- Industrial Goods & Service

- Individual Fall Protection Equipment Market

Individual Fall Protection Equipment Market Size, Share, and Growth Forecast, 2026 - 2033

Individual Fall Protection Equipment Market by Product Type (Fall Arrest Systems, Self-Retracting Lifelines, Others), End-Use Industry (Construction, Manufacturing, Others), Component, and Regional Analysis for 2026 - 2033

Individual Fall Protection Equipment Market Size and Trends Analysis

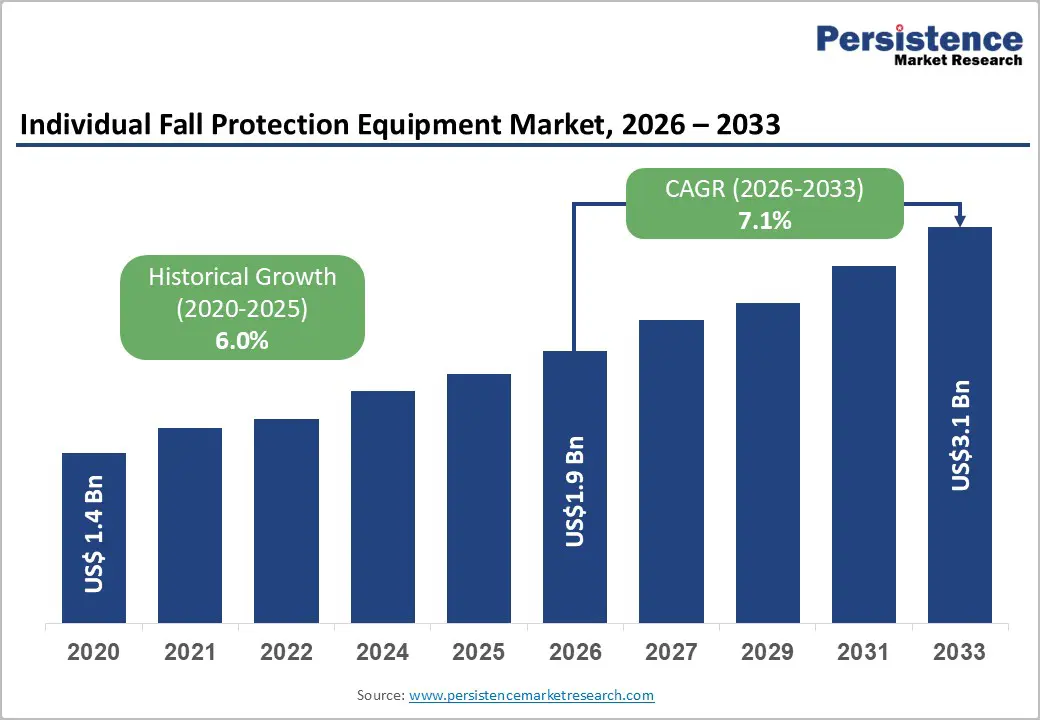

The global individual fall protection equipment market size is likely to be valued at US$1.9 billion in 2026 and is expected to reach US$3.1 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033, driven by stringent workplace safety regulations mandating fall protection in elevated environments. Increasing enforcement of personal protective equipment (PPE) standards, along with rising awareness of occupational safety, is strengthening replacement demand.

Core industries such as construction, manufacturing, energy, and utilities continue to drive consistent demand due to structurally embedded work-at-height activities. A sustained injury burden further reinforces market expansion. Falls remain the leading cause of fatalities in construction, with workplace injury statistics indicating persistent risk exposure. This ensures that fall protection equipment operates within a recurring procurement cycle, as organizations prioritize compliance, workforce safety, and operational continuity.

