- Hardware & Software IT Services

- Linux OS Market

Linux OS Market Size, Share, Trends, Growth, Regional Forecasts, 2026 to 2033

Linux OS Market by Application (Servers, Desktops, Embedded Systems, Others), End-User (Individual Users, Enterprises, Government, Educational Institutions), Deployment Mode (On-Premises, Cloud-Based), and Regional Analysis for 2026-2033

Linux OS Market Share and Trends Analysis

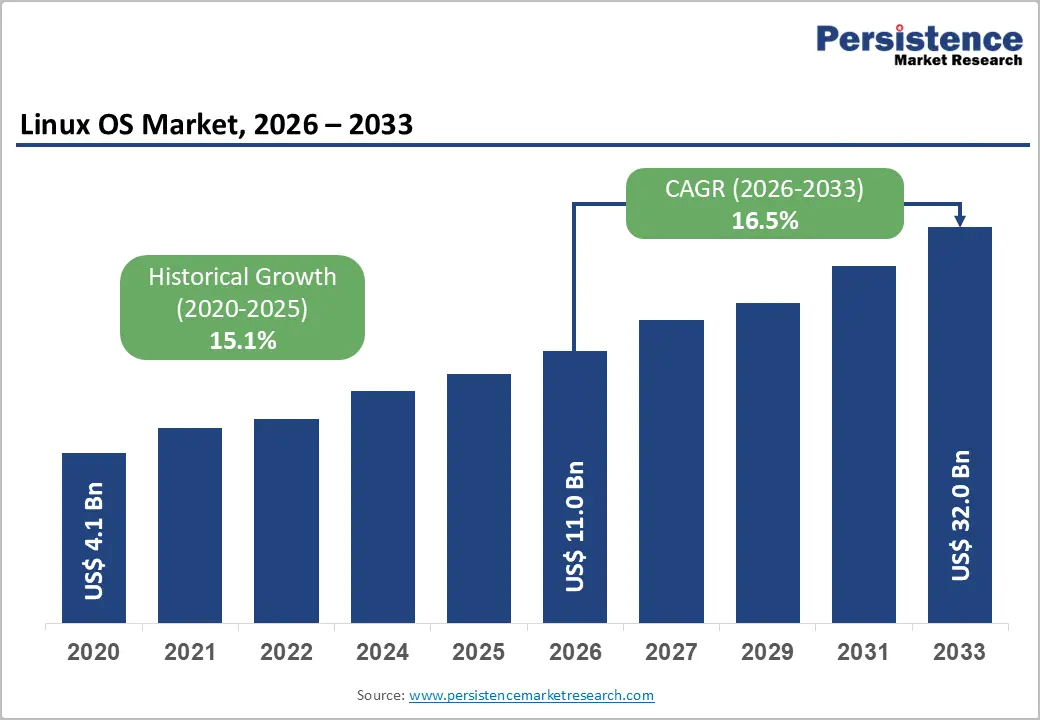

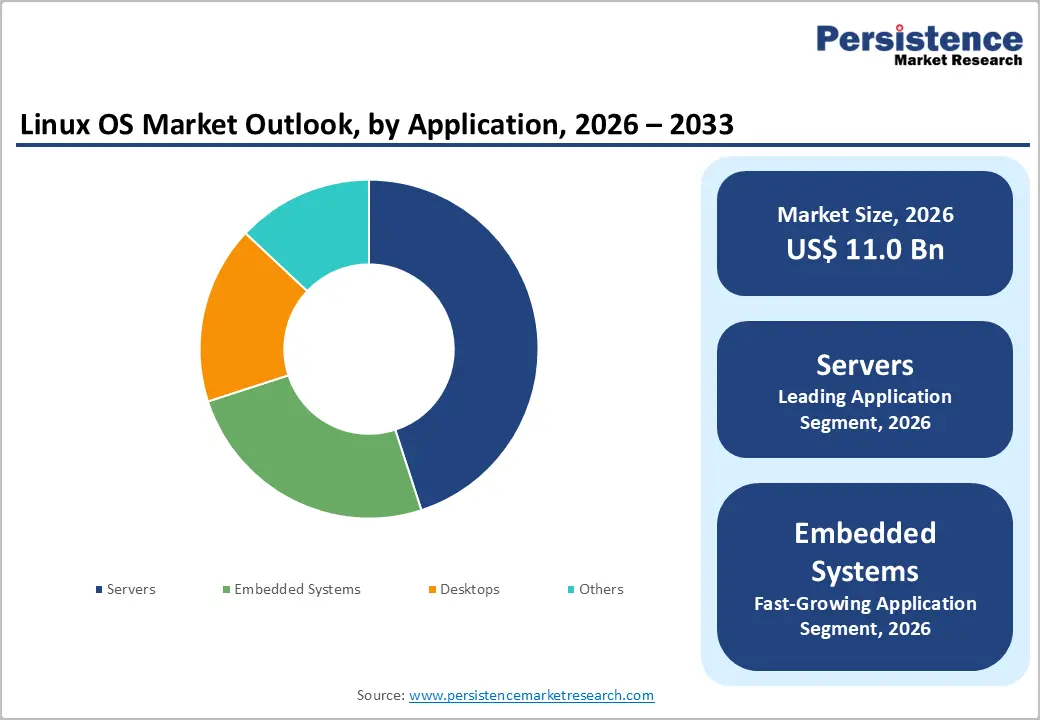

The global Linux OS market size is likely to be valued at US$ 11.0 billion in 2026, and is projected to reach US$ 32.0 billion by 2033, growing at a CAGR of 16.5% during the forecast period 2026−2033. The primary growth engines include the rapid migration of enterprise infrastructure to cloud-native