- Executive Summary

- Global Green Cement Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Mn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Challenges

- Key Trends

- Product Lifecycle Analysis

- Green Cement Market: Value Chain

- List of Raw Material Suppliers

- List of Manufacturers

- List of Distributors

- Profitability Analysis

- Forecast Factors - Relevance and Impact

- Covid-19 Impact Assessment

- PESTLE Analysis

- Porter Five Force’s Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Application Landscape

- Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- Global Parent Market Overview

- Price Trend Analysis, 2020 - 2033

- Key Highlights

- Key Factors Impacting Product Prices

- Prices By Product Type/Composition/Application

- Regional Prices and Product Preferences

- Global Green Cement Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Market Size and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Mn) Analysis and Forecast

- Historical Market Size Analysis, 2020-2025

- Current Market Size Forecast, 2026-2033

- Global Green Cement Market Outlook: Product Type

- Introduction / Key Findings

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis By Product Type, 2020 - 2025

- Current Market Size (US$ Mn) and Volume (Tons) Forecast By Product Type, 2026 - 2033

- Fly Ash Based Cement

- Slag Based Cement

- Limestone Based Cement

- Geopolymer Cement

- Silica Fume Based Cement

- Recycled Aggregate Based Cement

- Misc.

- Market Attractiveness Analysis: Product Type

- Global Green Cement Market Outlook: Application

- Introduction / Key Findings

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis By Application, 2020 - 2025

- Current Market Size (US$ Mn) and Volume (Tons) Forecast By Application, 2026 - 2033

- Residential Construction

- Commercial Construction

- Infrastructure

- Market Attractiveness Analysis: Application

- Key Highlights

- Global Green Cement Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis By Region, 2020 - 2025

- Current Market Size (US$ Mn) and Volume (Tons) Forecast By Region, 2026 - 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Green Cement Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis By Market, 2020 - 2025

- By Country

- By Product Type

- By Application

- Current Market Size (US$ Mn) and Volume ( Tons) Forecast By Country, 2026 - 2033

- U.S.

- Canada

- Current Market Size (US$ Mn) and Volume (Tons) Forecast By Product Type, 2026 - 2033

- Fly Ash Based Cement

- Slag Based Cement

- Limestone Based Cement

- Geopolymer Cement

- Silica Fume Based Cement

- Recycled Aggregate Based Cement

- Misc.

- Current Market Size (US$ Mn) and Volume ( Tons) Forecast By Application, 2026 - 2033

- Residential Construction

- Commercial Construction

- Infrastructure

- Market Attractiveness Analysis

- Europe Green Cement Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis By Market, 2020 - 2025

- By Country

- By Product Type

- By Application

- Current Market Size (US$ Mn) and Volume (Tons) Forecast By Country, 2026 - 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Rest of Europe

- Current Market Size (US$ Mn) and Volume (Tons) Forecast By Product Type, 2026 - 2033

- Fly Ash Based Cement

- Slag Based Cement

- Limestone Based Cement

- Geopolymer Cement

- Silica Fume Based Cement

- Recycled Aggregate Based Cement

- Misc.

- Current Market Size (US$ Mn) and Volume ( Tons) Forecast By Application, 2026 - 2033

- Residential Construction

- Commercial Construction

- Infrastructure

- Market Attractiveness Analysis

- East Asia Green Cement Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis By Market, 2020 - 2025

- By Country

- By Product Type

- By Application

- Current Market Size (US$ Mn) and Volume ( Tons) Forecast By Country, 2026 - 2033

- China

- Japan

- South Korea

- Current Market Size (US$ Mn) and Volume (Tons) Forecast By Product Type, 2026 - 2033

- Fly Ash Based Cement

- Slag Based Cement

- Limestone Based Cement

- Geopolymer Cement

- Silica Fume Based Cement

- Recycled Aggregate Based Cement

- Misc.

- Current Market Size (US$ Mn) and Volume ( Tons) Forecast By Application, 2026 - 2033

- Residential Construction

- Commercial Construction

- Infrastructure

- Market Attractiveness Analysis

- South Asia & Oceania Green Cement Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis By Market, 2020 - 2025

- By Country

- By Product Type

- By Application

- Current Market Size (US$ Mn) and Volume (Tons) Forecast By Country, 2026 - 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Current Market Size (US$ Mn) and Volume (Tons) Forecast By Product Type, 2026 - 2033

- Fly Ash Based Cement

- Slag Based Cement

- Limestone Based Cement

- Geopolymer Cement

- Silica Fume Based Cement

- Recycled Aggregate Based Cement

- Misc.

