- Executive Summary

- Global HVAC Insulation Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Residential HVAC Industry Overview

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 – 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global HVAC Insulation Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Global HVAC Insulation Market Outlook: Product Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Product Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Pipes

- Ducts

- Market Attractiveness Analysis: Product Type

- Global HVAC Insulation Market Outlook: Material Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Material Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Material Type, 2026-2033

- Mineral Wool

- Glass Wool

- Stone Wool

- Plastic Foam

- Phenolic, PIR & PUR

- Elastomeric Foam

- Polyethylene

- Mineral Wool

- Market Attractiveness Analysis: Material Type

- Global HVAC Insulation Market Outlook: End-use Industry

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by End-use Industry, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by End-use Industry, 2026-2033

- Residential

- Commercial

- Industrial

- Market Attractiveness Analysis: End-use Industry

- Global HVAC Insulation Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America HVAC Insulation Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Pipes

- Ducts

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Material Type, 2026-2033

- Mineral Wool

- Glass Wool

- Stone Wool

- Plastic Foam

- Phenolic, PIR & PUR

- Elastomeric Foam

- Polyethylene

- Mineral Wool

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by End-use Industry, 2026-2033

- Residential

- Commercial

- Industrial

- Europe HVAC Insulation Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Pipes

- Ducts

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Material Type, 2026-2033

- Mineral Wool

- Glass Wool

- Stone Wool

- Plastic Foam

- Phenolic, PIR & PUR

- Elastomeric Foam

- Polyethylene

- Mineral Wool

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by End-use Industry, 2026-2033

- Residential

- Commercial

- Industrial

- East Asia HVAC Insulation Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Pipes

- Ducts

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Material Type, 2026-2033

- Mineral Wool

- Glass Wool

- Stone Wool

- Plastic Foam

- Phenolic, PIR & PUR

- Elastomeric Foam

- Polyethylene

- Mineral Wool

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by End-use Industry, 2026-2033

- Residential

- Commercial

- Industrial

- South Asia & Oceania HVAC Insulation Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Pipes

- Ducts

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Material Type, 2026-2033

- Mineral Wool

- Glass Wool

- Stone Wool

- Plastic Foam

- Phenolic, PIR & PUR

- Elastomeric Foam

- Polyethylene

- Mineral Wool

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by End-use Industry, 2026-2033

- Residential

- Commercial

- Industrial

- Latin America HVAC Insulation Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Pipes

- Ducts

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Material Type, 2026-2033

- Mineral Wool

- Glass Wool

- Stone Wool

- Plastic Foam

- Phenolic, PIR & PUR

- Elastomeric Foam

- Polyethylene

- Mineral Wool

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by End-use Industry, 2026-2033

- Residential

- Commercial

- Industrial

- Middle East & Africa HVAC Insulation Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- Pipes

- Ducts

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Material Type, 2026-2033

- Mineral Wool

- Glass Wool

- Stone Wool

- Plastic Foam

- Phenolic, PIR & PUR

- Elastomeric Foam

- Polyethylene

- Mineral Wool

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by End-use Industry, 2026-2033

- Residential

- Commercial

- Industrial

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Owens Corning

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Rockwool International A/S

- Armacell International SA

- Knauf Insulation

- Saint Gobain SA

- Glassrock Insulation Co

- Kingspan Group

- CSR Buildings Products Ltd.

- Thermaflex

- Johns Manville Corporation

- Panasonic Industry Co., Ltd.

- American Flexible Products

- Climatech International

- Owens Corning

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Advanced Materials

- HVAC Insulation Market

HVAC Insulation Market Size, Share, and Growth Forecast 2026 - 2033

HVAC Insulation Market by Product Type (Pipes, Ducts), Material Type (Mineral Wool, Plastic Foam), Industry (Residential, Commercial, Industrial), and Regional Analysis for 2026 - 2033

