- Oil & Gas

- Hydraulic Fracturing Market

Hydraulic Fracturing Market Size, Share, and Growth Forecast, 2026 - 2033

Hydraulic Fracturing Market by Technology (Plug and Perf, Sliding Sleeve, Others), Application (Shale Gas, Tight Oil, Others), Material, and Regional Analysis for 2026 - 2033

Hydraulic Fracturing Market Size and Trends Analysis

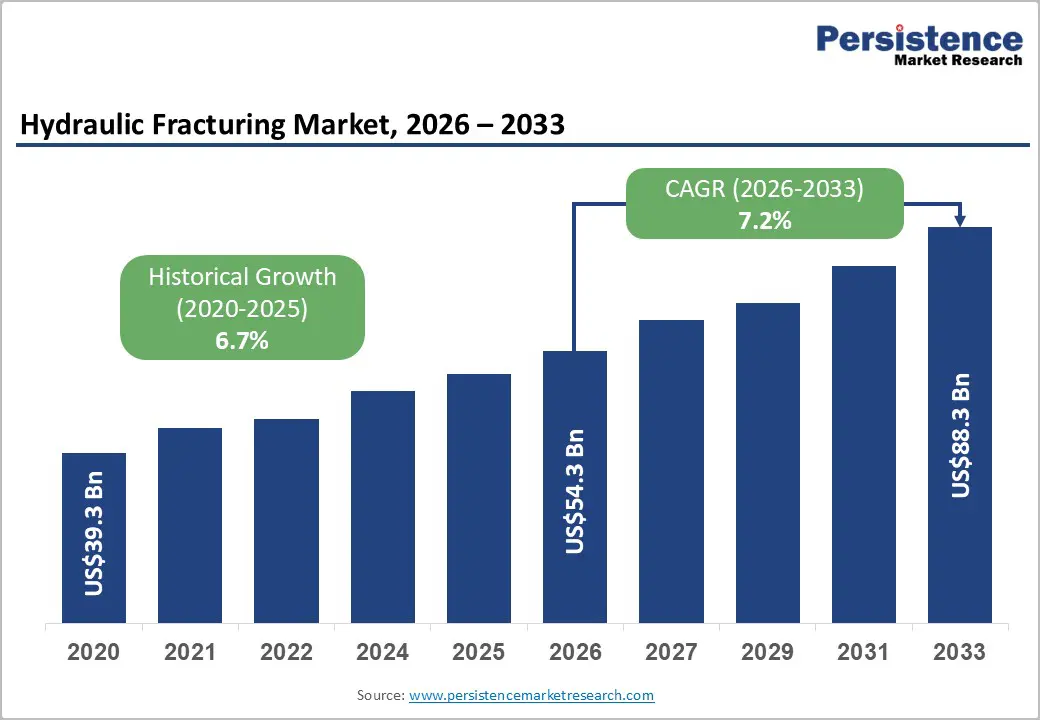

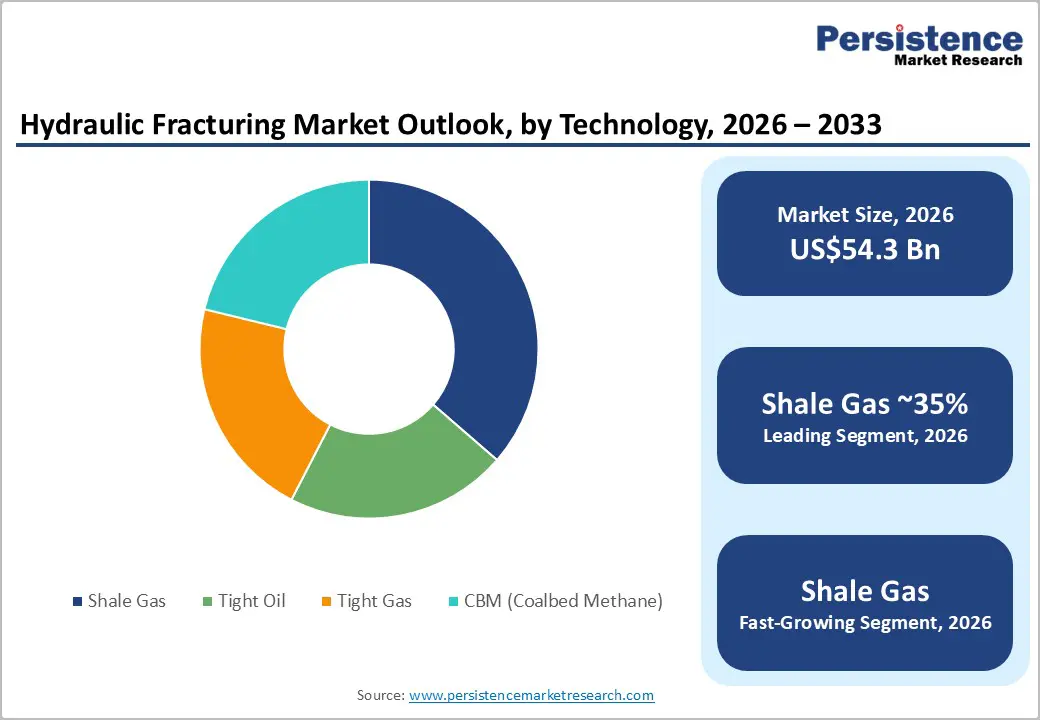

The global hydraulic fracturing market size is likely to be valued at US$54.3 billion in 2026 and is expected to reach US$88.3 billion by 2033, growing at a CAGR of 7.2% during the forecast period from 2026 to 2033, driven by sustained investment in unconventional oil and gas resources, increasing drilling activity across major shale basins, and the adoption of advanced completion technologies.