- Current Market Size (US$ Mn) and Volume ( Tons) Forecast By Application, 2026 - 2033

- Residential Construction

- Commercial Construction

- Infrastructure

- Market Attractiveness Analysis

- Latin America Green Cement Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis By Market, 2020 - 2025

- By Country

- By Product Type

- By Application

- Current Market Size (US$ Mn) and Volume (Tons) Forecast By Country, 2026 - 2033

- Brazil

- Mexico

- Rest of Latin America

- Current Market Size (US$ Mn) and Volume (Tons) Forecast By Product Type, 2026 - 2033

- Fly Ash Based Cement

- Slag Based Cement

- Limestone Based Cement

- Geopolymer Cement

- Silica Fume Based Cement

- Recycled Aggregate Based Cement

- Misc.

- Current Market Size (US$ Mn) and Volume ( Tons) Forecast By Application, 2026 - 2033

- Residential Construction

- Commercial Construction

- Infrastructure

- Market Attractiveness Analysis

- Middle East & Africa Green Cement Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis By Market, 2020 - 2025

- By Country

- By Product Type

- By Application

- Current Market Size (US$ Mn) and Volume (Tons) Forecast By Country, 2026 - 2033

- GCC

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Current Market Size (US$ Mn) and Volume (Tons) Forecast By Product Type, 2026 - 2033

- Fly Ash Based Cement

- Slag Based Cement

- Limestone Based Cement

- Geopolymer Cement

- Silica Fume Based Cement

- Recycled Aggregate Based Cement

- Misc.

- Current Market Size (US$ Mn) and Volume ( Tons) Forecast By Application, 2026 - 2033

- Residential Construction

- Commercial Construction

- Infrastructure

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2026

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Apparent Production Capacity

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- LafargeHolcim

- Overview

- Segments and Products

- Key Financials

- Market Developments

- Market Strategy

- Taiwan Cement Corporation

- ACC Ltd.

- CEMEX S.A.B. de C.V.

- China National Building Materials

- Green Cement Inc

- Anhui Conch Cement

- heildelberg Cement

- CRH PIC

- Ultratech Cement Ltd

- LafargeHolcim

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Specialty & Fine Chemicals

- Green Cement Market

Green Cement Market Size, Share, and Growth Forecast, 2026 - 2033

Green Cement Market by Product Type (Fly Ash Based Cement, Slag Based Cement, Limestone Based Cement, Geopolymer Cement, Silica Fume Based Cement, Recycled Aggregate Based Cement, and Misc.), Application (Residential, Commercial, and Infrastructure), and Regional Analysis for 2026 - 2033