HVAC Insulation Market Size and Trend Analysis

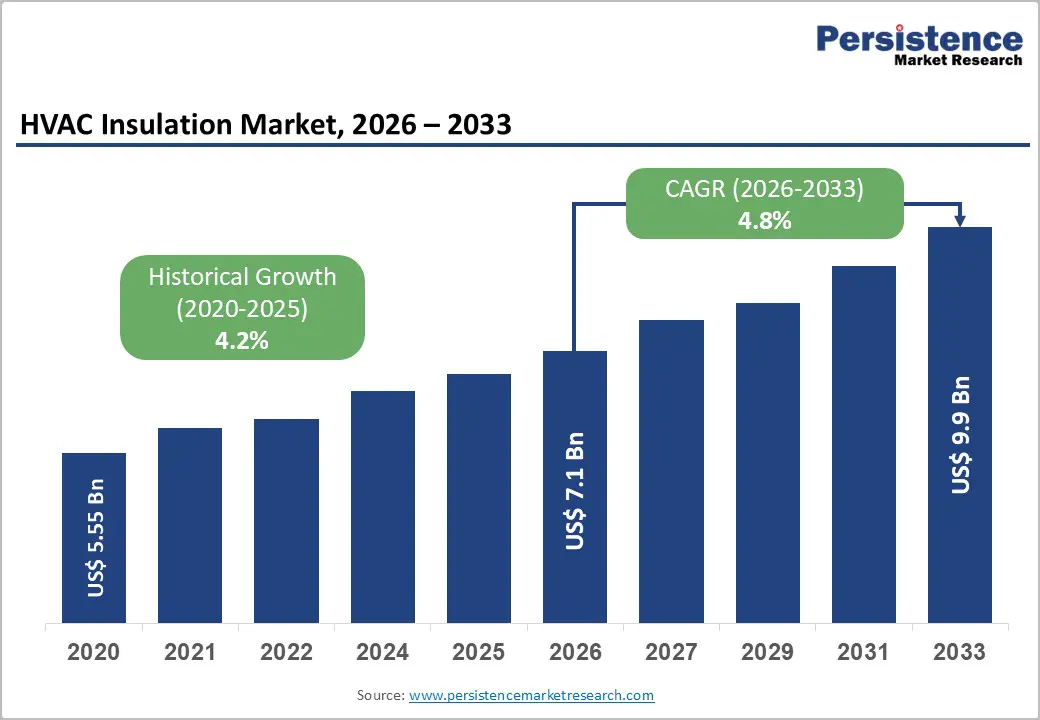

The global HVAC Insulation market size is valued at US$ 7.1 Bn in 2026 and is projected to reach US$ 9.9 Bn by 2033, growing at a CAGR of 4.8% between 2026 and 2033.

Rising global emphasis on building energy efficiency, stringent regulatory mandates such as the European Union's Energy Performance of Buildings Directive (EPBD) and the U.S. Department of Energy (DOE) Building Energy Codes, and rapid urbanization across the Asia Pacific and the Middle East are the primary drivers of market expansion. The escalating demand for thermally efficient HVAC systems in both new construction and retrofit applications continues to underpin sustained investment across the insulation value chain, supporting robust volume uptake of pipe and duct insulation products.

Key Industry Highlights:

