- Agrochemicals

- U.S. Industrial Enzymes Market

U.S. Industrial Enzymes Market Size, Share, and Growth Forecast 2026 – 2033

U.S. Industrial Enzymes Market by Enzyme Type (Carbohydrases (Amylases, Cellulases), Proteases, Lipases, Misc.), End-user (Food and Beverages (Bakery and Confectionery, Dairy Products, Beverages, Processed Food) Detergents and Cleaners; Animal Feed; Biofuels; Pharmaceuticals and Nutraceuticals, Textiles, Pulp and Paper, Personal Care and Cosmetics), and Regional Analysis, 2026–2033

U.S. Industrial Enzymes Market Size and Share Analysis

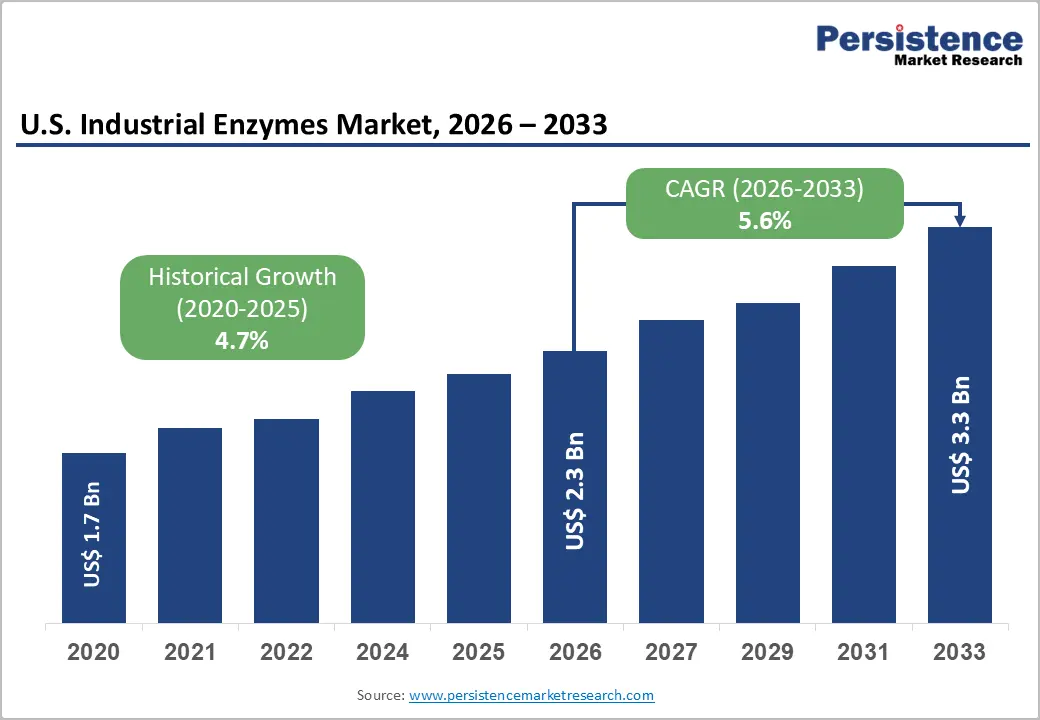

The U.S. industrial enzymes market size is expected to be valued at US$2.3 billion in 2026 and projected to reach US$3.4 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033. The market's consistent growth is anchored in the structural integration of enzyme-based bioprocessing across food manufacturing, biofuel production, pharmaceutical synthesis, and household detergent formulation sectors that collectively benefit from enzymes' superior substrate specificity, process efficiency, and regulatory alignment with clean-label and sustainability mandates.

The U.S. food and beverage manufacturing sector, which accounted for 16.8% of total U.S. manufacturing sales in 2021 per U.S. Census Bureau data and employed approximately 1.7 million workers across over 42,700 establishments, is the primary structural anchor for industrial enzyme demand, with enzyme applications embedded throughout starch processing, dairy, brewing, and meat tenderization workflows. Simultaneously, the U.S. Renewable Fuel Standard (RFS) and biofuel mandates sustain cellulase and amylase demand at a commercial scale within the ethanol production supply chain.