Green Cement Market Size and Trends Analysis

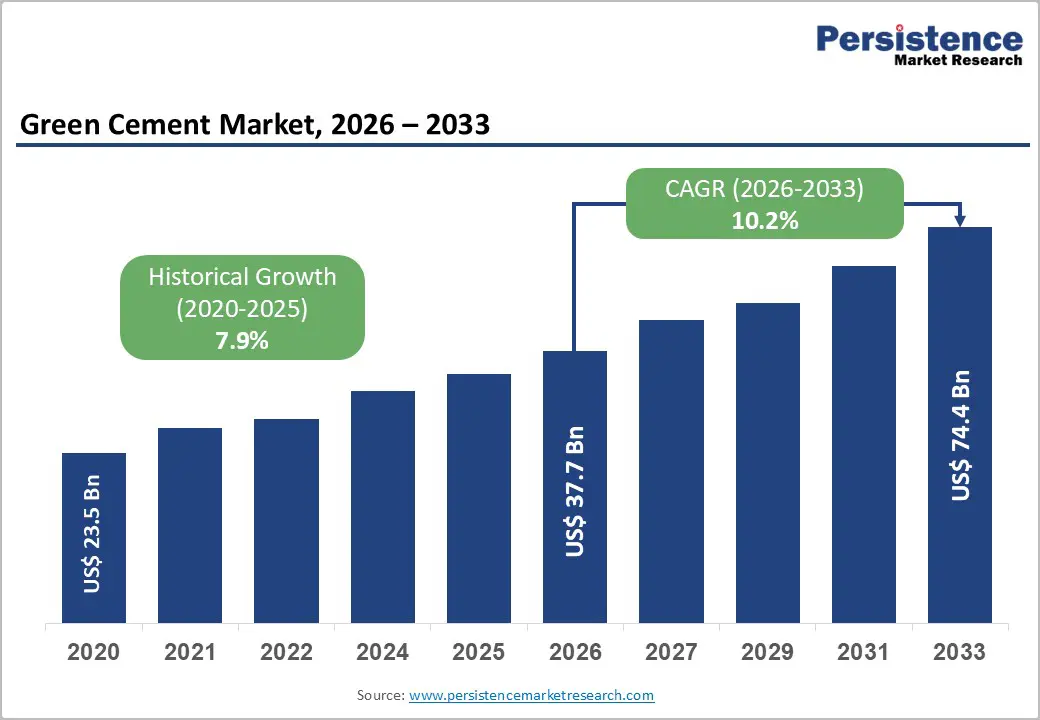

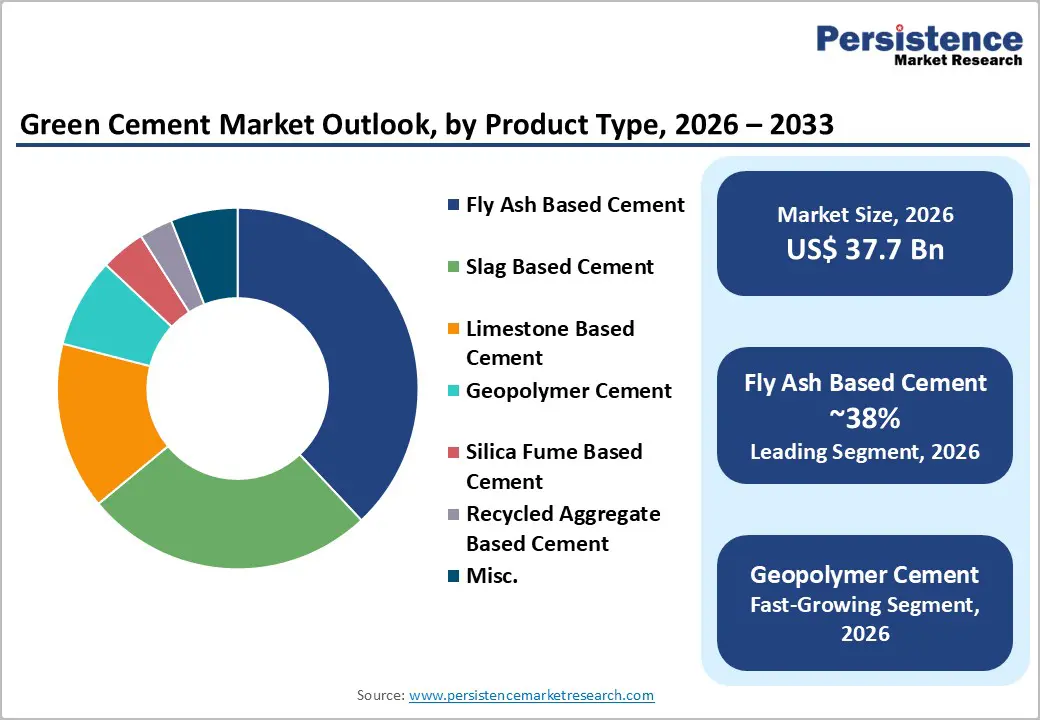

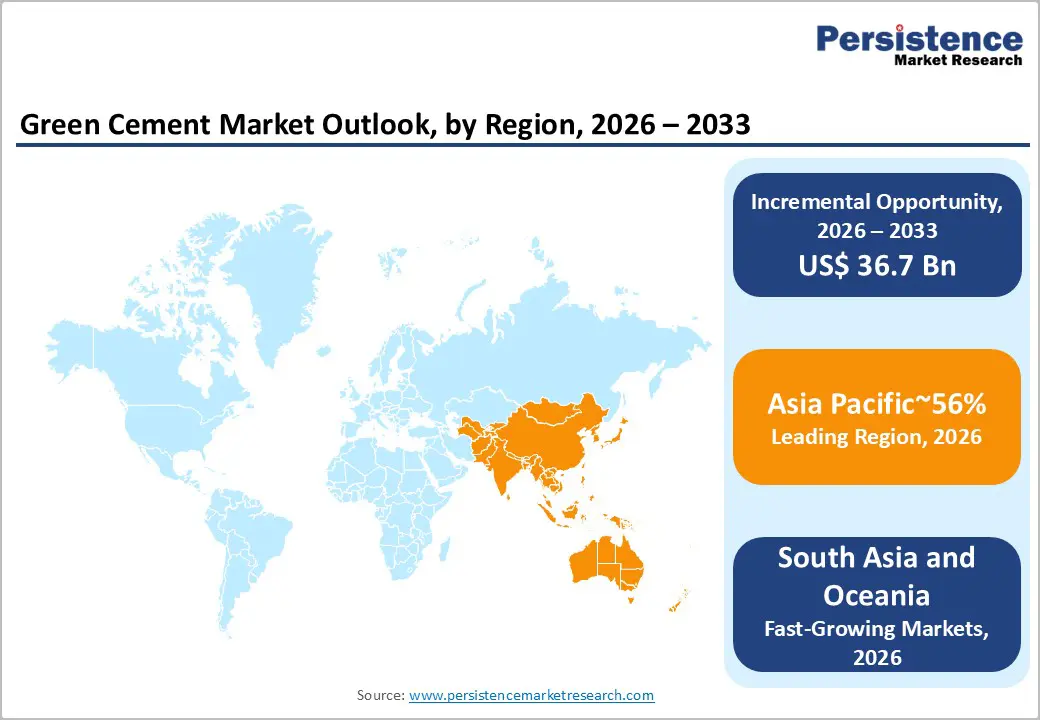

The global green cement market size is likely to be valued at US$ 37.7 billion in 2026 and is projected to reach US$ 74.4 billion by 2033, growing at a CAGR of 10.2% between 2026 and 2033.

This trajectory reflects structural demand driven by decarbonization mandates, urbanisation, and the availability of industrial byproducts. Cement production accounts for roughly 8% of global greenhouse gas emissions, and regulatory frameworks such as the EU Carbon Border Adjustment Mechanism (CBAM) entered full force in January 2026, attaching carbon costs directly to cement imports and incentivising low-clinker alternatives. Supplementary cementitious materials (SCMs) displace clinkers, avoiding approximately 0.83 tonnes of CO2 per tonne substituted, while 21 million new homes are needed each year globally to sustain urban growth, ensuring sustained construction demand.

Key Industry Highlights:

- Asia Pacific Dominance: Asia Pacific leads the Green Cement Market with approximately 56% share, supported by China and India’s large-scale cement production, carbon neutrality targets, infrastructure expansion, and strong government-backed decarbonisation roadmaps.

- Residential Leading Application: Residential construction accounts for nearly 42% of total market share, driven by rising housing demand, India’s PMAY-U program, and sustained U.S. homebuilding activity integrating low-carbon materials.

- Fly Ash-Based Cement Market Leadership: Fly ash-based cement holds around 38% share, remaining the backbone of clinker substitution strategies due to established ASTM and EN standards, cost efficiency, and strong availability across major producing economies.

- Infrastructure Fastest-Growing Segment: Infrastructure represents the fastest-growing application segment, propelled by large-scale public investment programs such as the UK’s GBP 725 billion infrastructure pipeline and Saudi Arabia’s Vision 2030 giga-projects mandating sustainable construction materials.

- Geopolymer Cement Accelerating Adoption: Geopolymer cement is rapidly expanding as a clinker-free alternative, supported by regulatory acceptance, superior durability in roads and bridges, and CO2 emissions reductions of up to 60-70% compared to conventional Portland cement.

- North America Policy and Investment Momentum: North America captures roughly 15% market share, strengthened by U.S. construction spending of USD 2.2 trillion, SCM supply consolidation, carbon capture funding, and recycled content mandates under state-level Buy Clean policies.

