- Executive Summary

- Global Industrial Automation and Control System Market Snapshot 2025 and 2034

- Market Opportunity Assessment, 2025 - 2033, US$ Mn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Industrial Automation Demand by Region

- Global Automation Adoption by Industry Vertical

- Global Robotics & Control System Deployment Trends

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 - 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Industrial Automation and Control System Market Outlook:

- Key Highlights

- Global Industrial Automation and Control System Market Outlook: Component

- Introduction/Key Findings

- Historical Market Size (US$ Mn) Analysis by Component, 2020-2024

- Current Market Size (US$ Mn) Analysis and Forecast, by Component, 2025-2033

- Hardware

- Software

- Services

- Market Attractiveness Analysis: Component

- Global Industrial Automation and Control System Market Outlook: System Type

- Introduction/Key Findings

- Historical Market Size (US$ Mn) Analysis by System Type, 2020-2024

- Current Market Size (US$ Mn) Analysis and Forecast, by System Type, 2025-2033

- PLC/PAC

- DCS

- SCADA

- HMI

- Robotics & Motion Control Packages

- Market Attractiveness Analysis: System Type

- Global Industrial Automation and Control System Market Outlook: End-Use Industry

- Introduction/Key Findings

- Historical Market Size (US$ Mn) Analysis by End-Use Industry, 2020-2024

- Current Market Size (US$ Mn) Analysis and Forecast, by End-Use Industry, 2025-2033

- Aerospace & Defense

- Automotive

- Chemical

- Energy & Utilities

- Food & Beverage

- Healthcare

- Manufacturing

- Mining & Metal

- Oil & Gas

- Misc

- Market Attractiveness Analysis: End-Use Industry

- Global Industrial Automation and Control System Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Mn) Analysis by Region, 2020-2024

- Current Market Size (US$ Mn) Analysis and Forecast, by Region, 2025-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Industrial Automation and Control System Market Outlook:

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Mn) Analysis and Forecast, by Country, 2025-2033

- U.S.

- Canada

- North America Market Size (US$ Mn) Analysis and Forecast, by Component, 2025-2033

- Hardware

- Software

- Services

- North America Market Size (US$ Mn) Analysis and Forecast, by System Type, 2025-2033

- PLC/PAC

- DCS

- SCADA

- HMI

- Robotics & Motion Control Packages

- North America Market Size (US$ Mn) Analysis and Forecast, by End-Use Industry, 2025-2033

- Aerospace & Defense

- Automotive

- Chemical

- Energy & Utilities

- Food & Beverage

- Healthcare

- Manufacturing

- Mining & Metal

- Oil & Gas

- Misc

- Europe Industrial Automation and Control System Market Outlook:

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Mn) Analysis and Forecast, by Country, 2025-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Mn) Analysis and Forecast, by Component, 2025-2033

- Hardware

- Software

- Services

- Europe Market Size (US$ Mn) Analysis and Forecast, by System Type, 2025-2033

- PLC/PAC

- DCS

- SCADA

- HMI

- Robotics & Motion Control Packages

- Europe Market Size (US$ Mn) Analysis and Forecast, by End-Use Industry, 2025-2033

- Aerospace & Defense

- Automotive

- Chemical

- Energy & Utilities

- Food & Beverage

- Healthcare

- Manufacturing

- Mining & Metal

- Oil & Gas

- Misc

- East Asia Industrial Automation and Control System Market Outlook:

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Mn) Analysis and Forecast, by Country, 2025-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Mn) Analysis and Forecast, by Component, 2025-2033

- Hardware

- Software

- Services

- East Asia Market Size (US$ Mn) Analysis and Forecast, by System Type, 2025-2033

- PLC/PAC

- DCS

- SCADA

- HMI

- Robotics & Motion Control Packages

- East Asia Market Size (US$ Mn) Analysis and Forecast, by End-Use Industry, 2025-2033

- Aerospace & Defense

- Automotive

- Chemical

- Energy & Utilities

- Food & Beverage

- Healthcare

- Manufacturing

- Mining & Metal

- Oil & Gas

- Misc

- South Asia & Oceania Industrial Automation and Control System Market Outlook:

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Mn) Analysis and Forecast, by Country, 2025-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Mn) Analysis and Forecast, by Component, 2025-2033

