- Technology

- Fiber Optic Gyroscope (FOG) Market

Fiber Optic Gyroscope (FOG) Market Size, Share, and Growth Forecast, 2026 - 2033

Fiber Optic Gyroscope (FOG) Market by Product Type (Fiber Optic Gyroscope Sensors (FOGS), Inertial Measurement Units (IMU), Inertial Navigation Systems (INS), Gyrocompass Systems, Attitude & Heading Reference Systems (AHRS)), Technology (Interferometric FOG, Resonant FOG, Integrated/Chip-Scale FOG), End-Use Industry (Aerospace & Defense, Marine & Subsea, Land & Autonomous Vehicles, Industrial & Robotics, Energy & Utilities, Space & Research), and Regional Analysis for 2026 - 2033

Fiber Optic Gyroscope (FOG) Market Share and Trends Analysis

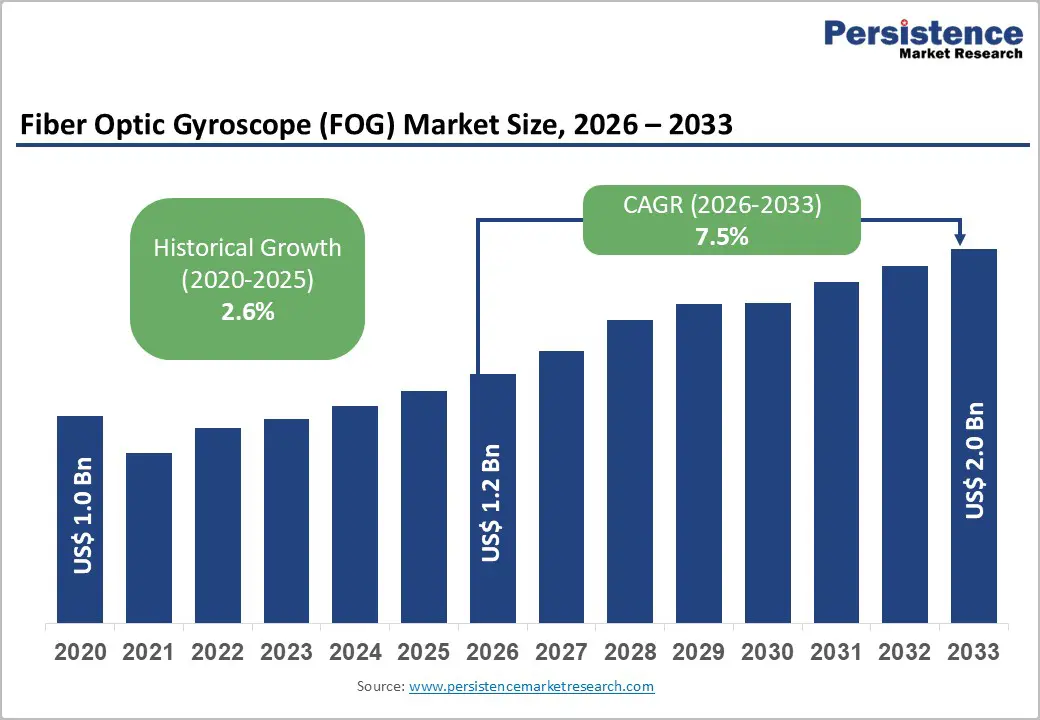

The global fiber optic gyroscope (FOG) market size is likely to be valued at US$ 1.2 billion in 2026, and is estimated to reach US$ 2.0 billion by 2033, growing at a CAGR of 7.5% during the forecast period 2026 - 2033. The expansion of the market is gaining momentum due to the increasing demand for high-precision navigation in defense modernization programs, autonomous systems, and Global Navigation Satellite System (GNSS)-denied operational environments. Defense procurement cycles and aerospace platform integration represent the largest revenue contributors, while emerging adoption in robotics, autonomous mobility, and subsea infrastructure is strengthening the medium-term growth trajectory.