Key Industry Highlights:

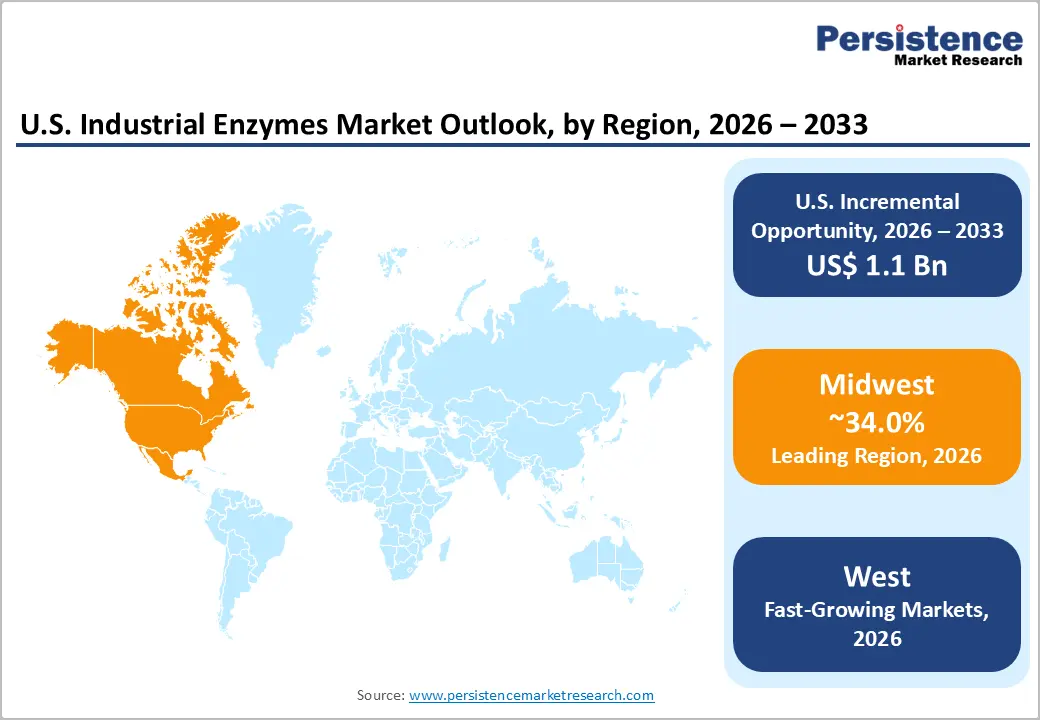

- Leading Region: The Midwest leads the U.S. industrial enzymes market with approximately US$ 731 million in revenue in 2026, driven by the region's dominance of U.S. fuel ethanol production, contributing over 75% of national output, and its concentration of corn starch processing and grain fermentation facilities requiring continuous high-volume carbohydrase inputs.

- Fast-growing Region: The West region is emerging as the fastest-growing sub-national market, propelled by California's food and beverage manufacturing leadership, the highest establishment count nationally per U.S. Census Bureau, the Pacific Coast's expanding biotech enzyme R&D ecosystem, and speciality beverage enzyme demand from the world's largest North American wine industry.

