- Industrial Goods & Service

- Firefighting Foam Market

Firefighting Foam Market Size, Share, and Growth Forecast 2026 - 2033

Firefighting Foam Market by Foam Type (Aqueous Film Forming Foam (AFFF), Alcohol-Resistant Aqueous Film Forming Foam (AR-AFFF), Protein Foam, Synthetic Detergent Foam, Fluorine-Free Foam (F3), High-Expansion Foam), by Fire Class (Class A Fires, Class B Fires, Class C Fires), by Application, by End Use, by Regional Analysis, 2026 - 2033

Firefighting Foam Market Size and Trend Analysis

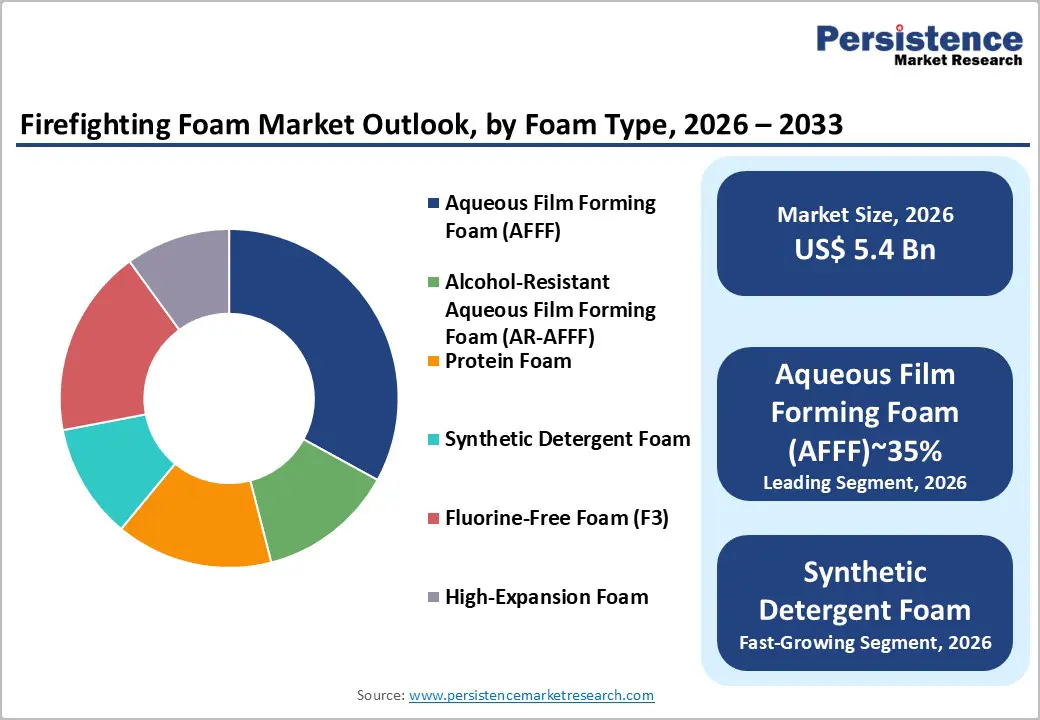

The global firefighting foam market size is likely to be valued at US$ 5.4 Billion in 2026 and is expected to reach US$ 7.0 Billion by 2033, growing at a CAGR of 3.7% during the forecast period from 2026 to 2033.

The market's steady growth trajectory is underpinned by escalating industrial fire hazard risks, tightening mandatory fire safety regulations across oil and gas, aviation, and chemical end-use sectors, and a transformative regulatory-driven shift toward environmentally compliant foam formulations.