- Hardware

- Software

- Services

- South Asia & Oceania Market Size (US$ Mn) Analysis and Forecast, by System Type, 2025-2033

- PLC/PAC

- DCS

- SCADA

- HMI

- Robotics & Motion Control Packages

- South Asia & Oceania Market Size (US$ Mn) Analysis and Forecast, by End-Use Industry, 2025-2033

- Aerospace & Defense

- Automotive

- Chemical

- Energy & Utilities

- Food & Beverage

- Healthcare

- Manufacturing

- Mining & Metal

- Oil & Gas

- Misc

- Latin America Industrial Automation and Control System Market Outlook:

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Mn) Analysis and Forecast, by Country, 2025-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Mn) Analysis and Forecast, by Component, 2025-2033

- Hardware

- Software

- Services

- Latin America Market Size (US$ Mn) Analysis and Forecast, by System Type, 2025-2033

- PLC/PAC

- DCS

- SCADA

- HMI

- Robotics & Motion Control Packages

- Latin America Market Size (US$ Mn) Analysis and Forecast, by End-Use Industry, 2025-2033

- Aerospace & Defense

- Automotive

- Chemical

- Energy & Utilities

- Food & Beverage

- Healthcare

- Manufacturing

- Mining & Metal

- Oil & Gas

- Misc

- Middle East & Africa Industrial Automation and Control System Market Outlook:

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Mn) Analysis and Forecast, by Country, 2025-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Mn) Analysis and Forecast, by Component, 2025-2033

- Hardware

- Software

- Services

- Middle East & Africa Market Size (US$ Mn) Analysis and Forecast, by System Type, 2025-2033

- PLC/PAC

- DCS

- SCADA

- HMI

- Robotics & Motion Control Packages

- Middle East & Africa Market Size (US$ Mn) Analysis and Forecast, by End-Use Industry, 2025-2033

- Aerospace & Defense

- Automotive

- Chemical

- Energy & Utilities

- Food & Beverage

- Healthcare

- Manufacturing

- Mining & Metal

- Oil & Gas

- Misc

- Competition Landscape

- Market Share Analysis, 2024

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- ABB Ltd.

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Siemens AG

- Automation, Inc.

- Electric SE

- Electric Corporation

- Controls International

- Electric Co.

- International Inc.

- Beckhoff Automation

- Omron Corporation

- FANUC Corporation

- Electric Corporation

- Industrial Automation

- IDEC Corporation

- ABB Ltd.

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Automation & Robotics

- Industrial Automation and Control System Market

Industrial Automation and Control System Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Industrial Automation and Control System market by Component (Hardware, Software, Services), System Type (PLC/PAC, DCS, SCADA), Industry (Manufacturing, Oil & Gas, Automotive, Energy & Utilities, Other), and Regional Analysis 2026 - 2033

Key Industry Highlights:

- Hardware leads with 46% share, while services grow fastest at 11.1% CAGR due to rising demand for integration, technical support, and performance optimization.