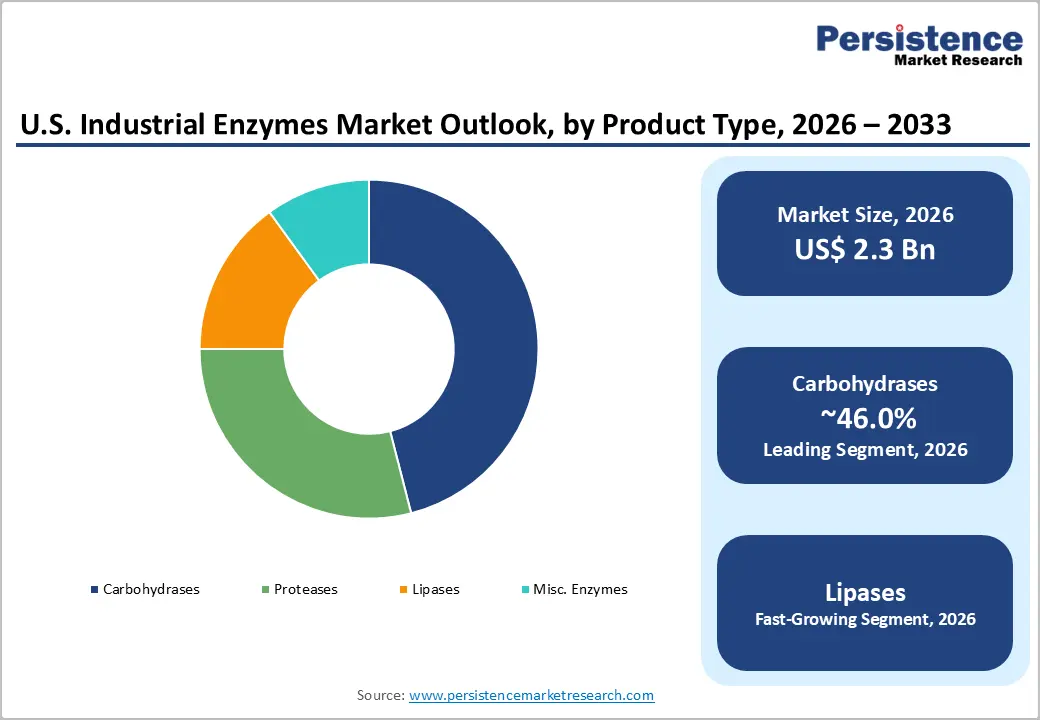

- Leading Enzyme Segment: Carbohydrases dominate the enzyme type category with approximately 46% market share in 2026, anchored by their indispensable role in U.S. corn starch processing and the 15.8-billion-gallon annual fuel ethanol industry, the world's largest, where amylases and glucoamylases function as non-substitutable process inputs at commercial scale.

- Fast-growing Enzyme Segment: Lipases are the fastest-growing enzyme segment, projected at a CAGR of 5% (2026–2033), fuelled by their expanding deployment in sustainable detergent formulations, personal care product clean-label reformulation, and pharmaceutical lipid synthesis, all sectors where regulatory and consumer sustainability pressures are systematically displacing petrochemical-derived functional ingredients.

- Key Opportunity: Pharmaceutical biocatalysis and sustainable cleaning formulations, where the Ginkgo Bioworks–Merck API enzyme collaboration and BASF–IFF partnership both signal major forthcoming investment, create a premium-tier enzyme demand segment that commands significantly higher per-unit pricing than commodity food processing applications

DRO Analysis

Drivers - Deep Integration of Enzymes Across U.S. Food and Beverage Manufacturing

The U.S. food and beverage manufacturing sector's scale and structural enzyme dependency create a durable, non-cyclical demand foundation for the industrial enzymes market. U.S. Census Bureau data confirms that food and beverage establishments numbering over 42,700 in 2022 and concentrated in California, Texas, and New York accounted for 16.8% of total U.S. manufacturing sales and 15.4% of manufacturing employment in 2021.

Within this, the starch processing relies on amylases for glucose syrup and high-fructose corn syrup production; dairy processing employs lactases and proteases in cheese making and lactose-free product manufacturing; and baking extensively uses xylanases and amylases to improve dough extensibility and shelf life. Meat processing, which contributes 26.2% of food manufacturing sales, uses protease-based tenderisers. This multi-process enzyme dependency across the value chain ensures sustained baseline demand regardless of macroeconomic conditions.

Biofuel Production Mandates Sustaining High-Volume Carbohydrase Demand in Ethanol Processing

U.S. biofuel policy directly underpins a significant and structurally committed demand base for industrial carbohydrases, particularly alpha-amylases, glucoamylases, and cellulases that are essential catalysts in grain-to-ethanol fermentation and cellulosic ethanol production. The U.S. Environmental Protection Agency (EPA)'s Renewable Fuel Standard (RFS) mandates blending of 36 billion gallons of renewable fuels annually by 2022, with cellulosic biofuels receiving the highest subsidy weighting.

The U.S. Energy Information Administration (EIA) confirmed that the United States produced approximately 15.8 billion gallons of fuel ethanol in 2023, the highest volume globally, requiring continuous enzyme inputs at a commercial scale. The June 2024 acquisition by Lallemand of BASF's San Diego-based bioenergy enzymes business, including the Spartec® portfolio, directly reflects the commercial depth of this enzyme demand segment in North America.

