- Pharmaceuticals

- Ferritin Testing Market

Ferritin Testing Market Size, Share, and Growth Forecast 2026 – 2033

Ferritin Testing Market by Product Type (Instrument, Reagent, Kits), Specimen Type (Serum/Plasma, Whole Blood), Application (Anemia, Hemochromatosis, Lead Poisoning, Pregnancy), and Regional Analysis, 2026 – 2033

Ferritin Testing Market Size and Trends Analysis

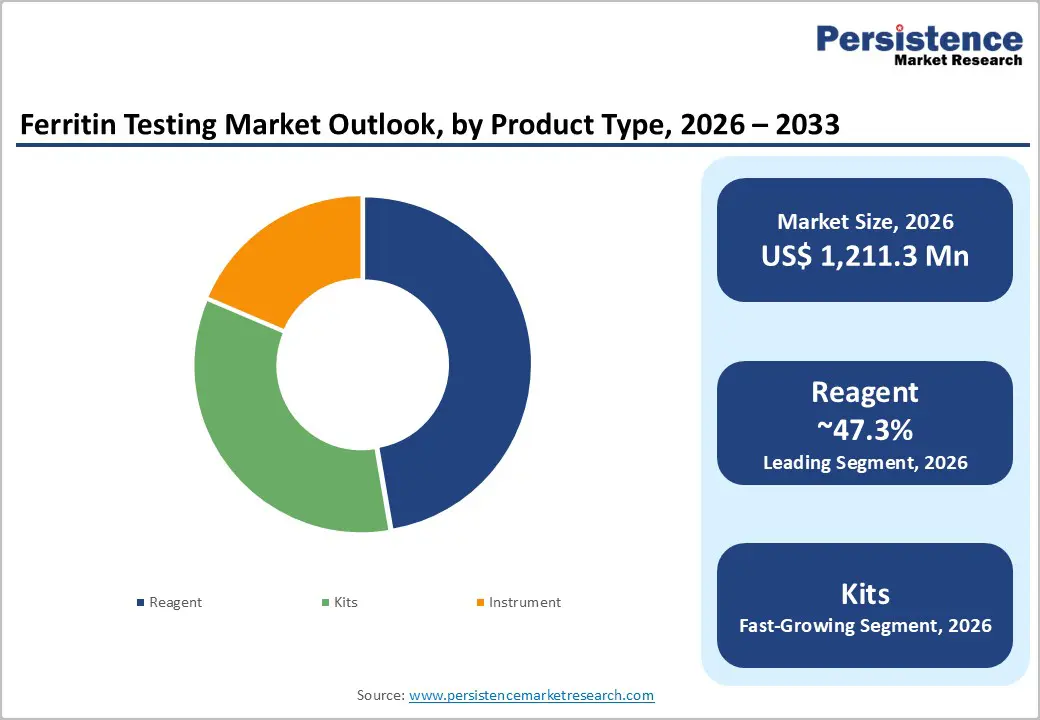

The global ferritin testing market size is likely to be valued at US$1,211.3 million in 2026 and is expected to reach US$1,996.5 million by 2033, growing at a CAGR of 7.4% during the forecast period from 2026 to 2033, driven by the rising global burden of iron deficiency and anemia, especially among women and children.

Growth is further fueled by increasing adoption of automated immunoassay platforms in hospitals and diagnostic laboratories.

Key Industry Highlights:

- Leading Product Type: Reagents, approximately 47.3% share in 2026, as they are consumables required for every test, creating continuous and recurring demand.

- Dominant Application: Anemia, nearly 45.8% share in 2026, as ferritin is the most reliable early marker of iron deficiency, which is the leading cause of anemia globally.

- Latest Study: In October 2025, researchers from the University of Pittsburgh and the University of Pennsylvania published findings in JAMA Internal Medicine examining the impact of revised ferritin thresholds on iron deficiency anemia diagnosis. The study demonstrated that high ferritin cut-offs could identify substantially more patients with iron deficiency, supporting broad adoption of updated diagnostic criteria.