- Growth Indicator: Strategic collaborations in carbon capture, electrified kilns, and zero-carbon heat solutions are accelerating deep decarbonisation, creating scalable commercial pathways for next-generation green cement production globally.

| Key Insights | Details |

|---|---|

| Market Green Cement Size (2026E) | US$ 37.7 Bn |

| Market Value Forecast (2033F) | US$ 74.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.9% |

Market Dynamics

Drivers - Carbon Emission Regulations and Policy Mandates Accelerate Low-Clinker Cement Adoption

Binding carbon regulations at national and supranational levels are the most powerful structural driver of the Green Cement Market, compelling producers to reformulate products or face material financial penalties. The EU Carbon Border Adjustment Mechanism (CBAM), fully operative from January 2026, requires importers to purchase carbon certificates for embedded emissions in cement, iron, steel, and fertilisers, effectively equalising the cost burden between EU27 producers and overseas suppliers. Together with the EU Emissions Trading System (ETS), which is phasing out free allowances for cement producers through 2034, this framework incentivises clinker substitution and SCM adoption.

In India, NITI Aayog has published a formal Roadmap for Cement Sector Decarbonisation, targeting clinker-to-cement ratio reductions from the current 67.5% toward the global threshold. China's 14th Five-Year Plan mandates peak carbon by 2030 and carbon neutrality by 2060, directly requiring low-carbon material transitions across its cement industry. These binding regulatory environments collectively define investment and production priorities for companies operating within the green cement market.

Technological Innovation in Calcination and Carbon Capture Enables Deep Emission Cuts

Advanced industrial technologies are transforming the calcination stage of cement production, enabling near-zero emissions without compromising cement performance or throughput. Calcination generates roughly 60% of cement-related CO2, making it the priority intervention point for decarbonization. Adani Cement and Coolbrook (Finland) completed the world's first commercial deployment of Coolbrook's RotoDynamic Heater technology at Adani Cement's Boyareddypalli plant in Andhra Pradesh, delivering carbon-free industrial heat with an expected reduction of approximately 60,000 tonnes of CO2 annually and potential to scale ten times.

Cemex secured a EUR 157 million EU Innovation Fund grant for carbon capture at its Rüdersdorf plant, while also reporting a 15 to 18% reduction in Scope 1 and 2 CO2 emissions since 2020 and noting that its Vertua low-carbon line accounts for 63% of total cement sales. Digitalisation, artificial intelligence, and advanced process automation are further deployed across plant operations to reduce energy consumption by optimising kiln temperatures and raw material blending in real time. These technology investments make the Green Cement Market accessible to producers seeking both compliance and competitive differentiation.

Urban Infrastructure Demand and Housing Deficits Create Sustained Volume Requirements

Infrastructure investment programs worldwide are generating multi-decade cement demand that can only be fulfilled sustainably through green cement formulations. Globally, an estimated 21 million new homes are needed each year to accommodate urbanisation. In India, the government raised capital expenditure by 11.1% to USD 133 billion in FY 2024 to 2025, equivalent to 3.4% of GDP, and the PMAY-U program has sanctioned 1.18 crore houses with 86.6 lakh already completed.

The US construction sector recorded total annual spending of USD 2.2 trillion in 2024, representing 4.5% of GDP, with 1.6 million new homes built in the same period. The UK government has committed to a GBP 725 billion investment plan, creating procurement opportunities for green materials. Saudi Arabia's Vision 2030 giga-projects, including NEOM, The Line, King Salman Park, and Diriyah Gate, demand sustainable construction inputs. These large-scale, policy-funded programs systematically channel volume toward the Green Cement Market as public procurement criteria mandate low-carbon materials.

Restraint - High Capital Requirements for SCM Processing Infrastructure Constrain Smaller Producers

Converting existing plants to process supplementary cementitious materials and alternative fuels requires capital expenditure in preprocessing, handling, and quality testing infrastructure. Logistics premiums of USD 15 to USD 30 per tonne for transported SCMs add to operating costs. Small and mid-sized producers without vertically integrated supply chains face disproportionate financial barriers to adoption, limiting competitive reach and slowing the pace of clinker substitution in cost-sensitive regional markets.

Declining Coal Power Generation Threatens Consistent Fly Ash Supply

Fly ash availability is structurally linked to coal-fired power generation, which is contracting under national decarbonization commitments in Europe and North America. This supply contraction introduces long-term feedstock uncertainty, as imported fly ash carries additional cost and quality variability risks. India and China currently produce over 250 million metric tonnes of fly ash annually, but quality inconsistencies and transportation constraints limit their capacity to compensate globally. Slag supply is similarly subject to shifts in steel manufacturing toward electric arc furnaces, demanding long-term contractual frameworks that smaller operators are ill-equipped to secure.

