- Automation & Robotics

- Generator Sets Market

Generator Sets Market Size, Share, and Growth Forecast 2026 - 2033

Generator Sets Market by Load Capacity (Below 75 kVA, 75-375 kVA, 375-750 kVA, 750-2000 kVA, Above 2,000 kVA), Fuel Type (Diesel, Natural Gas, Others), Mobility (Stationary, Portable), Application (Prime/Continuous, Standby, Peak Shaving), End-user (Commercial, Residential, Oil & Gas, Construction & Mining, Marine, Healthcare, Data Center, Others), and Regional Analysis, 2026 - 2033

Generator Sets Market Size and Trend Analysis

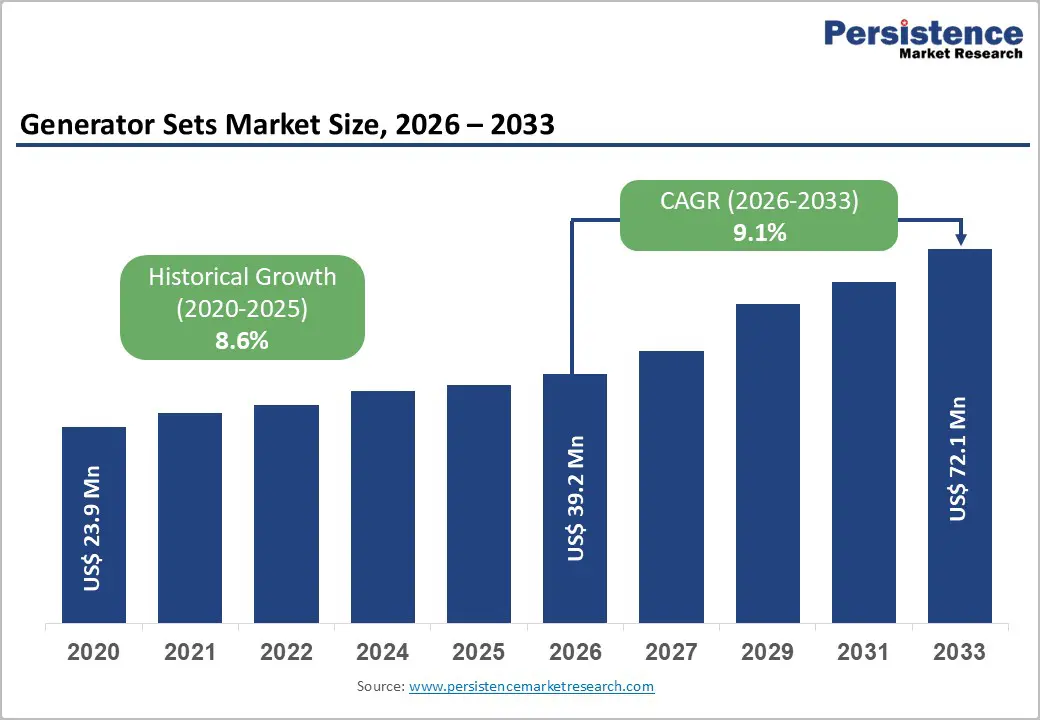

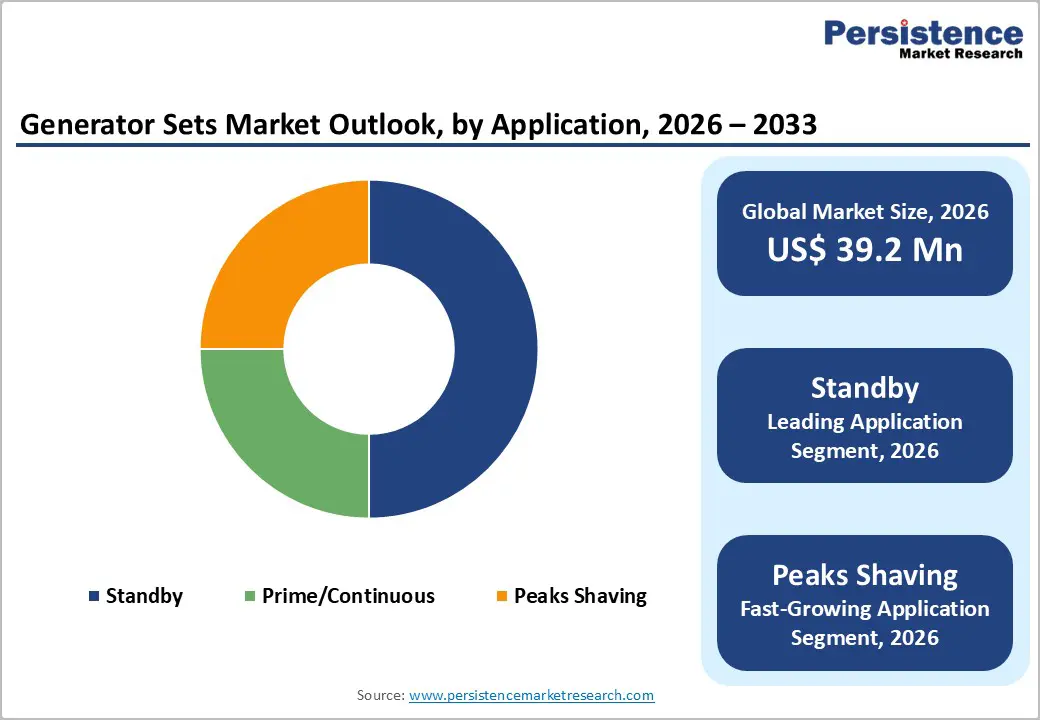

The global generator sets market size is expected to be valued at US$ 39.2 billion in 2026 and projected to reach US$ 72.1 billion by 2033, growing at a CAGR of 9.1% between 2026 and 2033.

Surging demand for reliable backup power, accelerating data center construction, and persistent grid instability across emerging economies are the principal catalysts propelling this growth. According to the U.S. Department of Energy, the country faces a projected dispatchable power shortfall of 78 GW by 2030, underscoring the urgency of distributed power solutions. Simultaneously, the rapid expansion of digital infrastructure globally and rising frequency of extreme weather events are compelling industries across healthcare, oil & gas, and construction to prioritize uninterrupted power generation, sustaining robust demand for generator sets across all capacity ranges and fuel types.

Key Industry Highlights

- Leading Region: Asia Pacific accounts for approximately 37% of global generator sets revenue in 2025, underpinned by rapid industrialization, persistent grid instability, and massive infrastructure investments across China, India, and ASEAN nations.

- Fastest Growing Region: The Middle East & Africa region is projected to register the highest CAGR during 2026 - 2033, driven by Saudi Arabia's Vision 2030 mega-infrastructure projects, Sub-Saharan grid electrification deficits, and large-scale industrial zone developments.