Growing demand for energy security, rising natural gas consumption, and improvements in hydraulic fracturing efficiency are supporting market growth. Technological advancements in automation, digital monitoring, and low-emission fracturing systems are improving operational productivity while helping operators address environmental and regulatory requirements.

Key Industry Highlights:

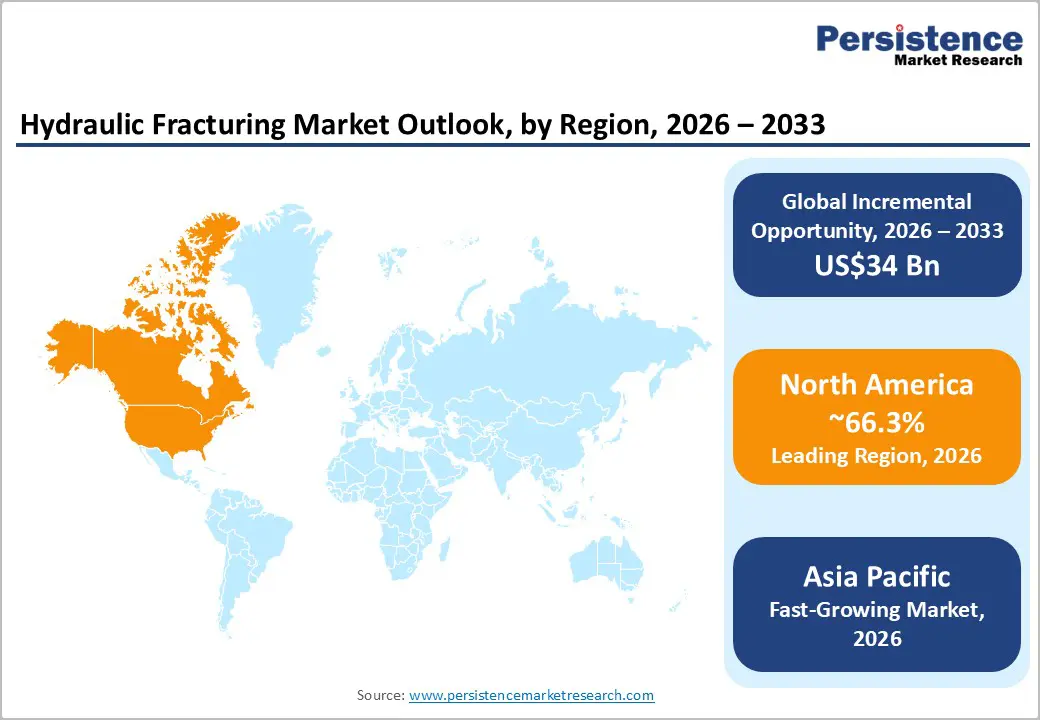

- Leading Region: North America is projected to account for 66.3% of market share in 2026, driven by extensive shale developments across the Permian Basin, Marcellus Shale, Eagle Ford, and Bakken formations, supported by advanced completion technologies and a mature oilfield services ecosystem.

