- Medical Devices

- Intravaginal Device Market

Intravaginal Device Market Size, Share, and Growth Forecast, 2026 - 2033

Intravaginal Device Market by Product Type (Contraceptive Devices, Therapeutic Devices, Others), Application (Birth Control, STD, Stress Urinary Incontinence, Others), End-user (Hospitals, Clinics, Others), and Regional Analysis for 2026 - 2033

Intravaginal Device Market Size and Trends Analysis

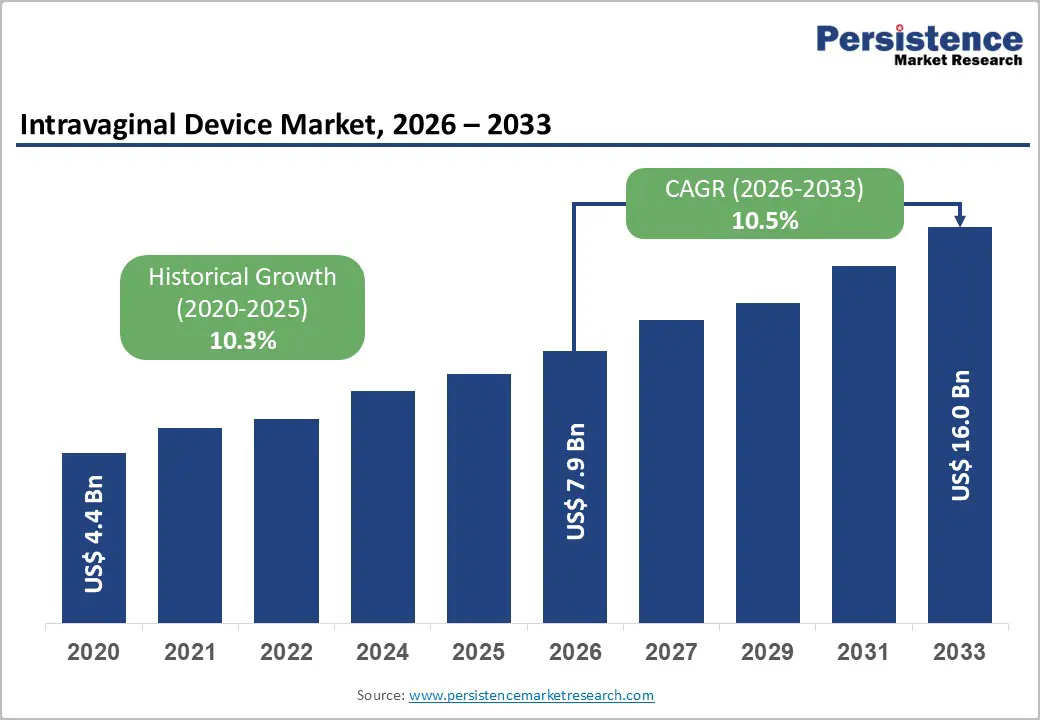

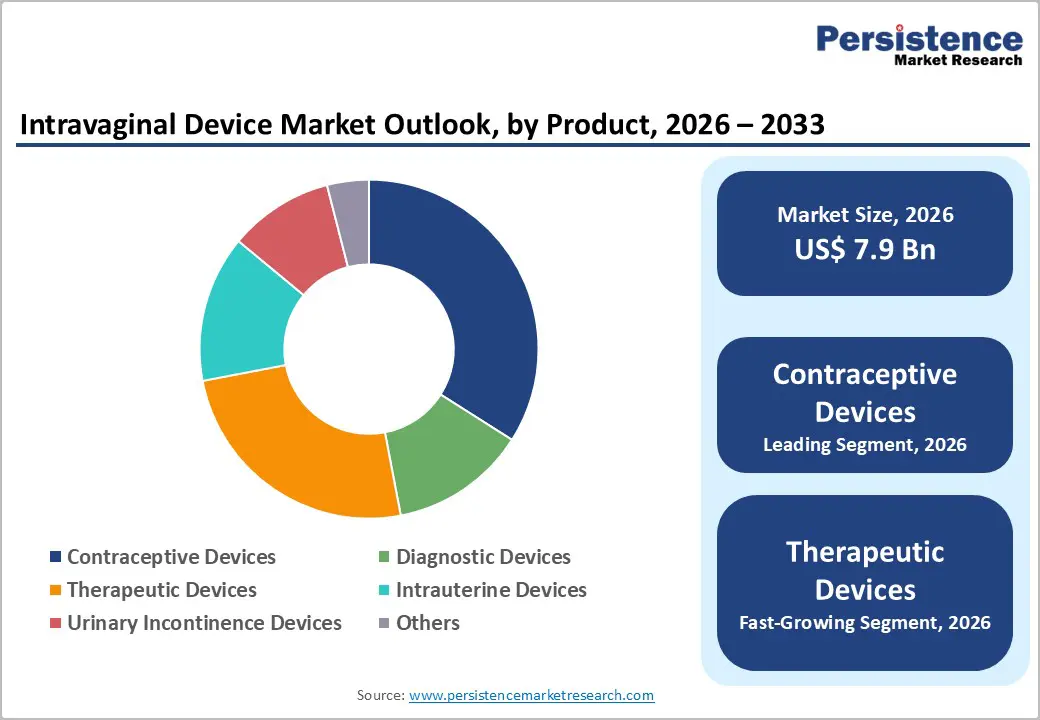

The global intravaginal device market size is likely to be valued at US$7.9 billion in 2026 and is expected to reach US$16.0 billion by 2033, growing at a CAGR of 10.5% during the forecast period from 2026 to 2033, driven by rising demand for minimally invasive solutions in women’s healthcare, encompassing contraceptive, therapeutic, and diagnostic applications.

Increasing awareness of reproductive health, coupled with expanding adoption of long-acting reversible contraceptives and advanced drug delivery systems, is