- Animal Feed & Additives

- India Pet Food Market

India Pet Food Market Size, Share, and Growth Forecast 2026 - 2033

India Pet Food Market by Product Type (Food, Pet Nutraceuticals/Supplements, Pet Treats, Pet Veterinary Diets), by Pet (Cats, Dogs), Distribution Channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets), and Regional Analysis, 2026 - 2033

India Pet Food Market Size and Trend Analysis

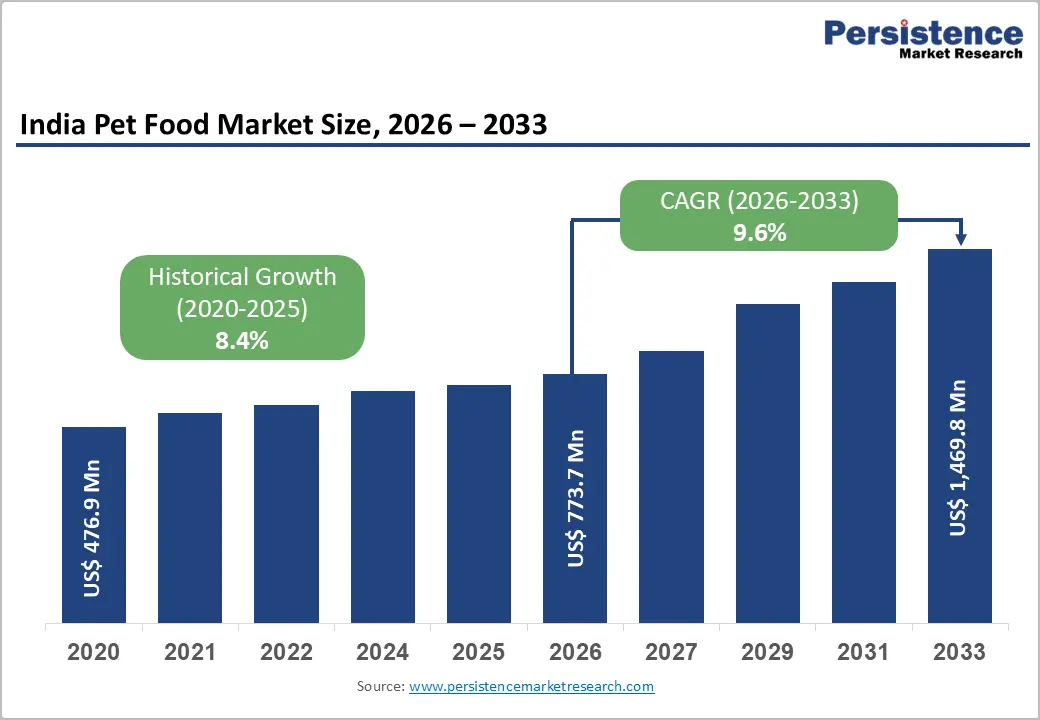

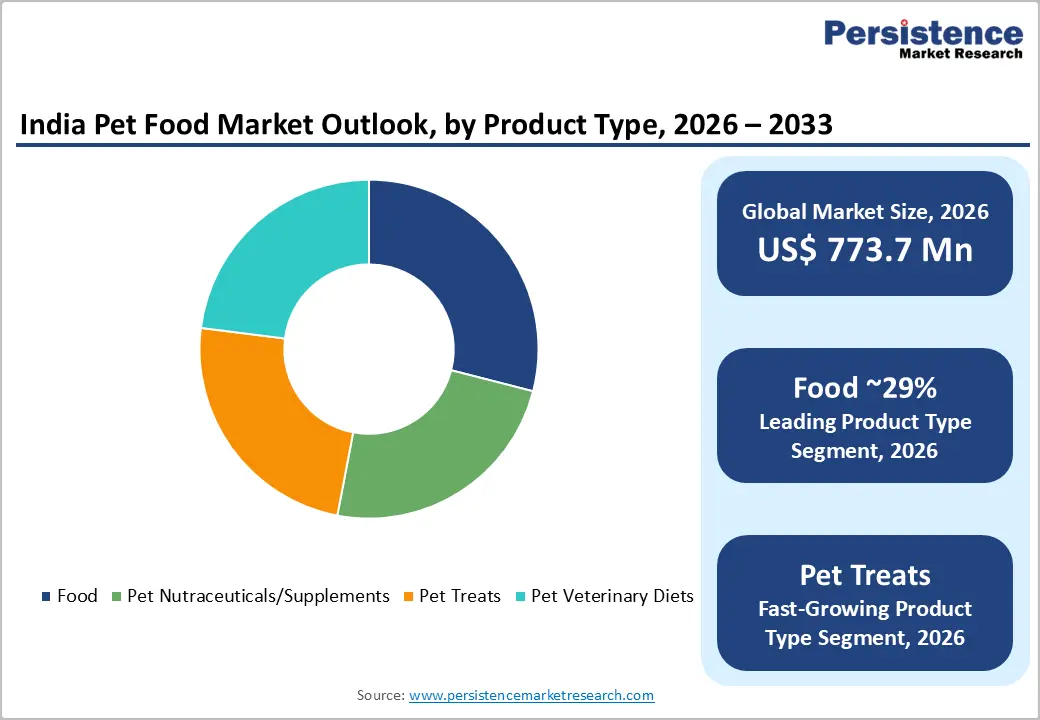

India pet food market size is expected to be valued at US$ 773.7 million in 2026 and projected to reach US$ 1,469.8 million by 2033, growing at a CAGR of 9.6% between 2026 and 2033. It is witnessing strong growth, supported by rising pet ownership and evolving consumer attitudes toward animal care. Increasing urbanization, higher disposable incomes, and the growing trend of pet humanization are encouraging owners to shift from traditional feeding practices to nutritionally balanced, packaged pet food.

Younger demographics, particularly millennials and Gen Z, are driving adoption, while awareness around pet health and wellness continues to improve. Additionally, the rapid expansion of e-commerce platforms and organized retail channels has enhanced product accessibility across urban and semi-urban areas. Veterinary recommendations and premium product offerings are further shaping purchasing behavior, positioning the market for sustained long-term expansion.

Key Industry Highlights:

- Leading Region: West India leads the India pet food market with around 34% share in 2025, driven by Maharashtra’s metros, higher incomes, nuclear families, and strong presence of global manufacturers.

- Fastest Growing Region: East India is the fastest-growing region, supported by urbanization in Kolkata and Bhubaneswar, shifting attitudes toward pets, rising e-commerce penetration, and increasing domestic brand investments.

- Dominant Product Segment: The food segment dominates with about 29% share in 2025, driven by dry pet food’s convenience, affordability, longer shelf life, and growing preference for scientifically formulated diets.

- Fastest Growing Segment: Pet Treats is the fastest-growing segment, projected at around 10.3% CAGR through 2033, driven by humanization trends, demand for natural snacks, D2C expansion, and innovative product offerings.