Opportunities - Carbon Capture, Utilisation, and Storage Partnerships Unlock Structural Emission Reductions

CCUS represents the next frontier for deep decarbonization in the cement sector, particularly for process emissions that cannot be eliminated by SCM substitution alone. It addresses the irreducible chemical CO2 released during clinker formation, which constitutes approximately 60% of cement emissions and is inaccessible to fuel or material changes.

The India to Sweden Industry Transition Partnership launched seven green-industry projects targeting deep decarbonization in cement and steel, with participation from Ambuja Cements, IIT Bombay, JK Cement, EcoTech Solutions, and Cemvision. These initiatives focus on integrated carbon-capture and utilisation units and conversion of steel slag into SCMs, enabling circular low-carbon cement. The Green Cement Market stands to benefit substantially from policy-funded pilot programs that reduce the commercialisation risk of CCUS for smaller adopters.

Electrified Kiln Technologies and Zero-Carbon Heat Solutions Create New Production Models

Zero-carbon heat technologies allow cement producers to fully decouple clinker production from fossil fuel consumption, addressing the most energy-intensive and carbon-intensive stage of the manufacturing process without altering the final product specification.

Conch Group (China) and CATL (China) signed a strategic cooperation agreement to implement zero-carbon factories, electrified logistics, and smart mining operations across their cement and building materials production. Combined with Coolbrook's RotoDynamic Heater deployment at Adani Cement, these partnerships demonstrate a commercially viable pathway to fossil-free calcination. The Green Cement Market is positioned to absorb these technologies at scale as investment costs decline and demonstrated plant performance data confirms commercial viability.

Waste-to-Resource Integration Through Municipal Solid Waste and Industrial Byproducts

Co-processing of industrial byproducts and municipal waste in cement kilns enables dual benefits: reduction of fossil fuel dependency and diversion of waste from landfill, consistent with circular economy policy frameworks. It directly addresses both SCM supply and alternative fuel use within a single operational framework.

India generates approximately 62 million tonnes of municipal solid waste annually, projected to reach 436 million tonnes by 2050, providing a large and proximate feedstock for refuse-derived fuel. CRH acquired Eco Material Technologies for USD 2.1 billion, gaining a national network of over 125 facilities that recycle 7 million tonnes of fly ash and 3 million tonnes of synthetic gypsum annually across North America. The Green Cement Market benefits from these models as regulatory support for waste co-processing deepens across major economies.

Category-wise Analysis

Product Type Insights

Fly Ash-Based Cement leads the product type segment, holding approximately 38% of total market share. Its dominance reflects a favourable combination of material availability, established technical standards, and cost competitiveness. Fly ash, sourced as a byproduct of coal combustion in thermal power plants, provides pozzolanic reactivity that contributes to concrete strength and durability while displacing clinker, thereby avoiding approximately 0.83 tonnes of CO2 per tonne substituted. Standardisation under frameworks such as EN 450 in Europe and ASTM C618 in North America ensures quality benchmarks that support widespread specification by engineers and procurement authorities.

Geopolymer Cement is the fastest-growing product type in the Global Green Cement Market. Unlike fly ash-based blended cements, geopolymers are produced entirely without clinker, using alkali activation of aluminosilicate precursors such as fly ash or slag, and emit between 0.25 to 0.35 tonnes of CO2 per tonne compared to approximately 0.83 tonnes for conventional Portland cement.

New Zealand's Building Code formally equates geopolymer cement performance with Portland cement, setting a regulatory precedent that other jurisdictions are beginning to follow. Governments and procurement bodies in infrastructure-intensive regions are mandating or incentivising their use, with California's Buy Clean Act specifying recycled content thresholds that geopolymers readily satisfy. Research published in Scientific Reports confirmed viable geopolymer mortars using ferrochrome slag and fly ash meeting structural grade requirements, reinforcing technical credibility.