fueling market expansion. The prevalence of conditions such as stress urinary incontinence and pelvic organ prolapse among aging populations is creating significant clinical demand for pessaries and supportive devices. Technological innovations, including bioresorbable materials, drug-eluting vaginal rings, and digitally integrated monitoring devices, are enhancing treatment efficacy and patient adherence. Government initiatives promoting family planning and women’s health programs, along with growing healthcare accessibility in emerging regions, are accelerating adoption.

Key Industry Highlights:

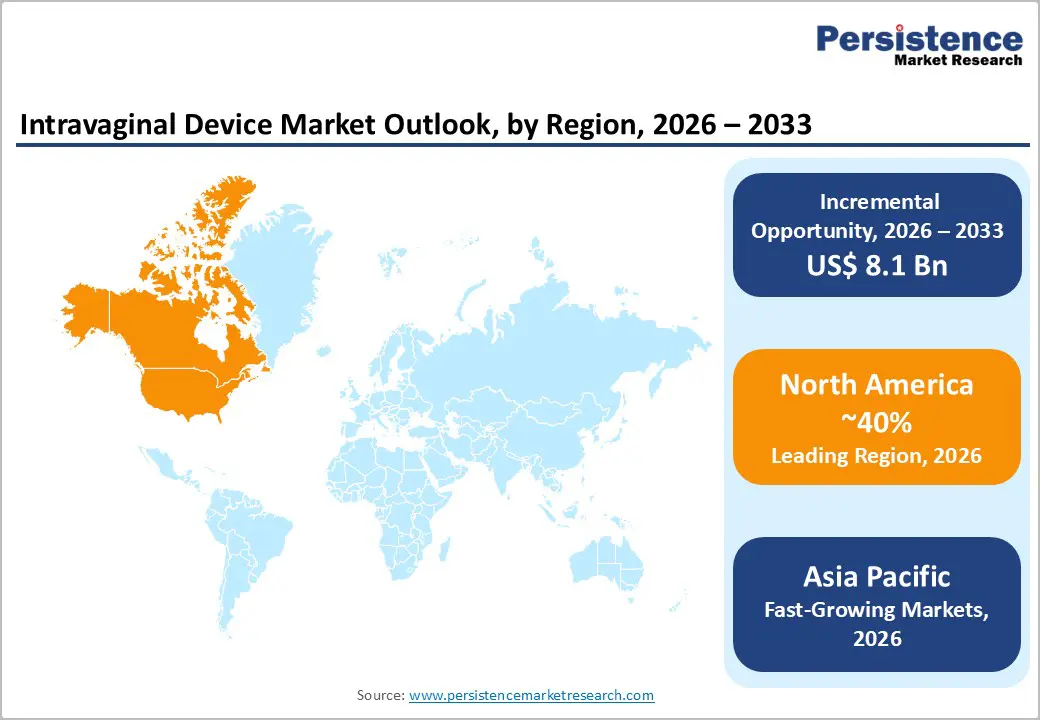

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by advanced healthcare infrastructure, high women’s health awareness, strong innovation, and adoption of minimally invasive and home-use intravaginal devices.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by large populations, improving healthcare infrastructure, rising incomes, and growing demand for affordable devices.