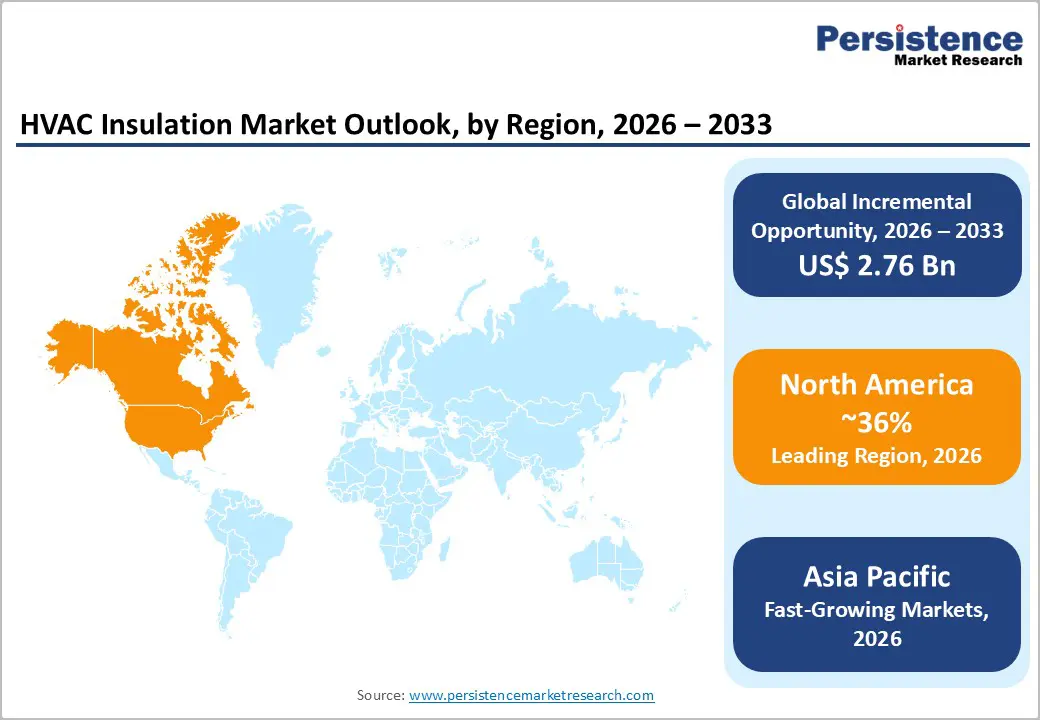

- Leading Region: North America leads the HVAC insulation market, with 36% market share, driven by mandatory compliance with ASHRAE 90.1, DOE Building Energy Codes, and strong commercial construction activity across the U.S. and Canada, supported further by IRA 2022 retrofit incentives.

- Fastest Growing Region: Asia Pacific is expanding at the fastest pace, propelled by China's 14th Five-Year Plan, India's ECBC 2017, and surging construction across ASEAN nations, with rising urbanization and manufacturing FDI creating robust, sustained demand for HVAC insulation products.

- Dominant Segment: The Ducts segment dominates the product type category with approximately 60% share, underpinned by ASHRAE 90.1 duct sealing mandates, extensive commercial building HVAC networks, and DOE research confirming 25-40% energy losses from poorly insulated ductwork.

- Fastest Growing Segment: Plastic Foam insulation, particularly PIR & PUR, is the fastest-growing material type segment, driven by superior thermal conductivity values, moisture resistance, lightweight handling advantages, and growing adoption in industrial cold-chain and data center cooling applications globally.

- Key Market Opportunity: The convergence of the EU Renovation Wave targeting 35 million building retrofits and expanding global district heating networks, with China covering over 5.5 billion sq. m., offers insulation manufacturers a multi-decade, policy-backed demand expansion opportunity through the forecast period.