Rising geopolitical tensions are driving investments in inertial navigation redundancy technologies, particularly in North America, Europe, and the Asia Pacific, where governments are prioritizing resilient positioning, navigation, and timing (PNT) systems to reduce dependence on satellite navigation, according to NATO and U.S. Department of Defense (DOD) modernization roadmaps. Simultaneously, technological advancements in photonic integration, miniaturization, and tactical-grade cost optimization are enabling FOG adoption beyond traditional aerospace and naval applications into industrial automation, drilling guidance, and autonomous vehicle platforms.

Key Industry Highlights

- Technology Leadership: Interferometric FOGs are expected to lead with nearly 78% revenue share in 2026, driven by their established adoption across aerospace, naval, and defense navigation systems.

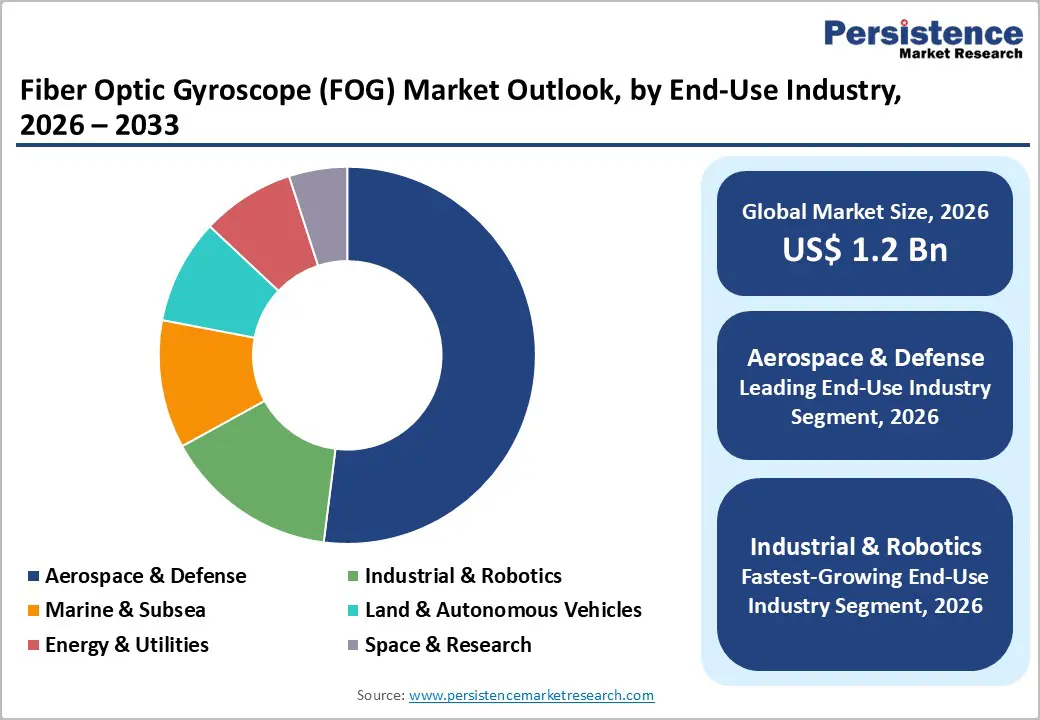

- Leading End-Use Industry: Aerospace and defense applications are anticipated to account for approximately 52% of global revenue in 2026, fueled by the ongoing modernization of military and aviation platforms.

- Fastest-growing End-Use Industry: Industrial and robotics applications are forecast to grow at a CAGR of 10.2% through 2033, driven by increasing demand for reliable navigation in GNSS-denied environments.