- Leading Product Type: Contraceptive devices are projected to represent the leading product type in 2026, accounting for 50% of the revenue share, driven by widespread use of vaginal rings, established efficacy, user control, and integration with hormonal or barrier technologies.

- Leading Application: Stress urinary incontinence is anticipated to be the leading application, accounting for over 60% of the revenue share in 2026, supported by high reliance on long-acting reversible contraceptives and vaginal rings for effective, reversible pregnancy prevention.

| Key Insights | Details |

|---|---|

| Intravaginal Device Market Size (2026E) | US$7.9 Bn |

| Market Value Forecast (2033F) | US$16.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.3% |

DRO Analysis

Driver - Rising Prevalence of Pelvic Floor Disorders and Aging Demographics

The increasing incidence of stress urinary incontinence and pelvic organ prolapse among aging populations is driving demand for intravaginal devices. Postmenopausal women often seek non-invasive, effective solutions for maintaining pelvic health, and pessaries or supportive rings provide a practical alternative to surgery. Healthcare providers are prioritizing conservative management strategies, emphasizing comfort, safety, and long-term outcomes. Growing awareness of pelvic floor health, routine gynecological screening, and early intervention programs have expanded the target population.

Intravaginal devices designed for pelvic floor disorders also offer enhanced quality of life, reducing discomfort and supporting daily activity. Integration of adjustable and customizable designs ensures higher compliance and patient satisfaction. Clinicians are increasingly recommending devices that can be managed independently at home, reducing the burden on hospital resources and healthcare costs.

Advancements in Contraceptive Technologies and User-Controlled Delivery Systems

Technological innovation in intravaginal contraceptive devices, including hormone-eluting rings and multipurpose vaginal systems, has enhanced efficacy, safety, and convenience. User-controlled delivery allows women to manage their reproductive health with autonomy, reducing dependence on clinic visits and increasing adherence. Modern devices incorporate biodegradable materials, controlled-release mechanisms, and long-acting designs, improving patient experience. Integration with mobile health apps enables tracking and monitoring, supporting personalized care.

Innovation also addresses limitations of traditional contraceptives, reducing side effects and improving hormonal balance. Market players invest heavily in R&D to develop rings compatible with multiple therapeutic agents, including antiviral or probiotic compounds, combining reproductive health management with disease prevention. Educating users on device insertion, maintenance, and benefits enhances trust and encourages broader use. Rising awareness campaigns and supportive policies reinforce demand, particularly in regions with increasing female workforce participation.

Restraint - Regulatory and Approval Hurdles for Novel Drug-Device Combinations

The development and commercialization of intravaginal devices face complex regulatory landscapes, particularly for drug-device combination products. Approval processes require extensive clinical trials, stringent safety evaluations, and documentation compliance, which can delay market entry and increase costs. Variations in regulatory requirements across countries complicate launches, necessitating region-specific strategies. Regulatory uncertainty can discourage smaller innovators from investing in novel technologies.

Navigating regulatory pathways requires significant collaboration with authorities, alignment with international standards, and robust clinical evidence. Delays in approval may result in lost market opportunities and competitive disadvantages for companies. Combination products face additional scrutiny regarding drug release profiles, material safety, and long-term outcomes. Manufacturers must also manage intellectual property considerations and potential litigation risks.

Cultural and Social Barriers to Adoption

In certain regions, cultural norms, social stigma, and limited awareness restrict acceptance of intravaginal devices. Discussions around reproductive and pelvic health may be considered sensitive, limiting patient education and counseling opportunities. Misconceptions about device safety, efficacy, or hygiene impede adoption, particularly in rural or conservative populations. Women may prefer traditional contraceptive methods or avoid treatment for pelvic disorders due to embarrassment or societal pressure. Lack of trained healthcare professionals for device fitting and follow-up exacerbates the challenge.

These barriers also impact market penetration in emerging economies, where limited outreach and low literacy levels reduce awareness of innovative intravaginal solutions. Healthcare providers often face difficulty in counseling patients due to cultural sensitivities, affecting adherence and patient confidence. Misconceptions and myths about device use may lead to discontinuation or avoidance of treatment. Addressing these challenges necessitates multifaceted strategies, including digital education tools, peer support initiatives, and collaboration with local health authorities to normalize intravaginal device use while maintaining respect for cultural values.

Opportunity - Smart and Digitally Integrated Intravaginal Devices

The integration of digital technology into intravaginal devices presents a significant growth opportunity. Smart rings and monitoring-enabled devices allow real-time tracking of hormone release, adherence, and physiological responses, enhancing personalized care. Data connectivity with mobile apps and telehealth platforms improves user engagement, enabling remote consultations, reminders, and health analytics. Digital integration enhances patient confidence and empowers women to manage reproductive and pelvic health proactively.

