- Non-food Packaging

- Eyeliner and Kajal Sculpting Pencil Packaging Market

Eyeliner and Kajal Sculpting Pencil Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Eyeliner and Kajal Sculpting Pencil Packaging Market by Product Type (Recyclable Pencil Packaging, Refillable Systems, Others), End-user (Cosmetics Brands, Luxury Market, Others), Material, and Regional Analysis for 2026 - 2033

Eyeliner and Kajal Sculpting Pencil Packaging Market Size and Trends Analysis

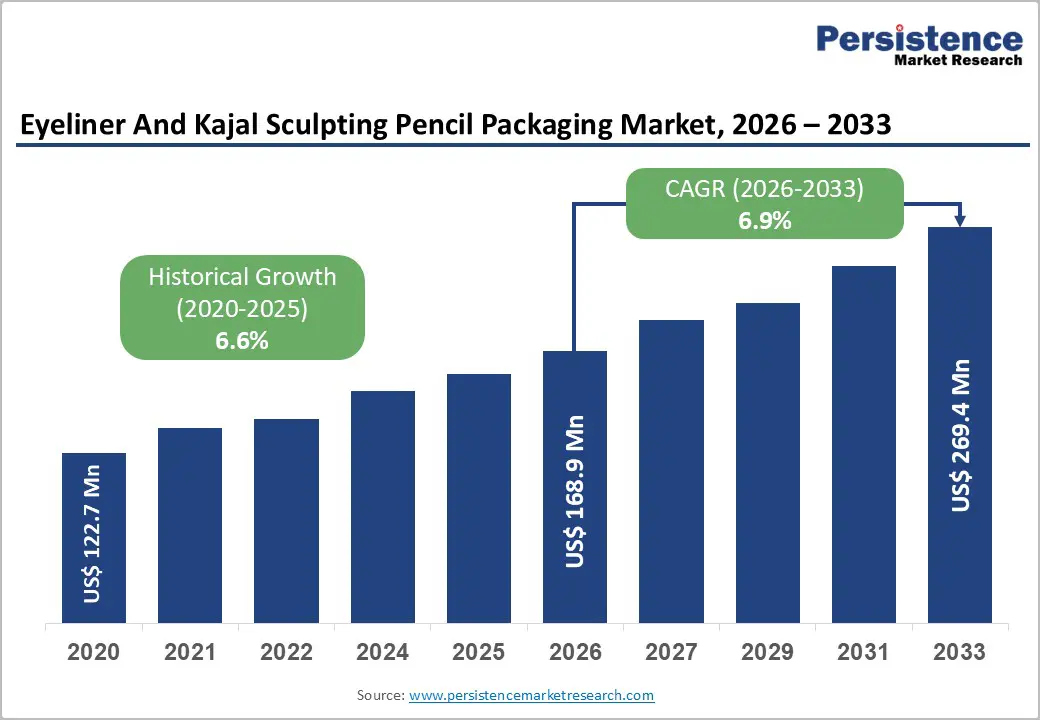

The global eyeliner and kajal sculpting pencil packaging market size is likely to be valued at US$168.9 million in 2026 and is expected to reach US$269.4 million by 2033, growing at a CAGR of 6.9% between 2026 and 2033, driven by rising demand for sustainable and refillable cosmetic packaging, continued premiumization within eye-makeup categories, and strong adoption by cosmetics brands prioritizing circular economy alignment and shelf differentiation.

Structural shifts in regional manufacturing toward Asia Pacific, combined with increasing regulatory pressure on single-use plastics, are accelerating the transition toward PCR, mono-material, and refillable pencil packaging systems. This analysis follows a data-integrity-first approach and links market dynamics directly to actionable investment and sourcing strategies.