Key Industry Highlights:

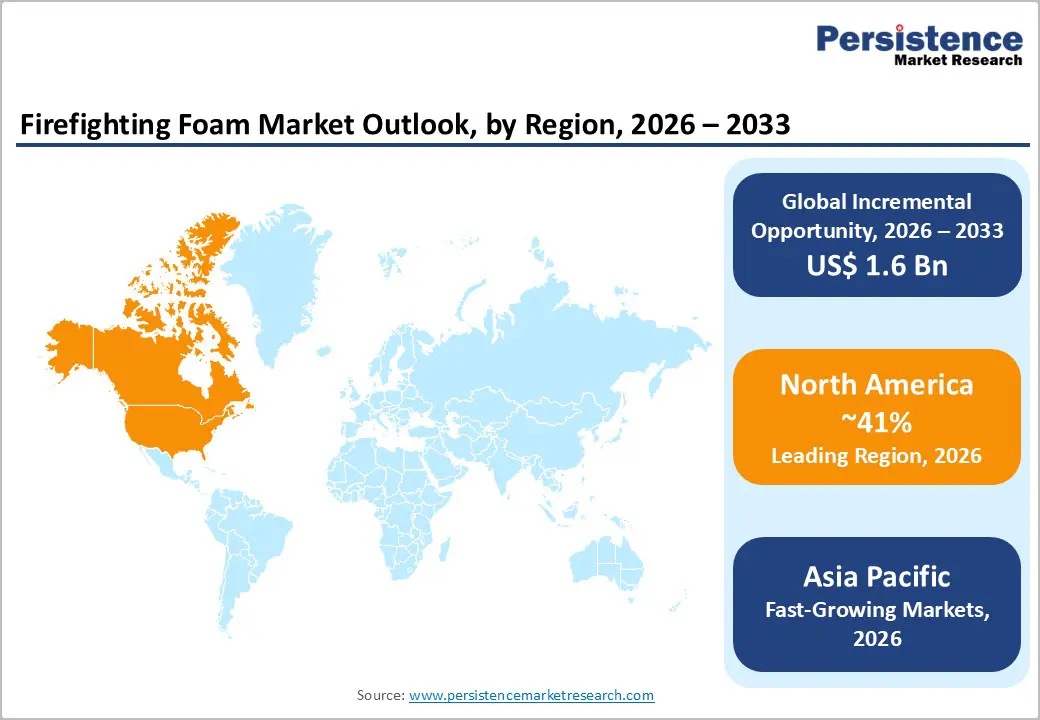

- Leading Region: North America is a leading firefighting foam innovation hub holding 41% share in the market, accelerated by the U.S. NDAA's mandate for DoD PFAS foam phase-out, EPA PFAS MCLs, and over 1,400 fire departments actively transitioning to fluorine-free alternatives, driving major OEM R&D and manufacturing investment.

- Fastest-Growing Region: Asia Pacific is the fastest-growing regional market, with rising CAGR of 5.1%, driven by India's UDAN airport rollout, China's petrochemical complex growth, and ASEAN LNG infrastructure investments generating sustained foam system procurement demand.

- Leading Region: Class B fire suppression is the dominant application category with approximately 62% market share, anchored by mandatory NFPA 11 and ICAO ARFF standards governing foam systems at petroleum storage facilities, international airports, marine fuel depots, and chemical plants worldwide.

- Fastest-Growing Segment: Fluorine-Free Foam (F3) is the fastest-growing foam type segment, propelled by EU COMMISSION REGULATION (EU) 2025/1988 mandating full PFAS phase-out by 2030 and the U.S. NDAA directive, compelling systemic fleet replacement across military, industrial, and municipal fire service sectors.

- Key Opportunity: The global PFAS-to-F3 transition represents the most significant market opportunity, as manufacturers achieving ICAO Level B and EN 1568 performance certification for fluorine-free formulations will command premium positioning across the aviation, oil and gas, and military segments through 2033.

| Key Insights | Details |

|---|---|

| Firefighting Foam Market Size (2026E) | US$ 5.4 Billion |

| Market Value Forecast (2033F) | US$ 7.0 Billion |

| Projected Growth CAGR (2026 - 2033) | 3.7% |

| Historical Market Growth (2020 - 2025) | 2.8% |

Market Dynamics

Drivers - Expanding Oil & Gas and Chemical Infrastructure Driving Mandatory Foam Deployment

The oil and gas sector continues to be the most significant demand driver for the Firefighting Foam Market. Ongoing global investments in upstream, midstream, and downstream hydrocarbon infrastructure are directly supporting the steady procurement of firefighting foam systems. Strict regulatory frameworks such as the National Fire Protection Association (NFPA) Standard 11, which governs the use of low-, medium-, and high-expansion foam systems, and NFPA 30 for flammable and combustible liquids require foam-based fire suppression systems at refineries, storage terminals, offshore platforms, and processing plants.