and containerized environments, the proliferation of edge computing deployments, and mounting governmental and institutional mandates for open-source software adoption on grounds of digital sovereignty and cost efficiency.

Simultaneously, intensifying cybersecurity concerns are driving enterprises toward Linux's transparent, auditable code base. Emerging markets in Asia Pacific and the Middle East are contributing incremental demand, expanding the addressable market and reducing the market's historical dependence on North American revenue streams.

Key Industry Highlights

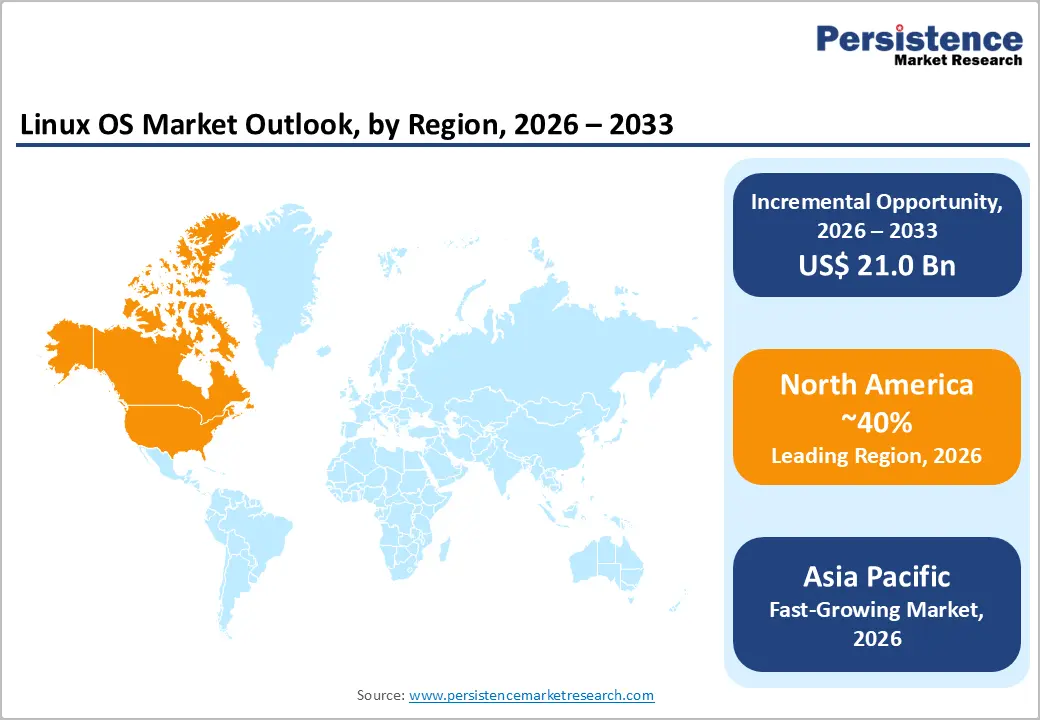

- Dominant Region: North America is expected to command a market share of about 40% in 2026, supported by advanced enterprise adoption and mature cloud infrastructure.