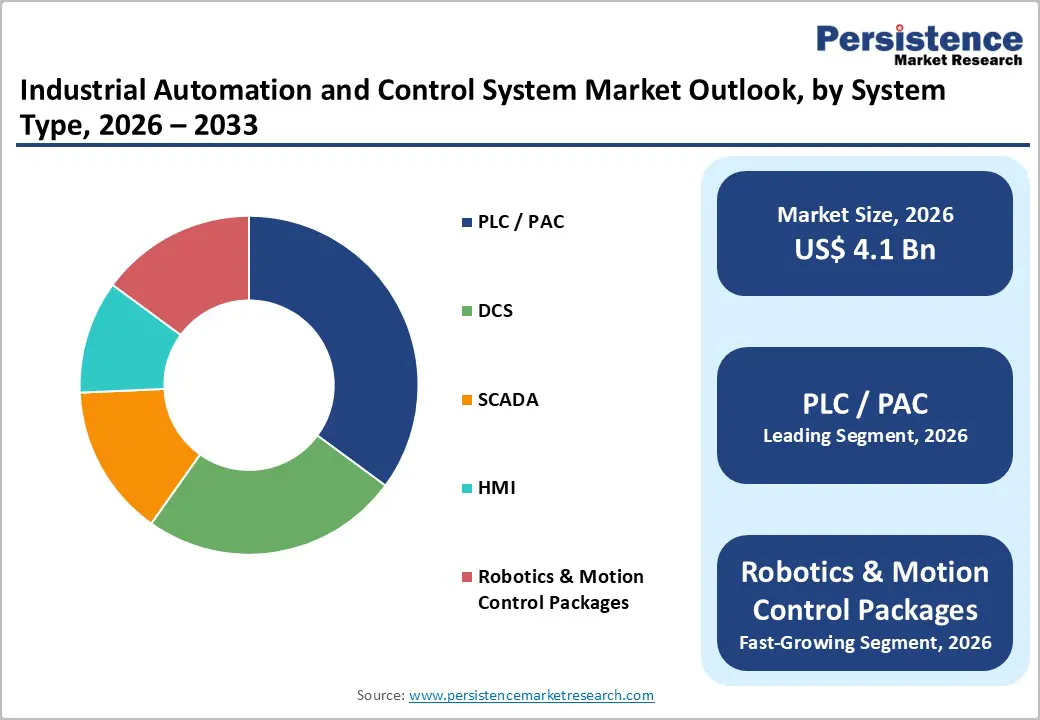

- PLC/PAC systems hold a 35% share, whereas robotics and motion control advance at a 12.6% CAGR, driven by labor substitution, collaborative automation, and healthcare manufacturing needs.

- Manufacturing leads end-use with a 24% share, while healthcare grows fastest at an 11.3% CAGR under stringent regulatory, contamination-control, and complexity-driven requirements.

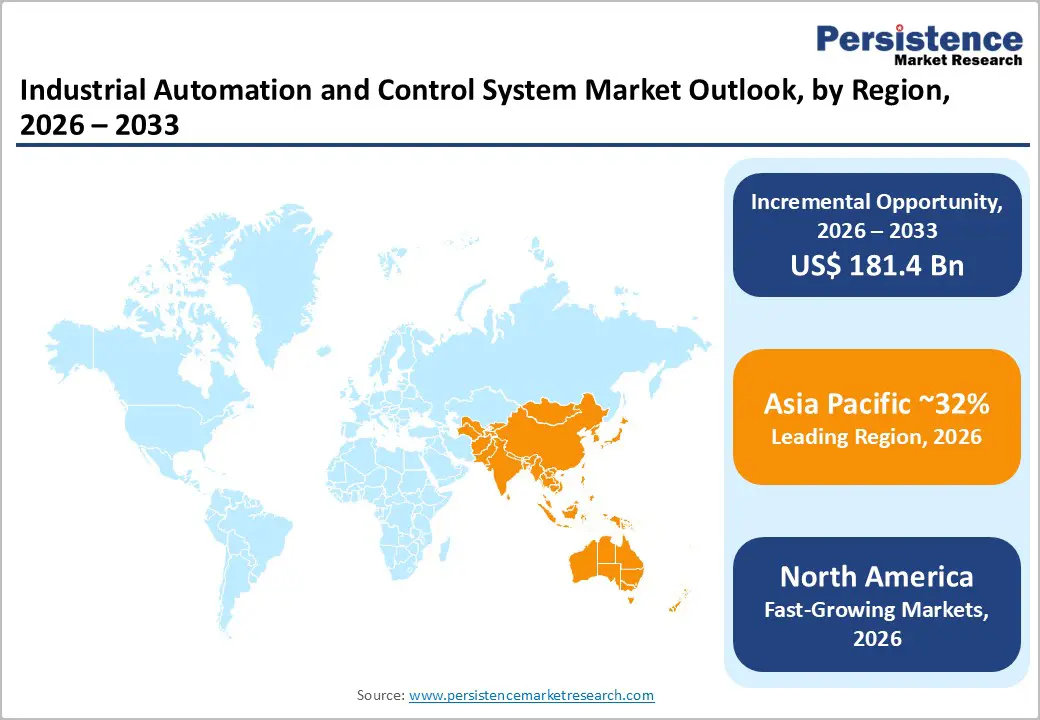

- Asia Pacific dominates with 32% share and 10.3% CAGR, while North America 27% and Europe 24% expand steadily through manufacturing upgrades and adoption acceleration.