Smart intravaginal devices also facilitate research and clinical insights by collecting anonymized user data, enabling improved product design and evidence-based recommendations. They support preventive care by alerting users to anomalies, enhancing early intervention for pelvic disorders or contraceptive compliance. Partnerships between technology providers and healthcare companies accelerate innovation and adoption.

Emerging-Market Expansion and Women-Health-Care Reform

Emerging markets offer substantial growth potential for intravaginal devices due to increasing healthcare access, rising disposable incomes, and government-supported family planning programs. Expansion into these regions allows manufacturers to tap into underserved populations and meet rising demand for affordable contraceptive, therapeutic, and diagnostic devices. Health policy reforms promoting women’s health awareness, subsidized programs, and rural outreach initiatives are accelerating device adoption. Increasing investments in local manufacturing and distribution networks reduce costs and improve availability.

Partnerships with local healthcare providers and NGOs enhance education, distribution, and community engagement, fostering trust and long-term adoption. Tailoring devices to local preferences, including reusable or low-cost options, addresses affordability barriers while complying with regional regulations. Programs targeting reproductive health, pelvic floor management, and STDs complement device promotion, reinforcing preventive care approaches.

Category-wise Analysis

Product Type Insights

Contraceptive devices are expected to lead the intravaginal device market, accounting for approximately 50% of revenue in 2026, driven by the widespread use of vaginal rings and related delivery systems for family planning, offering women effective, reversible, and user-controlled contraception. For example, the NuvaRing®, a widely adopted hormonal vaginal ring, allows monthly use with minimal clinical supervision, demonstrating high adherence and convenience compared to daily oral pills.

Therapeutic devices are likely to represent the fastest-growing segment, supported by increasing clinical preference for non-invasive management of gynecological conditions such as stress urinary incontinence and pelvic organ prolapse. These devices, including pessaries and support rings, provide effective symptom relief while avoiding surgical intervention, making them highly suitable for aging populations and patients seeking conservative treatment. For example, the Milex® Pessary by CooperSurgical is widely used in clinical settings for managing pelvic floor disorders, offering customizable sizing and long-term usability.

Application Insights

Stress urinary incontinence is projected to lead the market, capturing around 60% of the revenue share in 2026, supported by high prevalence of SUI among aging women and postnatal populations drives demand for effective, non-invasive management solutions. Intravaginal support devices, such as pessaries and continence rings, are widely used to provide symptom relief and improve quality of life without requiring surgery. For example, the Uresta® Bladder Support is a reusable intravaginal device designed specifically for SUI management, allowing women to maintain daily activities comfortably.

Pelvic organ prolapse is likely to be the fastest-growing application, driven by increasing incidence among aging women, rising awareness of pelvic health, and preference for non-invasive treatment options. Intravaginal pessaries are widely adopted for managing prolapse, offering effective support without surgical risks. For example, the Ring Pessary by MedGyn Products, Inc. is commonly used for POP management, providing a simple, cost-effective, and patient-friendly solution. Clinical guidelines increasingly recommend pessaries as an initial treatment approach, especially for patients who are not candidates for surgery or prefer conservative care.

Regional Insights

North America Intravaginal Device Market Trends

North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by advanced healthcare infrastructure, high awareness of women’s health, and widespread adoption of minimally invasive solutions. Hospitals, gynecology clinics, and ambulatory surgical centers actively recommend intravaginal contraceptive devices, therapeutic pessaries, and drug-eluting rings for contraception and pelvic floor management. Aging demographics, increasing prevalence of stress urinary incontinence (SUI) and pelvic organ prolapse (POP), and rising female workforce participation contribute to demand.

Public health initiatives emphasizing reproductive health, preventive care, and early diagnosis of pelvic disorders support market growth. Strong reimbursement policies and high procedural volumes encourage adoption of innovative devices. Companies for example, CooperSurgical, Inc. have introduced patient-friendly vaginal rings and SUI devices, leveraging North America’s robust R&D ecosystem and telehealth integration for home-based guidance.

Europe Intravaginal Device Market Trends

Europe is likely to be a significant market for intravaginal device, due to well-established healthcare systems, favorable reimbursement policies, and high patient awareness. Countries such as Germany, France, and the U.K. are witnessing increasing adoption of contraceptive rings, long-acting reversible contraceptives (LARCs), and therapeutic pessaries. Regulatory oversight by agencies such as the European Medicines Agency (EMA) ensures product safety and efficacy, creating trust among patients and clinicians. For example, Bayer AG have leveraged these trends by offering technologically advanced drug-eluting rings and pessaries with user-friendly designs and minimal clinical supervision requirements.