- Fastest-growing Market: Asia Pacific is set to be the fastest-growing regional market from 2026 to 2033, due to the rapid digitalization and expanding cloud infrastructure.

- Leading & Fastest-growing End-User: Servers are likely to lead with an estimated 45% revenue share in 2026, whereas embedded systems are expected to be the fastest-growing segment over the 2026-2033 forecast period.

- Leading & Fastest-growing Application: Enterprises are poised to command approximately 58% market revenue share in 2026, while government is likely to be the fastest-growing segment during the 2026-2033 forecast period.

- March 2026: NVIDIA released the 595 series Linux graphics driver as its latest production branch version, adding support for Vulkan extensions.

| Key Insights | Details |

|---|---|

| Linux OS Market Size (2026E) | US$ 11.0 Bn |

| Market Value Forecast (2033F) | US$ 32.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 16.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 15.1% |

DRO Analysis

Accelerated Enterprise Cloud Migration and Open-Source Adoption

Enterprise-wide cloud transformation is steadily reshaping demand for the Linux operating system (OS). Organizations are migrating critical workloads to cloud environments, and they are relying on Linux because it is flexible, scalable, and cost-efficient. Major cloud service providers such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP) are continuing to standardize their infrastructure around Linux-based systems. This shift is reinforcing Linux as the default foundation for modern application deployment. Businesses are also modernizing legacy systems, and they are adopting containerization and microservices architectures that are running most efficiently on Linux. As enterprises are accelerating digital transformation initiatives, Linux is becoming deeply embedded in infrastructure strategies, and it will have strengthened its position as a core enabler of cloud-native innovation.

Public sector adoption is also expanding the Linux ecosystem across multiple regions. Governments are prioritizing digital sovereignty, security, and regulatory compliance, and they are turning to open-source solutions to meet these goals. Linux is offering greater transparency and control, which is aligning with national data governance policies. Agencies are modernizing IT systems and are reducing dependency on proprietary platforms, which is encouraging broader Linux deployment. This trend is extending across Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS) models.

Expansion of Edge Computing, IoT, and Embedded Systems

The growth of edge computing and Internet of Things (IoT) networks is driving a significant demand for Linux-based OS. Organizations are deploying devices closer to data sources to reduce latency, and they are selecting Linux because it provides stability, efficiency, and flexibility in resource-limited environments. Specialized Linux distributions are gaining traction in industrial automation, smart manufacturing, and connected vehicle systems, where performance and reliability are critical. Real-time Linux variants such as PREEMPT_RT are enabling deterministic response times, and custom builds based on the Yocto Project are allowing companies to tailor operating systems to their specific hardware and functional requirements.

Industrial and automotive sectors are driving further Linux adoption through long-term support and predictable upgrade cycles. Enterprises are increasingly prioritizing system longevity, and Linux is providing the consistency needed to support connected devices over extended lifecycles. Embedded systems are being integrated into operational technology and safety-critical applications, and Linux is ensuring that performance, security, and compliance requirements are consistently met. As global IoT ecosystems are evolving, each new device node is creating an additional deployment opportunity for Linux. By continuously adapting to emerging hardware architectures and communication protocols, Linux is strengthening its position as the platform of choice for future-ready edge and IoT environments.

Fragmented Distribution Ecosystem and Compatibility Challenges

The wide variety of Linux distributions is creating challenges for enterprises seeking to standardize their IT environments. Organizations are managing multiple versions such as Red Hat Enterprise Linux (RHEL), Ubuntu, and Debian, and they are facing difficulties in ensuring application compatibility across these systems. Differences in package management, kernel versions, and system libraries are increasing complexity and raising the total cost of ownership (TCO) for IT teams. Enterprises in regulated industries are particularly cautious, and they are carefully evaluating how distribution fragmentation may introduce operational and compliance risks. Small and medium-sized enterprises (SMEs) are finding it difficult to allocate limited resources to manage multiple distributions, and this is slowing Linux adoption in segments where simplification is critical.