- Key Market Opportunity: Veterinary diets and nutraceuticals offer strong opportunities, supported by expanding veterinary infrastructure, growing pet insurance adoption, and rising lifestyle-related diseases among companion animals, driving specialized nutrition demand.

Market Dynamics

Drivers - Pet Humanization and Premiumization Driving Demand for High-Quality Nutrition

The growing trend of treating pets as family members is fundamentally transforming feeding habits across India. Millennials and Gen Z now account for 68% of first-time pet adopters in India, emphasizing emotional bonds and seeking premium, scientifically backed nutrition for their companions. These demographic fuels strong demand for grain-free formulations, single-protein recipes, and functional treats enriched with probiotics or omega-3 fatty acids. These categories, which had minimal shelf presence in 2020, surged to represent 18% of specialty-store revenue by 2025.

Premium and super-premium segments grew at over 20% annually in 2024, significantly outpacing overall market growth. The rise in apartment-dwelling small-breed ownership with breeds such as Shih Tzus, Beagles, and Labradors gaining popularity is further reinforcing the demand for calorie-specific and breed-specific commercial diets, providing sustained structural tailwinds for the India pet food market.

Rapid E-Commerce Expansion and Strengthening Retail Infrastructure

E-commerce has emerged as a pivotal driver of the India pet food market, enabling brands to access consumers in Tier-2 and Tier-3 cities beyond traditional metro strongholds. According to the Unicommerce 2025 Report, India's online pet care segment recorded approximately 95% year-on-year growth in FY25. Quick-commerce delivery, now covering 42 cities, is shortening replenishment cycles and accelerating trial among first-time buyers. Simultaneously, India's broader e-commerce market reached US$ 107.7 billion in 2024, with expanding digital penetration benefiting pet food brands.

Large retail chains such as Reliance Fresh, Big Bazaar, and D-Mart are progressively dedicating more shelf space to pet food, while specialty pet stores provide curated, high-value product assortments. This omnichannel infrastructure growth is dramatically widening market reach and customer acquisition, reinforcing volume and value uptake.