| Key Insights | Details |

|---|---|

|

HVAC Insulation Market Size (2026E) |

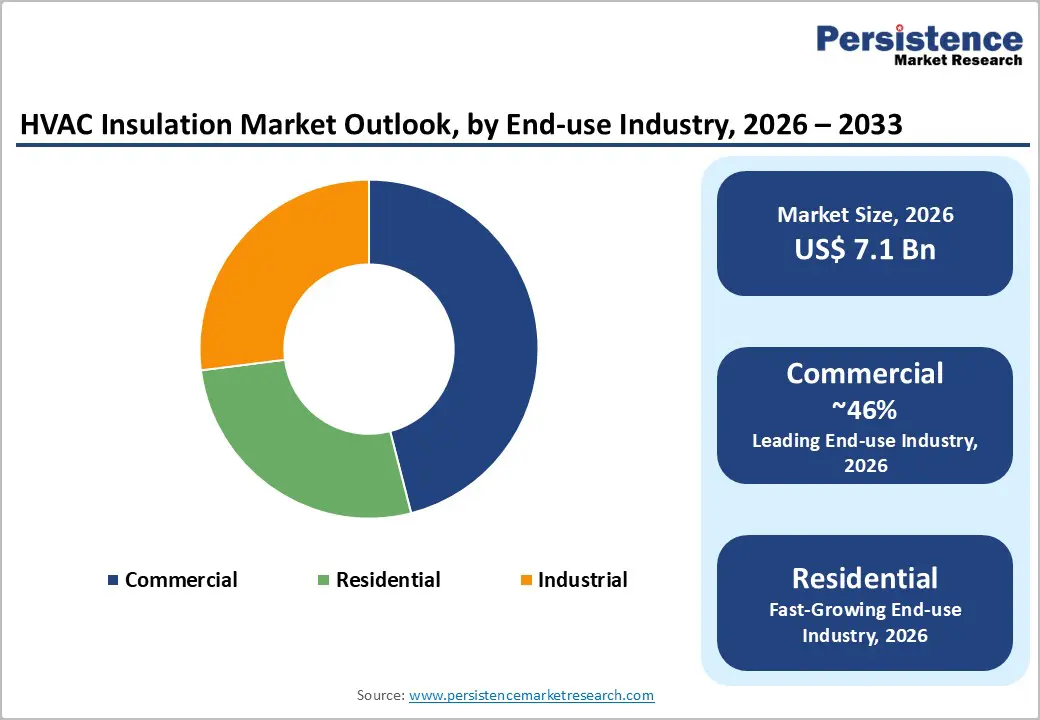

US$ 7.1 Bn |

|

Market Value Forecast (2033F) |

US$ 9.9 Bn |

|

Projected Growth CAGR (2026–2033) |

4.8% |

|

Historical Market Growth (2020–2025) |

4.2% CAGR |

Market Dynamics

Drivers - Stringent Building Energy Efficiency Regulations Spurring Insulation Demand

The global shift toward net-zero energy buildings has elevated HVAC insulation to a critical component of modern energy-efficient construction. Regulatory authorities across major regions are continually strengthening thermal performance requirements for both new developments and existing structures. According to the U.S. Department of Energy, commercial buildings account for roughly 36% of national electricity consumption, with HVAC systems responsible for nearly 40% of that usage.

Similarly, the European Union’s revised Energy Performance of Buildings Directive (2023) mandates that all new buildings meet zero-emission criteria by 2028, with full compliance for existing buildings by 2050. These increasingly rigorous standards are driving architects, engineers, and contractors to adopt high-performance duct and pipe insulation solutions, thereby generating sustained demand across all end-use sectors.

Accelerating Urbanization and Large-Scale Infrastructure Development

Rapid urban expansion across Asia Pacific, the Middle East, and Latin America is generating substantial construction activity that necessitates modern, code-compliant HVAC systems equipped with high-performance insulation. Projections from the United Nations Department of Economic and Social Affairs indicate that the global urban population will increase by approximately 2.5 billion by 2050, with most growth occurring in Asia and Africa.

China’s 14th Five-Year Plan (2021-2025) reinforces this trajectory by mandating energy-efficient construction across more than 2 billion square meters of certified green building space. Likewise, India’s Smart Cities Mission and Housing for All initiative are intensifying demand for thermally efficient residential and commercial building systems, including insulated ductwork and piping, thereby significantly expanding the addressable market.

Restraints - Volatile Raw Material Prices Creating Cost Pressure Across the Supply Chain

HVAC insulation manufacturers continue to experience significant cost pressures due to the pronounced volatility of key raw materials, particularly petrochemical-derived inputs such as polyurethane (PUR), polyisocyanurate (PIR), and glass fiber. Crude oil price fluctuations, compounded by geopolitical uncertainty and supply chain disruptions observed between 2021 and 2023, substantially increased production costs for foam-based insulation products.

The U.S. Bureau of Labor Statistics reported that the Producer Price Index for plastic foam products rose by more than 18% in 2022 compared with pre-pandemic levels. This instability compresses margins, complicates long-term project pricing, and may prompt the substitution of premium insulation materials with lower-performance alternatives.