According to the International Energy Agency, global oil and gas investment reached approximately US$ 570 billion in 2024, with a significant portion allocated to new facility development and safety system upgrades. As petrochemical complexes continue expanding across the Middle East, Asia Pacific, and North America, the number of mandatory foam system installations is also rising. This trend is sustaining strong baseline demand for both traditional fluorinated foams and the emerging fluorine-free foam formulations.

Aviation Sector Expansion and ICAO-Mandated Fire Protection Standards

The recovery and expansion of the global aviation industry are creating sustained demand for specialized firefighting foam concentrates. The International Civil Aviation Organization requires all international airports to maintain foam-based fire suppression systems capable of meeting ICAO Level B performance standards. These standards define strict requirements for foam application rates, fire extinguishing time, and resistance to re-ignition during aircraft rescue and firefighting operations. According to the Airports Council International, global passenger traffic exceeded 8.7 billion in 2023 and continues to move toward pre-pandemic levels.

This recovery is driving significant investment in airport infrastructure, runway expansion, and aviation safety systems. Several countries in Asia and the Middle East are actively developing new airports and expanding existing terminals. For example, Saudi Arabia’s large-scale aerotropolis projects are generating new opportunities for firefighting foam suppliers. As aviation infrastructure grows, demand for high-performance foam concentrates certified under ICAO and EN 1568 standards is expected to increase steadily.

Restraints - PFAS Contamination Liability and Legacy AFFF Phase-Out Suppressing Near-Term Revenue

The global regulatory phase-out of PFAS-based firefighting foams, particularly Aqueous Film Forming Foam (AFFF), is creating temporary disruption in the market. Many legacy foam products are being withdrawn before fluorine-free alternatives reach full commercial maturity. A major industry turning point occurred when 3M agreed to a US$ 10.3 billion settlement with U.S. municipalities related to PFAS groundwater contamination. This case highlighted the financial and legal risks associated with PFAS-based firefighting foams for both manufacturers and end users.

The Fire Industry Association reported in its 2025 regulatory update that fluorotelomer-based AFFF containing C8 chemicals was banned across the UK and EU starting July 4, 2025. Furthermore, a complete PFAS foam phase-out is expected between 2030 and 2035. These regulations are reducing sales of traditional foam products while manufacturers continue investing in alternative solutions. As a result, the market is experiencing short-term revenue pressure during this transition phase.

Performance Gaps of Fluorine-Free Foams Limiting Full-Scale Transition

Although environmental regulations strongly encourage the shift toward fluorine-free foams (F3), performance limitations continue to slow large-scale adoption. Several studies highlight the operational differences between fluorine-free formulations and traditional fluorinated foams. Research published in the scientific journal ACS Omega in 2024 found that F3 foams often require 1.5 to 3 times higher application rates compared with C6 AR-AFFF foams to achieve similar fire suppression results, especially for Class B flammable liquid fires.

The National Fire Protection Association has also acknowledged that fluorine-free foams may require modified firefighting strategies and higher application volumes. These operational requirements lead to increased foam consumption per incident, larger storage capacity needs, and potential equipment upgrades. Such additional costs can discourage adoption among budget-constrained end users, including municipal fire departments and smaller industrial facilities in developing economies, thereby slowing the market’s transition toward fluorine-free technologies.

Opportunities - Fluorine-Free Foam (F3) Innovation as a Transformative Replacement Market

The global transition away from PFAS-based firefighting foams toward fluorine-free alternatives represents one of the largest commercial opportunities in the Firefighting Foam Market. The European Union introduced Commission Regulation (EU) 2025/1988, which restricts PFAS-containing foams in portable extinguishers by October 2026 and establishes a broader market ban by October 2030. These deadlines are forcing airports, industrial facilities, military bases, and municipal fire departments worldwide to begin long-term foam replacement programs.

In the United States alone, more than 1,400 fire departments have already started transitioning to fluorine-free foam systems. Responding to this growing demand, Perimeter Solutions introduced its SOLBERG SPARTAN™ 1% Fluorine-Free Class A/B foam concentrate at FDIC International 2025. The product is designed to suppress most fire scenarios without intentionally added PFAS chemicals. Continuous research and development efforts are also helping fluorine-free formulations achieve ICAO Level B certification, which will open the aviation sector, one of the most valuable market segments, for wider adoption.

