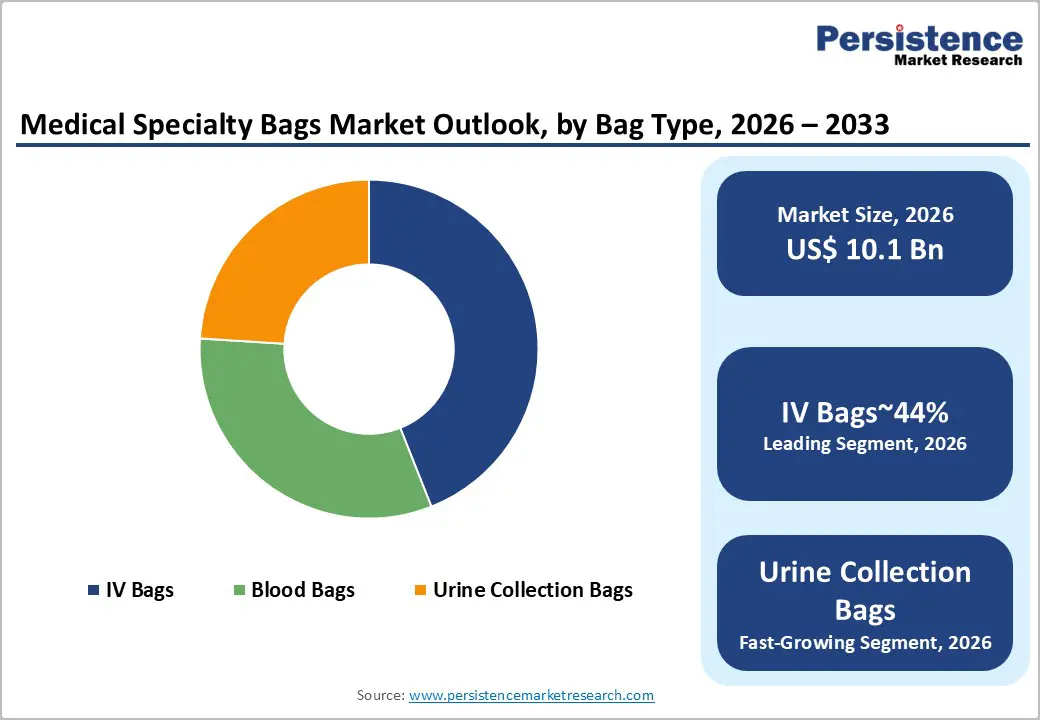

The global medical specialty bags market size is likely to be valued at US$ 10.1 billion in 2026 and is expected to reach US$ 14.1 billion by 2033, growing at a CAGR of 4.9% during the forecast period from 2026 to 2033.

The market's robust and sustained growth is fundamentally driven by the global rise in chronic disease burden, expanding hospital infrastructure across emerging economies, and accelerating demand for safe, sterile, and single-use medical fluid management solutions across all clinical settings.

Key Industry Highlights:

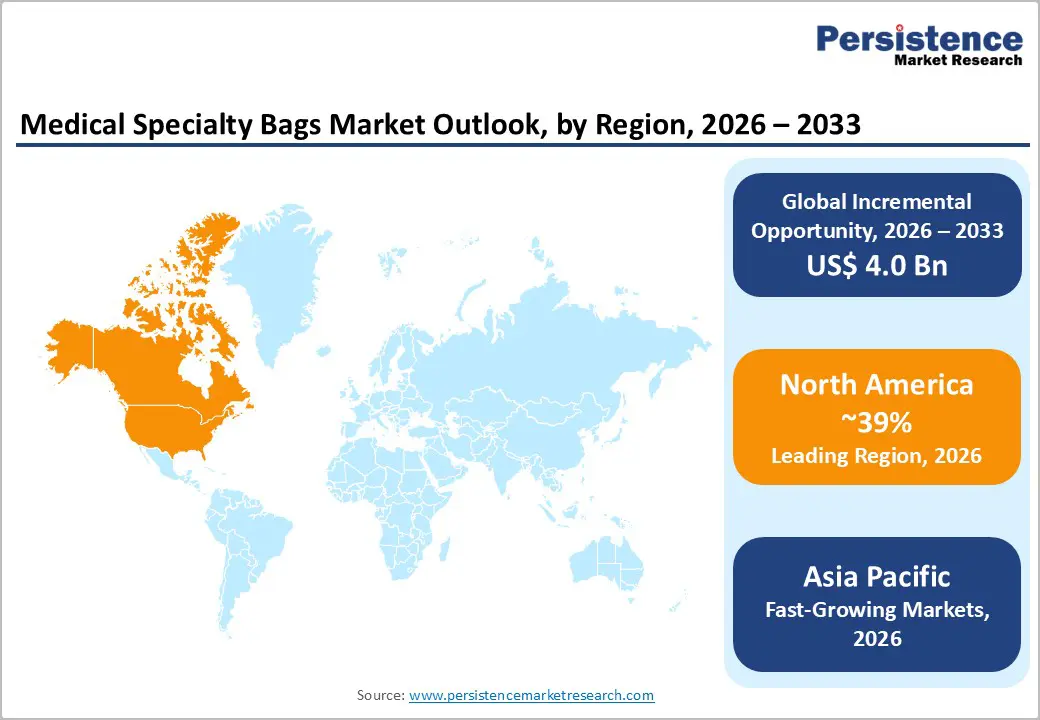

- Leading Region: North America leads the global market accounting for 39% share, underpinned by the U.S.'s world-highest per-capita healthcare expenditure of US$ 12,555 per person, the FDA's rigorous medical device regulatory framework, and dominant institutional players including Baxter International Inc. and Fresenius Medical Care AG & Co.

- Fastest-Growing Region: Asia Pacific is the fastest-growing regional market with rising CAGR of 6.1%, driven by China's 3.8 billion annual hospital visits, India's Ayushman Bharat PM-JAY program enabling over 500 million beneficiaries' hospital access, and cost-competitive polymer manufacturing hubs expanding regional specialty bag supply capacity.

- Leading Segment: IV Bags dominate the Bag Type segment with approximately 44% revenue share, anchored by their universal clinical indispensability across IV therapy, emergency care, chemotherapy, and parenteral nutrition, with 93% of all IV bag consumption occurring through single-use sterile formats.

- Fastest-Growing Segment: Polypropylene (PP) is the fastest-growing material segment, expanding at the highest CAGR within the materials category as FDA guidance and EU MDR regulations accelerate institutional transition away from DEHP-containing PVC bags toward safer, recyclable, and autoclave-compatible non-PVC polymer alternatives.

- Key Opportunity: Home infusion therapy represents the key market opportunity, with the National Home Infusion Association (NHIA) estimating 3 million U.S. patients receiving home infusion annually and CMS reimbursement expansion under the 21st Century Cures Act driving accelerating deployment of portable, extended-stability specialty IV bags in out-of-hospital settings.

| Key Insights | Details |

|---|---|

| Medical Specialty Bags Market Size (2026E) | US$ 10.1 Billion |

| Market Value Forecast (2033F) | US$ 14.1 Billion |

| Projected Growth CAGR (2026 - 2033) | 4.9% |

| Historical Market Growth (2020 - 2025) | 3.4% |

Market Dynamics

Drivers - Rising Global Burden of Chronic Diseases Expanding Demand for IV and Specialty Bag Therapies

The rapidly increasing global burden of chronic and life-threatening diseases is one of the most powerful factors driving sustained demand for medical specialty bags across all product categories. According to the International Diabetes Federation, about 537 million adults worldwide were living with diabetes in 2021, and this number is projected to reach 643 million by 2030. This rising patient population continues to generate strong clinical demand for IV fluid therapy, parenteral nutrition bags, and dialysis-related specialty bags on a large scale.