- Fastest-growing Region: Asia Pacific is supported by rising shale gas development in China, increasing energy security initiatives in India, and growing unconventional resource exploration across ASEAN countries.

- Dominant Technology: The plug and perf segment is anticipated to account for 84% of market share in 2026, owing to its superior stage isolation capabilities, compatibility with horizontal drilling, and widespread adoption in major shale basins.

- Leading Application: Shale gas is estimated to hold 35% of the market share in 2026, supported by growing natural gas demand, expanding LNG infrastructure, and continued development of unconventional gas reserves globally.

DRO Analysis

Drivers - Growing Development of Unconventional Oil and Gas Resources

The expansion of unconventional oil and gas production remains the primary driver of the hydraulic fracturing market. Shale gas, tight oil, and tight gas reservoirs require advanced stimulation techniques to achieve commercial production levels. Hydraulic fracturing has become an essential component of resource extraction in major producing regions, particularly across North America. The continued development of large shale basins, including the Permian, Marcellus, Eagle Ford, and Bakken formations, supports consistent demand for pressure pumping services, fracturing fluids, and proppants.

Energy security concerns and increasing global natural gas consumption are encouraging governments and operators to maximize domestic hydrocarbon production. As drilling activity increases and well completion intensity rises, hydraulic fracturing service providers benefit from recurring demand for equipment deployment, consumables, and field operations. This long-term dependence on unconventional resources is expected to sustain market growth throughout the forecast period.

Technological Advancements in Automated and Electrified Fracturing Systems

Technological innovation is significantly improving the economics of hydraulic fracturing operations. Service providers are increasingly deploying automated pumping systems, real-time monitoring platforms, intelligent completion technologies, and electrified fracturing fleets. These solutions enhance stage consistency, improve resource recovery rates, reduce operational downtime, and lower fuel consumption.

Electrified fleets and natural gas-powered pumping systems are helping operators reduce emissions while improving operating efficiency. Digital completion technologies enable real-time adjustments during stimulation activities, allowing operators to optimize fracture placement and maximize reservoir contact. These advancements are increasing productivity while reducing overall operating costs, making hydraulic fracturing more attractive for both established and emerging unconventional developments. As operators prioritize efficiency and environmental performance, adoption of advanced fracturing technologies is expected to accelerate.

Restraint - Increasing Environmental Regulations and Compliance Costs

Environmental concerns surrounding water usage, wastewater disposal, methane emissions, and groundwater protection remain significant challenges for the hydraulic fracturing industry. Regulatory authorities across several regions continue to implement stricter requirements for emissions monitoring, methane leak detection, wastewater treatment, and operational transparency.

Compliance with evolving environmental standards increases operational expenses and may extend project approval timelines. Companies are often required to invest in advanced water recycling systems, emissions-control technologies, environmental monitoring equipment, and reporting frameworks. Public opposition to hydraulic fracturing activities in certain jurisdictions can further delay project development and increase regulatory uncertainty. These factors create additional financial and operational burdens for service providers and exploration companies, potentially limiting market expansion in environmentally sensitive regions.

Opportunities - Expansion of Low-Emission and Electrified Fracturing Operations

The growing emphasis on sustainability presents a major opportunity for hydraulic fracturing service providers. Operators are increasingly adopting low-emission technologies to reduce diesel consumption, lower greenhouse gas emissions, and improve operational efficiency. Electrified pumping fleets, natural gas-powered engines, automated controls, and digital optimization platforms are gaining traction across major shale-producing regions.

As environmental performance becomes a key procurement criterion, service providers capable of delivering measurable emissions reductions are expected to secure premium contracts and strengthen customer relationships. The commercialization of advanced completion technologies also creates opportunities for equipment manufacturers, software providers, and engineering service companies participating in the hydraulic fracturing value chain.