Key Industry Highlights

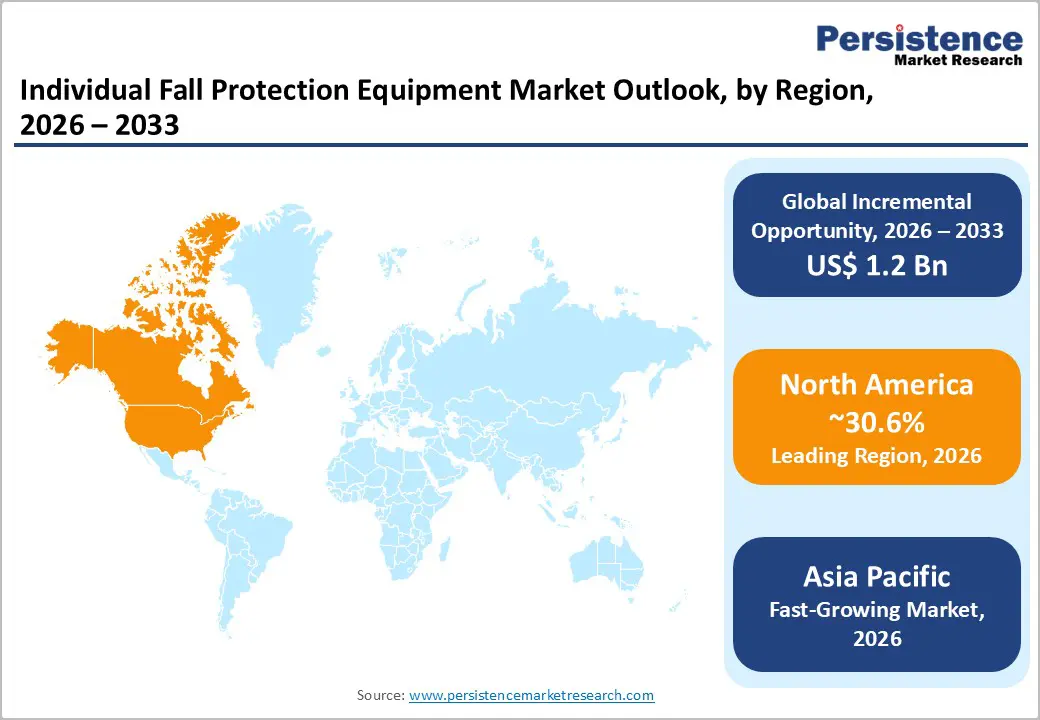

- Leading Region: North America holds the dominant position with an anticipated 30.6% revenue share, driven by stringent regulatory enforcement, high safety compliance standards, and the strong presence of established manufacturers.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing region, supported by rapid industrialization, infrastructure expansion, and increasing adoption of workplace safety regulations across countries such as China and India.

- Investment Plans: Market players are increasingly investing in ergonomic product innovation, digital compliance solutions (QR-enabled tracking, smart inspection systems), and regional manufacturing expansion, particularly in Asia Pacific, to capitalize on high-growth opportunities.