In addition, chronic kidney disease affects nearly 10% of the global population, as reported by the International Society of Nephrology, creating substantial demand for dialysis fluid bags and sterile IV medication delivery systems. Furthermore, the World Health Organization estimates that around 313 million surgical procedures are performed globally each year, requiring extensive use of specialty bags for fluid management. Rising hospital admissions worldwide further strengthen this demand, ensuring a stable and long-term procurement pipeline for specialty bag manufacturers across multiple therapeutic areas and healthcare settings.

Accelerating Shift to Single-Use, Sterile, and DEHP-Free Medical Bags: Elevating Product Premiumization

A major transformation in the global medical specialty bags market is the rapid shift toward safer, single-use, sterile, and DEHP-free medical bags. Healthcare institutions and regulators are increasingly moving away from traditional Polyvinyl Chloride bags that contain the plasticizer Di-2-ethylhexyl phthalate. The U.S. Food and Drug Administration has issued several guidance documents highlighting potential reproductive and developmental toxicity risks associated with DEHP leaching into medical fluids, particularly affecting vulnerable groups such as neonates, pediatric patients, and pregnant women.

In response, leading manufacturers are expanding product portfolios based on safer materials such as polypropylene (PP) and polyethylene (PE). North America accounted for 46.7% of the global non-PVC IV bags market in 2025, reflecting strong institutional adoption of safer materials. Companies such as Fresenius Kabi introduced DEHP-free freeflex polyolefin bags in the U.S. in April 2022, setting new competitive benchmarks. This transition toward safer materials is increasing average selling prices and improving revenue potential for manufacturers globally.

Restraints - Stringent Regulatory Requirements and Lengthy Product Approval Timelines

The global medical specialty bags market operates within a highly regulated environment, which creates significant barriers for product development and market entry. In the United States, specialty bags are generally classified as Class II or Class III medical devices under the oversight of the U.S. Food and Drug Administration. As a result, manufacturers must obtain regulatory clearance through the 510(k) premarket notification process or the more rigorous Premarket Approval (PMA) pathway, both of which require detailed documentation related to biocompatibility, sterility validation, and product performance testing.

In Europe, compliance with the EU Medical Device Regulation has further increased regulatory complexity. Manufacturers must provide extensive clinical evidence, maintain ISO 13485-certified quality management systems, and complete registration with national regulatory authorities. These approval processes can extend product launch timelines by 18 to 36 months. As a result, regulatory compliance costs remain high, particularly for smaller manufacturers, limiting new market entrants and slowing innovation and commercialization in the global specialty bags market.

Environmental and Disposal Concerns Surrounding Single-Use Plastic Medical Waste

The heavy reliance on single-use plastic materials such as PVC, polyethylene, and polypropylene in medical specialty bags has created growing environmental concerns related to healthcare waste management. Governments and healthcare organizations are increasingly scrutinizing the environmental impact of disposable medical products. In Europe, initiatives such as the European Union Single-Use Plastics Directive and the broader European Green Deal are encouraging healthcare systems to consider sustainability when procuring medical supplies.

According to the World Health Organization, nearly 85% of healthcare waste is classified as general waste, while the remaining portion is considered hazardous, including contaminated IV bags and fluid management bags that require specialized disposal methods. Additionally, stricter landfill regulations and medical waste incineration rules in countries such as Germany, France, and Japan are increasing waste treatment costs for hospitals. These rising disposal costs create indirect financial pressure on healthcare institutions and may influence purchasing decisions for specialty bags in environmentally regulated markets over time.

Opportunity - Growing Home Healthcare and Ambulatory Infusion Services Expanding Specialty Bag Deployment

The rapid expansion of home healthcare services and ambulatory infusion therapy is creating significant new growth opportunities for medical specialty bag manufacturers. In the United States, the Centers for Medicare & Medicaid Services has expanded reimbursement coverage for home infusion therapy under the 21st Century Cures Act. This policy change allows a wider range of intravenous medications, including antibiotics, immunoglobulins, and chemotherapy drugs, to be administered outside traditional hospital settings.