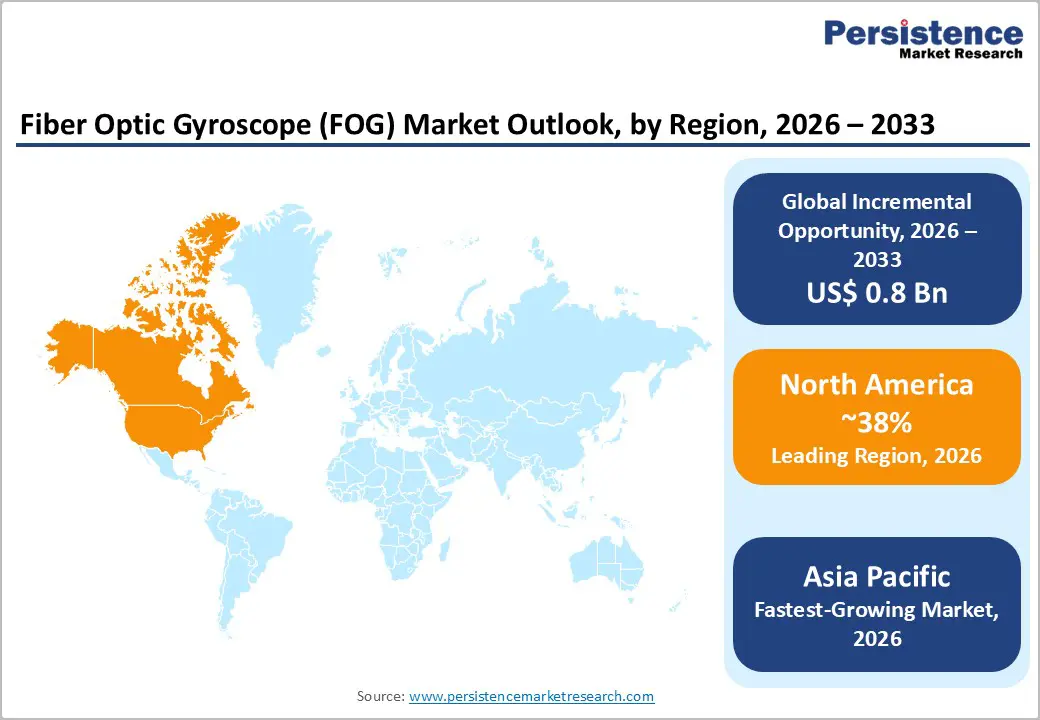

- Regional Leadership: North America is expected to capture nearly 38% market share in 2026, owing to advanced aerospace manufacturing ecosystems and early adoption of autonomous technologies.

- Fastest-growing Market: The Asia Pacific market is projected to exhibit a CAGR of approximately 9.1% from 2026 to 2033, driven by expanding defense expenditures and the surge in industrial automation.

- May 2025: Chinese researchers developed an FOG using hollow optical fibers that is significantly less sensitive to temperature fluctuations, improving navigation stability for platforms such as aircraft, ships, and offshore equipment.

| Key Insights | Details |

|---|---|

| Fiber Optic Gyroscope (FOG) Market Size (2026E) | US$ 1.2 Bn |

| Market Value Forecast (2033F) | US$ 2.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Defense Modernization and Resilient Navigation Investments to Aid Procurement Cycles

Global defense expenditure surpassed US$ 2.4 trillion in 2024 according to the Stockholm International Peace Research Institute (SIPRI), while governments are allocating a larger share of budgets toward resilient navigation, autonomous combat platforms, and unmanned systems. Military agencies are prioritizing inertial navigation technologies that operate independently of GNSS signals, as electronic warfare capabilities such as spoofing and jamming are becoming more sophisticated. Strategic initiatives such as Assured Positioning, Navigation, and Timing (APNT) programs led by the North Atlantic Treaty Organization (NATO) and the United States Department of Defense (DOD) are accelerating procurement of navigation-grade and tactical-grade fiber optic gyroscope-based systems.

This spending trajectory is creating structurally attractive conditions for fiber-optic gyroscope suppliers because defense procurement cycles typically extend over long periods and generate predictable aftermarket revenues through maintenance, upgrades, and replacement requirements. Navigation-grade fiber-optic gyroscope systems are commanding significantly higher prices than industrial sensors, thereby concentrating revenue contribution within defense and aerospace programs. Market participants are also benefiting from platform lifecycle extensions and retrofit programs, which help ensure sustained demand even during periods of slower new-platform production. Strategic alignment with defense primes and system integrators is therefore becoming essential for suppliers that are seeking stable revenue visibility and long-term margin expansion.