- Strategic priorities center on AI/ML, cloud connectivity, and cybersecurity, with leaders advancing vertical ecosystems, outcome-based services, and industry-tailored solutions.

| Key Insights | Details |

|---|---|

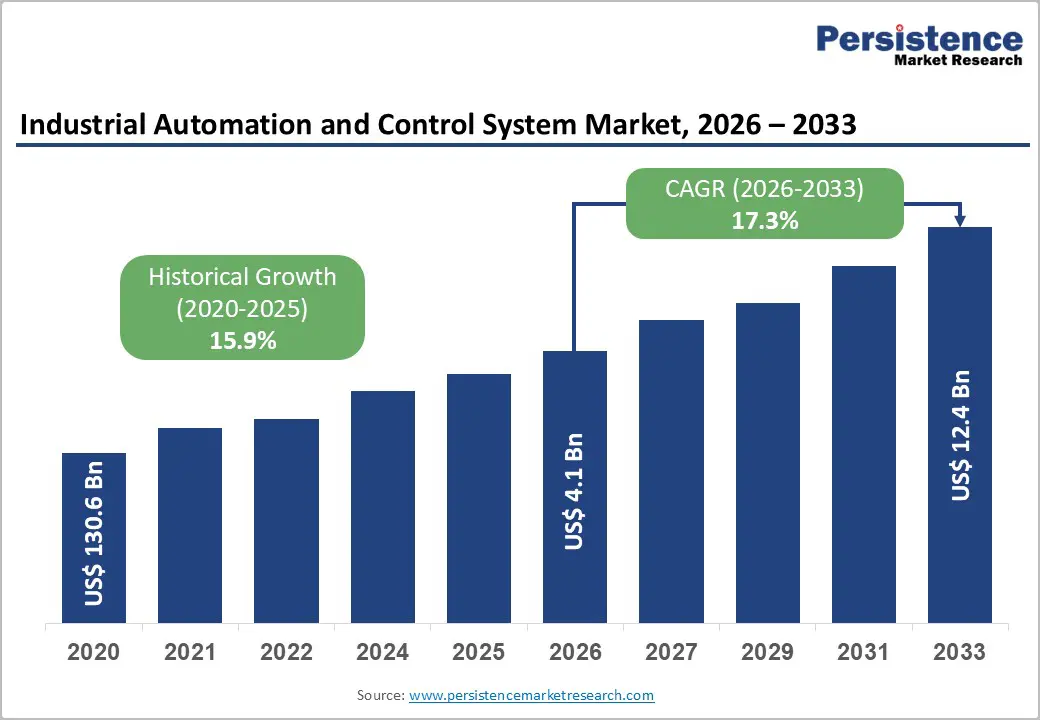

| Industrial Automation and Control System Market Size (2026E) | US$ 4.1 billion |

| Market Value Forecast (2033F) | US$ 12.4 billion |

| Projected Growth CAGR (2026 - 2033) | 17.3% |

| Historical Market Growth (2020 - 2025) | 15.9% |

Market Dynamics

Drivers - Industry 4.0 Adoption and Digital Transformation Imperatives

The global manufacturing sector is facing unprecedented pressure to adopt Industry 4.0 technologies, fundamentally transforming production methods. Industrial automation and control systems represent the foundational infrastructure enabling this transition. According to the United Nations Industrial Development Organization (UNIDO), digital manufacturing initiatives are expected to reduce production costs by 20-25% and improve output quality by 15-30%. Advanced economies, including Germany, Japan, and the United States, have established national Industry 4.0 strategic frameworks, allocating substantial government funding to support technology adoption.

The convergence of IoT sensors, artificial intelligence, and cloud computing with traditional control systems creates interconnected ecosystems that enhance predictive maintenance capabilities, reduce unplanned downtime by around 45-50%, and optimize resource allocation. Manufacturing enterprises across the automotive, chemical, food & beverage, and energy sectors are increasingly prioritizing automation investments as a means of competitive differentiation, with average automation technology expenditures rising across developed economies.

Labor Scarcity and Wage Inflation Pressures

Demographic shifts and labor market tightening across developed nations are creating acute workforce challenges. The International Labour Organization reports that skilled manufacturing workers in European and North American markets can expect a 30-40% wage increase over the next decade. This economic reality has catalyzed unprecedented capital investment in automation technologies as labor replacement and complementary mechanisms. Automated manufacturing systems demonstrate payback periods of 3-5 years in most industrial applications, with long-term operational cost reductions of 25-35% compared to manual labor-intensive processes.