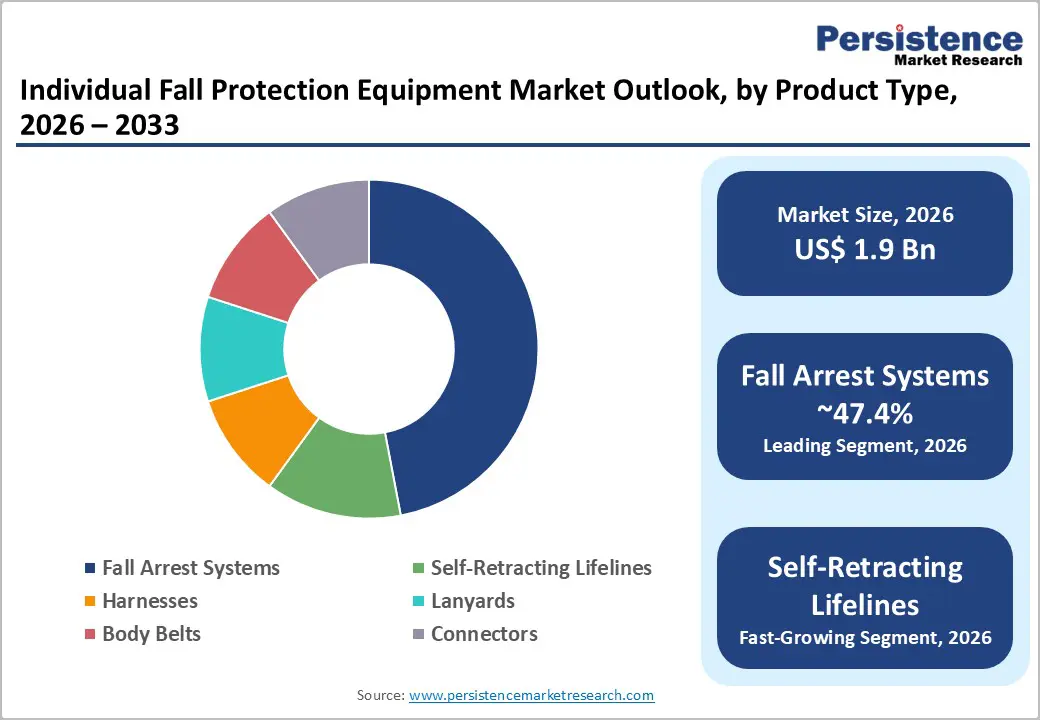

- Dominant Product Type: Fall arrest systems lead the market with an anticipated 47.4% revenue share, driven by mandatory usage across construction, oil & gas, and utilities sectors.

- Leading End-use Industry: Construction dominates with approximately 39.1% revenue share, supported by high exposure to work-at-height activities and strict regulatory requirements for fall protection.

| Key Insights | Details |

|---|---|

| Individual Fall Protection Equipment Market Size (2026E) | US$1.9 Bn |

| Market Value Forecast (2033F) | US$3.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.0% |

DRO Analysis

Driver Analysis - Regulatory Enforcement and PPE Compliance Requirements

Regulatory frameworks remain the most influential driver of demand. Workplace safety regulations mandate fall protection at defined heights, requiring employers to implement certified safety systems. The enforcement of stricter PPE fit requirements, effective January 2025, has increased the emphasis on properly sized and ergonomically designed equipment. Organizations are now prioritizing compliance readiness, audit preparedness, and workforce acceptance when selecting equipment. This shift is particularly evident among large contractors and industrial operators managing multiple sites, where standardized safety protocols are essential. As a result, replacement cycles are accelerating, and demand for advanced, well-documented equipment solutions is increasing.

High Incidence of Fall-Related Workplace Injuries

The persistent prevalence of fall-related incidents continues to drive market demand. Falls represent the leading cause of fatalities in construction and remain a major contributor to workplace injuries across industries. Annual workplace fatality data indicate that construction accounts for a significant share of total occupational deaths, reinforcing the critical need for reliable fall protection systems. This structural risk creates a non-discretionary demand environment, where employers cannot delay or substitute safety investments. Consequently, procurement of harnesses, lifelines, and fall arrest systems remains resilient even during economic slowdowns, ensuring stable long-term market growth.

Product Innovation and Ergonomic Advancements

Technological innovation is reshaping purchasing behavior across the market. Manufacturers are introducing ergonomically enhanced harnesses, self-retracting lifelines (SRLs), and integrated systems designed to improve mobility, comfort, and usability. Recent product developments include features such as reinforced housings, integrated carrying systems, QR-enabled inspection documentation, and improved load distribution designs. These innovations address worker fatigue, ease of use, and inspection efficiency, shifting buyer preference toward performance-based solutions rather than basic compliance products. This trend supports premium pricing strategies and strengthens vendor differentiation in a competitive landscape.

Restraint Analysis - High Total Cost of Ownership

Cost considerations remain a significant barrier, particularly for small and medium-sized contractors. Individual fall protection equipment involves not only initial procurement costs but also ongoing expenses related to inspection, maintenance, certification, and replacement. Equipment used in fall incidents must often be retired, increasing lifecycle costs. For cost-sensitive buyers, especially in developing regions or informal sectors, these expenses can delay adoption or extend replacement cycles. Price competition in commoditized product categories further constrains supplier margins, limiting the ability to fully capitalize on innovation.