Autonomous Systems and Robotics Adoption to Fuel Demand for Tactical-Grade Sensors

Autonomous mobility deployment is expanding across multiple sectors such as unmanned aerial vehicles, industrial robotics, mining automation, and autonomous maritime transport, while governments and industry bodies are promoting automation to improve productivity and operational safety. The International Federation of Robotics (IFR) finds that annual industrial robot installations are exceeding 500,000 units globally, which indicates strong momentum in automation adoption across manufacturing and logistics sectors. At the same time, the International Maritime Organization (IMO) is progressing regulatory frameworks for maritime autonomous surface ships (MASS), encouraging investment in advanced navigation technologies for marine platforms. Autonomous systems require reliable motion sensing in environments where GNSS signals remain unavailable or degraded, including underground tunnels, indoor warehouses, subsea environments, and dense urban areas.

This technology positioning is enabling fiber optic gyroscope adoption to expand into commercial sectors that historically relied on lower-cost sensors, thereby increasing total addressable market volume beyond traditional aerospace and defense applications. As manufacturing scale improves and photonic integration reduces size, weight, and power consumption, suppliers are gaining access to emerging customer segments, such as warehouse automation companies, autonomous logistics providers, and offshore robotics operators. These applications are demanding higher reliability than micro electro mechanical systems (MEMS) can consistently provide, particularly for mission-critical operations involving heavy equipment or remote environments.

High Manufacturing Complexity and Cost Structures to Limit Commercial Penetration

Fiber optic gyroscope production entails highly specialized manufacturing processes that include precision fiber coil winding, polarization-maintaining optical components, electro-optic modulators, and temperature-stabilized packaging architectures. These requirements are creating significantly higher production costs compared with MEMS gyroscopes, which benefit from semiconductor-scale fabrication efficiencies. Industrial-grade fiber optic gyroscope units are typically priced from several hundred to several thousand United States dollars per unit, while navigation-grade systems often reach tens of thousands of dollars, depending on accuracy and environmental specifications. Semiconductor supply chain volatility and limited availability of specialty photonic components continue to constrain production scalability, particularly for manufacturers without vertically integrated fabrication capabilities.

These cost challenges are limiting adoption in price-sensitive sectors such as automotive autonomy and consumer robotics, where system developers are prioritizing cost efficiency alongside acceptable performance. MEMS sensors are steadily improving in accuracy and reliability, which is intensifying competitive pressure on fiber optic gyroscope manufacturers in high-volume applications. Unless photonic integration and manufacturing automation significantly reduce production costs, penetration into mass market mobility platforms may remain restricted during the forecast period. Suppliers are therefore needing to focus on applications that prioritize reliability and precision over cost sensitivity, while simultaneously investing in next-generation integrated photonics technologies to improve long-term competitiveness.

Export Controls and Certification Requirements to Erect New Market Entry Barriers

FOG technologies are frequently subject to export control regulations due to their strategic importance in defense and aerospace applications. Regulatory frameworks such as the International Traffic in Arms Regulations (ITAR) administered by the U.S. State Department and dual use export control regimes governed by the European Union (EU) are increasing compliance costs and administrative complexity for manufacturers. Companies are often required to obtain multiple certifications, licenses, and documentation approvals before exporting navigation-grade systems, which extends sales cycles and increases operational overhead. In addition, aerospace and defense qualification requirements involve rigorous testing, validation, and platform integration processes that can extend beyond two to three years before commercial deployment.

Such a tightening regulatory environment is creating significant barriers to entry and is slowing innovation cycles across the industry. Companies that lack export approvals or government partnerships are facing restricted access to high-growth defense markets in regions such as Asia and the Middle East, where demand for navigation technologies is increasing. Geopolitical tensions are also increasing the likelihood of supply chain fragmentation, particularly when components or technologies are sourced across multiple jurisdictions with competing regulatory frameworks. Investors are therefore feeling the need to evaluate regulatory exposure, export compliance capability, and geopolitical risk when assessing market participation strategies.