Major commercial distributions are gradually consolidating features and support models to address these challenges. Vendors are providing unified support contracts, extended lifecycle options, and compatibility layers that allow applications to run consistently across multiple distributions. Enterprises are beginning to adopt standardized distributions for core workloads, and they will have reduced integration overhead while strengthening security and operational predictability. Simplifying the Linux ecosystem is also helping IT teams deploy cloud, edge, and embedded workloads more efficiently. By fostering harmonization across distributions, Linux is positioning itself to support broader enterprise adoption, and it will have mitigated the risks that previously limited market expansion.

Talent Scarcity and Training Cost Barriers

The shortage of Linux-skilled professionals is creating a structural barrier to widespread adoption. Organizations are planning migrations from legacy systems, and they are struggling to find engineers with expertise in Linux administration, system architecture, and cloud integration. This talent gap is most pronounced in emerging regions such as Southeast Asia and Sub-Saharan Africa, where the availability of trained personnel is limited. Companies are investing in internal training and certification programs, and they are working to upskill existing IT staff to manage Linux environments. Delays in securing qualified personnel are extending migration timelines and slowing the realization of return on investment (ROI). Enterprises are also facing operational risk during the transition, as inexperienced teams may encounter system instability or configuration errors that impact critical business processes.

Corporate training and workforce development initiatives are evolving to address this challenge. Businesses are partnering with educational institutions, Linux foundations, and professional training organizations to create structured learning pathways. Employees are gaining proficiency in areas such as Linux server management, security hardening, and container orchestration, which is enabling smoother deployment and integration. As these programs are scaling, organizations will have accelerated migration schedules and improved operational resilience. The expansion of a skilled Linux workforce is strengthening confidence in enterprise adoption, and it will have increased the overall readiness of organizations to leverage Linux across cloud, edge, and hybrid IT environments.

Emerging Market Digitalization and Government IT Infrastructure Build-Out

Emerging economies in South and Southeast Asia, Latin America, and Sub-Saharan Africa are presenting a substantial growth opportunity for Linux operating systems. Governments and public institutions are accelerating digital transformation initiatives, and they are seeking cost-effective alternatives to proprietary software licensing. Linux is offering a financially sustainable solution for national IT infrastructure, enabling governments to deploy desktops, servers, and educational platforms without the high expenses associated with commercial operating systems. Public education systems are adopting Linux to expand access to technology for students and educators, and this approach is helping to reduce total IT spend while building local digital capacity.

Enterprises and institutions are also exploring Linux for small and medium-sized technology projects, which are often underfunded and require low-cost solutions. Organizations are deploying Linux to manage servers, host cloud applications, and enable software development environments efficiently. Training programs are being developed to enhance local IT workforce capabilities, and this is supporting broader adoption across public and private sectors. These initiatives are advancing, Linux will have captured a larger share of underpenetrated markets, strengthening its presence in regions with growing digital demand and expanding the total addressable market for enterprise and government deployments.

AI/ML Infrastructure and High-Performance Computing

The rapid expansion of artificial intelligence (AI) training infrastructure and high-performance computing (HPC) deployments is driving concentrated demand for enterprise Linux distributions. Data centers and research institutions are building systems that require stability, scalability, and deep hardware integration, and Linux is providing the foundation to meet these requirements. Custom Linux distributions are enabling optimized performance for machine learning (ML) workloads, including efficient utilization of graphics processing units (GPUs), tensor processing units (TPUs), and other specialized accelerators. Enterprises and national laboratories are deploying Linux to manage complex AI pipelines, and they are benefiting from reduced downtime, enhanced resource allocation, and streamlined software integration.

Cloud providers and AI-first enterprises are increasingly relying on Linux to support premium services and high-value contracts. Vendors are offering specialized distributions with integrated support for compute unified device architecture (CUDA), deep learning libraries, and hardware-specific drivers, enabling clients to maximize performance while maintaining operational control. Hyperscalers are standardizing on these Linux distributions to simplify management across large-scale clusters. The AI and HPC ecosystem is expanding, Linux is capturing a growing share of strategic enterprise workloads, and it will have become an essential enabler of innovation in AI research, commercial AI services, and next-generation computing projects.

