- Biotechnology

- Hemato Oncology Testing Market

Hemato Oncology Testing Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Hemato Oncology Testing Market by Product (Assay Kits, Reagents, Instruments / Platforms, Software & Services), Technology (Next-Generation Sequencing (NGS), Polymerase Chain Reaction (PCR), Flow Cytometry, Immunohistochemistry (IHC), Others), Cancer Type (Leukemia, Lymphoma, Multiple Myeloma, Myelodysplastic Syndromes (MDS), Others), End-user, and Regional Analysis from 2026 - 2033

Hemato Oncology Testing Market Share and Trends Analysis

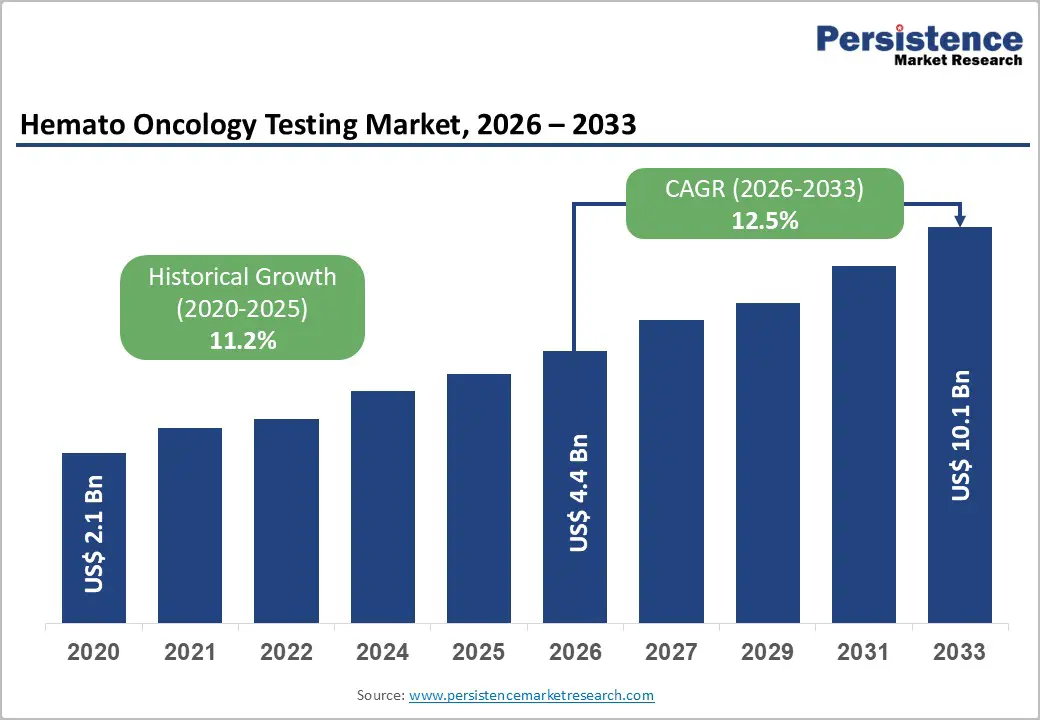

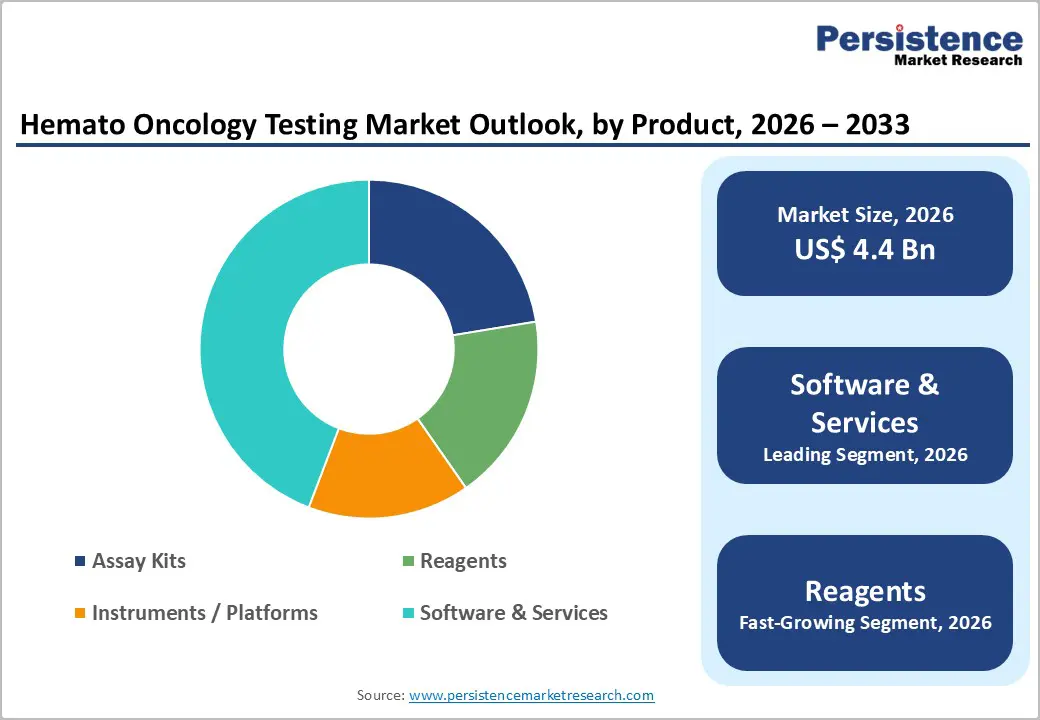