Restraints - High Price Sensitivity and Low Penetration in Semi-Urban and Rural Areas

Despite rapid urban growth, the India pet food market faces significant penetration challenges in non-metro geographies. In Tier-2 cities such as Jaipur, Lucknow, and Visakhapatnam, packaged food penetration lags below 20% owing to price sensitivity and limited retail access. Northern states, including Uttar Pradesh, Bihar, and Madhya Pradesh, collectively account for only 12% of national market revenue, driven by lower per-capita incomes and a cultural preference for feeding pets household leftovers. Daily feeding of commercial diets remains low at 29% of the owned-dog population, reflecting the vast market gap that persists between awareness and adoption.

Opportunities - Pet Nutraceuticals and Veterinary Diet Segment Offering High-Growth Revenue Potential

The growing awareness of preventive pet healthcare is creating a significant opportunity in pet nutraceuticals, supplements, and veterinary diets segments, exhibiting demand well ahead of conventional food categories. In April 2024, HDFC ERGO launched India's first comprehensive pet insurance product, 'Paws n Claws,' for dogs and cats aged 3 months to 10 years, which reimburses up to 80% of costs for therapeutic diets prescribed for conditions such as renal disease, diabetes, or obesity.

The policy covers annual premiums between INR 5,000 and INR 15,000. Such financial instruments are effectively subsidizing high-value veterinary nutrition products (priced at INR 800 to INR 1,200 per kg) from brands like Hill's Prescription Diet and Royal Canin Veterinary Range, unlocking a structurally new consumer base for condition-specific and life-stage nutrition. As the veterinary infrastructure with over 12,000 hospitals and polyclinics across India as of FY2022 continues to grow, this segment holds highly attractive long-term commercial upside.

Category-wise Analysis

Product Type Insights

The food segment dominates India pet food market, accounting for 29% of the total share in 2025, making it the undisputed leading product category. This leadership is anchored in dry pet food's widespread appeal, driven by its convenience, long shelf life, affordability, and ease of portion control compared to wet food alternatives.

Dry food is particularly suited to India's urban households, where storage space and refrigeration may be limited. According to IMARC Group, dry pet food accounted for 89.6% of total Indian pet food sales in 2024. Manufacturers are further enhancing the product's appeal by fortifying kibble with vitamins, minerals, probiotics, and breed-specific functional ingredients. The segment benefits from well-established supply chains, strong veterinary endorsements, and wide retail distribution through supermarkets, pet specialty stores, and e-commerce channels, ensuring consistent penetration across both metro and emerging Tier-2 markets.

Pet Type Insights

Dogs represent the dominant pet type in India's pet food market, accounting for the largest revenue share in 2025, with dogs comprising over 85% of the total pet-type segment. India's pet dog population stood at approximately 31 million in 2024, with an annual addition of around 2 million companion animals in metro areas, according to industry estimates based on veterinary clinic registrations. The well-established cultural familiarity with dogs, combined with rising preference for branded feeding over home-cooked diets, reinforces the segment's leadership.

Meanwhile, the cat segment, though smaller at approximately 5.5 million domestic cats and representing 9.5% of the pet population as of 2023, is growing rapidly. Rising apartment-living culture, social media influence, and increasing awareness of cat-specific nutrition are accelerating adoption, with cat food commanding higher average selling prices due to fish-based formulations and imported treats.

Distribution Channel Insights

By distribution channel, the pet food market is segregated into convenience stores, online channel, specialty stores, and supermarkets/hypermarkets. Online channel is expected to dominate by holding nearly 32% India pet food market share in 2025. Growth is primarily driven by the increasing shift of pet owners toward convenience. Online platforms provide a wide range of products from multiple brands and price ranges. Hence, owners can easily choose the desired product to get it delivered at their doorstep.

Supermarkets/hypermarkets are speculated to showcase steady growth in the forecast period due to their ability to offer trust-based physical visibility and instant availability. Ongoing expansion of modern retail outlets in semi-urban and urban areas is projected to create opportunities for brands to gain consumer recall. As per a study, in 2023, in India, organized retail formats accounted for over 20% of total pet food sales. This number is poised to surge in the future with the rapid expansion of chains such as Spencer’s and Reliance Smart.

Regional Insights

West India Pet Food Market Trends and Insights

West India leads the India pet food market with 34% of total market share in 2025, anchored by the pet-friendly cultures of Mumbai and Pune in Maharashtra. The region's higher disposable incomes, nuclear family structures, and prevalence of pet-friendly apartment housing have accelerated pet adoption, particularly among urban millennials. Maharashtra leads within the region as pet adoption rates skyrocket in cities such as Nashik, Nagpur, Mumbai, and Pune. Major global players, including Mars, Incorporated and Royal Canin have established manufacturing bases in Maharashtra, benefiting from supply chain efficiencies and accelerated product launch cycles. In July 2024, the Tata Trusts Small Animal Hospital was inaugurated in Mumbai to provide 24/7 emergency veterinary care, further strengthening the region's premium pet care ecosystem.