Key Industry Highlights

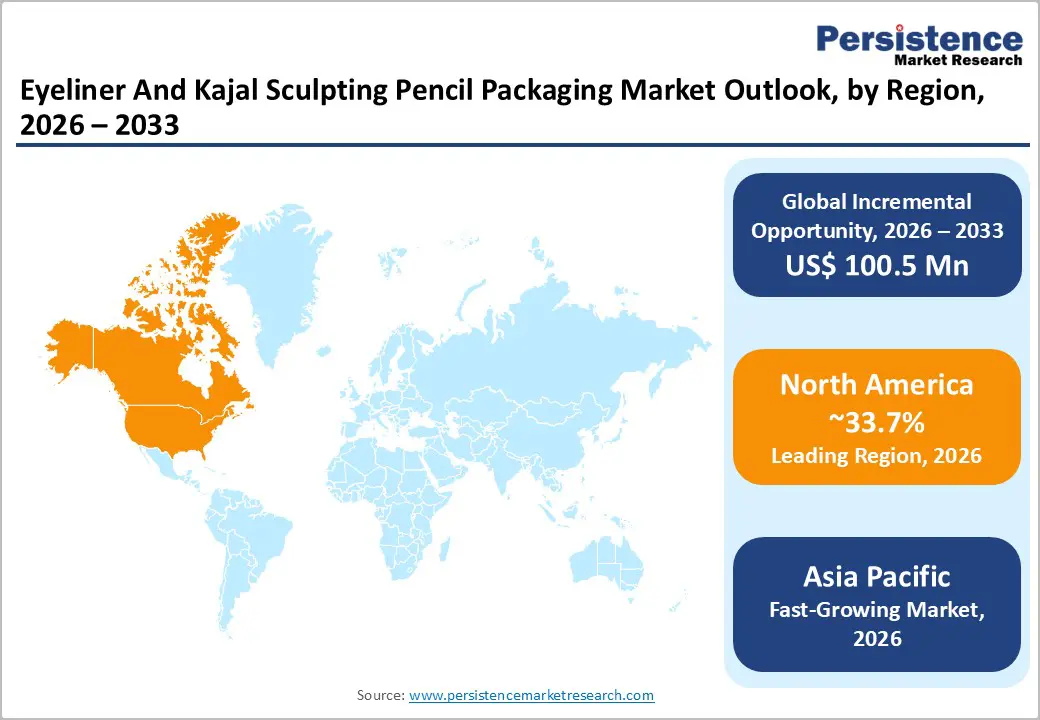

- Leading Region: North America, holding an estimated 33.7% share of the market, driven by strong prestige beauty demand, concentration of multinational cosmetics brands, and advanced retail and DTC ecosystems.

- Fastest-growing Region: Asia Pacific, recording the highest growth rate globally, supported by rapid cosmetics consumption growth, expanding middle-class populations, and its role as a dominant manufacturing and sourcing base for global beauty brands.

- Investment Plans: Industry investment is concentrated in refill-compatible pencil systems, high-precision decoration technologies, and PCR material integration, with capital allocation increasingly linked to compliance with recyclability and circular packaging targets across North America and Europe.

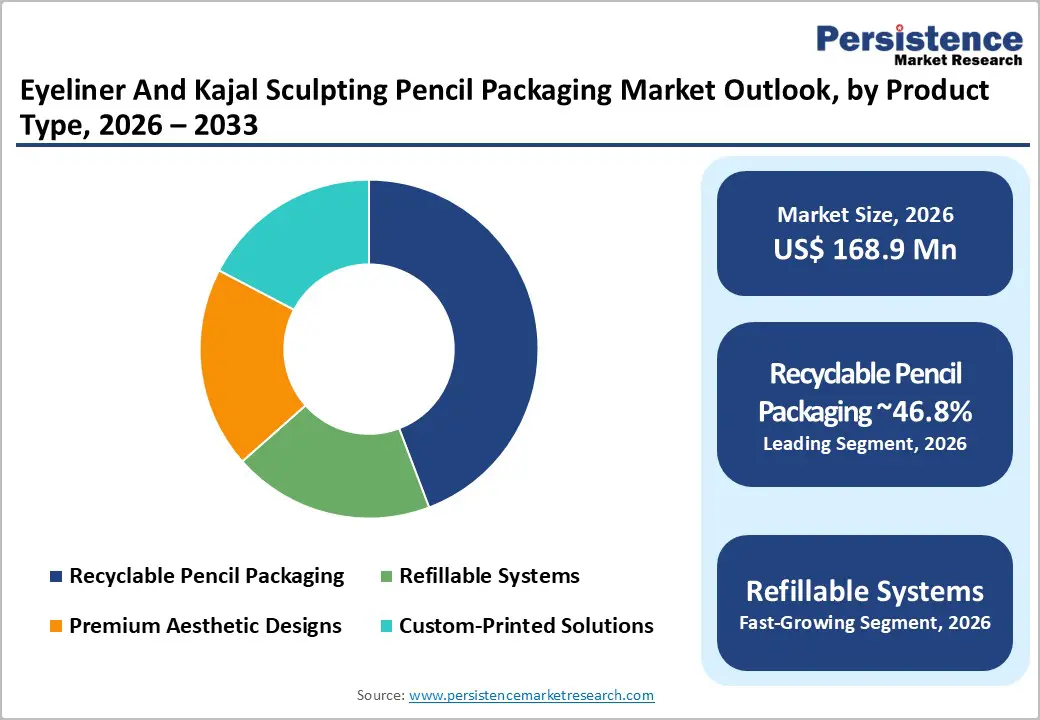

- Dominant Product Type: Recyclable pencil packaging, accounting for 46.8% market share, supported by broad brand acceptance, cost parity with conventional formats, and strong retailer endorsement of recyclable mono-material designs.

- Leading End-user: Cosmetics brands, representing 57.5% market share, reflecting their control over product innovation pipelines, global SKU strategies, and sustainability-led packaging transitions across eyeliner and kajal product lines.

| Key Insights | Details |

|---|---|

| Eyeliner and Kajal Sculpting Pencil Packaging Market Size (2026E) | US$168.9 Mn |

| Market Value Forecast (2033F) | US$269.4 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Sustainability Mandates and Brand Commitments (Consumer and Regulatory Pressure)

Global beauty brands are accelerating commitments to reusable, recyclable, and post-consumer recycled (PCR) packaging formats as part of broader environmental, social, and governance strategies. These commitments are reshaping procurement priorities across eyeliner and kajal categories, prompting suppliers to commercialize mono-material and refillable pencil systems that align with recyclability and waste-reduction targets. From a cost perspective, higher recycled content can lower long-term raw material exposure, while sustainability claims strengthen brand loyalty among environmentally conscious consumers. For packaging suppliers, certified recyclability and PCR validation increasingly command procurement premiums and long-term contracts. Collectively, these shifts reflect a structural transition toward circular packaging models rather than short-term compliance initiatives.