Complexity of Training and Proper Equipment Fitting

Effective use of fall protection equipment requires proper training and accurate sizing. The introduction of stricter PPE fit requirements has increased procurement complexity, particularly for organizations with diverse or transient workforces. Employers must manage multiple sizes, conduct training programs, and ensure compliance across all workers. Improper fit can reduce equipment effectiveness and lower worker acceptance, increasing the risk of misuse. This complexity creates operational challenges and may slow adoption in markets with limited safety infrastructure or training capabilities.

Opportunity Analysis - Expansion in Asia Pacific Industrial and Infrastructure Sectors

Asia Pacific represents the most significant growth opportunity due to rapid industrialization and infrastructure development. Countries such as China, India, and those in Southeast Asia are experiencing sustained increases in construction activity, urban infrastructure projects, and manufacturing output. This expansion directly elevates exposure to work-at-height risks across sectors such as commercial construction, transportation infrastructure, and industrial maintenance. The region’s large and cost-sensitive workforce further amplifies the need for scalable and compliant safety solutions. At the same time, governments are progressively tightening occupational safety regulations and enforcement mechanisms, particularly in urban and export-oriented industrial zones. As compliance frameworks mature and awareness improves, adoption rates for fall protection equipment are expected to accelerate, creating long-term, volume-driven growth opportunities for both global and regional manufacturers.

Digital Integration and Premium Product Positioning

The integration of digital technologies into safety equipment presents a high-value and differentiation-driven opportunity for market participants. Features such as QR-based inspection tracking, digital compliance logs, and real-time equipment traceability are gaining traction among large enterprises managing multi-site operations. These capabilities reduce administrative burden, improve audit readiness, and minimize human error in safety compliance processes. At the same time, advancements in ergonomic engineering-such as lightweight materials, enhanced padding, and task-specific configurations-are enabling manufacturers to position products in premium segments. This shift reflects a broader transition from compliance-driven purchasing to performance- and productivity-driven decision-making. Companies that successfully integrate hardware, software, and training services can deliver end-to-end safety solutions, strengthening customer retention and creating recurring revenue streams.

Aftermarket Services and Replacement Demand

The growing installed base of fall protection equipment is generating a sustainable aftermarket revenue stream driven by mandatory inspection, maintenance, and replacement cycles. Regulatory standards and manufacturer guidelines often require periodic equipment checks and immediate replacement following fall incidents or wear-related degradation. This creates predictable demand for components such as harnesses, lifelines, connectors, and shock absorbers. Increasingly, buyers are prioritizing suppliers that offer comprehensive lifecycle management, including inspection services, digital asset tracking, and maintenance contracts. This trend is encouraging the development of service-oriented business models, where vendors move beyond one-time product sales to long-term partnerships. As a result, aftermarket services are emerging as a key profitability driver, improving revenue stability while enhancing customer engagement and safety outcomes.

Category-wise Analysis

Product Type Insights

Fall arrest systems are anticipated to dominate the market, accounting for approximately 47.4% of total revenue share in 2026. Their leadership is driven by mandatory usage across high-risk industries such as construction, oil & gas, utilities, and industrial maintenance, where working at height is unavoidable. These systems are integral to regulatory compliance frameworks and are specifically designed to arrest falls and minimize injury severity. For example, in large-scale infrastructure projects such as bridge construction or high-rise building development, full-body harnesses combined with anchorage systems and shock-absorbing lanyards are standard safety requirements. Their modular configuration allows customization based on site conditions, enabling compatibility with different anchorage points, vertical lifelines, and horizontal systems. This flexibility makes them a central component of enterprise-level safety programs. As enforcement of occupational safety regulations intensifies globally and companies adopt stricter internal safety policies, demand for certified, high-performance fall arrest systems is expected to remain strong, particularly in regulated and high-liability environments.