According to the National Home Infusion Association, nearly 3 million patients in the U.S. receive home infusion therapy each year. This growing patient base requires specialty IV bags designed with longer stability profiles, tamper-evident packaging, and simplified administration systems suitable for home use. In Europe, programs such as the NHS Hospital at Home Program are expanding community-based treatment models, further increasing demand for specialty bags outside hospitals. Manufacturers that develop patient-friendly designs with barcode tracking, longer shelf life, and easy handling features are well-positioned to capture high-value opportunities in this expanding care segment.

Pharmaceutical Compounding and Parenteral Nutrition Segment Creating High-Value Growth Pipeline

The pharmaceutical compounding sector, particularly the preparation of parenteral nutrition and complex IV admixtures, represents a high-value growth opportunity for medical specialty bag manufacturers. According to the American Society for Parenteral and Enteral Nutrition, more than 350,000 patients in the United States receive parenteral nutrition each year across critical care, oncology, neonatal, and surgical treatment settings. Increasingly, hospitals and specialty pharmacies are using multi-chamber specialty bags that keep nutrients separated until administration.

This design helps extend product shelf life, maintain nutrient stability, and significantly reduce compounding preparation errors. Evidence from the U.S. Food and Drug Administration shows that clinical settings using validated multi-chamber bag systems experience a 54% reduction in compounding errors compared with traditional single-chamber manual preparation methods. Because of these safety and efficiency benefits, pharmaceutical companies and large hospital networks are increasingly procuring advanced multi-chamber bags. These premium products command higher average selling prices, allowing manufacturers to generate stronger revenue contributions compared with standard specialty bag categories.

Category-wise Insights

By Bag Type

IV Bags dominate the global Medical Specialty Bags market by bag type, accounting for approximately 44% of the total market revenue in 2026 supported by clinical demand data from healthcare systems worldwide. Their leading position is driven by their essential and irreplaceable role across nearly every stage of patient care, from emergency resuscitation and surgical fluid management to chemotherapy administration, antibiotic infusion, and long-term parenteral nutrition.

Disposable formats are widely preferred, with single-use IV bags accounting for about 93% of the segment in 2025, reflecting strong adoption for infection-control compliance. In addition, the growing transition toward non-PVC and DEHP-free materials, supported by regulatory guidance from the U.S. Food and Drug Administration, is increasing the average selling price of IV bags and reinforcing the segment’s revenue leadership across regions during the forecast period.

By Material

Polyvinyl Chloride (PVC) remains the leading material used in the Medical Specialty Bags market, accounting for nearly 48% of the total material segment revenue in 2026. PVC continues to dominate due to its well-established manufacturing ecosystem, relatively low raw material cost, and strong functional characteristics such as flexibility and transparency that enable healthcare professionals to visually monitor fluid levels. Decades of clinical use have also helped integrate PVC-based bags into global hospital procurement standards and pharmacopoeia guidelines.

However, the material landscape is gradually evolving as Polypropylene (PP) emerges as the fastest-growing alternative. PP offers important benefits including a DEHP-free composition, better compatibility with autoclave sterilization, and improved recyclability. These features align well with increasingly strict environmental and patient-safety regulations in North America and Europe, encouraging healthcare providers to adopt PP-based medical bags.

By End-user

Hospitals represent the largest end-user segment in the global Medical Specialty Bags market, accounting for approximately 55% of total segment revenue in 2026. This dominance reflects the high concentration of clinical procedures requiring specialty bags within hospital environments. Hospitals serve as the primary settings for IV therapy administration, blood transfusions, surgical fluid management, and urological drainage care, procedures that rely heavily on medical specialty bags for safe and effective treatment.

In the Asia Pacific region, expanding public healthcare programs are also boosting hospital demand. For example, Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (PM-JAY) in India provides healthcare access to more than 500 million beneficiaries, significantly increasing hospital-based treatment volumes. In addition, research centres and pharmaceutical companies are emerging as a high-value growth segment due to rising clinical trials and advanced drug compounding activities requiring specialized multi-chamber and high-precision medical bags.