The global hemato oncology testing market is estimated to grow from US$ 4.4 Bn in 2026 to US$ 10.1 Bn by 2033. The market is projected to record a CAGR of 12.5% during the forecast period from 2026 to 2033.

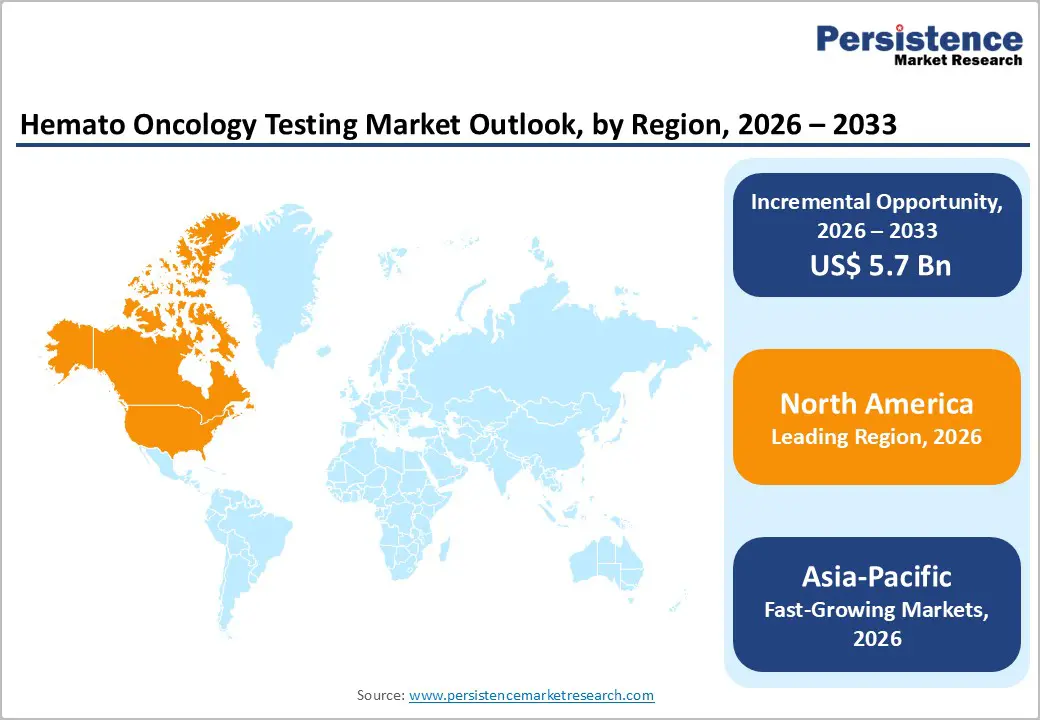

The global market is expanding steadily, driven by rising incidence of blood cancers, growing demand for precision diagnostics, and increasing adoption of molecular testing technologies. North America leads due to advanced diagnostic infrastructure and strong adoption of genomic testing, while Asia-Pacific is the fastest-growing region, supported by improving healthcare systems and increasing cancer screening awareness.