Category-wise Analysis

Application Insights

Servers are expected to dominate by capturing approximately 45% of Linux OS market revenue share in 2026. Organizations are adopting Linux for server environments because it is delivering strong scalability across a wide range of deployments, from compact systems to large HPC clusters. Native support for virtualization technologies such as kernel-based virtual machine (KVM) and Xen hypervisor is enabling efficient resource utilization and workload isolation. Linux is also supporting a broad ecosystem of server software and middleware, and it is strengthening its position as the preferred platform for enterprise and cloud infrastructure.

Embedded systems are expected to be the fastest-growing segment over the 2026-2033 forecast period. Embedded Linux deployments are expanding across diverse applications such as automotive infotainment, advanced driver assistance systems (ADAS), industrial automation controllers, smart home devices, networking equipment, digital signage, and medical systems. Organizations are selecting Linux because it is offering flexibility, reliability, and efficient performance in resource-constrained environments. The automotive sector is emerging as a key growth area, as manufacturers are transitioning toward software-defined vehicles. These systems are requiring advanced capabilities, and Linux is supporting features such as over-the-air (OTA) update management, secure boot processes, and real-time scheduling to ensure safety, performance, and long-term system stability.

End-user Insights

Enterprises are projected to hold an estimated 58% of the Linux OS market share in 2026. These entities are dominating Linux OS adoption, and are generating the highest demand across server, cloud, and data center environments. Organizations are deploying Linux to support mission-critical workloads, enterprise applications, and scalable infrastructure. IT teams are selecting Linux because it is offering strong security, flexibility, and cost efficiency compared to proprietary systems. Enterprises are also integrating Linux into cloud-native architectures, container platforms, and DevOps pipelines, which is strengthening its role in digital transformation strategies. As businesses are expanding cloud and hybrid deployments, Linux will have remained the preferred platform for managing complex and high-performance enterprise workloads.

Government is likely to be the fastest-growing segment during the 2026-2033 forecast period. Public sector organizations are modernizing digital infrastructure, and they are choosing Linux to reduce licensing costs and improve data control. Educational institutions are implementing Linux-based systems to expand access to affordable computing resources and support open-source learning environments. Governments are also prioritizing data sovereignty and cybersecurity, and Linux is enabling greater transparency and customization. As digital inclusion initiatives are progressing, Linux adoption will have accelerated across public services and education systems, strengthening its presence in these rapidly evolving segments.

Regional Insights

North America Linux OS Market Trends

North America is set to command a significant portion of the Linux OS market value at approximately 40% in 2026, due to advanced enterprise adoption and mature cloud infrastructure. The United States is driving most of the regional demand, supported by major technology hubs, financial institutions, and federal agencies. Organizations in these sectors are deploying Linux to support scalable cloud environments, secure data processing, and high-performance computing workloads. Canada is also contributing to regional growth, with enterprises and public institutions adopting Linux to enhance digital infrastructure and reduce reliance on proprietary systems.

Cloud expansion and regulatory frameworks are shaping market dynamics in North America. Leading cloud providers such as AWS, GCP, and Microsoft Azure are building services on Linux, and they are reinforcing its role in managed and hybrid environments. Federal agencies are modernizing IT systems, and they are adopting Linux to meet compliance standards such as Federal Risk and Authorization Management Program (FedRAMP) and Cybersecurity Maturity Model Certification (CMMC). The competitive landscape is evolving as companies such as IBM through Red Hat, Canonical, and SUSE are offering enterprise-grade distributions and support services.Top of FormBottom of Form

Europe Linux OS Market Trends

Europe is establishing itself as a strong market for Linux OS, driven by strict data protection and sovereignty requirements. Organizations are prioritizing compliance with the General Data Protection Regulation (GDPR), and they are adopting Linux to maintain greater control over data and infrastructure. Governments and enterprises are reducing reliance on proprietary software vendors, and they are shifting toward open-source solutions that offer transparency and customization. Germany is leading adoption through its advanced manufacturing sector, where Linux is supporting Industry 4.0 initiatives and industrial automation systems. France is promoting Linux through national digital policies, while the United Kingdom is expanding usage across cloud-native environments within financial services.