Restraints - Thermal and pH Sensitivity of Native Enzymes Constraining Process Applicability

Conventional industrial enzymes, particularly proteases and lipases, exhibit narrow operational windows of temperature stability and pH tolerance, limiting their applicability across high-temperature industrial processes such as paper pulping, textile scouring, and certain pharmaceutical synthesis pathways. Enzyme denaturation above process-specific stability thresholds necessitates either process temperature adjustment, incurring energy cost trade-offs or procurement of premium thermostable engineered variants at significantly higher unit cost.

The American Chemical Society (ACS) peer-reviewed literature documents that thermal inactivation remains the primary attrition mechanism limiting enzyme reuse cycles in immobilised enzyme systems, directly constraining the per-unit economics of industrial enzyme deployment in high-temperature continuous manufacturing environments.

Regulatory Complexity and GRAS Classification Requirements Creating Commercialisation Barriers

Industrial enzymes used in food processing and pharmaceutical manufacturing require U.S. Food and Drug Administration (FDA) approval either as food additives under 21 CFR or through the Generally Recognised as Safe (GRAS) self-affirmation pathway, both processes involving substantial technical dossier preparation, toxicological assessment, and regulatory review timelines that can extend from 12 to 36 months.

For novel enzyme variants produced through protein engineering or synthetic biology, a rapidly growing category, regulatory pathway ambiguity under existing FDA and USDA frameworks adds compliance cost and commercial risk. This regulatory burden disproportionately affects small and mid-size enzyme developers, consolidating market access toward large established producers with dedicated regulatory affairs capabilities.

Opportunities - Pharmaceutical and Biocatalysis Applications Creating Premium-Tier Enzyme Demand

The pharmaceutical and nutraceutical sectors represent distinct growth vectors for U.S. industrial enzyme providers, driven by the rapid adoption of biocatalysis as a core manufacturing strategy by both large pharmaceutical companies and emerging biotech firms. Enzymatic synthesis routes offer measurable advantages over traditional chemical synthesis in active pharmaceutical ingredient (API) manufacturing, including higher stereoselectivity, reduced generation of hazardous byproducts, and alignment with the FDA's green chemistry and Process Analytical Technology (PAT) guidance frameworks.

The October 2022 collaboration between Ginkgo Bioworks and Merck to engineer up to four biocatalytic enzymes for API manufacturing illustrates the deep integration of industrial enzyme innovation within U.S. pharmaceutical supply chains.

As the global pharmaceutical industry is committed to more sustainable manufacturing practices guided by the American Chemical Society's Green Chemistry Institute (ACS GCI), the pharmaceutical roundtable demand for custom, high-purity industrial enzymes in U.S. drug production is well-positioned to attain market growth.

Enzyme Innovation for Sustainable Detergent and Personal Care Formulations: Unlocking New Demand

The U.S. detergent and personal care industries are undergoing a formulation transformation driven by consumer sustainability preferences, regulatory pressure on surfactant and chemical ingredient safety, and brand commitments to biodegradability and reduced environmental footprint, all of which structurally favor enzyme-based active ingredient substitution. Proteases, lipases, and amylases in laundry and dishwashing detergents enable effective stain removal at lower wash temperatures, directly supporting the U.S. Department of Energy (DOE)'s cold water washing initiatives and energy efficiency standards.

The October 2025 strategic collaboration between BASF and International Flavours & Fragrances (IFF) to accelerate next-generation enzyme innovation for fabric care, dishwashing, personal care, and industrial cleaning applications, combining advanced protein engineering with large-scale biomaterial commercialisation, signals significant forthcoming investment in this segment.

Lipases, specifically, represent the fastest-growing enzyme type within the U.S. personal care and detergent applications, as formulators replace petrochemical-derived cleaning agents with biocatalytic alternatives to meet environmental and clean-label product positioning requirements.

Category-wise Analysis

Enzyme Type Insights

Carbohydrases dominate the U.S. industrial enzymes market, commanding approximately 46% of total share in 2026. This leadership is structurally supported by the enzyme class's indispensable role across the two largest end-use sectors, food and beverages, and biofuels, where amylases and cellulases function as process-critical catalysts with no practical non-enzymatic substitute at a commercial scale. In starch processing, alpha-amylases and glucoamylases are essential for converting corn starch into glucose, high-fructose corn syrup, and fermentation substrates, industries worth tens of billions of dollars annually in the U.S. alone.