Environmental and Regulatory Compliance Costs

Certain HVAC insulation materials, especially closed-cell foams that rely on hydrofluorocarbon (HFC) blowing agents, are increasingly constrained by evolving regulatory frameworks. The EU F-Gas Regulation (EU) 2024/573, effective from March 2024, significantly accelerates HFC phase-down requirements, compelling manufacturers to transition toward low-GWP formulations. Achieving compliance demands substantial research and development investment, as well as additional capital expenditure, posing notable challenges for smaller producers.

Simultaneously, the European Chemicals Agency (ECHA) continues its oversight of certain synthetic mineral fibers under the REACH regulation, necessitating enhanced occupational safety measures and stricter labeling standards. These combined obligations further heighten industry-wide compliance costs.

Opportunities - Massive Retrofit Opportunity in Aging Building Stock Across North America and Europe

The extensive stock of aging residential and commercial buildings across developed economies presents a significant long-term opportunity for HVAC insulation suppliers. The U.S. Department of Energy estimates that nearly 80% of the buildings expected to be in use by 2050 already exist, many of which possess inadequate insulation performance. Europe faces a comparable challenge, with the European Commission’s Renovation Wave Strategy aiming to double annual energy renovation rates to at least 3% across 35 million structures by 2030.

Elevated energy prices following the 2022 crisis have further accelerated investment in thermal envelope improvements, including duct and pipe insulation. This sustained retrofit momentum is expected to support a stable, long-duration demand cycle for insulation manufacturers, installers, and distributors.

Expansion of District Heating and Cooling Networks Driving Pipe Insulation Demand

The rapid expansion of district heating and cooling (DHC) infrastructure is creating a significant growth opportunity for pipe insulation manufacturers within the HVAC sector. The International Energy Agency recognizes district heating as a critical decarbonization mechanism, with existing networks supplying nearly 10% of global space-heating demand. China remains the largest contributor, operating systems that service more than 5.5 billion square meters of heated floor area.

Nordic countries, Germany, and Poland are similarly advancing large-scale transitions toward renewable and waste-heat-based district systems, necessitating full re-insulation of aging distribution pipelines. Concurrently, the increasing development of data centers and industrial facilities, each requiring extensive chilled-water loops, continues to drive substantial demand for high-performance pipe insulation, further expanding market potential for specialized suppliers.

Category-wise Analysis

Product Type Insights

The Ducts segment maintains a leading position within the HVAC insulation market, accounting for approximately 60% of total revenue. Duct insulation plays a critical role in minimizing thermal losses across air distribution networks, with research from the U.S. Lawrence Berkeley National Laboratory indicating that insufficiently insulated ductwork can contribute to 25-40% of overall HVAC energy loss in residential settings.

The widespread adoption of centralized air-and ventilation systems in commercial environments, such as offices, healthcare facilities, and data centers, continues to drive substantial demand for duct-wrap and duct-board insulation solutions. Furthermore, stringent leakage and efficiency requirements under ASHRAE Standard 90.1 and comparable international codes further advance duct insulation specifications, reinforcing this segment’s dominant market position across North America and Europe.

Material Type Insights

The Mineral Wool category, comprising both glass wool and stone wool, represents the leading material segment in the HVAC insulation market, accounting for approximately 42% of total market share. Glass wool maintains a dominant position due to its strong thermal efficiency, non-combustible nature, acoustic absorption capabilities, and cost-effectiveness compared with alternative materials.

Fire-safety regulations across major global construction markets, including the EU Construction Products Regulation (CPR), the U.S. NFPA 90A Standard, and ASHRAE 90.1, require the use of non-combustible or fire-resistant materials in commercial HVAC systems. These mandates significantly reinforce mineral wool's competitive advantages over plastic foam, particularly in high-occupancy buildings. Leading manufacturers such as Owens Corning and Knauf Insulation continue to play a prominent role in advancing this material segment.

Industry Insights

The Commercial segment constitutes the leading end-use category in the HVAC insulation market, accounting for an estimated 46% share globally. Commercial facilities, including offices, retail centers, healthcare institutions, educational campuses, and hospitality properties, utilize extensive and complex HVAC systems that require significant volumes of insulated ductwork and piping.