Wildland and Forest Fire Suppression, An Emerging High-Growth Application Segment

Rising frequency and intensity of wildland and forest fires worldwide are creating a rapidly expanding demand segment for specialized Class A foam and fire-retardant concentrates. According to the National Interagency Fire Center, the United States alone has experienced several years in which 9 to 10 million acres of land burned annually. These large-scale fires have significantly increased procurement of firefighting chemicals by federal and state agencies.

To address this growing demand, Perimeter Solutions opened a new 110,000-square-foot high-technology production facility in June 2025 dedicated to manufacturing PHOS-CHEK aerial fire retardant concentrates. Climate-driven wildfire events are now expanding beyond traditional hotspots and affecting regions such as Southern Europe, Australia, Canada, and Chile. As governments strengthen their wildfire response strategies and increase firefighting stockpiles, demand for advanced fire retardants and Class A foams is expected to grow steadily over the coming years, creating new long-term opportunities in the firefighting foam industry.

Category-wise Analysis

By Foam Type Insights

Aqueous Film Forming Foam (AFFF) currently holds the leading position in the Firefighting Foam Market by foam type, accounting for nearly 35% of the total market share. This dominance is largely due to its long history of use across high-risk environments such as oil and gas refineries, military bases, and international airports. AFFF gained widespread adoption because of its fast film-forming capability, which quickly suppresses flammable liquid fires and prevents re-ignition.

The regulatory and safety standards from organizations such as the National Fire Protection Association (NFPA) and the International Civil Aviation Organization (ICAO) have referenced AFFF performance benchmarks for aircraft rescue and firefighting systems worldwide. However, increasing environmental concerns about PFAS chemicals are changing the market landscape. Regulations such as the EU’s PFAS phase-out mandate and the UK’s ban on certain fluorinated foams are gradually reducing AFFF demand. Despite this transition, AFFF still has the largest installed base globally, while Fluorine-Free Foam (F3) is emerging as the fastest-growing foam category.

By Fire Class Insights

Class B fires dominate the Firefighting Foam Market by fire class, accounting for approximately 62% of the total market share. These fires involve flammable and combustible liquids such as petroleum products, organic solvents, and polar solvents, which require specialized foam suppression systems. The dominance of this segment is closely linked to the fundamental purpose of firefighting foam technology, which was originally developed to control and extinguish liquid fuel fires.

Many major industrial sectors, including oil and gas refineries, fuel storage terminals, chemical plants, aviation facilities, and marine fuel depots, face high exposure to Class B fire risks. The National Fire Protection Association classifies locations such as petroleum storage facilities, aircraft refueling areas, and marine bunkering stations as high-risk environments that require foam-based suppression systems. Because global industrial operations handle large volumes of flammable liquids, the demand for Class B fire protection systems remains consistently strong and is expected to continue driving firefighting foam consumption throughout the forecast period to 2033.

By Application Insights

Flammable liquid fire suppression represents the leading application segment in the Firefighting Foam Market, contributing roughly 40% of the global revenue share. The strong demand in this segment is driven by the essential role of foam systems in controlling fuel-based fires across industries such as petroleum refining, chemical processing, aviation fueling, and marine fuel storage. These sectors manage large quantities of flammable hydrocarbons, making fast and effective foam-based fire suppression critical for operational safety. Industry standards also play a major role in sustaining demand.

The National Fire Protection Association established NFPA 11, which provides detailed guidelines for designing foam systems used in flammable liquid fire scenarios. This standard is widely adopted by regulators across North America, Europe, and major Asia Pacific markets. In addition, the International Maritime Organization requires foam suppression systems on oil tankers, LNG carriers, and chemical vessels under the SOLAS convention, further supporting consistent demand across the marine and shipping sectors.

By End-user Insights

The oil and gas industry remains the largest end-use segment in the Firefighting Foam Market, accounting for approximately 34% of the total global market share. This leadership is primarily due to the sector’s high exposure to severe fire risks and the massive volumes of flammable hydrocarbons handled daily during exploration, refining, storage, and transportation activities. Because of these risks, strict safety regulations require advanced fire protection systems across oil and gas infrastructure.