In biofuel production, the EIA confirmed U.S. fuel ethanol output of approximately 15.8 billion gallons in 2023, with gluco-amylases and cellulases embedded as core process inputs. The Lallemand acquisition of BASF's Spartec® carbohydrase portfolio in June 2024 further validates the commercial centrality of this enzyme class in the North American biofuel and distilled spirits segments.

End-user Insights

Food and beverages are the leading end-use segment in the U.S. industrial enzymes market, capturing approximately 38% of the total share in 2026. The segment's primacy is anchored in the U.S. food manufacturing sector's scale and its deep multi-process reliance on enzymatic bioprocessing across bakery, dairy, beverage, meat, and grain processing applications. The U.S. Census Bureau data confirming over 42,700 food and beverage manufacturing establishments in 2022, spread across California, Texas, New York, and beyond, represents an extensive installed base of enzyme-consuming production processes.

Within the food and beverages segment, bakery and confectionery applications leveraging xylanases, amylases, and glucose oxidases for dough conditioning and shelf-life extension, and dairy processing applications employing lactases, chymosins, and proteases for cheese production and lactose-free dairy manufacturing collectively represent the highest-volume enzyme consumption categories. The sector's clean-label trend, with consumers demanding shorter and more natural ingredient lists, further reinforces enzyme adoption as a functional ingredient alternative to synthetic chemical additives.

Zonal Insights

Midwest Industrial Enzymes Market Size

The Midwest is the largest sub-national region in the U.S. industrial enzymes market, with an estimated market value of approximately US$ 731 million in 2026, representing the highest regional concentration of enzyme demand nationally. This dominance is directly attributable to the Midwest's position as the geographic heart of U.S. corn processing, grain milling, and fuel ethanol production industries that generate the largest single industrial enzyme demand pool in the country.

Illinois, Iowa, Nebraska, and Indiana collectively host the majority of the U.S. grain processing and ethanol production capacity: the U.S. Renewable Fuels Association (RFA) confirms that the Midwest produces over 75% of U.S. fuel ethanol output. This concentration of starch-to-sugar and grain-to-ethanol conversion facilities creates a high-density, geographically compact enzyme procurement ecosystem dominated by carbohydrase applications for amylase, glucoamylase, and cellulase deployment at industrial fermentation scale.

West Industrial Enzymes Market Size

The West region accounts for an estimated US$ 516 million in U.S. industrial enzyme market revenue in 2025, driven by a combination of the nation's highest concentration of food and beverage manufacturing establishments, a world-class biotechnology and synthetic biology research ecosystem, and a structurally significant wine and craft beverage industry that creates distinctive enzyme demand. U.S. Census Bureau data confirms that California alone leads all U.S. states in food and beverage manufacturing establishment count, with the West region hosting a disproportionate share of the 42,700+ national establishments.

California's wine industry the largest in North America uses pectinases, proteases, and glucose oxidases extensively in fermentation and clarification, while the Pacific Northwest's craft brewing and food processing sectors create additional specialty enzyme consumption. The region also hosts major enzyme R&D operations from Ginkgo Bioworks, Novozymes, and DSM-Firmenich, linking commercial demand with innovation activity.

Southeast Industrial Enzymes Market Size

The Southeast region contributes an estimated US$ 380 million to the U.S. industrial enzymes market in 2025, underpinned by substantial animal feed, poultry processing, textile manufacturing, and paper and pulp industry concentrations that generate structurally distinct enzyme demand profiles relative to the Midwest and West.

The Southeast is the United States' largest broiler chicken and turkey production region. USDA data confirms that Georgia, North Carolina, Arkansas, and Alabama collectively account for approximately 60% of U.S. broiler production, creating high-volume demand for phytases and proteases in animal feed enzyme supplementation that improve nutrient digestibility and reduce phosphorus excretion. The region's extensive textile manufacturing base, concentrated in North and South Carolina, sustains demand for cellulases and amylases in biostoning, desizing, and fabric finishing applications that are progressively replacing environmentally damaging chlorine and chemical treatment processes.

Competitive Landscape

The U.S. industrial enzymes market is moderately consolidated at the top tier, with three multinational life science and speciality chemicals companies, Novozymes (Chr. Hansen/Novonesis), DSM-Firmenich, and BASF SE, collectively commanding the largest revenue shares through diversified enzyme portfolios spanning food, biofuel, detergent, and pharmaceutical applications. Key competitive differentiators include protein engineering capability, strain development for fermentation yield optimisation, proprietary immobilisation and formulation technologies, and regulatory affairs depth for GRAS and FDA clearance management.