The region's regulatory alignment with FSSAI standards ensures product quality and reinforces consumer trust in packaged nutrition. West India's robust organized retail infrastructure, encompassing specialty stores, modern trade, and fast-growing e-commerce platforms, provides brands with a strong multi-channel consumer reach. Mars, Incorporated introduced breed-specific Pedigree SKUs in June 2024, tailored to apartment residents, resulting in a 22% increase in trial rates within the first quarter of launch, reflecting the innovation-driven growth dynamic that characterizes this leading regional market.

East India Pet Food Market Trends and Insights

East India represents the fastest-growing regional segment in India pet food market, with Kolkata serving as the primary consumption hub. While the region currently holds a smaller share relative to West and North India, it is witnessing accelerating growth driven by expanding urbanization, rising middle-class incomes, and a generational shift in attitudes toward pet ownership. Younger demographics in cities such as Kolkata and Bhubaneswar are increasingly adopting pets as companions rather than for traditional guard roles, creating fresh demand for commercial packaged food. E-commerce platforms are proving critical in bridging the retail access gap in the region, enabling brands to reach first-time pet owners with competitive pricing, convenience, and variety.

The expansion of quick-commerce delivery across an increasing number of Indian cities is shortening purchase cycles and catalyzing first-time buyer trials in East India. Domestic brands such as Drools (IB Group) and Purepet are actively targeting eastern markets through affordably priced, locally relevant product portfolios. As per APEDA data, India's pet food exports including to neighboring markets in the east grew by 35% in 2024 versus the prior year, highlighting the broader regional expansion dynamic. With growing veterinary infrastructure and increasing digital penetration, East India is poised to emerge as a significant growth engine for the national pet food market through 2033.

Competitive Landscape

The India pet food market displays moderate consolidation, with the top five players Mars, Incorporated; Nestlé (Purina); IB Group (Drools); Colgate-Palmolive (Hill's Pet Nutrition); and Royal Canin commanding a significant portion of organized market revenue. Multinational players dominate the premium and veterinary nutrition segments through established brand equity, R&D capabilities, and wide distribution networks, while domestic manufacturers such as Drools and Farmina Pet Foods are aggressively targeting mid-market and Tier-2 consumers. Key competitive strategies include D2C channel investment, subscription-based models, vet-partnered marketing, and premiumization through breed- and condition-specific formulations. Emerging business models center on omnichannel retail, AI-driven personalized nutrition, and sustainability-focused packaging innovations.

Key Developments:

- In April 2026, Indian pet food brand Benny's Bowl secured approximately $1.4 million in a pre-Series A funding round led by Atomic Capital, aiming to invest in research and development, expand its product portfolio, and strengthen distribution across major Indian cities.

- In December 2025, Mankind Pharma announced the launch of PetStar Delight, expanding its PetStar portfolio into the cat food segment. The new range is designed to support overall feline wellness and represents a key milestone in the company’s pet care journey, following the introduction of PetStar dog food.

- In April 2025, a subsidiary of Godrej Consumer Products, Godrej Pet Care, introduced Godrej Ninja, its pet food brand in Tamil Nadu. The brand provides dog food scientifically formulated to enhance immunity and gut health.

- In March 2025, Avanti Pet Care launched a new cat food brand to mark its presence in India’s pet food industry. The company joined hands with Bluefalo Group, a Thailand-based pet food company, to launch the new product.

India Pet Food Market - Key Insights & Scope

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 476.9 Million |

| Projected Market Value (2026) | US$ 773.7 Million |

| Projected Market Value (2033) | US$ 1,469.8 Million |

| CAGR (2026 - 2033) | 9.6% |

| Leading Region | West India, 34% share |

| Dominant Product Type | Food, 29% share |

| Top-ranking Distribution Channel | Online, 32% |

| Incremental Opportunity | US$ 696.1 Million |

Companies Covered in India Pet Food Market

- ADM

- FARMINA PET FOODS

- Charoen Pokphand Group

- General Mills Inc.

- Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- IB Group (Drools Pet Food Pvt. Ltd.)

- Nestle (Purina)

- Mars Incorporated

- Virbac

- Schell & Kampeter Inc. (Diamond Pet Foods)

- Others

Frequently Asked Questions

India pet food market is expected to be valued at US$ 773.7 million in 2026.

The growing acceptance of pets as family members and the increasing demand for condition-specific food are the key market drivers.

The market is poised to witness a CAGR of 9.6% from 2026 to 2033.

Increasing investments of key companies to strengthen online presence and high demand for plant-based pet food are the key market opportunities.

The leading companies in India Pet Food Market include ADM, FARMINA PET FOODS, and Charoen Pokphand Group, among others.