Regional Insights

North America Medical Specialty Bags Trends

North America remains the leading regional market for Medical Specialty Bags, supported by the highly advanced healthcare infrastructure of the United States and the world’s highest per-capita healthcare expenditure. According to the Centers for Medicare & Medicaid Services, healthcare spending in the U.S. reached US$12,555 per person in 2022, reflecting strong demand for advanced medical supplies and devices. Strict regulatory standards further support market growth, with the U.S. Food and Drug Administration enforcing quality frameworks such as 21 CFR Part 820, which governs manufacturing standards for medical devices.

Additional clinical guidelines issued by organizations such as the American Association of Blood Banks and the American Society of Health-System Pharmacists reinforce high-quality specifications for IV bags and blood collection systems. The expansion of home infusion therapy, supported by reimbursement provisions under the 21st Century Cures Act, is creating a growing demand channel for portable and extended-stability IV bags. Leading companies such as Baxter International Inc. and Fresenius Medical Care AG & Co. KGaA maintain strong regional market positions through vertically integrated manufacturing and direct hospital contracting networks.

Europe Medical Specialty Bags Trends

Europe represents the second-largest regional market for medical specialty bags and is among the most strictly regulated healthcare markets globally. Key countries driving demand include Germany, France, the United Kingdom, and Italy. The implementation of the EU Medical Device Regulation has significantly strengthened compliance and clinical evidence requirements for medical devices, including specialty bags. As a result, established multinational companies with strong regulatory expertise have gained a competitive advantage over smaller suppliers.

The European Directorate for the Quality of Medicines & HealthCare publishes the European Pharmacopoeia, which defines strict standards for pharmaceutical packaging materials used in IV and parenteral nutrition bags across the region. Germany leads regional consumption due to its large hospital network, which includes nearly 1,900 hospitals and over 490,000 beds, according to the Federal Statistical Office of Germany. In France, regulatory initiatives by the Agence nationale de sécurité du médicament restricting DEHP-containing medical devices in pediatric care are accelerating the shift toward polypropylene and polyethylene specialty bags.

Asia Pacific Medical Specialty Bags Trends

Asia Pacific is the fastest-growing regional market for medical specialty bags, driven by rapid healthcare infrastructure expansion, rising hospitalization rates, and a large patient population across major economies. China represents the region’s largest market, with the National Health Commission of China reporting more than 3.8 billion hospital visits in 2022. This high patient volume creates sustained demand for IV therapy bags, blood collection systems, and urological drainage products across the country’s expanding hospital network.

Government initiatives such as the Healthy China 2030 Action Plan are further strengthening healthcare infrastructure and increasing institutional procurement of specialty medical bags. India is emerging as the region’s fastest-growing market, supported by expanding private hospital networks and public health insurance programs such as Ayushman Bharat PM-JAY. ASEAN countries including Vietnam, Indonesia, and Thailand are attracting increased investment in healthcare infrastructure and medical device manufacturing. Competitive production costs and strong polymer manufacturing capabilities further position Asia Pacific as both a major demand center and supply hub for the global market.

Competitive Landscape

The global Medical Specialty Bags market demonstrates a moderately consolidated competitive structure, led by a group of large multinational healthcare companies. Major players such as Baxter International Inc., Fresenius Medical Care AG & Co. KGaA, B. Braun Medical, Terumo Corporation, and Fresenius Kabi collectively control a significant share of global revenues from IV bags and blood collection bags. Competitive advantage in this market is largely determined by leadership in material innovation, particularly the development of non-PVC and DEHP-free medical bag technologies, along with strong regulatory approvals across multiple international markets.