- Dominant Segment: Diesel generator sets command approximately 65% of global market share in 2025, sustained by superior energy density, universal fuel availability, and proven load-handling performance across industrial, commercial, and emergency standby applications worldwide.

- Fastest Growing Segment: The Data Center end-use segment is the fastest growing category, driven by the global AI compute boom and hyperscale cloud infrastructure expansion, with data center generator installations growing at 16% year-on-year in 2024.

- Key Market Opportunity: The transition to low-emission power generation presents significant revenue opportunities, with gas-powered genset sales growing 21% in 2024 and Cummins and Rolls-Royce actively commercializing HVO-compatible and hydrogen-ready generator platforms.

| Key Insights | Details |

|---|---|

| Generator Sets Market Size (2026E) | US$ 39.2 Billion |

| Market Value Forecast (2033F) | US$ 72.1 Billion |

| Projected Growth CAGR (2026 - 2033) | 9.1% |

| Historical Market Growth (2020 - 2025) | 8.6% CAGR |

Market Dynamics

Drivers - Rising Frequency of Power Outages and Grid Vulnerabilities

Increasing grid instability is a foundational driver for the global generator sets market. According to the U.S. Energy Information Administration (EIA), U.S. electricity customers experienced an average of 5.5 hours of power interruptions per year in 2022, with weather-related events accounting for the majority of outages. Globally, developing economies face even steeper reliability deficits; for instance, Nigeria's peak grid supply of approximately 6,003 MW in 2024 falls dramatically short of actual demand, forcing commercial and industrial users to treat gensets as primary power infrastructure. This dynamic is similarly pronounced across South and Southeast Asia, Latin America, and Sub-Saharan Africa, where utilities struggle to meet burgeoning urban and industrial electricity loads, making generator sets indispensable for business continuity and economic productivity.