According to the U.S. Energy Information Administration’s 2018 Commercial Buildings Energy Consumption Survey, space heating and cooling represent more than 40% of energy use in commercial buildings, underscoring the importance of effective insulation for reducing operational costs. The continued expansion of healthcare infrastructure and data centers, both highly HVAC-intensive environments, further strengthens the dominance of the commercial segment, driving consistent demand for advanced insulation solutions across major regions.

Regional Insights

North America HVAC Insulation Market Trends

North America remains the most established and revenue-dominant region in the global HVAC insulation market, led primarily by the United States. The U.S. DOE Building Energy Codes Program defines minimum insulation requirements, while ASHRAE Standard 90.1-2022 introduces progressively higher R-value specifications for commercial duct and pipe insulation. The Inflation Reduction Act (2022) further strengthens market demand by allocating substantial funding toward clean-energy and building-efficiency initiatives, including tax incentives that directly encourage insulation upgrades.

Canada is also emerging as an important regional contributor, with the National Building Code of Canada 2020 aligning energy-efficiency provisions with national net-zero objectives. Residential HVAC insulation activity is particularly strong across the U.S. Sun Belt and Canadian Prairie regions, while innovations such as aerogel-based and vacuum-insulation panels gain traction among premium commercial developers.

Europe HVAC Insulation Market Trends

Europe represents the second-largest regional market for HVAC insulation, supported by some of the world’s most stringent building energy regulations. Germany leads the region, driven by the Gebäudeenergiegesetz (GEG) of 2020, which consolidates energy performance requirements across all building categories. The European Green Deal, together with the Fit for 55 package, mandates a 55% reduction in greenhouse gas emissions by 2030 compared with 1990 levels, and investing in high-performance HVAC insulation is a regulatory necessity for member states.

The United Kingdom’s Part L updates (2021–2022) have further tightened efficiency standards for new dwellings, while France’s RE2020 regulation promotes low-carbon insulation materials, including stone wool and bio-based alternatives. Spain and Poland continue to benefit from EU Cohesion Funds targeted at large-scale renovation, bolstering regional insulation demand.

Asia Pacific HVAC Insulation Market Trends

Asia Pacific remains the fastes-growing market for HVAC insulation, driven by rapid urbanization, rising household incomes, and a significant expansion of commercial real estate across major economies. China continues to dominate regional demand, supported by the 14th Five-Year Plan’s green-building requirements and the GB 50736-2012 design code, which outlines mandatory insulation standards for HVAC ductwork and piping.

The Ministry of Housing and Urban-Rural Development’s ongoing expansion of Green Building Star certification further reinforces institutional demand for high-quality insulation solutions. India represents another key growth frontier, underpinned by the Energy Conservation Building Code (ECBC) 2017, which mandates insulation performance in commercial HVAC systems. Rapid construction growth in Indonesia, Vietnam, and Thailand, along with Japan’s stringent energy-efficiency requirements, continues to strengthen demand across industrial and high-density urban applications.

Competitive Landscape

The global HVAC insulation market is characterized by a moderately consolidated competitive landscape, with leading companies, Owens Corning, Rockwool International A/S, Armacell International SA, Knauf Insulation, and Saint-Gobain SA, collectively accounting for an estimated 45-50% of total revenue. These firms differentiate themselves through extensive product portfolios spanning mineral wool and foam insulation, broad manufacturing capabilities, and strong partnerships with tier-one mechanical contractors and major building material distributors. Strategic priorities across the industry include targeted acquisitions to strengthen regional presence, accelerated investment in sustainable and low-GWP insulation technologies, and the integration of advanced digital modelling tools. Meanwhile, emerging Asian manufacturers continue to gain momentum through competitive pricing, intensifying market rivalry.

Key Developments:

- August 2025: Saint-Gobain announced the commencement of construction of its 7th float glass line and 5th mineral wool insulation line in Oragadam, Chennai. This expansion marks a significant milestone, reinforcing the Group’s strategic commitment to strengthening local manufacturing capabilities and growing in the Indian market.