Rising Unconventional Resource Development across Asia Pacific

Asia Pacific represents one of the most attractive growth opportunities for the hydraulic fracturing market. Governments across the region are seeking to strengthen energy security through domestic resource development while reducing dependence on imported energy supplies. Significant investments in shale gas exploration, tight gas production, and unconventional resource assessment are creating new opportunities for hydraulic fracturing technologies and services.

China remains the leading growth engine within the region due to large shale gas reserves and increasing production activity. India and several Southeast Asian countries are also evaluating unconventional resource potential, creating long-term opportunities for drilling contractors, pressure pumping service providers, and proppant suppliers. As technical expertise and infrastructure continue to improve, Asia Pacific is expected to emerge as a key contributor to future market growth.

Category-wise Analysis

Technology Insights

The plug and perf segment is anticipated to account for approximately 84% of the market share in 2026, maintaining its position as the dominant technology segment. Its leadership is driven by superior stage isolation, operational flexibility, and compatibility with long horizontal wells used in major shale formations. The technology is widely deployed across the Permian Basin, Eagle Ford, and Marcellus shale plays, where operators require precise fracture placement to maximize hydrocarbon recovery.

The plug and perf segment is also anticipated to register the fastest growth through 2033. Growth is supported by increasing horizontal drilling activity, rising completion intensity, and continued adoption of automated completion technologies. Major operators such as Chevron, ConocoPhillips, and EOG Resources increasingly utilize plug and perf systems to improve well productivity and reservoir contact.

Application Insights

Shale gas is anticipated to account for approximately 35% of the market share in 2026, making it the largest application segment. Demand is driven by growing natural gas consumption, LNG export expansion, and continued development of unconventional gas reserves. Major shale gas-producing regions such as the Marcellus, Haynesville, and Permian basins continue to generate substantial demand for fracturing services, proppants, and completion technologies.

Shale gas is also anticipated to be the fastest-growing application segment. Rising energy security concerns, increasing natural gas demand, and improvements in drilling efficiency are supporting sustained investment in shale gas production across North America and emerging Asian markets, particularly China.

Regional Insights

North America Hydraulic Fracturing Market Trends

North America is anticipated to account for approximately 66.3% of the market share in 2026, maintaining its position as the leading regional market. Strong unconventional resource development, advanced oilfield service infrastructure, and continuous technological innovation support regional growth.

U.S. Hydraulic Fracturing Market Trends

The U.S. is expected to represent approximately 79% of the North America market share in 2026, driven by extensive shale developments across the Permian Basin, Marcellus Shale, Eagle Ford, and Bakken formations. Continued investments in horizontal drilling, longer lateral wells, and high-intensity completion programs support demand for fracturing services. Major operators are increasingly adopting automated fracturing systems, electrified fleets, and digital completion technologies to improve productivity and lower operating costs.

Canada Hydraulic Fracturing Market Trends

Canada is expected to account for approximately 21% of regional revenue share in 2026, supported by unconventional oil and gas activity in Alberta and British Columbia. The country continues to invest in emissions reduction initiatives, water recycling technologies, and operational efficiency improvements. Increasing focus on environmentally responsible resource development is encouraging adoption of advanced fracturing solutions and lower-emission equipment.

North America's mature infrastructure, abundant shale resources, and strong technological capabilities are expected to sustain regional market leadership throughout the forecast period.

Europe Hydraulic Fracturing Market Trends

Europe represents a comparatively smaller share of the global hydraulic fracturing market but remains strategically important due to its strong regulatory framework, technological expertise, and focus on environmental sustainability.

U.K. Hydraulic Fracturing Market Trends

The U.K. remains one of the region's most technically advanced markets for unconventional resource evaluation. While regulatory restrictions continue to influence large-scale shale development, the country maintains strong capabilities in drilling technologies, reservoir engineering, and energy infrastructure development.

Germany Hydraulic Fracturing Market Trends

Germany's hydraulic fracturing market is shaped primarily by strict environmental regulations and energy transition policies. Demand is concentrated around advanced monitoring technologies, emissions management systems, and engineering services designed to improve operational compliance and sustainability.

France Hydraulic Fracturing Market Trends

France maintains a cautious approach toward hydraulic fracturing development while prioritizing environmental protection and emissions reduction. Opportunities primarily exist in environmental monitoring, water management technologies, and energy-sector innovation.