Exponential Growth of Data Centers and Digital Infrastructure

The global proliferation of hyperscale and colocation data centers is generating unprecedented demand for high-capacity, mission-critical generator sets. The International Energy Agency (IEA) estimates that global data center electricity consumption could double by 2026, reaching approximately 1,000 TWh annually. Each large hyperscale facility typically deploys multiple generators ranging from 750 kVA to above 2,000 kVA as N+1 redundancy backup systems, ensuring zero downtime for cloud computing, AI workloads, and streaming services. Data center generator installations grew by 16% year-on-year in 2024, and this trajectory is expected to steepen as AI-driven compute demand escalates. Major cloud providers such as Amazon Web Services, Microsoft Azure, and Google Cloud continue to announce large-scale facility expansions, directly stimulating demand for premium standby power solutions.

Restraints - Stringent Emission Regulations and Compliance Costs

Tightening environmental regulations pose a significant challenge to genset market growth, particularly for diesel-powered units. The U.S. Environmental Protection Agency's (EPA) Tier 4 Final mandate requires reductions of over 90% in NOx and particulate matter emissions from Tier 1 baseline levels, substantially increasing the cost of compliant engines. Similarly, the European Union's Stage V off-road emission standards and India's CPCB IV+ norms require advanced after-treatment technologies such as Selective Catalytic Reduction (SCR) and Diesel Particulate Filters (DPF), increasing unit prices by 10-20%. These cost escalations create adoption barriers, particularly for price-sensitive small and medium enterprise (SME) customers across emerging markets.

Volatility in Diesel Fuel Prices and Supply Chain Disruptions

Fuel price volatility remains a persistent restraint, given that diesel generator users attribute up to 70% of lifecycle operational costs to fuel expenditure. Average wholesale diesel in the United States fluctuated between US$ 3.30 and US$ 4.05 per gallon during 2024, creating unpredictable operating budgets for end users. In remote mining and island grid applications, supply chain disruptions can create multi-week fuel shortages, limiting operational reliability. This economic uncertainty is accelerating feasibility studies on alternative fuels and hybrid energy storage systems, but the transition timeline remains extended for many large installed-base users.

Opportunities - Transition to Gas-Powered and Hybrid Generator Systems

The global shift toward cleaner energy presents a compelling opportunity for natural gas, dual-fuel, and hydrogen-ready generator set manufacturers. Gas-powered generator set sales grew by 21% in 2024, reflecting accelerating adoption driven by lower emissions and more stable operating costs compared to diesel. In September 2025, Cummins Inc. unveiled a new line of hydrogen-powered generator sets, signaling a pivotal industry shift toward decarbonized power generation. Governments across Europe, North America, and Asia Pacific are actively incentivizing clean energy backup power through grants, tax credits, and regulatory frameworks. The European Union's REPowerEU Plan and the U.S. Inflation Reduction Act (IRA) both contain provisions that encourage investments in low-emission and alternative-fuel power infrastructure. Market participants developing dual-fuel and HVO-compatible gensets are well-positioned to capture significant incremental revenue in regions subject to strict carbon reduction mandates.

Surging Infrastructure Investment in Middle East, Africa, and South Asia

Massive public infrastructure spending programs across the Middle East and Africa represent a high-growth demand corridor for generator sets. Saudi Arabia's Vision 2030 program encompasses over US$ 1 trillion in planned infrastructure projects, including NEOM city, hospitality mega-projects, and industrial zones, all requiring reliable prime and standby power solutions. India's Interim Budget 2024-25 allocated approximately US$ 134 billion (3.4% of GDP) to infrastructure development, accelerating construction and manufacturing sector genset demand. In Sub-Saharan Africa, grid electrification rates remain critically low, creating vast addressable markets for prime-power generator solutions. Companies that localize manufacturing, establish robust distribution networks, and offer rental or genset-as-a-service models are poised to capture outsized growth in these underpenetrated markets.

Category-wise Analysis

Load Capacity Insights

The 75-375 kVA segment is the leading load capacity category in the global generator sets market, commanding approximately 38% of total market share in 2025. This dominance is attributed to the segment's versatility across a broad range of commercial, industrial, and institutional applications, including hospitals, hotels, mid-size manufacturing facilities, and telecommunications infrastructure. The segment benefits from a favorable balance of power output, installation footprint, and procurement cost that aligns with the budget parameters of small-to-medium enterprises and institutional buyers. Diesel generators in this range are extensively deployed as standby power systems for commercial real estate, providing compliance with building safety codes in markets including the United States, India, and Southeast Asia. The fastest growing segment is Above 2,000 kVA, driven by hyperscale data centers and large industrial applications demanding high-capacity, mission-critical power backup.