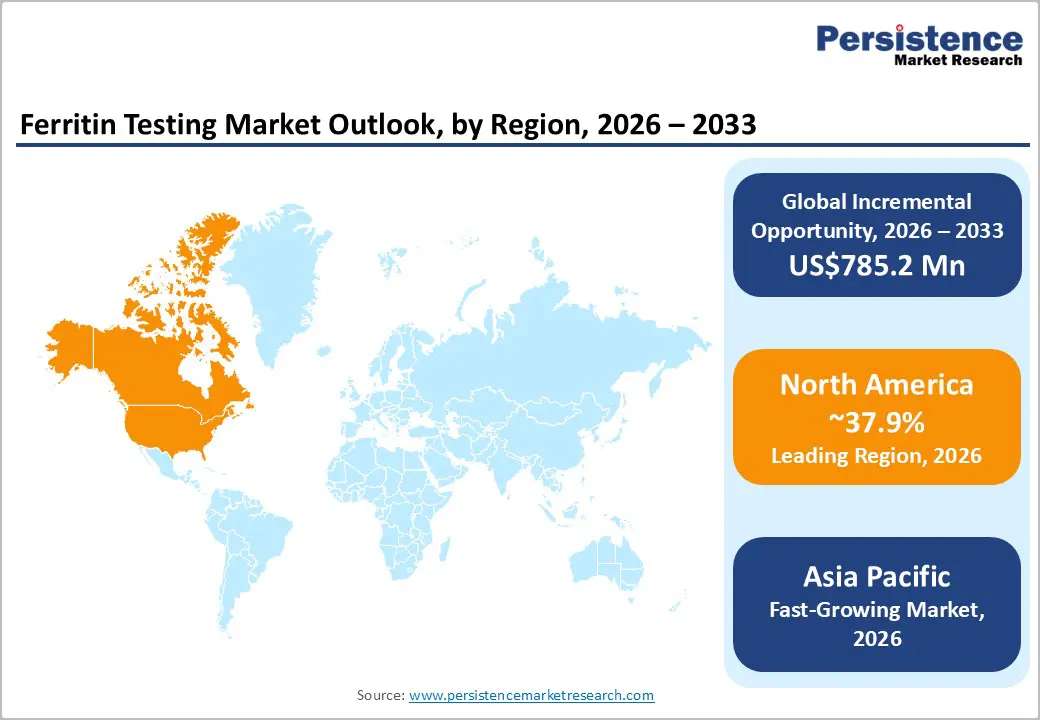

- Leading Region: North America, with about a 37.9% share in 2026, fostered by a well-established diagnostic infrastructure and high testing frequency in chronic diseases.

- Fast-growing Region: Asia Pacific, owing to high anemia burden and expanding healthcare access.

DRO Analysis

Driver - Surging CKD-Related Anemia to Fuel Demand for Iron Monitoring

Anemia is one of the most consistent complications of Chronic Kidney Disease (CKD). As kidney function declines, iron stores become difficult to interpret due to hepcidin-mediated iron trapping. It is a mechanism that makes ferritin testing indispensable rather than optional. The KDIGO 2026 Clinical Practice Guideline for Anemia in CKD, published in Kidney International, now mandates ferritin as part of the standard diagnostic panel at every stage of CKD monitoring.

Testing intervals are recommended at least annually for CKD G3, twice yearly for G4, and every three months for G5 and G5D patients. New therapies such as HIF-PHI stabilizers and ferric carboxymaltose also require ongoing ferritin surveillance to avoid iron overload. The KDIGO 2024 guideline specifies that monthly ferritin and TSAT testing is reasonable for CKD G5HD patients receiving iron therapy to guide decisions and maintain safe anemia control. This structured and protocol-driven testing cadence is translating into sustained, repeated demand for ferritin diagnostics across nephrology care.

Rising Government Support for Anemia Screening in Pregnant Women

Iron deficiency during pregnancy carries real risks for both mother and child, and international bodies are increasingly formalizing ferritin's role in prenatal care. The 2023 FIGO guidelines recommend screening all women for iron deficiency starting from menarche, regardless of anemia, including before planned pregnancies and at the end of the second trimester. The 2024 European Hematology Association also emphasizes identifying pre-conceptual iron deficiency and normalizing iron stores before conception.