Self-retracting lifelines (SRLs) are anticipated to be the fastest-growing segment. Their increasing adoption is driven by enhanced mobility, reduced fall clearance requirements, and ease of operation in dynamic work environments. SRLs automatically extend and retract with worker movement, minimizing slack and significantly reducing fall distance compared to traditional lanyards. This makes them especially suitable for applications such as steel erection, tower maintenance, and warehouse operations involving elevated platforms. Recent product innovations include compact and lightweight designs, corrosion-resistant materials for outdoor use, and integrated visual indicators for inspection status. For instance, SRLs are increasingly deployed in wind turbine maintenance and telecom tower installations, where worker mobility and rapid repositioning are critical. As employers focus on improving both safety outcomes and operational efficiency, SRLs are gaining traction as a preferred alternative to conventional fall protection solutions.

End-use Industry Insights

The construction industry is anticipated to lead the market, accounting for approximately 39.1% of revenue share in 2026, driven by the high prevalence of elevated work activities across residential, commercial, and infrastructure projects. Regulatory requirements mandate the use of fall protection systems in tasks such as scaffolding, roofing, façade installation, and structural steel assembly. For example, high-rise developments in urban centers and large-scale infrastructure projects such as metro rail systems and highway bridges require continuous use of harnesses, lifelines, and anchorage systems. The sector’s fragmented workforce, reliance on subcontractors, and high labor turnover further contribute to frequent equipment procurement and replacement cycles. In addition, increasing investment in smart cities and urban infrastructure is expanding the volume of construction activity globally. As safety compliance becomes more strictly enforced and project owners prioritize risk mitigation, the construction segment is expected to maintain its dominant position in the market.

Manufacturing is anticipated to be the fastest-growing end-use segment, supported by industrial expansion, automation, and facility modernization. As manufacturing plants incorporate advanced machinery, multi-level storage systems, and automated production lines, the need for fall protection in maintenance and operational tasks is increasing. Workers frequently access elevated platforms, overhead equipment, and confined spaces, necessitating reliable and flexible safety solutions. For example, in automotive manufacturing plants and large warehousing facilities, workers often perform maintenance on overhead conveyors and robotic systems, requiring the use of SRLs and harness-based systems. The shift toward ergonomic, lightweight, and user-friendly equipment is particularly critical in this segment, where prolonged usage is common. As industries continue to prioritize worker safety alongside productivity and operational efficiency, demand for advanced fall protection equipment in manufacturing is expected to grow steadily.

Regional Insights

North America Individual Fall Protection Equipment Market Trends - Regulation-Driven Demand and Innovation in Ergonomic Fall Protection Systems

North America is projected to lead the market with an anticipated 30.6% revenue share in 2026, driven by strict regulatory enforcement and a mature safety culture. The U.S. is the primary contributor, supported by extensive construction activity, energy infrastructure, and industrial operations. Regulatory frameworks continue to mandate fall protection across multiple industries, with periodic updates reinforcing compliance requirements and proper PPE usage. This creates a stable demand environment characterized by frequent equipment replacement, upgrades, and lifecycle management.

Innovation remains a defining characteristic of the regional market. Companies such as 3M, Honeywell International Inc., and MSA Safety Incorporated are actively investing in advanced product designs, including ergonomic harnesses and leading-edge self-retracting lifelines. For instance, Honeywell’s expansion of its Miller harness portfolio and MSA’s continued focus on SRL innovation are improving worker mobility and compliance efficiency. The region also benefits from a strong distribution network led by companies such as WernerCo, which enhances product accessibility across job sites. Increasing investment in digital compliance tools, training programs, and inspection systems is further strengthening long-term demand and reinforcing North America’s leadership position.

Europe Individual Fall Protection Equipment Market Trends - Standardized Safety Compliance and Advanced Rope-Based Protection Solutions

Europe represents a well-regulated and mature market, with a strong emphasis on workplace safety, compliance, and standardization. Countries such as Germany, the U.K., France, and Spain play a significant role due to their industrial base, infrastructure renewal projects, and stringent labor safety laws. Harmonized PPE regulations across the European Union enable product standardization and facilitate cross-border trade, allowing manufacturers to scale efficiently within the region.