Aging populations and the rising prevalence of pelvic floor disorders such as SUI and POP have encouraged clinicians to recommend non-invasive, conservative treatment options. Public health campaigns and women’s health initiatives continue to promote awareness and adoption of intravaginal devices, supporting steady growth. Integration of evidence-based clinical guidelines and minimally invasive device options reinforces Europe’s position as a region with high standards for women’s health management.

Asia Pacific Intravaginal Device Market Trends

The Asia Pacific region is likely to be the fastest growing region, driven by large populations, improving healthcare infrastructure, and rising disposable incomes in China, India, and ASEAN nations. Local manufacturing advantages, cost-effective production, and supply chain resilience enable competitive pricing and broader access to intravaginal contraceptive and therapeutic devices. For example, FemCap, Inc. have introduced affordable, reusable contraceptive vaginal caps for the region, addressing unmet needs in emerging markets.

The Asia Pacific market offers significant opportunities through emerging-market expansion, telehealth-enabled device fitting, and digital awareness campaigns targeting contraception and pelvic health. Affordable, reusable, and culturally acceptable devices are gaining traction, while partnerships between domestic players improve distribution in rural and semi-urban areas. Regulatory harmonization with international standards is facilitating the introduction of innovative devices, including drug-eluting rings and therapeutic pessaries.

Competitive Landscape

The global intravaginal device market exhibits a moderately fragmented structure, driven by the presence of both multinational corporations and specialized women’s health device manufacturers focusing on diverse applications such as contraception, pelvic floor management, and diagnostic solutions. Companies are actively investing in research and development to introduce advanced, user-friendly, and minimally invasive devices that improve patient comfort and treatment outcomes. Increasing emphasis on biocompatible materials, drug-eluting technologies, and digital integration is shaping competitive dynamics.

With key leaders including CooperSurgical, Inc., MedGyn Products, Inc., Boston Scientific Corporation, Bayer AG, and Merck & Co., Inc., the market reflects strong competition across regional players. These players compete through continuous product innovation, expansion of product portfolios, mergers and acquisitions, and geographic expansion strategies to enhance market reach. Focus areas include development of next-generation vaginal rings, pessaries, and smart intravaginal devices, along with partnerships for distribution and clinical adoption.

Key Industry Developments:

- In January 2026, Organon entered into an agreement to exclusively license global rights to MIUDELLA®, a hormone-free copper intrauterine device from Sebela Pharmaceuticals, strengthening its women’s health portfolio and expanding access to long-acting, reversible contraceptive options, with commercialization subject to regulatory approvals and supply chain clearances.

- In January 2025, women’s health startup Cntrl+ announced the launch of its FDA-cleared bladder support device designed for managing stress urinary incontinence, offering a reusable, user-friendly, and non-invasive solution that enables women to prevent bladder leaks during daily activities and exercise.

- In April 2025, COOLOGICS announced the initiation of multi-center clinical trials for its innovative intravaginal cooling device, Vlisse, designed to treat vaginal yeast infections through a drug-free approach, aiming to demonstrate safety and efficacy for potential FDA clearance.

Companies Covered in Intravaginal Device Market

- CooperSurgical, Inc.

- MedGyn Products, Inc.

- Boston Scientific Corporation

- FemCap, Inc.

- Evofem Biosciences, Inc.

- Theramex

- Milex Products Inc.

- Joylux, Inc.

- Elvie

- YARLAP, Inc.

- INTIMINA

- Ceek Women’s Health

- Roche Diagnostics

- Pathway Genomics Corporation

Frequently Asked Questions

The global intravaginal device market is projected to reach US$7.9 billion in 2026.

The intravaginal device market is driven by rising demand for minimally invasive women’s health solutions, increasing prevalence of pelvic floor disorders, and growing adoption of user-controlled contraceptive technologies.

The intravaginal device market is expected to grow at a CAGR of 10.5% from 2026 to 2033.

Key market opportunities include development of smart, digitally integrated intravaginal devices and expansion into emerging markets driven by improving women’s healthcare access and awareness.

CooperSurgical, Inc., MedGyn Products, Inc., Boston Scientific Corporation, FemCap, Inc., Evofem Biosciences, Inc., Theramex, and Milex Products Inc. are the leading players.