Standards issued by the National Fire Protection Association, including NFPA 11, NFPA 15, and NFPA 30, mandate foam-based suppression systems in refineries, tank farms, offshore platforms, and liquefied natural gas terminals. According to the International Energy Agency, global upstream oil and gas investment reached around US$570 billion in 2024, with safety systems forming a mandatory part of facility capital expenditure. Regions such as the Middle East, which host some of the world’s largest oil processing facilities, continue to maintain high foam system capacity, supporting the sector’s long-term market leadership.

Regional Insights

North America Firefighting Foam Market Trends

North America represents one of the most important markets for firefighting foam, influenced by its extensive oil and gas infrastructure, strict safety regulations, and rapid transition toward fluorine-free foam technologies. Regulatory changes are playing a key role in reshaping the regional market. The U.S. National Defense Authorization Act requires the U.S. Department of Defense to stop purchasing and using PFAS-based firefighting foams, triggering a large-scale replacement program across military airbases, naval facilities, and defense installations

The United States Environmental Protection Agency has introduced Maximum Contaminant Levels for PFAS chemicals in drinking water, increasing legal and environmental pressure on municipalities and industrial operators to transition to safer foam alternatives. As a result, more than 1,400 U.S. fire departments have already started adopting fluorine-free foams. Companies such as Perimeter Solutions have responded by launching new fluorine-free products and expanding manufacturing capacity, positioning North America as both a major demand center and a key innovation hub for advanced firefighting foam technologies.

Europe Firefighting Foam Market Trends

Europe is leading the global transition toward environmentally safer firefighting foam, supported by some of the world’s most stringent chemical and environmental regulations. The European Union introduced Commission Regulation (EU) 2025/1988 under the REACH framework to restrict PFAS chemicals in firefighting foam products. This regulation establishes strict concentration limits and sets clear phase-out timelines, including a deadline of October 2026 for portable extinguisher foams and a complete market ban scheduled for October 2030.

In the United Kingdom, the Fire Industry Association confirmed that C8-based firefighting foams were banned from July 2025, with broader PFAS restrictions expected in the coming decade. Major European markets such as Germany, the United Kingdom, France, and Spain drive regional demand due to their large industrial and chemical sectors. Companies including ANGUS FIRE and Dafo Fomtec AB are investing heavily in EN-1568-compliant fluorine-free foam technologies, supporting the region’s push toward sustainable and environmentally responsible firefighting solutions.

Asia Pacific Firefighting Foam Market Trends

Asia Pacific represents the fastest-growing regional market for firefighting foam, the region’s strong position is supported by rapid industrialization, expanding petrochemical infrastructure, and significant investments in aviation and energy sectors across countries such as China, India, Japan, and ASEAN nations. China leads the regional market due to its extensive petrochemical complexes, large airport network, and growing domestic manufacturing capacity for foam concentrates.

Companies such as Jiangsu Suolong Fire Science and Technology Co., Ltd. supply cost-competitive firefighting foam products throughout the region. Although PFAS regulations in China are currently less strict than in Europe and North America, increasing environmental awareness and export requirements are encouraging manufacturers to develop fluorine-free alternatives. India is emerging as the fastest-growing market in the region, driven by refinery expansion, rapid airport development under the UDAN Scheme, and strict fire safety regulations for gas infrastructure implemented by the Petroleum and Natural Gas Regulatory Board.

Competitive Landscape

The global Firefighting Foam Market is moderately fragmented, with a mix of multinational safety solution providers, specialized chemical manufacturers, and regional foam producers competing for market share. Major companies such as Perimeter Solutions, Johnson Controls through its Ansul and Chemguard brands, and ANGUS FIRE hold strong global positions due to their broad product portfolios, strong certification capabilities, and continuous investment in fluorine-free foam technologies.

In this market, key competitive advantages include internationally recognized certifications such as NFPA compliance, ICAO Level B performance standards, and EN 1568 approvals. As environmental regulations tighten worldwide, companies are increasingly focusing on PFAS-free formulations that meet evolving safety and sustainability requirements. In addition, new business models are emerging in the industry, including foam-as-a-service contracts, full-service system maintenance agreements, and digital foam testing solutions. These strategies allow companies to compete not only on product performance but also on long-term service reliability and operational support for industrial customers.