Application Insights

The Residential segment leads the application segment with approximately 42% market share in 2026. Residential construction is the single largest consumer of cement globally, and housing deficits across developing and developed economies alike ensure sustained demand. Government programs provide direct volume mandates: India's PMAY-U sanctioned 1.18 crore affordable houses with 86.6 lakh already completed, while the US completed 1.6 million new homes in 2024. Green cement formulations are increasingly mandated or preferred in subsidised housing programs due to cost savings from lower clinker content and compliance with evolving building codes that incorporate embodied carbon standards. India's real estate market is projected to reach USD 5.8 trillion by 2047, contributing 15.5% of GDP, ensuring that residential construction will remain the dominant channel.

Infrastructure is the fastest-growing application segment in the Green Cement Market. The scale, public funding, and procurement criteria of national infrastructure programs create structured demand for low-carbon construction materials that private residential builders are slower to adopt. The UK government committed to a GBP 725 billion infrastructure investment plan with green material integration requirements. Saudi Arabia's Vision 2030 giga-projects include NEOM, The Line, and Diriyah Gate, all requiring high-volume, performance-grade cement. The IMF projects Middle East GDP growth at 4.2%, supporting construction activity on a large scale. Geopolymer concrete, favoured in this segment, is projected by industry analysis to record its fast adoption in infrastructure and public works through the forecast period, given superior chemical resistance and durability in roads, bridges, and sewage systems.

Regional Insights and Trends

Asia Pacific Green Cement Market Trends

Asia Pacific holds 56% of the global green cement market, underpinned by China and India's status as the world's two largest cement producers and their national commitments to carbon neutrality. Asia Pacific accounts for more than 50% of global cement production. China leads regional demand, with its 14th Five-Year Plan targeting peak carbon emissions by 2030 and carbon neutrality by 2060, alongside the "Green GDP" initiative that incentivises low-carbon industrial practices.

China's Belt and Road Initiative involve large-scale cross-border infrastructure projects, many of which prioritise sustainable materials. Conch Group and CATL signed a cooperation agreement for zero-carbon factories, electrified logistics, and smart mining for cement production. Taiwan Cement Corporation issued Taiwan's first Sustainability-Linked Convertible Bond worth NTD 8 billion, linking yields to greenhouse gas reduction targets and a commitment to carbon-neutral concrete by 2050

India, as the world's second-largest cement producer, recorded output of 391 million tonnes in 2023 and faces a projected emission pathway of 1,323 MtCO2e annually by 2070 under business-as-usual, according to NITI Aayog. The government's capital expenditure of USD 133 billion in FY 2024 to 2025 and the India to Sweden Industry Transition Partnership collectively channel investment into green cement through CCU units, slag conversion, and co-processing with municipal solid waste. Navrattan Group launched green cement into the Indian market to provide a sustainable alternative to traditional Portland cement. India aims for 40% renewable energy by 2030, directly supporting clean energy inputs for cement kilns.

North America Green Cement Market Trends

North America holds 15% of the global green cement market, with the United States representing the dominant sub-market driven by construction scale and emerging procurement mandates. Total US construction spending reached USD 2.2 trillion in 2024, representing 4.5% of GDP, with the sector employing over 8.2 million people. CRH acquired Eco Material Technologies for USD 2.1 billion, securing a national network of over 125 facilities recycling 7 million tonnes of fly ash and 3 million tonnes of synthetic gypsum annually, the largest SCM supply consolidation in North American history. Holcim and CRH jointly invested USD 75 million in Sublime Systems (USA), whose electrochemical cement production method reduces CO2 by up to 90% compared to conventional cement.

Cemex and the Mission Possible Partnership, supported by the Bezos Earth Fund, launched a joint decarbonization analysis at Cemex's Balcones plant in Texas, examining alternative fuels, low-carbon materials, CCUS, and kiln electrification. The California Buy Clean Act mandates recycled content thresholds that favor fly ash and geopolymer formulations, while EPA rules on coal combustion residuals promote fly ash reuse over landfilling. The American Coal Ash Association reports that close to 50% of collected fly ash is already repurposed in construction applications, providing a strong feedstock base.

Europe Green Cement Market Trends

Europe holds 18% of the global green cement market, where the regulatory environment is the most advanced globally and investment into net-zero cement facilities is accelerating. CBAM entered full force in January 2026, requiring importers to pay carbon certificates equivalent to EU-based producers and removing the competitive advantage of high-emission cement imports. The EU ETS phases out free allowances for cement through 2034, creating a progressive internal carbon cost. EU construction output averaged a decline of 0.9% annually in 2024, with civil engineering output stable and building construction recovering in markets such as Spain at plus 11.2% annual growth and Czechia at plus 9.7%.