Regions such as Spain and Nordic countries are strengthening public sector adoption through digital transformation programs. Regulatory frameworks are actively shaping Linux adoption across the region. The European Union (EU) is implementing policies such as the Cyber Resilience Act (CRA) and the Network and Information Security Directive 2 (NIS2), and these are encouraging organizations to adopt secure and auditable operating systems. The Interoperable Europe Act is requiring public institutions to evaluate open-source software during procurement processes, which is expanding opportunities for Linux deployments. Governments are also investing in sovereign cloud infrastructure, and they are supporting Linux-based platforms to ensure long-term technological independence.

Asia Pacific Linux OS Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing market for Linux OS through 2033, reinforced by rapid digitalization and expanding cloud infrastructure. Countries across the region are accelerating adoption to support enterprise transformation, public sector modernization, and technology self-reliance. China is leading regional growth through government-backed initiatives that are promoting domestic Linux distributions for use in critical infrastructure and administrative systems. India is advancing adoption through national digital programs, where telecom networks and public services are integrating Linux to improve scalability and reduce costs. Japan is strengthening its position through industrial applications, as manufacturers are deploying Linux in robotics and smart factory environments.

Southeast Asian nations such as Singapore, Indonesia, and Vietnam are also expanding Linux usage through fintech innovation and cloud platform development. Investment activity is reinforcing Linux adoption across Asia Pacific. Global cloud providers such as AWS and GCP are building large-scale data centers, and they are standardizing on Linux-based infrastructure to support regional demand. Governments are also investing in domestic software ecosystems to reduce reliance on foreign technologies, and this is encouraging the development of localized Linux distributions. Enterprises are adopting Linux to support AI, data analytics, and digital services, and they are benefiting from its flexibility and cost efficiency.

Competitive Landscape

The global Linux OS market structure is moderately fragmented, dominated by leading players such as IBM (Red Hat), Canonical (Ubuntu), SUSE, Oracle Corporation, and Amazon Web Services. These players collectively capture 35-40% of the market share. The market is operating through a dual-tier structure that is shaping competitive dynamics. A small group of enterprise-focused vendors is generating most of the revenue through subscription models, support services, and managed solutions. These companies are targeting large organizations that require stability, security, and long-term support. Alongside this, a broad ecosystem of community-driven distributions, niche providers, and system integrators is addressing specialized use cases and cost-sensitive segments. This layered structure is enabling innovation while ensuring commercial scalability, and it will have continued to support diverse enterprise and emerging workload requirements.

Key Industry Developments

- In March 2026, Kali Linux 2026.1 was released, introducing a new default theme, fresh penetration testing tools, and a Backtrack mode for legacy compatibility. This update enhances the popular Debian-based distro's visual appeal and functionality for security professionals.

- In March 2026, Oracle released Unbreakable Enterprise Kernel (UEK) 8.2 for Oracle Linux, based on Linux 6.12 LTS, featuring advancements in confidential computing with Intel TDX support for trusted execution environments, XFS online repair for higher file system reliability, lightweight guard pages for efficient memory protection, and new memory allocation profiling tools.

- In July 2025, Intel officially discontinued its high-performance Clear Linux OS, ending all updates, security patches, and maintenance, while archiving the project’s repositories in read-only mode. The move, linked to cost-cutting and restructuring, marks the end of a decade-long initiative, with users advised to migrate to actively supported Linux distributions for security and stability.

Companies Covered in Linux OS Market

- IBM (Red Hat)

- Canonical Ltd.

- SUSE LLC

- Oracle Corporation

- Amazon Web Services

- Google LLC

- Microsoft Corporation

- Wind River Systems, Inc.

- MontaVista Software, LLC

- Kylin Software Co., Ltd.

- UnionTech Software Technology Co., Ltd.

- AlmaLinux OS Foundation

- Rocky Linux

- TurboLinux, Inc.

Frequently Asked Questions

The global Linux OS market is projected to reach US$ 11.0 billion in 2026.

Cloud computing, server virtualization, and open-source cost savings are driving market growth, alongside rising demand for secure, customizable systems in enterprises.

The market is poised to witness a CAGR of 16.5% from 2026 to 2033.

Emerging markets in Asia Pacific and Latin America offer expansion via government open-source initiatives and rapid digitalization of SMEs.

IBM (Red Hat), Canonical (Ubuntu), SUSE, Oracle Corporation, and Amazon Web Services are some of the key players in the market.