Spain Hydraulic Fracturing Market Trends

Spain continues to evaluate domestic energy resources while investing in energy security and infrastructure modernization. The market offers opportunities for technology providers supporting reservoir analysis, emissions monitoring, and operational optimization.

Across Europe, methane reduction requirements, environmental compliance measures, and sustainability objectives are expected to drive demand for advanced monitoring systems, digital technologies, and engineering solutions.

Asia Pacific Hydraulic Fracturing Market Trends

Asia Pacific is anticipated to be the fastest-growing regional market through 2033, driven by increasing energy demand, industrialization, urbanization, and efforts to strengthen domestic energy security.

China Hydraulic Fracturing Market Trends

China remains the largest hydraulic fracturing market in Asia Pacific due to significant investments in shale gas exploration and production. The country continues to expand unconventional resource development through advanced drilling technologies, precision fracturing techniques, and improved reservoir characterization. Major shale gas projects in the Sichuan Basin continue to drive demand for pressure pumping services and completion technologies.

India Hydraulic Fracturing Market Trends

India is increasingly exploring domestic unconventional oil and gas resources to reduce dependence on imported energy. Government initiatives supporting exploration and production activities are expected to create long-term opportunities for hydraulic fracturing service providers, equipment manufacturers, and technology developers.

Japan Hydraulic Fracturing Market Trends

Japan contributes primarily through technological innovation, equipment manufacturing, and energy infrastructure investment. The country's expertise in engineering, automation, and energy technologies supports the broader development of advanced hydraulic fracturing solutions across the region.

Competitive Landscape

The global hydraulic fracturing market exhibits a moderately consolidated structure at the global level, with several large multinational service providers maintaining strong market positions through technological expertise, extensive service portfolios, and established customer relationships. Competition is based on operational efficiency, technology innovation, equipment reliability, emissions reduction capabilities, and service quality.

Leading companies continue to invest heavily in automation, digital completion technologies, electrified fleets, and advanced stimulation solutions to differentiate their offerings and improve profitability. Leading companies are focusing on automation, electrification, digital transformation, emissions reduction, and geographic expansion to strengthen competitive positioning. Investments in advanced completion technologies, data analytics, and environmentally responsible operating practices are becoming key differentiators. Strategic partnerships and technology collaborations continue to accelerate innovation and support long-term market growth.

Key Industry Developments:

- In January 2025, Halliburton and Coterra Energy announced the launch of North America's first fully automated hydraulic fracturing program using Halliburton's Octiv® Auto Frac service, part of the ZEUS intelligent fracturing platform.

- In June 2025, Halliburton expanded the capabilities of its ZEUS IQ™ intelligent fracturing platform through its collaboration with Chevron, integrating OCTIV® Auto Frac automation and Sensori™ monitoring technologies to deliver real-time completion optimization and enhanced reservoir performance.

Companies Covered in Hydraulic Fracturing Market

- Halliburton Company

- SLB

- Baker Hughes Company

- Liberty Energy Inc.

- Weatherford International plc

- ProPetro Holding Corp.

- Calfrac Well Services Ltd.

- Trican Well Service Ltd.

- NexTier Oilfield Solutions Inc.

- Patterson-UTI Energy, Inc.

- RPC, Inc.

- Cudd Energy Services

- FTS International, Inc. (FTSI)

- STEP Energy Services Ltd.

- Nabors Industries Ltd.

- Basic Energy Services, Inc.

Frequently Asked Questions

The global hydraulic fracturing market is estimated to be valued at US$54.3 billion in 2026.

The hydraulic fracturing market is projected to reach US$88.3 billion by 2033.

Key trends include the adoption of automated fracturing systems, electrified pressure pumping fleets, digital completion technologies, low-emission stimulation solutions, and increased shale gas development across North America and Asia Pacific.

Plug and perf is the leading technology segment, accounting for approximately 84% of the market share, owing to its effectiveness in multistage horizontal well completions and enhanced reservoir stimulation efficiency.

The hydraulic fracturing market is anticipated to grow at a CAGR of 7.2% between 2026 and 2033.

Major companies include Halliburton, SLB, Baker Hughes, Liberty Energy, Weatherford International.