Regions experiencing the most severe labor shortages, including Germany, Japan, and Scandinavia, exhibit the highest adoption rates of automation systems, with the highest capital expenditures on control systems. Regulatory mandates for workplace safety and ergonomic compliance further amplify automation investments, as automated systems inherently reduce occupational injury rates by 35-40% and enhance compliance with OSHA, EU Machine Directive, and ISO 12100 standards.

Restraints - Substantial Capital Investment Requirements and ROI Uncertainty

Industrial automation and control system implementations demand significant upfront capital investments, ranging from around US$500,000 to US$50+ million, depending on production facility scale and complexity. This capital intensity creates substantial barriers for small and medium-sized enterprises (SMEs), which represent approximately 70-75% of global manufacturing establishments. Implementation timelines typically extend 18-36 months, creating extended periods of operational disruption and production uncertainty. Integration complexity with legacy systems, which remain operational in ~60% of existing industrial facilities, compounds costs by 30-40% beyond new system installation expenses. Risk quantification research indicates that many major automation projects experience significant cost overruns, while a substantial share fail to achieve projected ROI targets within specified timeframes. Economic uncertainties, fluctuating capital availability, and competing investment priorities limit technology adoption among price-sensitive manufacturers, particularly in emerging markets, where alternative labor-cost advantages remain viable.

Cybersecurity Vulnerabilities and Operational Risk Management Challenges

The convergence of IT and OT systems creates expanded attack surfaces and cybersecurity vulnerabilities. Industrial control systems increasingly operate on networked architectures, exposing them to malware, ransomware, and sophisticated cyberattacks. The Cybersecurity and Infrastructure Security Agency (CISA) documented ~649 reported incidents affecting critical infrastructure in 2023, with industrial automation systems representing 28-30% of affected assets. Security breach remediation costs average US$4.5-6.2 million per incident, including operational downtime, system recovery, and regulatory compliance expenses. Regulatory compliance burdens, including NIST Cybersecurity Framework, IEC 62443 industrial automation security standards, and GDPR data protection requirements, require substantial ongoing investment in security infrastructure, monitoring capabilities, and personnel training. Legacy system vulnerabilities and the absence of built-in security architectures in many existing installations create persistent compliance challenges, deterring investment by risk-conscious enterprises and regulatory-sensitive organizations.

Opportunity - Emerging Markets Industrialization and Manufacturing Expansion

Emerging economies across Asia, Africa, and Latin America are experiencing rapid industrialization, resulting in substantial demand for automation systems. India's manufacturing sector is projected to expand from around US$500 billion in 2023 to US$900 billion by 2030, driven by government initiatives including "Make in India" and Production-Linked Incentive (PLI) schemes. Southeast Asian manufacturing hubs, particularly Vietnam, Thailand, and Indonesia, are attracting capital investment fleeing supply chain risks in China, creating new opportunities for deploying automation systems in the forecast years. African nations, including Egypt, Nigeria, and Kenya, are investing in manufacturing infrastructure development, with projected automation system market opportunities exceeding around US$4-6 billion over the next decade. These emerging market opportunities are characterized by greenfield facility development, enabling the adoption of modern automation architectures without legacy system integration constraints, potentially accelerating technology deployment and market penetration.

AI-enabled Defect Detection and Intelligent Inspection Platforms

The convergence of edge computing technologies, artificial intelligence, and industrial control systems creates opportunities for advanced predictive maintenance, autonomous optimization, and real-time adaptive manufacturing. AI-enabled predictive maintenance systems reduce unplanned downtime by 45-55% and decrease maintenance costs by 20-25%, generating substantial value proposition improvements. Edge computing architecture enables real-time data processing at manufacturing facility locations, eliminating cloud infrastructure dependencies and reducing latency-sensitive application constraints. Organizations, including automotive OEMs and advanced chemical manufacturers, are investing heavily in autonomous production line optimization, creating differentiated competitive capabilities and justifying premium automation system pricing, potentially significantly expanding the total addressable market.

Category-wise Analysis

Component Insights

Hardware components, including programmable controllers, distributed I/O modules, industrial computers, sensors, and actuators, constitute the dominant market segment, representing approximately 46%. Hardware installations form the physical foundation of industrial automation infrastructure, with replacement cycles extending 8-12 years, creating recurring revenue opportunities and sustained demand. Major industrial facilities typically contain multiple hardware components, with complex production lines incorporating 100-500+ individual hardware elements.