Companies with established hospital contracting networks and integrated cold-chain distribution systems maintain stronger relationships with healthcare providers. Emerging business strategies include outcome-based supply agreements with large hospital group purchasing organizations (GPOs) and investments in digital tracking technologies, including RFID and barcode serialization for inventory management. At the same time, regional manufacturers in China and India continue to compete aggressively on price within the standard PVC bag segment, creating margin pressure for multinational suppliers operating in high-volume product categories.

Key Developments:

- In February 2024: Baxter International Inc. introduced an expanded portfolio of advanced IV fluid bags designed to enhance drug stability and patient safety. The new range strengthens Baxter’s non-PVC offerings and supports healthcare providers’ growing preference for DEHP-free infusion solutions in North American hospitals.

- In December 2023: Fresenius Kabi highlighted strong year-end performance driven by increasing adoption of its freeflex polyolefin IV bag platform, which provides flexible, non-PVC infusion solutions. Rising hospital demand across Europe and North America contributed to expanding procurement of advanced plastic infusion bags.

- In September 2024: Terumo Corporation announced plans to expand blood bag production capacity at its Asia Pacific manufacturing facility to meet rising demand from government blood bank programs in India, Southeast Asia, and Oceania as national blood safety regulations strengthen.

Companies Covered in Medical Specialty Bags Market

- Hollister Incorporated

- B. Braun Medical Inc.

- Terumo Corporation

- Coloplast A/S

- Pall Corporation

- C.R. Bard Inc.

- Kawasumi Laboratories Inc.

- Fresenius Medical Care AG & Co. KGaA

- Baxter International Inc.

- ConvaTec Inc.

- Macopharma

- Westfield Medical Ltd.

- Fresenius Kabi AG

- ICU Medical, Inc.

- Haemonetics Corporation

- Renolit SE

- JW Life Science

Frequently Asked Questions

The global Medical Specialty Bags market is estimated to be valued at US$ 10.1 Billion in 2026 and is projected to reach US$ 14.1 Billion by 2033, registering a forecast CAGR of 4.9% during the period 2026 to 2033. The market recorded a historical growth rate of 3.4% CAGR between 2020 and 2025.

The primary demand drivers are the escalating global burden of chronic diseases, with the WHO estimating that 74% of all global deaths are attributable to non-communicable diseases, and the accelerating regulatory shift toward DEHP-free and non-PVC specialty bag formulations, driven by FDA guidance and the EU MDR 2017/745, which are simultaneously expanding clinical demand and elevating average product values.

The IV Bags segment leads the Bag Type category with approximately 44% market revenue share in 2026. Its dominance is driven by the universal clinical requirement for IV therapy across emergency, surgical, oncology, and chronic care settings, with single-use IV bags representing 93% of all IV bag consumption as confirmed by clinical procurement data, reflecting deep institutional adoption of disposable sterile formats for infection control compliance.

North America leads the global Medical Specialty Bags market, anchored by the United States' world-highest per-capita healthcare spending of US$ 12,555 per person as reported by the Centers for Medicare & Medicaid Services (CMS), a rigorous FDA regulatory framework that mandates high-specification product procurement, and the dominant market presence of multinational leaders Baxter International Inc. and Fresenius Medical Care AG & Co. KGaA.

The most significant opportunities lie in home infusion therapy expansion, with 3 million U.S. patients receiving home infusion annually and growing CMS reimbursement support under the 21st Century Cures Act, and the pharmaceutical compounding and parenteral nutrition segment, where multi-chamber bag adoption is accelerating driven by FDA evidence of 54% compounding error reduction compared to manual admixture preparation, offering manufacturers superior average selling prices and margin profiles.

The leading companies operating in the global Medical Specialty Bags market include Baxter International Inc., Fresenius Medical Care AG & Co. KGaA, Fresenius Kabi AG, B. Braun Medical Inc., Terumo Corporation, ICU Medical Inc., Haemonetics Corporation, Hollister Incorporated, ConvaTec Inc., Coloplast A/S, Macopharma, C.R. Bard Inc. (a BD company), Kawasumi Laboratories Inc., and Renolit SE, among other prominent participants across IV bags, blood bags, and urine collection bag product categories.