Key Industry Highlights:

- Dominant Technology: Polymerase Chain Reaction (PCR) held 34.0% share in 2025, driven by its high sensitivity, rapid turnaround time, and widespread use in detecting genetic mutations and chromosomal abnormalities associated with leukemia, lymphoma, and other hematologic malignancies.

- Dominant Region: North America is the leading region in the hemato-oncology testing market with 40.6% share in 2025, supported by advanced molecular diagnostic infrastructure, strong adoption of genomic testing, high cancer screening rates, and the presence of major diagnostic companies.

- Growth Indicators: Growth is driven by rising incidence of blood cancers, increasing adoption of precision medicine, expanding use of molecular and genomic diagnostics, and growing demand for early detection and monitoring of hematologic malignancies.

- Market Opportunity: Opportunities include expansion of next-generation sequencing-based diagnostics, development of advanced biomarker tests, increasing adoption of liquid biopsy technologies, and growing investments in oncology diagnostics across emerging healthcare markets.

| Key Insights | Details |

|---|---|

|

Global Hemato Oncology Testing Market Size (2026E) |

US$ 4.4 Bn |

|

Market Value Forecast (2033F) |

US$ 10.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

12.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

11.2% |

Market Dynamics

Driver: Increasing Adoption of Molecular and Genomic Diagnostic Technologies

The increasing adoption of molecular and genomic diagnostic technologies is a major driver of the Hemato-Oncology Testing Market, as blood cancers require highly precise genetic characterization for diagnosis and treatment planning. Hematologic malignancies such as leukemia, lymphoma, and multiple myeloma are strongly associated with genetic mutations and chromosomal abnormalities that cannot be detected through conventional microscopy alone. According to global cancer data, approximately 1.31 million new cases of hematologic malignancies and over 700,000 related deaths occurred worldwide in 2022, highlighting the growing burden of these diseases and the need for advanced diagnostic methods. Molecular techniques such as PCR, fluorescence in-situ hybridization (FISH), and next-generation sequencing (NGS) enable clinicians to identify mutations like BCR-ABL, FLT3, and JAK2, which guide targeted therapy decisions and improve patient outcomes.

The shift toward precision medicine has further accelerated the integration of genomic testing in oncology laboratories and hospitals. Molecular profiling allows clinicians to classify hematologic cancers more accurately, monitor minimal residual disease, and predict treatment response. Next-generation sequencing has become particularly important because it can analyze hundreds of cancer-related genes simultaneously, enabling comprehensive genomic profiling. Studies indicate that nearly 68% of cancer centers in developed healthcare systems have incorporated NGS into their diagnostic workflows, reflecting the rapid clinical adoption of genomic technologies. The growing use of such advanced diagnostic tools supports earlier detection, personalized treatment strategies, and better disease monitoring, significantly driving demand for hemato-oncology testing services and technologies worldwide.

Restraint: Limited Access to Specialized Diagnostic Infrastructure in Developing Regions

Despite technological advancements, limited access to specialized diagnostic infrastructure in developing regions remains a major restraint for the Hemato-Oncology Testing Market. Accurate diagnosis of hematologic cancers requires sophisticated laboratory facilities, including molecular testing platforms, pathology laboratories, and trained hematopathologists. However, these resources are unevenly distributed globally. According to the World Health Organization (WHO), less than 30% of low-income countries have generally accessible cancer diagnosis and treatment services, and referral systems for suspected cancer cases are often inadequate. In many regions, patients experience delayed diagnosis because hospitals lack pathology laboratories or advanced diagnostic technologies needed for accurate cancer classification.