The automotive manufacturing sector alone, representing 12-15% of global demand for automation hardware, requires sophisticated hardware architectures that support real-time multi-axis control, safety interlocking, and quality assurance functions. Hardware market leadership reflects technological maturity, standardized performance specifications, and established supplier relationships, though competitive pressures are moderating pricing and compressing hardware-specific margins.

Services, spanning integration, consulting, installation, training, and support, are the fastest-growing component, growing at 11.1% CAGR through 2033. Lifetime service revenue surpasses hardware, representing 60-70% of five-year acquisition costs. Complexity, cybersecurity, and advanced software drive demand. Emerging categories such as cloud migration, cybersecurity fortification, and AI integration grow 15-18% annually, with integrators capturing higher-margin value and accelerating market expansion.

System Type Insights

Programmable Logic Controllers (PLCs) and Programmable Automation Controllers (PACs) maintain a dominant market position, commanding around 35% of the market. PLC/PAC systems represent foundational automation building blocks deployed across discrete manufacturing, process industries, and hybrid production environments. The installed base of operational PLC/PAC systems exceeds 50 million units globally, with average replacement cycles of 10-15 years, creating substantial installed base revenues.

Standardized communication protocols (Ethernet/IP, PROFINET, Modbus TCP) and open architecture characteristics enable broad ecosystem development and third-party integration, sustaining competitive advantages and market leadership. PLC/PAC market growth, while more modest than overall market expansion, reflects maturity and established adoption, with primary growth drivers including legacy system replacement, capacity expansion in emerging markets, and enhanced capability integration (cybersecurity, cloud connectivity, edge computing).

Robotics and motion control packages are the fastest-expanding system category, growing at 12.6% CAGR through 2033. Collaborative robots enable semi- or fully automated operations beyond traditional factories. The automotive, electronics, pharmaceutical, and food sectors are accelerating adoption. Labor savings, safety integration, and flexible manufacturing position robotics as core infrastructure for Industry 4.0, while precision motion control commands premium pricing and attracts new investors.

Industry Insights

Manufacturing represents the dominant end-use market, accounting for approximately 24% of total industrial automation and control system expenditures. Discrete manufacturing (automotive, electronics, appliances) and process manufacturing (chemicals, pharmaceuticals, food & beverage) both drive substantial investments in automation. Automotive manufacturing alone represents 10-14% of total global automation system spending, with per-facility automation capital investments for modern assembly facilities. Automation adoption in the manufacturing sector is driven by competitive pressure, labor cost dynamics, quality assurance requirements, and compliance with safety mandates. The sector's market maturity, combined with continuous technology upgrade cycles and geographic expansion into emerging markets (particularly Mexico, India, Vietnam, and Southeast Asia), sustains high-growth demand.

Healthcare is the fastest-growing end-use sector, expanding at 11.3% CAGR through 2033. Pharmaceutical manufacturing, medical device assembly, and laboratory automation drive adoption, supported by compliance with FDA 21 CFR Part 11 and EMA requirements. Personalized medicine, cell and gene therapy, and diagnostic automation are creating new opportunities. Healthcare automation delivers superior performance and stronger long-term service engagement compared to traditional manufacturing segments.

Regional Market Insights

North America Industrial Automation and Control System Market Trends

North America accounts for approximately 27% of the global industrial automation and control systems market. The United States dominates the region, supported by technology maturity, large manufacturing capacity, and strong capital availability. Growth is driven by accelerated adoption of Industry 4.0, reshoring initiatives reversing previous offshoring trends, and major federal investments, including the CHIPS and Science Act funding for domestic semiconductor production. OSHA safety rules, EPA environmental mandates, and evolving cybersecurity requirements sustain automation spending. The region features major global automation suppliers, with enterprises demonstrating a strong willingness to adopt advanced integrated solutions.

North America shows strong adoption of AI-enabled systems, edge computing, and cloud-integrated automation. Sustainability initiatives aim to achieve significant energy reductions through technology deployment. Competitive intensity remains high as major suppliers expand through acquisitions in AI, cybersecurity, and analytics. Key opportunities include legacy facility modernization, reshoring-driven growth in advanced manufacturing, and emerging applications in healthcare, semiconductor production, and clean energy manufacturing.