Emerging competitive dynamics include synthetic biology-driven enzyme design platforms exemplified by Ginkgo Bioworks' cell programming approach and the entry of mid-size speciality enzyme producers, including Biocatalysts Ltd. and Amano Enzyme, targeting niche high-purity applications in pharmaceuticals and speciality food processing.

Key Developments:

- October 2025, BASF and International Flavours & Fragrances Inc. announced a strategic collaboration to accelerate next-generation enzyme and biobased polymer innovation for fabric care, dishwashing, personal care, and industrial cleaning applications, strengthening sustainable industrial enzyme development through advanced biotechnology, protein engineering, and large-scale biomaterial commercialisation.

June 2024, BASF sold its San Diego-based bioenergy enzymes business, including the Spartec® product portfolio and related pipeline technologies, to Lallemand subsidiaries Danstar Ferment AG and Lallemand Specialities Inc. The acquisition strengthens Lallemand Biofuels & Distilled Spirits’ position in the North American fuel ethanol enzyme market and expands its industrial enzyme capabilities for biofuel production through integrated gluco and alpha amylase fermentation technologies.

U.S. Industrial Enzymes Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 1.7 Billion |

|

Current Market Value (2026) |

US$ 2.3 Billion |

|

Projected Market Value (2033) |

US$ 3.4 Billion |

|

CAGR (2026–2033) |

5.6% |

|

Leading Region |

Midwest, largest share (~US$ 731.0 Mn, 2025) |

|

Dominant Category-1 (Enzyme Type) |

Carbohydrases, ~46% share |

|

Top-ranking Category-2 (End Use) |

Food and Beverages, ~38% share |

|

Incremental Opportunity (2026–2033) |

US$ 1.1 Billion |

Companies Covered in U.S. Industrial Enzymes Market

- AB Enzymes

- Adisseo

- Advanced Enzyme Technologies

- Amano Enzyme Inc.

- BASF

- Biocatalysts

- Codexis

- DuPont

- DSM-Firmenich

- Kemin Industries, Inc.

- Kerry Group plc

- Novozymes A/S

- Dyadic Applied Biosolutions

- Enzyme Development Corporation

Frequently Asked Questions

The U.S. industrial enzymes market is estimated at US$2.3 billion in 2026, driven by deep structural integration of enzymes across food manufacturing, biofuel production, pharmaceutical biocatalysis, and sustainable cleaning product formulation.

The enzyme dependency of U.S. food and beverage manufacturing confirmed by U.S. Census Bureau data showing over 42,700 establishments and 16.8% of total manufacturing sales in 2021 and the EPA's Renewable Fuel Standard (RFS) mandating 36 billion gallons of annual renewable fuel blending, which sustains large-volume commercial demand for amylases, glucoamylases, and cellulases in the U.S. fuel ethanol industry producing approximately 15.8 billion gallons annually per the U.S. Energy Information Administration (EIA).

The Midwest is the leading U.S. regional market for industrial enzymes, with an estimated US$ 731 million in revenue in 2026. Its dominance reflects the region's concentration of fuel ethanol production, contributing over 75% of national output per the Renewable Fuels Association (RFA) and its scale of corn starch processing and grain fermentation operations, which collectively represent the largest single industrial enzyme demand pool in the United States, anchored entirely in carbohydrase applications.

The highest-value opportunity is the pharmaceutical biocatalysis segment, where custom enzyme engineering for active pharmaceutical ingredient manufacturing, exemplified by the Ginkgo Bioworks–Merck collaboration to develop biocatalytic enzymes for API synthesis, offers per-unit pricing multiples above commodity food processing enzymes. The BASF–IFF strategic collaboration on next-generation enzymes for sustainable detergent and personal care applications, announced in October 2025, signals significant forward investment in lipase and protease applications that are systematically displacing petrochemical ingredients across high-margin consumer product categories.

The leading companies in the U.S. industrial enzymes market include Novozymes A/S (now operating as Novonesis following merger with Chr. Hansen), DSM-Firmenich AG, BASF SE, International Flavors & Fragrances (IFF), DuPont (Danisco), Amano Enzyme, Lallemand Biofuels & Distilled Spirits, Ginkgo Bioworks, Biocatalysts Ltd., and AB Enzymes.