Infrastructure limitations also extend to laboratory capacity, workforce shortages, and diagnostic equipment availability. Studies on global pathology services indicate that only about one-quarter of low-income countries have readily available pathology services, which are essential for confirming cancer diagnoses and guiding treatment. Limited availability of diagnostic tools results in delayed disease detection, misdiagnosis, and reduced survival rates for patients with hematologic malignancies. Additionally, health facility surveys in several low- and middle-income countries reported that basic diagnostic tests were available in only about 19% of primary healthcare facilities, demonstrating the significant infrastructure gap in cancer diagnostics. These barriers restrict widespread adoption of advanced hemato-oncology testing technologies and slow market expansion in emerging healthcare systems.

Opportunity: Growing Adoption of Next-Generation Sequencing in Oncology Diagnostics

The growing adoption of next-generation sequencing (NGS) in oncology diagnostics represents a significant opportunity for the Hemato-Oncology Testing Market. NGS technology allows simultaneous sequencing of multiple genes and detection of complex genomic alterations associated with hematologic malignancies. This capability is particularly important for cancers such as acute myeloid leukemia (AML), chronic lymphocytic leukemia (CLL), and multiple myeloma, where multiple genetic mutations influence disease progression and therapy response. With increasing emphasis on personalized medicine, healthcare providers are increasingly relying on genomic sequencing to identify biomarkers and guide targeted treatment strategies. As a result, NGS is becoming a central component of modern oncology diagnostics and clinical decision-making.

Clinical adoption of sequencing technologies has expanded significantly in recent years. Reports indicate that approximately 68% of cancer centers have incorporated next-generation sequencing into their diagnostic workflows, demonstrating its growing role in routine oncology testing. NGS enables comprehensive genomic profiling that improves diagnostic accuracy, facilitates risk stratification, and supports the development of targeted therapies. Additionally, the technology is being increasingly used to monitor minimal residual disease and detect relapse in hematologic malignancies. As healthcare systems continue investing in precision oncology programs and genomic medicine initiatives, the demand for NGS-based hemato-oncology testing is expected to increase substantially, creating strong growth opportunities for diagnostic companies and clinical laboratories worldwide.

Category-wise Analysis

By Product Insights

Software and services dominate the hemato-oncology testing market with 44.2% share in 2025, because advanced cancer diagnostics increasingly rely on specialized laboratory services, data interpretation, and bioinformatics platforms. Hematologic malignancies involve complex genetic mutations that require genomic sequencing, molecular profiling, and continuous disease monitoring. These processes generate large datasets that must be analyzed using dedicated clinical software and expert laboratory services. According to the World Health Organization (WHO), cancer accounted for nearly 10 million deaths globally in 2022, highlighting the growing demand for advanced diagnostic testing and interpretation systems. In hematologic cancers such as leukemia and lymphoma, patients often undergo repeated molecular tests to monitor treatment response and relapse. This continuous need for diagnostic testing, data management, and clinical interpretation significantly increases reliance on specialized software platforms and laboratory testing services worldwide.

By Technology Insights

Polymerase Chain Reaction (PCR) dominates the hemato-oncology testing market because it is a highly sensitive and reliable method for detecting genetic mutations associated with blood cancers. PCR amplifies small quantities of DNA or RNA, enabling early detection of disease-related genetic abnormalities. In hematologic malignancies such as chronic myeloid leukemia (CML), PCR is widely used to identify the BCR-ABL1 fusion gene, a key diagnostic biomarker. According to global cancer statistics, around 487,000 new leukemia cases were reported worldwide in 2022, emphasizing the need for accurate molecular diagnostics. Quantitative PCR is also used to monitor minimal residual disease and evaluate treatment response in leukemia patients. Due to its rapid results, high sensitivity, and relatively lower cost compared with genomic sequencing technologies, PCR remains the most widely adopted diagnostic technology in hemato-oncology testing laboratories.

Regional Insights

North America Hemato Oncology Testing Market Trends

North America dominates the hemato-oncology testing market due to its advanced healthcare infrastructure, strong cancer screening programs, and widespread adoption of molecular diagnostics. High-income healthcare systems enable early detection and genomic testing for hematologic malignancies such as leukemia and lymphoma. According to global cancer statistics, the United States reported about 181,894 new hematologic malignancy cases in 2022, reflecting a significant diagnostic demand for advanced testing technologies. High-income regions such as North America also show some of the highest age-standardized incidence rates of leukemia and lymphoma globally, partly due to strong screening and reporting systems. Additionally, extensive research funding, strong presence of biotechnology companies, and widespread use of precision medicine technologies further strengthen the region’s leadership in hemato-oncology diagnostics.