Fuel Type Insights

Diesel remains the dominant fuel type in the global generator sets market, accounting for approximately 65% of total market share in 2025. Diesel generator sets offer superior energy density, fuel availability, and load-handling performance compared to alternatives, making them the preferred choice for industrial prime power, construction sites, and emergency standby applications. The maturity of diesel engine technology, combined with widespread global diesel distribution infrastructure, reinforces this segment's leadership position. Additionally, diesel gensets in the 75 kVA to 2,000 kVA range continue to dominate procurement in regions experiencing frequent grid outages, particularly across Sub-Saharan Africa and South Asia. Meanwhile, Natural Gas is the fastest growing fuel segment, expanding at a strong CAGR as emission regulations tighten and gas infrastructure matures globally.

Mobility Insights

Stationary generator sets represent the dominant mobility segment, accounting for approximately 70% of the global market in 2025. Stationary gensets are permanently installed at facilities requiring continuous or standby backup power, including data centers, hospitals, manufacturing plants, and commercial buildings. The high capital investment in these installations is justified by the critical nature of power continuity requirements in these environments. NFPA 110 (National Fire Protection Association) standards in the United States and equivalent international codes mandate stationary backup power systems in healthcare, high-rise commercial buildings, and emergency services facilities. Portable generator sets represent the fastest growing mobility segment, benefiting from rising demand in construction, events, disaster recovery, and off-grid applications, with portable generator rentals increasing by 20% globally in 2024.

Application Analysis

The Standby application segment commands the leading position in the generator sets market, holding approximately 50% of total market share in 2025. Standby generators are deployed exclusively as emergency backup systems that activate automatically during grid power failures, making them essential investments for facilities where power interruptions carry significant operational, safety, or financial consequences. Regulatory frameworks in healthcare, telecommunications, and data center sectors mandate standby power provisions, creating a captive and recurring demand pool. The Joint Commission in the United States, for example, requires hospitals to maintain 96-hour fuel reserves for standby generators. The Peak Shaving application is the fastest growing segment, as commercial and industrial users increasingly leverage generators to reduce utility demand charges during peak consumption periods, offering attractive economic returns on generator investment.

End-user Insights

The Commercial end-use segment is the dominant category in the generator sets market, accounting for approximately 45% of total market share in 2025. Commercial establishments, including office buildings, retail centers, hotels, hospitals, and educational institutions, represent the largest aggregate consumer of backup power solutions globally. This segment's leadership is underpinned by stringent life-safety codes, business continuity mandates, and tenant expectations for uninterrupted operations in developed markets. The U.S. commercial real estate sector alone maintains millions of installed standby generator units across healthcare facilities, telecommunications hubs, and high-rise office developments. The Data Center end-use segment is the fastest growing category, registering double-digit CAGR growth driven by the AI compute boom, cloud infrastructure expansion, and stringent uptime SLA requirements across global hyperscale and colocation operators.

Regional Insights

North America Generator Sets Market Trends and Insights

North America represents the second largest regional market for generator sets globally, characterized by strong regulatory frameworks, mature infrastructure, and high technology adoption rates. The United States drives regional demand, with the U.S. Department of Energy projecting a 78 GW dispatchable power shortfall by 2030, catalyzing substantial investment in distributed backup power across data centers, healthcare systems, and industrial facilities. Escalating severity of hurricane, wildfire, and ice storm events has heightened residential and commercial awareness of energy security, driving robust demand for both stationary and portable gensets.

The EPA Tier 4 Final emission standards are reshaping the North American market toward cleaner, more fuel-efficient diesel and gas generator solutions. In June 2025, Rolls-Royce committed US$ 24 million to expand its mtu Series 4000 diesel generator manufacturing capacity in Mankato, Minnesota, targeting surging data center demand. Canada is also witnessing growing adoption of natural gas gensets driven by its extensive pipeline infrastructure and provincial clean air policies, reinforcing the region's transition toward lower-emission backup power technologies.

Europe Generator Sets Market Trends and Insights

Europe's generator sets market is shaped by stringent environmental compliance, energy security imperatives heightened post-2022 geopolitical disruptions, and the continent's accelerating renewable energy transition. EU Stage V emission norms are the primary regulatory driver, compelling OEMs to invest in advanced after-treatment systems and gas-capable platforms across Germany, the United Kingdom, France, and Spain. Germany is projected to register a CAGR of 8.5% in the generator sets market, supported by its industrial base, manufacturing sector resilience, and backup power requirements for critical digital infrastructure.

The REPowerEU Plan and diversification of energy sources have elevated awareness of backup power for both industrial and institutional users. The United Kingdom's growing data center ecosystem, particularly in the Greater London area, has spurred demand for premium high-capacity standby gensets compliant with local noise and emission standards. In July 2024, Wartsila introduced a prefabricated, modular, scalable power generation solution specifically designed for data centers, highlighting Europe's leadership in smart, low-carbon generator innovation.