On the diagnostic side, a ferritin level below 30 μg/dL carries a 92% sensitivity and 98% specificity for diagnosing iron deficiency. Maternal ferritin below 13.4 μg/dL has been shown to compromise fetal iron stores. These thresholds are giving governments and health systems a concrete basis for protocol-based prenatal screening. It is further making ferritin a frontline tool rather than a secondary add-on in maternal health programs.

Restraint - Competition from Transferrin Saturation Tests

Ferritin's limitation as an acute-phase reactant, meaning it rises during inflammation regardless of iron status, has long been known. But recent research is actively shifting clinical preference toward transferrin saturation (TSAT) in high-burden conditions. A 2025 study published in JACC: Heart Failure examining 372 patients with HFpEF found that higher peak oxygen consumption was associated with higher TSAT, TSAT/hepcidin ratio, and serum iron. But it was not associated with ferritin level, a finding that challenges ferritin's utility in functional assessment.

A separate analysis published in Circulation: Heart Failure in 2025, drawing from 2,050 heart failure patients in the Penn HF Study, found that ferritin concentrations were not associated with outcomes. However, low TSAT and serum iron were associated with the risk of all-cause death. As cardiology guidelines now recognize TSAT as the more reliable prognostic marker in inflammatory or fluid-overloaded states, some clinical workflows may deprioritize standalone ferritin testing, particularly in heart failure management.

Opportunity - Use of Ferritin as a Biomarker in Inflammation Research

Ferritin's role is evolving well beyond iron storage. In inflammatory and autoimmune diseases, extreme hyperferritinemia has become a diagnostically significant signal. A 2025 retrospective study published in Diagnostics (MDPI) on 113 patients with Adult-Onset Still's Disease (AOSD) at Chonnam National University Hospital found that ferritin levels exceeding 3,000 to 5,000 ng/mL are often reported in AOSD. Extreme hyperferritinemia above 10,000 ng/mL is highly suggestive of the condition in the appropriate clinical context.

The study explored whether ferritin levels could predict the need for advanced therapy escalation, including tocilizumab and anakinra, positioning ferritin as a prognostic tool alongside its diagnostic role. In pediatric critical care, the HiHASC 2023 diagnostic framework introduced a '3-F' mnemonic, namely, fever, falling blood counts, and ferritin, as a sepsis-adapted prompt for identifying macrophage activation syndrome in pediatric septic shock. As ferritin is embedded into more disease-specific protocols and trial endpoints, demand for standardized and reproducible ferritin testing methods is likely to surge across rheumatology, critical care, and oncology research settings.

Expansion of Rapid Ferritin Diagnostics in Underserved Markets

Hemoglobin testing has historically dominated anemia screening in low-resource settings due to cost and accessibility. But hemoglobin alone cannot confirm iron deficiency. This only signals its presence after significant depletion. Point-of-care ferritin devices are beginning to address this diagnostic gap. Research published in Blood (2025) by investigators from the American Society of Hematology evaluated the Gazelle platform, a battery-powered, low-cost device priced at approximately US$500, as a fingerstick-based ferritin assay. The findings support further deployment and clinical validation of the Gazelle platform to address global gaps in anemia diagnosis and iron deficiency management.

The authors also flagged its potential in high-resource settings where general pediatricians and obstetricians still rely on hemoglobin alone. There is a recognized role for such tools in high-resource settings as a screening option for general pediatricians and obstetricians who are still using hemoglobin as the primary screening tool for iron deficiency. As validation continues across sub-Saharan Africa and South Asia, these devices represent a significant untapped deployment opportunity.

Category-wise Analysis

Product Type Insights

Reagents are predicted to lead with a share of approximately 47.3% in 2026, as they are consumables that must be purchased repeatedly, unlike analyzers that are installed once and used for years. Every ferritin test performed in a laboratory requires reagent consumption. This creates continuous demand from hospitals, diagnostic laboratories, blood banks, and public health screening programs. As testing volumes increase, reagent sales rise automatically. This recurring revenue model makes reagents the most important product category in the market. Surging use of fully automated immunoassay systems is also predicted to fuel the segment.