Market demand is supported by both new installations and retrofit projects, particularly as aging infrastructure is upgraded to comply with modern safety standards. Companies such as Petzl and SKYLOTEC GmbH are leading innovation in lightweight harnesses and rope access systems tailored for industrial and rescue applications. For example, Petzl’s advancements in rope-based fall protection solutions are widely adopted in maintenance and industrial access applications, while SKYLOTEC focuses on high-performance safety systems for complex environments. The region’s focus on sustainability and worker welfare is also influencing product design, encouraging the use of durable materials and longer lifecycle equipment. These factors collectively support steady market growth and high product standards across Europe.

Asia Pacific Individual Fall Protection Equipment Market Trends - Infrastructure Expansion Driving Scalable and Cost-Effective Safety Adoption

Asia Pacific is expected to be the fastest-growing region, driven by rapid industrialization, urbanization, and infrastructure development. Countries such as China and India are experiencing significant expansion in construction and manufacturing, leading to increased demand for fall protection equipment. Large-scale infrastructure initiatives, including urban transit systems, high-rise developments, and industrial corridors, are creating substantial exposure to work-at-height risks. The region’s large workforce and evolving regulatory environment provide a strong foundation for market growth. Manufacturing expansion and urbanization remain key drivers, supported by government initiatives aimed at improving workplace safety standards. For instance, India’s increased focus on labor safety compliance in infrastructure and manufacturing projects is encouraging the adoption of certified fall protection systems. Regional players such as Karam Industries are expanding their product portfolios and distribution networks to meet local demand, while global companies such as 3M and Honeywell International Inc. are strengthening their presence through localized manufacturing and partnerships.

Southeast Asian markets are also benefiting from manufacturing relocation trends, increasing the need for standardized safety practices across factories and logistics hubs. As awareness of occupational safety continues to rise and enforcement becomes more consistent, demand for advanced, ergonomic, and cost-effective fall protection solutions is expected to grow significantly across the region.

Competitive Landscape

The global individual fall protection equipment market is moderately fragmented, with a mix of global leaders and regional manufacturers. Leading companies hold significant market share due to their strong brand presence, product innovation, and extensive distribution networks. While premium segments are dominated by established players, lower-cost segments remain highly competitive. Companies differentiate through technology, compliance expertise, and service offerings.

Key players focus on innovation, regulatory compliance, and market expansion. Differentiation is achieved through ergonomic design, advanced materials, and integrated digital features. Companies are also expanding service offerings, including training and lifecycle management, to strengthen customer relationships and drive recurring revenue.

Key Industry Developments

- In September 2025, MSA Safety Incorporated introduced two new safety solutions at the National Safety Congress, including the V-Gard H2® Full Brim Safety Helmet and the ALTAIR io™ 6 connected multigas detector, reinforcing its strategy to integrate connected safety technologies and expand its industrial safety ecosystem across construction and utilities applications.

- In May 2025, MSA Safety Incorporated announced the acquisition of M&C TechGroup, a gas analysis technology provider, to strengthen its connected safety and monitoring capabilities, supporting broader integration of smart technologies into industrial safety solutions.

Companies Covered in Individual Fall Protection Equipment Market

- 3M

- Honeywell International Inc.

- MSA Safety Incorporated

- WernerCo

- Guardian Fall Protection

- SKYLOTEC GmbH

- Petzl Group

- FallTech

- Karam Industries

- Kee Safety Group

- Tractel Group

- Protective Industrial Products (PIP)

- FrenchCreek Production

- Safewaze

- DBI-SALA

- Capital Safety

Frequently Asked Questions

The global individual fall protection equipment market is estimated to be valued at US$1.9 billion in 2026.

The individual fall protection equipment market is projected to reach approximately US$3.1 billion by 2033.

Key trends include growing adoption of self-retracting lifelines (SRLs), increasing focus on ergonomic and lightweight harness designs, and the integration of digital compliance tools such as QR-based inspection tracking and smart safety systems.

Fall arrest systems are the leading product segment, accounting for approximately 47.4% of the market share, due to their mandatory use in high-risk industries.

The individual fall protection equipment market is expected to grow at a CAGR of 7.1% from 2026 to 2033.

Some of the companies include 3M, Honeywell International Inc., MSA Safety Incorporated, WernerCo, and Petzl.