Photonic Integration and Chip-Scale FOG to Open Unexplored Avenues

Advances in silicon photonics and integrated optical circuit technologies are enabling the development of miniaturized fiber optic gyroscope systems with smaller size, weight, and power consumption profiles, which are improving suitability for mobile and space-constrained platforms. Research programs supported by institutions such as the European Commission (EC) and the Defense Advanced Research Projects Agency (DARPA) are actively promoting the development of photonic inertial sensors for autonomous navigation applications across the defense and commercial sectors. Chip-scale fiber optic gyroscope architectures are expected to reduce manufacturing costs by approximately 30-50% over the long term through wafer-level fabrication efficiencies and simplified assembly processes, according to photonics industry evaluations.

These cost reductions are expanding feasibility for deployment in applications such as robotics, unmanned aerial systems, and advanced driver assistance systems (ADAS) where traditional fiber optic gyroscopes were previously cost prohibitive. Companies that are investing early in photonic integration, scalable semiconductor manufacturing partnerships, and intellectual property development are likely to achieve competitive advantages through cost leadership and performance differentiation. Forward-thinking collaboration with semiconductor foundries and robotics system integrators will further accelerate commercialization timelines and strengthen market positioning through 2033.

Subsea Infrastructure and Offshore Energy Robotics to Catalyze FOG Market Growth

Offshore wind installations, subsea pipeline networks, and deep-sea exploration activities are expanding globally as governments and energy companies are investing in energy transition infrastructure and maritime energy security initiatives. The International Energy Agency (IEA) reveals rapid growth in offshore wind capacity, particularly across Europe and the Asia Pacific, where countries are accelerating renewable energy deployment to meet decarbonization targets. Subsea robotics platforms that perform inspection, maintenance, and drilling guidance operations require highly precise inertial navigation systems since GNSS signals are unavailable underwater. FOG-based navigation technologies are delivering the accuracy, reliability, and long-term stability necessary for these mission-critical operations, enabling their adoption across offshore energy and marine engineering sectors.

The commercial potential is attractive as subsea equipment operates in high-value environments where reliability is prioritized over cost sensitivity, allowing suppliers to maintain premium pricing structures. Targeting offshore energy developers, marine robotics manufacturers, and subsea service providers is likely to secure long-duration contracts with predictable revenue streams and strong margins. Competitive intensity in these sectors remains lower than in automotive mobility markets, further strengthening the strategic attractiveness of subsea applications for fiber-optic gyroscope manufacturers seeking stable growth opportunities.

Category-wise Analysis

Technology Insights

Interferometric fiber optic gyroscopes are expected to claim around 78% of the FOG market revenue share in 2026, owing to their proven accuracy, long-term stability, and environmental robustness across aerospace, defense, and marine platforms. Closed-loop interferometric architectures are widely used in navigation grade systems due to superior bias stability, low noise characteristics, and broad dynamic range performance. Defense procurement agencies are continuing to prioritize this mature technology because certification pathways are well established and lifecycle reliability has been validated across multiple mission critical deployments. Manufacturers are benefiting from established component supply chains, specialized production expertise, and accumulated operational experience, which are supporting cost efficiency relative to emerging architectures.

Integrated and chip scale FOG technologies are projected to record the fastest growth between 2026 and 2033 as miniaturization and cost reduction initiatives are advancing. Silicon photonics integration is enabling compact sensor designs with lower size, weight, and power requirements, which are improving suitability for robotics, unmanned aerial systems, and autonomous mobility platforms. Research funding from defense agencies and photonics innovation programs is accelerating commercialization readiness and supporting pilot scale manufacturing. Demand is increasing for lightweight and energy efficient navigation sensors in drones and mobile robotic systems where conventional fiber optic gyroscopes were previously impractical due to size and cost constraints.

End-Use Industry Insights

Aerospace and defense applications are expected to dominate, accounting for approximately 52% of the fiber optic gyroscope market's revenue in 2026, driven by high unit pricing, strict performance specifications, and long-term procurement programs. Military aircraft, naval vessels, missile systems, and unmanned platforms continue to rely on navigation-grade inertial navigation technologies for mission-critical operations, where reliability and accuracy are essential. Defense spending increases across NATO, the U.S., China, and India are sustaining procurement demand for advanced inertial systems. Replacement cycles for legacy ring laser gyroscope (RLG) technologies are accelerating the adoption of fiber-optic gyroscope (FOG) solutions, particularly in aviation modernization and platform upgrade initiatives.