Kits are estimated to be the fastest-growing segment over the forecast period, as healthcare providers now prefer ready-to-use solutions instead of sourcing reagents, calibrators, controls, and accessories separately. Kits simplify procurement and reduce laboratory preparation time. This is especially valuable for small and medium-sized laboratories that may lack advanced technical staff. Another important factor is the expansion of ferritin testing into decentralized settings such as outpatient clinics, physician offices, and regional diagnostic centers. These facilities often require compact testing solutions that can be implemented quickly. Complete kits allow facilities to begin testing with minimal setup requirements.

Application Insights

The anemia segment is anticipated to dominate with a share of nearly 45.8% in 2026, as ferritin is considered one of the earliest and most reliable indicators of iron deficiency, which is the leading cause of anemia worldwide. Ferritin levels decline before hemoglobin levels fall significantly. This allows physicians to detect iron deficiency at an early stage and intervene before severe anemia develops. The World Health Organization (WHO) specifically recognizes ferritin as a key marker for assessing iron stores and diagnosing iron deficiency. In population-level health programs, ferritin testing is frequently performed alongside hemoglobin testing to evaluate the prevalence of anemia and guide treatment strategies.

The pregnancy segment is expected to remain in the second position in 2026, as iron requirements increase substantially during gestation. Iron is needed not only for the mother's expanding blood volume but also for fetal growth and placental development. Hence, pregnant women are among the populations most vulnerable to iron deficiency. The WHO highlights pregnancy as a critical period for ferritin assessment and iron monitoring. Healthcare providers are recognizing that hemoglobin testing alone may fail to identify early iron depletion during pregnancy. Ferritin testing can detect declining iron stores before anemia becomes clinically evident.

Regional Insights

North America Ferritin Testing Market Trends

North America is predicted to dominate in 2026 with a share of approximately 37.9%, owing to its well-established diagnostic infrastructure and early adoption of advanced immunoassay systems. Large hospital networks and reference labs widely use automated platforms from companies such as Roche and Abbott. This allows high-volume ferritin testing with fast turnaround times. The region also benefits from strict clinical guidelines. For example, the Centers for Disease Control and Prevention (CDC) recommends iron status assessment in high-risk groups, which supports routine ferritin testing.

U.S. Ferritin Testing Market Trends

A share of nearly 63.6% is expected to be held by the U.S. in 2026, owing to rising screening programs and preventive healthcare trends. Ferritin testing is now commonly included in routine blood panels, especially for women, athletes, and elderly patients. The National Institutes of Health has emphasized early detection of iron deficiency, even before anemia develops. Another driver is the expansion of outpatient and retail clinics. Chains such as CVS MinuteClinic and Walgreens clinics are increasing access to basic blood testing. This decentralization is pushing ferritin testing beyond hospitals.

Asia Pacific Ferritin Testing Market Trends

Asia Pacific is anticipated to be the fastest-growing region in 2026, with a share of nearly 31.5%, backed by the high burden of iron deficiency and improving healthcare access. The WHO reports that a large share of the global anemia population lives in this region, especially among women and children. This creates steady demand for ferritin-based diagnosis. Governments are also broadening national screening programs. India and China are investing in maternal and child health initiatives.

China Ferritin Testing Market Trends

China will likely lead in Asia Pacific in 2026 with a share of around 37.5%, spurred by large-scale hospital expansion and superior domestic diagnostics manufacturing. The government has increased investment in laboratory infrastructure under its healthcare reform plans. Tertiary hospitals now routinely include ferritin in iron metabolism panels. Another driver is the local production of low-cost testing solutions. Local companies such as Mindray and Autobio have developed cost-effective immunoassay systems, which have improved affordability and increased test volumes.

India Ferritin Testing Market Trends

In 2026, India is projected to account for a share of approximately 23.3%, boosted by high anemia prevalence and government-led programs. According to the Ministry of Health and Family Welfare, more than half of women of reproductive age are affected by anemia. Programs such as Anemia Mukt Bharat are pushing for better diagnostic practices, including iron status assessment. Another driver is the rise of private diagnostic chains such as Dr. Lal PathLabs and Metropolis. These labs are extending into Tier-2 and Tier-3 cities. They are providing ferritin tests as part of routine health packages.