Europe Industrial Automation and Control System Market Trends

Europe accounts for 24% of the global industrial automation and control system market. Germany, the United Kingdom, France, and Spain drive regional demand, with Germany holding the largest share due to advanced manufacturing depth and automation maturity. Growth is supported by EU regulatory harmonization, Industry 4.0 initiatives, and sustained investment in modern production infrastructure. Energy efficiency, sustainability compliance, and digital factory transformation act as core accelerators. Competitive participation includes multinational suppliers and strong regional integrators, with continued technology deployment across automotive, machinery, electronics, and pharmaceutical manufacturing sectors.

Key growth drivers in the Europe include strict environmental regulations, workforce scarcity in advanced economies, and technological differentiation. EU Machinery Directive, GDPR, and industry-specific standards sustain automation adoption and justify premium pricing. Established European suppliers dominate, emphasizing precision, reliability, and long-term partnerships. At the same time, investment trends focus on green manufacturing, circular economy practices, and digital twin technologies to optimize production and achieve sustainability goals.

Asia Pacific Industrial Automation and Control System Market Trends

Asia Pacific holds 32% of the global industrial automation and control system market and represents the fastest-growing region at 10.3% CAGR through 2033. China dominates due to large-scale manufacturing, export orientation, and government-driven modernization. Japan follows with strong robotics and advanced manufacturing capabilities, while India's rapidly growing production base accelerates adoption. Regional momentum is fueled by digital factory investments, the expansion of the automotive and electronics sectors, and rising sustainability mandates. Multinational suppliers and regional integrators actively compete, while localized automation ecosystems strengthen technology deployment across diverse industrial segments.

ASEAN nations, including Vietnam, Thailand, Indonesia, and Malaysia, are rapidly adopting automation driven by manufacturing expansion, supply chain diversification, and global competitiveness. Growth is supported by rising labor costs and government industrial policies such as China’s “Made in China 2025” and India’s PLI scheme. Regulatory environments vary, with developed markets enforcing strict standards and emerging economies progressively tightening requirements, sustaining long-term automation adoption.

Competitive Landscape

The industrial automation and control system market shows moderate concentration, with top suppliers holding small individual shares and the top ten collectively around two-fifths of global value. The rest is fragmented among regional and niche players. Leaders such as ABB, Siemens, Rockwell, Schneider, and Mitsubishi maintain strength through broad portfolios, distribution networks, and integrated solutions. Technology differentiation, cloud integration, AI, and cybersecurity shape competitive positioning.

Strategic Developments:

- In Oct 2025, SoftBank Group agreed to acquire ABB's robotics business for USD 5.375 billion, consolidating AI-driven robotics innovation. Transaction expected to close mid-to-late 2026, strengthening SoftBank's global AI robotics portfolio and ABB's capital reallocation strategy.

- In January 2025, Siemens unveiled Industrial Copilot for Operations at CES 2025, enabling AI tasks execution directly on shop floors with real-time decision-making capabilities. Integration with Industrial Edge ecosystem accelerates productivity improvements and downtime reduction across manufacturing facilities.

Companies Covered in Industrial Automation and Control System Market

- ABB Ltd.

- Siemens AG

- Rockwell Automation, Inc.

- Schneider Electric SE

- Mitsubishi Electric Corporation

- Johnson Controls International

- Emerson Electric Co.

- Honeywell International Inc.

- Beckhoff Automation

- Omron Corporation

- FANUC Corporation

- Yaskawa Electric Corporation

- B&R Industrial Automation

- IDEC Corporation

Frequently Asked Questions

The global industrial automation and control system market is valued at US$209.16 billion in 2026, projected to reach US$390.51 billion by 2033, with Asia Pacific holding 32%, North America 27%, and Europe 24%.

Growth is driven by Industry 4.0 adoption, labor shortages and rising wages, and stringent regulatory compliance across safety, environmental, and cybersecurity domains.

The Global Industrial Automation and Control System Market is projected to grow at 9.3% CAGR from 2026 to 2033.

Key opportunities include emerging market industrialization, AI-enabled predictive maintenance adoption, and sustainability-driven automation, collectively unlocking significant incremental potential by 2033.

The market is led by ABB, Siemens, Rockwell Automation, Schneider Electric, and Mitsubishi Electric, supported by regional leaders including Beckhoff, Omron, FANUC, Yaskawa, and B&R Industrial Automation.