Industrial automation and robotics are set to exhibit an estimated CAGR of 10.2% during the 2026-2033 forecast period, helped by increasing investment in autonomous operations and intelligent logistics systems across industries. Warehousing, mining, construction, and manufacturing environments require reliable navigation technologies that function effectively in Global Positioning System (GPS) denied indoor or underground conditions. Tactical-grade fiber optic gyroscope sensors are providing improved accuracy and robustness compared with MEMS alternatives, particularly for high-value robotic platforms operating in complex environments. Labor shortages, productivity optimization initiatives, and automation investments across Asia Pacific manufacturing economies are further accelerating demand.

Regional Insights

North America Fiber Optic Gyroscope (FOG) Market Trends

North America is anticipated to hold approximately 38% of the fiber optic gyroscope market share in 2026. The U.S. is the largest contributor, boosted by heavy investments in modernization programs that emphasize resilient navigation, autonomous defense platforms, and next-generation inertial systems by the DOD. The region is home to a highly developed aerospace manufacturing ecosystem that includes major aircraft producers, defense contractors, and specialized inertial navigation suppliers, which is strengthening supply chain integration and technological collaboration. Concentration of research institutions and photonics innovation programs is also supporting advancements in miniaturization and high performance navigation technologies across commercial and defense sectors.

Regulatory frameworks such as the ITAR are influencing competitive dynamics by restricting foreign supplier participation in sensitive defense programs while simultaneously increasing compliance requirements for domestic manufacturers. These regulations are creating entry barriers but are also protecting established suppliers with certification credentials and government partnerships. Investment activity across North America is increasingly focusing on silicon photonics integration, autonomous navigation technologies, and resilient positioning, navigation, and timing (PNT) solutions to reduce reliance on GNSS signals. Canada is generating additional demand through aerospace component manufacturing, marine navigation systems, and offshore resource applications.

Europe Fiber Optic Gyroscope (FOG) Market Trends

Europe is a critical market for fiber optic gyroscopes as defense modernization initiatives, offshore energy investments, and photonics innovation programs continue to advance across the region. France, Germany, and the U.K. are increasing procurement of advanced inertial navigation technologies for naval vessels, military aircraft, and missile systems, which is strengthening demand for high-precision fiber optic gyroscopes. Regional aerospace manufacturers and defense contractors are integrating next-generation navigation systems into modernization programs, while research institutions are supporting technological development through collaborative innovation projects. EU funding for photonics and autonomous systems research is accelerating the commercialization of integrated optical technologies and enabling suppliers to enhance product performance and miniaturization capabilities.

Offshore wind expansion across the North Sea and surrounding maritime regions is further increasing demand for subsea navigation systems used in installation, inspection, and maintenance operations. Fiber optic gyroscope technologies are providing reliable positioning in underwater environments where GNSS is unavailable, supporting adoption across offshore infrastructure projects. The regional regulatory environment is emphasizing dual use export controls, technological sovereignty, and supply chain resilience, which is shaping procurement strategies and encouraging localized production capabilities. European governments are also promoting domestic manufacturing and strategic autonomy initiatives to reduce reliance on external suppliers, creating opportunities for regional companies to strengthen market share.

Asia Pacific Fiber Optic Gyroscope (FOG) Market Trends

The Asia Pacific FOG market is anticipated to record the highest 2026-2033 CAGR of about 9.1%. China, Japan, South Korea, and India are strategically ramping up investment in aerospace manufacturing, naval fleet expansion, and unmanned systems development, which is strengthening demand for advanced inertial navigation technologies. Governments across the region are promoting domestic semiconductor and photonics manufacturing through industrial policies and incentive programs, which is improving local supply chain capabilities and reducing dependency on imports. The growing presence of robotics manufacturing hubs and electronics production ecosystems is also supporting the adoption of tactical-grade navigation sensors across industrial and commercial applications.