Asia Pacific Generator Sets Market Trends and Insights

Asia Pacific is the leading regional market for generator sets globally, commanding approximately 37% of total revenue share in 2025, driven by rapid industrialization, urbanization, and persistent grid reliability challenges across China, India, Indonesia, and Vietnam. China is projected to grow at a CAGR of 10.0%, supported by expansive data center construction, manufacturing sector backup power requirements, and government-backed energy security investments. Industrial generator set production volume in China increased by 19% in 2024, reflecting the country's dominant role as both a manufacturer and consumer.

India represents a high-priority growth market, expected to grow at 9.3% CAGR, supported by its US$ 134 billion infrastructure budget allocation in 2024-25 and rising commercial real estate development in major metropolitan areas. The Middle East and Africa region is the fastest growing globally, with Saudi Arabia leading CAGR performance driven by Vision 2030 construction projects. ASEAN economies including Vietnam and Indonesia are experiencing strong manufacturing FDI inflows, creating sustained demand for prime and standby power solutions in new industrial zones and export processing clusters.

Competitive Landscape

The global generator sets market exhibits a moderately consolidated structure, with a limited number of multinational manufacturers accounting for a substantial share of industry revenue. Large players maintain strong market positions through broad product portfolios covering diesel, natural gas, and hybrid generator platforms, supported by extensive distribution networks and after-sales service capabilities. At the same time, several regional manufacturers and specialized suppliers operate in niche segments, intensifying competition across price-sensitive and application-specific markets.

Competition is increasingly centered on technology integration, service expansion, and geographic penetration. Companies are investing in digital platforms incorporating IoT-enabled monitoring, remote diagnostics, and predictive maintenance to enhance reliability and generate recurring service revenue streams. In parallel, manufacturers are expanding operations in emerging markets across Asia Pacific, the Middle East, and Africa where power infrastructure gaps continue to drive genset demand. Product innovation is also focusing on low-emission, gas-based, and hydrogen-ready generator technologies, aligning with tightening environmental regulations and long-term energy transition trends.

Key Developments

- January, 2025: FÉTIS Group launched a hydrogen-powered hybrid generator set at the Hyvolution exhibition in Paris, designed for low-carbon on-site power generation, reducing carbon emissions by around 70% and targeting applications such as events, rentals, and renewable energy installations.

- June, 2025: Rolls-Royce committed US$ 24 million to more than double production capacity of its mtu Series 4000 diesel generator sets in Mankato, Minnesota, targeting surging U.S. data center demand.

- August, 2025: Caterpillar Inc. launched the Cat D1500 diesel generator set, delivering 1.5 MW of standby power from a compact 32.1-liter C32B engine, featuring up to 13% smaller footprint and 32% lighter design to improve installation efficiency and reliability for space-constrained backup power applications.

Companies Covered in Generator Sets Market

- Caterpillar Inc.

- Cummins Inc.

- Deere & Company

- Generac Power Systems, Inc.

- General Electric (GE Vernova)

- Honda Siel Power Products Ltd.

- Kohler Co.

- Briggs and Stratton Corporation

- Kirloskar Electric Company Ltd.

- Atlas Copco AB

- Mitsubishi Heavy Industries Ltd.

- Wartsila Corporation

- Rolls-Royce (mtu Onsite Energy)

- Sterling and Wilson

- Aggreko plc

- Himoinsa (Yanmar Group)

- Perkins Engines Company Limited

- Doosan Portable Power

Frequently Asked Questions

The global Generator Sets market is estimated to reach US$ 39.2 Billion in 2026 and is projected to grow to US$ 72.1 Billion by 2033 at a CAGR of 9.1%.

Rising power outages, expansion of data centers, increasing infrastructure investments, and growing adoption of natural gas and hybrid gensets are the primary demand drivers.

Asia Pacific leads the global Generator Sets market with around 37% revenue share, driven by industrialization and infrastructure expansion in countries such as China and India.

The key opportunity lies in the adoption of natural gas, dual-fuel, and hydrogen-ready generator sets supported by energy transition policies and large infrastructure investments.

Key players include Caterpillar Inc., Cummins Inc., Kohler Co., Generac Power Systems, Inc., Atlas Copco AB, Rolls‑Royce Holdings plc, Wärtsilä Corporation, Mitsubishi Heavy Industries, and General Electric.