Europe Hemato Oncology Testing Market Trends

Europe represents a major region in the hemato-oncology testing market due to its strong healthcare systems, high cancer detection rates, and extensive research in oncology diagnostics. Many European countries have well-established national cancer screening and registry programs that support early diagnosis and disease monitoring. Epidemiological data show that Western Europe recorded around 687,000 leukemia-related cases in recent global analyses, indicating a substantial disease burden requiring advanced diagnostic testing. Additionally, European countries invest heavily in cancer research initiatives and precision medicine programs, which promote the use of molecular diagnostics and genomic testing technologies. The presence of leading pharmaceutical and biotechnology companies, strong academic research networks, and collaborative oncology programs further strengthens Europe’s role in advancing hemato-oncology testing and improving cancer diagnosis across the region.

Asia Pacific Hemato Oncology Testing Market Trends

Asia Pacific is the fastest-growing region in the hemato-oncology testing market due to its large population base, rising cancer incidence, and expanding healthcare infrastructure. The region accounts for a substantial share of global hematologic malignancy cases because of population size and improving disease detection. Global studies indicate that Asia recorded the largest number of leukemia cases, exceeding 227,000 cases globally in recent estimates, highlighting the growing need for diagnostic testing services. Countries such as China and India are rapidly investing in healthcare infrastructure, oncology centers, and molecular diagnostic laboratories to improve cancer detection. Increasing government initiatives, expanding access to advanced diagnostic technologies, and rising awareness of early cancer screening are accelerating the adoption of hemato-oncology testing across Asia-Pacific healthcare systems.

Competitive Landscape

The hemato-oncology testing market is highly competitive, led by major diagnostic and biotechnology companies such as F. Hoffmann-La Roche Ltd., Abbott, Thermo Fisher Scientific, Illumina, and Bio-Rad Laboratories. These players focus on developing advanced molecular diagnostics, expanding genomic testing platforms, investing in precision oncology research, and strengthening global laboratory networks.

Key Industry Developments:

- In August 2025, Amoy Diagnostics announced that its AmoyDx® Pan Lung Cancer PCR Panel received regulatory approval in Japan as a companion diagnostic for LORBRENA® (lorlatinib), a targeted therapy used for treating patients with advanced ALK-positive non-small cell lung cancer (NSCLC).

- In May 2025, Thermo Fisher Scientific announced advancements in precision oncology during the American Society of Clinical Oncology Annual Meeting (ASCO 2025). The company highlighted new research findings, diagnostic technologies, and genomic testing solutions aimed at improving personalized cancer treatment

- In July 2024, Thermo Fisher Scientific announced that it would support advancements in clinical research and treatment of myeloid cancers by utilizing its next-generation sequencing (NGS) technology. The company aimed to enable comprehensive genomic profiling of myeloid malignancies such as acute myeloid leukemia (AML) and myelodysplastic syndromes.

Companies Covered in Hemato Oncology Testing Market

- Amoy Diagnostics Co., Ltd.

- Thermo Fisher Scientific, Inc.

- EntroGen, Inc.

- Bio-Rad Laboratories, Inc.

- Abbott

- F. Hoffmann-La Roche Ltd.

- ArcherDX, Inc. (IDT)

- Qiagen N.V.

- Illumina, Inc.

- Cepheid (Danaher Corporation)

- ASURAGEN, INC.

- Others

Frequently Asked Questions

The global hemato oncology testing market is projected to be valued at US$ 4.4 Bn in 2026.

Rising blood cancer incidence, expanding molecular diagnostics adoption, growing precision medicine demand, and advancements in genomic testing technologies.

The global hemato oncology testing market is poised to witness a CAGR of 12.5% between 2026 and 2033.

Expansion of next-generation sequencing, liquid biopsy diagnostics, emerging market healthcare investments, and precision oncology advancements.

Amoy Diagnostics Co., Ltd., Thermo Fisher Scientific, Inc., EntroGen, Inc., Bio-Rad Laboratories, Inc., Abbott, F. Hoffmann-La Roche Ltd.