Rapid infrastructure expansion, urban development, and transportation modernization are increasing demand for surveying, mapping, and guidance systems that rely on high-precision motion-sensing technologies. Autonomous mobility initiatives such as intelligent transportation systems, logistics automation, and drone deployment are further contributing to regional market growth as reliable navigation remains critical in environments where GNSS and GPS signals may be unreliable. Offshore energy investments, including offshore wind and subsea resource exploration, are also expanding demand for marine and underwater navigation solutions.

Competitive Landscape

The global fiber optic gyroscope market structure exhibits moderate consolidation, with a combination of large defense contractors and specialized inertial navigation technology providers controlling nearly 60% of global revenues. Companies that maintain vertically integrated manufacturing capabilities and possess defense certifications are securing competitive advantages because regulatory compliance requirements and qualification barriers remain high. Market positioning is primarily being determined by performance grade specialization, geographic presence, and the ability to integrate sensors into complete navigation systems such as inertial navigation systems (INS) and inertial measurement units (IMU). Established suppliers are leveraging long term relationships with aerospace manufacturers and defense agencies to maintain stable procurement pipelines, while high switching costs and certification timelines are reinforcing customer retention.

Competitive intensity is increasingly shifting toward tactical grade and miniaturized fiber optic gyroscope technologies. Partnerships between photonics technology firms and defense contractors are emerging to accelerate innovation in integrated optical architectures and next generation navigation solutions. Smaller niche companies are targeting industrial automation, robotics, and autonomous mobility applications by offering customized products and flexible integration support, which is allowing them to compete effectively outside traditional defense markets. As commercialization expands into new sectors, companies that balance technological innovation with scalable manufacturing and strategic collaborations are expected to strengthen competitive positioning through the forecast period.

Key Industry Developments

- In February 2026, MostaTech showcased its portfolio of FOG-based inertial sensors at Oceanology International 2026, highlighting low size, weight, and power solutions designed for subsea and autonomous applications such as unmanned vehicles and robotics. The lineup included compact inertial measurement units integrating fiber optic gyroscopes with MEMS accelerometers to deliver high stability and low noise performance for precision navigation and motion control.

- In October 2025, Paras Defence & Space Technologies signed a Memorandum of Understanding (MoU) with Israel-based Cielo Inertial Solutions to jointly develop and produce inertial sensors and closed-loop fiber optic gyroscope systems in India. The collaboration aims to strengthen local manufacturing, technology transfer, and commercialization of advanced navigation solutions for defense and aerospace applications.

- In August 2025, Advanced Navigation demonstrated its Hybrid Navigation System in the Pyhäsalmi Mine in Finland, showcasing high-precision positioning in deep underground environments where GNSS signals are unavailable. The system combines a Boreas D90 FOG inertial navigation system with a Laser Velocity Sensor to deliver sub-meter accuracy without relying on maps, beacons, or external infrastructure.

Companies Covered in Fiber Optic Gyroscope (FOG) Market

- Honeywell International Inc.

- Northrop Grumman Corporation

- Safran S.A.

- RTX Corporation (Collins Aerospace)

- KVH Industries, Inc.

- EMCORE Corporation

- iXblue SAS (Exail Technologies)

- Analog Devices, Inc.

- Thales Group

- L3Harris Technologies, Inc.

- Bosch Sensortec GmbH

- Fizoptika Corp.

- Advanced Navigation Pty Ltd

- Trimble Inc.

- VectorNav Technologies, LLC

Frequently Asked Questions

The global fiber optic gyroscope (FOG) market is projected to reach US$ 1.2 billion in 2026.

Growing need for high-precision navigation in defense modernization programs, autonomous systems, and GNSS-denied operational environments is driving the market.

The market is poised to witness a CAGR of 7.5% from 2026 to 2033.

Emerging FOG applications in robotics, autonomous mobility, and subsea infrastructure, rising geopolitical tensions that are driving investments in inertial navigation redundancy technologies, and technological advancements in photonic integration, miniaturization, and tactical-grade cost optimization are key market opportunities.

Honeywell International Inc., Northrop Grumman Corporation, Safran S.A., and RTX Corporation (Collins Aerospace) are some of the key players in the market.