Europe Ferritin Testing Market Trends

Europe will likely see decent growth over the forecast period, with a share of nearly 16.3% in 2026, backed by well-established clinical guidelines and stable healthcare systems. Organizations such as the European Medicines Agency and regional health authorities promote standardized diagnostic practices. Ferritin testing is commonly used in anemia, oncology, and chronic disease management. The region also benefits from aging populations. Older adults are more prone to iron deficiency and chronic diseases, which require regular monitoring.

Germany Ferritin Testing Market Trends

Germany will likely register a substantial share of approximately 32.6% in 2026, fostered by its advanced laboratory network and favorable reimbursement policies. The country has a high number of accredited diagnostic labs that follow strict quality standards. Ferritin testing is routinely included in preventive health checkups. Research activity is also high. Local clinical studies have explored ferritin as a marker in inflammation and metabolic disorders. This has expanded its use beyond anemia.

U.K. Ferritin Testing Market Trends

A share of around 24.8% is predicted to be held by the U.K. in 2026, owing to structured screening programs and National Health Service (NHS)-backed testing protocols. NHS includes ferritin testing in guidelines for anemia diagnosis and management. Demand is also rising due to increased focus on women’s health and pregnancy care. Ferritin testing is being used more frequently to detect early iron deficiency in prenatal care. Post-pandemic healthcare reforms are further pushing for quick diagnostics and reduced hospital burden, which may increase ferritin testing in community and outpatient settings.

Competitive Landscape

The global ferritin testing market is moderately consolidated with a small group of multinational diagnostics companies controlling a large share of testing platforms, reagents, and laboratory relationships. Competition is dominated by key diagnostics companies such as Roche Diagnostics, Abbott Laboratories, Siemens Healthineers, Thermo Fisher Scientific, Beckman Coulter, and DiaSorin. These firms compete primarily through automated immunoassay platforms that can process ferritin alongside hundreds of other biomarkers on a single instrument.

Another key battleground is point-of-care and rapid ferritin testing. Traditional laboratory testing remains dominant, but companies are investing in decentralized testing solutions for emergency departments, outpatient clinics, and resource-limited settings. Small-scale companies such as CTK Biotech, Pointe Scientific, Abnova, and Getein Biotech compete by providing cost-effective kits, specialized assays, and regional distribution networks.

Key Industry Developments:

- In May 2026, researchers from Amsterdam UMC and NHS Blood and Transplant reported the successful deployment of a federated machine-learning framework for iron deficiency prediction using routine blood test data. The system was developed to improve the identification of patients requiring ferritin testing while maintaining data privacy across healthcare institutions.

- In November 2025, researchers presented an evaluation of a rapid, low-cost point-of-care ferritin assay at the American Society of Hematology (ASH) Annual Meeting. The study assessed the feasibility of using portable ferritin testing for iron deficiency detection in low-resource settings, aiming to extend access beyond traditional laboratory environments.

- In January 2025, researchers from Sanquin Research and Amsterdam UMC reported results from the FORTE randomized controlled trial on ferritin-guided iron supplementation in blood donors. The study showed that ferritin-based monitoring and targeted iron supplementation significantly reduced iron deficiency among regular blood donors, supporting the wide use of ferritin testing in donor management programs.

Companies Covered in Ferritin Testing Market

- EUROLyser Diagnostica GmbH

- Cortez Diagnostics Inc.

- Pointe Scientific, Inc.

- bioMérieux

- Humankind Ventures Ltd.

- Aviva Systems Biology Corporation

- Abnova Corporation

- Cosmic Scientific Technologies

- CTK Biotech, Inc.

- Thermo Fisher Scientific Inc.

Frequently Asked Questions

The global ferritin testing market is projected to be valued at US$1,211.3 million in 2026.

The ferritin testing market is expected to reach US$1,996.5 million by 2033.

Key market trends include the rising adoption of automated platforms and surging use of ferritin in preventive health screening.

Reagents are expected to be the leading product type with a share of nearly 47.3% in 2026, as they are closely tied to specific analyzers, leading to long-term supplier dependency and repeat purchases.

The ferritin testing market is expected to grow at a CAGR of 7.4% from 2026 to 2033.

EUROLyser Diagnostica GmbH, Cortez Diagnostics Inc., and Pointe Scientific, Inc. are a few key market players.