Hoffmann Green Cement Technologies (France) tripled production of zero% clinker cement to 50,700 tonnes, targeting 100,000 tonnes, following domestic and international certifications. Titan Cement International (Greece) outlined its "Green Growth: Strategic Directions 2026" with a commitment to double low-carbon cement volumes and achieve an emission reduction of over 18% per tonne of cementitious material, targeting 550 kg CO2 per tonne. EnviroTech London 2026 convened over 200 industry stakeholders under the theme "The Gateway to Green Cement" to advance low-carbon technologies, decarbonization policy, and circular construction strategies. The Green Cement and Concrete Innovation Summit Europe 2026, held amid the UK's GBP 725 billion infrastructure plan, further reflects the region's structural commitment to accelerating green cement deployment.

Competitive Landscape

The global green cement market is moderately consolidated, dominated by major multinational players such as Holcim, LafargeHolcim, Cemex, Titan Cement International, Taiwan Cement Corporation (TCC), and Adani Cement, who led through investments in low-carbon technologies, supplementary cementitious materials, and digitalised manufacturing. These companies leverage global networks, R&D capabilities, and partnerships with innovators like Sublime Systems and Coolbrook to introduce low-carbon products such as ECOPlanet, ECOPact, and Vertua, enhancing their competitive edge.

The market shows regional fragmentation, with smaller players like Navrattan Group entering emerging markets such as India and Latin America to meet local sustainable construction demand. Competition is driven by technological differentiation, regulatory pressures, and sustainability commitments, pushing both global and regional players to adopt innovative decarbonization strategies. This combination of dominant multinational leaders and active regional participants defines a market that is consolidated yet dynamically evolving, with continuous growth in green cement adoption worldwide.

Key Industry Developments:

- In March 2026, EnviroTech London 2026, “The Gateway to Green Cement,” will convene global cement industry leaders, technical experts, and stakeholders to showcase the latest low-carbon technologies, decarbonisation processes, and policy strategies, driving innovation, collaboration, and market development in the green cement sector.

- In January 2026, Hoffmann Green Cement Technologies achieved a major milestone by tripling its low-carbon, 0% clinker cement production to 50,700 tonnes in 2025 (up from 16,269 tonnes in 2024) and set a 2026 target of 100,000 tonnes, driven by expanding demand, new construction projects, and recent certifications, highlighting rapid market growth and adoption of green cement solutions.

- In July 2025, CRH (Global) acquired Eco Material Technologies from One Equity Partners, Warburg Pincus, and Green Cement Investments for $2.1 billion, gaining control of a leading North American supplier of Supplementary Cementitious Materials (SCMs) and near-zero-carbon cement alternatives. Eco Material, formed from Boral Limited’s fly ash business and Green Cement Inc, operates a national network of 125+ facilities and annually recycles 7 million tons of fly ash and 3 million tons of synthetic gypsum, significantly advancing green cement production and low-carbon construction solutions across North America.

Companies Covered in Green Cement Market

- LafargeHolcim

- Taiwan Cement Corporation

- ACC Ltd.

- CEMEX S.A.B. de C.V.

- China National Building Materials

- Green Cement Inc.

- Anhui Conch Cement

- Heidelberg Cement

- CRH Plc

- Ultratech Cement Ltd

Frequently Asked Questions

The global green cement market is projected to be valued at US$ 37.7 Bn in 2026.

The Fly Ash-Based Cement segment is expected to account for approximately 38% of the Global Green Cement Market by Material Type in 2026.

The green cement market is expected to witness a CAGR of 10.2% from 2026 to 2033.

Global green cement market growth is driven by binding carbon regulations (CBAM, ETS, national decarbonisation roadmaps), breakthrough calcination and carbon-capture technologies, and large-scale infrastructure and housing investments that mandate low-carbon construction materials.

Key market opportunities in the global green cement market lie in scaling CCUS partnerships, deploying electrified and zero-carbon kiln technologies, and expanding waste-to-resource integration models that convert industrial byproducts and municipal waste into low-carbon cement inputs.

Key players in the Green Cement Market include Heidelberg Cement AG, CEMEX S.A.B. de C.V., Holcim, Titan Cement International, Taiwan Cement Corporation (TCC), and Adani Cement.