Key Market Developments

- In April 2025: Perimeter Solutions introduced the SOLBERG SPARTAN™ 1% Fluorine-Free Class A/B Foam Concentrate at FDIC International 2025. The PFAS-free formulation delivers rapid fire knockdown, reduces flashover risks, and effectively suppresses structural, wildland, vehicle, and fuel fires, covering nearly 99% of fire scenarios.

- In June 2025: Perimeter Solutions opened a 110,000-square-foot advanced fire-retardant manufacturing facility in the United States to produce PHOS-CHEK® aerial fire retardants. The facility significantly expands production capacity and supports large-scale wildfire suppression operations across North America.

- In October 2025: The European Union adopted Commission Regulation (EU) 2025/1988 under the REACH framework, introducing strict PFAS concentration limits in firefighting foams and establishing October 2030 as the final phase-out deadline, accelerating the transition toward fluorine-free foam technologies across Europe.

Companies Covered in Firefighting Foam Market

- BIO EX S.A.S.

- ANGUS FIRE

- National Foam

- Perimeter Solutions

- DIC Corp.

- Johnson Controls International plc

- Dafo Fomtec AB

- Fabrik Chemischer Praparate von Dr. Richard Sthamer GmbH & Co. KG

- Kerr Fire

- SFFECO GLOBAL

- Foamtech Antifire

- Sthamer

- Jiangsu Suolong Fire Science and Technology Co., Ltd.

- Amerex Corporation

- Buckeye Fire Equipment Co.

- KV Fire Chemicals Pvt. Ltd.

- Dr. Sthamer Hamburg GmbH & Co. KG

- Tyco Fire Products

Frequently Asked Questions

The global Firefighting Foam Market is valued at US$ 5.4 Billion in 2026 and is projected to grow to US$ 7.0 Billion by 2033, registering a CAGR of 3.7% during the forecast period from 2026 to 2033, driven by industrial fire safety mandates and regulatory transitions to fluorine-free foam formulations.

Demand is primarily driven by expanding oil and gas infrastructure investment , with global oil and gas capex reaching approximately US$ 570 billion in 2024 per the IEA , combined with ICAO and NFPA-mandated foam suppression requirements at airports and industrial facilities, and the mandatory global transition from PFAS-based AFFF to fluorine-free formulations under EU COMMISSION REGULATION (EU) 2025/1988 and the U.S. NDAA.

Aqueous Film Forming Foam (AFFF) currently leads with approximately 35% market share based on extensive legacy deployment across oil and gas, aviation, and military sectors. However, Fluorine-Free Foam (F3) is the fastest-growing segment, driven by EU and UK PFAS bans, the U.S. Department of Defense's mandatory AFFF phase-out, and more than 1,400 U.S. fire departments actively transitioning their foam inventories.

North America holds a 41% share of the firefighting foam market, driven by the U.S. NDAA's mandate for the phase-out of PFAS foams and the EPA's PFAS maximum contaminant levels. With over 1,400 fire departments transitioning to fluorine-free alternatives, major OEMs are increasing their R&D and manufacturing investments.

The mandatory global phase-out of PFAS-based foams , with the EU's full ban effective by October 2030 and the UK ban already active from July 2025 , represents the most transformative opportunity, as manufacturers developing ICAO Level B and EN 1568-certified fluorine-free formulations will capture premium replacement demand across aviation, military, and oil and gas sectors worth billions in re-procurement expenditure.

Leading players in the global Firefighting Foam Market include Perimeter Solutions, Johnson Controls International plc (operating under the Ansul and Chemguard brands), ANGUS FIRE, National Foam, DIC Corp., Dafo Fomtec AB, BIO EX S.A.S., SFFECO GLOBAL, Kerr Fire, Jiangsu Suolong Fire Science and Technology Co., Ltd., Foamtech Antifire, and Fabrik Chemischer Praparate von Dr. Richard Sthamer GmbH & Co. KG, collectively driving global innovation in fluorine-free and high-performance foam technologies.