- August 2025: Knauf Insulation, Inc. announced a significant investment in its Shelbyville, IN operations. The investment includes comprehensive upgrades to existing pipe production, the addition of a new state-of-the-art pipe production line, and expanded glass capacity to support both pipe and blowing wool production. This strategic investment underscores Knauf’s commitment to delivering high-quality products, meeting evolving customer needs, and driving continuous growth into the future.

- May 2025: Knauf Insulation, Inc., a leading North American manufacturer of fiberglass insulation, announced the addition of a new, dedicated blowing wool line at its Shelbyville, IN fiberglass insulation manufacturing facility. The new line is expected to be commissioned in Q2 of 2026.

Top Companies in HVAC Insulation

Owens Corning (Toledo, U.S.) is a global leader in insulation, roofing, and composites. Its HVAC insulation portfolio, anchored by FOAMGLAS® and Fiberglas™ brands, spans duct boards, pipe insulation, and duct wrap solutions. The company's extensive North American distribution network and dominant position in glass fiber insulation manufacturing make it the market's foremost player.

Rockwool International A/S (Hedehusene, Denmark) is the world's leading manufacturer of stone wool insulation products. Its HVAC-specific product lines, including ROCKWOOL® Technical Insulation for pipe and duct applications, are specified globally in commercial and industrial projects. The company's fire-safe, acoustically superior stone wool products command a premium in European and North American regulated markets.

Armacell International SA (Luxembourg) is the global leader in flexible foam insulation, primarily serving mechanical insulation and HVAC markets with its flagship ArmaFlex® elastomeric foam range. With operations across 23 manufacturing plants in over 16 countries, Armacell holds a commanding position in closed-cell elastomeric insulation for refrigerant piping, chilled water lines, and air conditioning ductwork, particularly in the Asia Pacific and European markets.

Companies Covered in HVAC Insulation Market

- Owens Corning

- Rockwool International A/S

- Armacell International SA

- Knauf Insulation

- Saint-Gobain SA

- Glassrock Insulation Co

- Kingspan Group

- CSR Building Products Ltd.

- Thermaflex

- Johns Manville Corporation

- Panasonic Industry Co., Ltd.

- American Flexible Products

- Climatech International

Frequently Asked Questions

The global HVAC Insulation market is valued at US$ 7.1 Bn in 2026 and is projected to reach US$ 9.9 Bn by 2033, advancing at a robust CAGR of 4.8% over the 2026–2033 forecast period, underpinned by tightening building energy codes and accelerating urbanization.

The market is primarily driven by stringent energy efficiency mandates, such as the EU EPBD and U.S. DOE Building Energy Codes, that mandate high-performance insulation in new and renovated buildings, alongside rapid urbanization and infrastructure growth across Asia Pacific and the Middle East, which is amplifying large-scale HVAC system deployment.

The Ducts segment is the dominant product type, holding approximately 60% of market share. This leadership reflects the extensive ductwork in commercial buildings, compliance with ASHRAE 90.1 duct insulation standards, and the significant energy savings achievable through proper duct insulation, which can reduce HVAC energy losses by 25–40% per U.S. Lawrence Berkeley National Laboratory research.

North America is the leading region, with the United States as the primary revenue contributor. Strong market fundamentals include mandatory compliance with ASHRAE 90.1, active DOE Building Energy Codes, robust commercial construction activity, and significant retrofit stimulus from the Inflation Reduction Act (IRA) 2022, collectively driving sustained insulation demand across residential, commercial, and industrial end-uses.

The most significant opportunities lie in the retrofit of aging building stock, with the EU Renovation Wave targeting 35 million building renovations and 80% of U.S. 2050 buildings already existing. The global expansion of district heating and cooling networks, particularly in China, Scandinavia, and Central Europe, is creating large-volume demand for high-performance pipe insulation products.

Leading companies in the global HVAC Insulation market include Owens Corning, Rockwool International A/S, Armacell International SA, Knauf Insulation, Saint-Gobain SA, Kingspan Group, Johns Manville Corporation, and Thermaflex, among others. These players compete based on product performance, thermal conductivity, fire safety ratings, geographic footprint, and sustainability credentials.