Premiumization and Differentiation In Eye-Makeup Categories

Cosmetics brands are increasingly investing in premium eyeliner and kajal formats to enhance margins and brand positioning. Packaging plays a central role in this strategy through the use of metallic finishes, custom printing, decorated wooden housings, and refined mechanical systems. Innovations such as precision sharpening, retractable mechanisms, and enhanced tactile finishes improve usability and support premium price points. As brands trade up, demand is rising for advanced decorative techniques, including hot-stamping and soft-touch coatings, particularly when combined with sustainable materials. Packaging vendors that can integrate aesthetic sophistication with recyclability requirements are best positioned to capture value in this segment.

Manufacturing and Supply-Chain Consolidation toward Integrated Suppliers

Leading packaging manufacturers are expanding vertically integrated capabilities across material processing, decoration, tooling, and refill system development. Co-locating production near major cosmetics hubs reduces lead times, lowers logistics emissions, and improves responsiveness to rapid product launch cycles. For brand owners, working with integrated suppliers reduces total cost of ownership by consolidating vendor relationships and minimizing coordination risk. This consolidation supports faster commercialization of novel pencil formats and strengthens single-source supplier models for global product portfolios, reinforcing long-term supplier-brand partnerships.

Barrier Analysis - Regulatory Complexity and Compliance Costs

Evolving packaging regulations, particularly in developed markets, impose stricter requirements on material composition, recyclability, and eco-design. Compliance often necessitates redesigning existing packaging formats, retooling production lines, and validating new materials against regulatory criteria. Smaller converters and emerging brands face disproportionately high capital expenditure burdens, which can compress margins and delay product launches. In some cases, accelerated regulatory timelines force rapid design changes that increase short-term supply costs and operational risk before long-term efficiencies are realized.

Material Cost Volatility and Technical Trade-offs

Transitioning to PCR or biodegradable materials introduces cost volatility linked to feedstock availability and processing complexity. These materials can also create technical trade-offs affecting sharpness, glide performance, and protection of the cosmetic core. Addressing these challenges requires additional formulation work, packaging compatibility testing, and certification, extending development timelines. For mass-market pencil lines with tight margin structures, these added costs can slow adoption despite regulatory and consumer pressure to shift toward sustainable alternatives.

Opportunity Analysis - Refillable Pencil Systems and Service-Based Ecosystems

Refillable eyeliner and kajal pencil packaging represents a meaningful expansion of the total addressable market. By separating durable outer housings from replaceable cores, brands can generate recurring refill revenue while reducing packaging waste per use. These systems are particularly attractive in premium and prestige segments, where higher initial prices are offset by longer product lifecycles and stronger brand loyalty. Modular tooling platforms allow rapid customization and limited-edition releases, enabling first-mover suppliers to capture elevated margins and long-term contracts.

PCR and Mono-material Decorative Solutions for Mass-Market Scale

PCR plastics and mono-material wooden or paper-composite housings offer a scalable pathway for mass-market compliance with recyclability mandates without compromising cost efficiency. Suppliers capable of delivering validated PCR content alongside recyclable decorative finishes are well-positioned to secure large, multi-regional contracts from multinational cosmetics brands seeking packaging standardization across product lines. This opportunity supports incremental volume growth beyond baseline 2026 demand, particularly in high-turnover eyeliner and kajal SKUs.

Digitalized and Connected Packaging for Premium Engagement

Digital and connected packaging elements, such as QR-enabled components and authentication features, are emerging as value-added services in the luxury eyeliner and kajal segments. These features support direct-to-consumer engagement, anti-counterfeiting measures, and refill loyalty programs. Brands can leverage digital touchpoints to improve repeat purchase rates and customer data collection, while packaging suppliers offering integrated physical-digital solutions can command higher service fees and strengthen long-term client relationships.

Category-wise Analysis

Product Type Insights

Recyclable pencil packaging is anticipated to lead the product type segment, accounting for 46.8% market share, due to broad acceptance across cosmetics brands, cost parity with conventional formats, and strong alignment with retailer sustainability requirements. Mono-material constructions using wood, PCR plastics, or paper-based composites enable compliance with recyclability standards while still supporting premium decorative finishes such as matte coatings, metallic foils, and branded embossing.

The 46.8% market share reflects the continued relevance of traditional wooden pencils in kajal formats, alongside the rapid conversion of plastic housings toward recyclable and PCR-based alternatives in eyeliners. Major global cosmetics brands increasingly specify recyclable pencil formats as default packaging for both mass-market and mid-premium SKUs, particularly for products distributed across multiple regulatory regions. Suppliers that offer validated recyclability credentials combined with advanced decoration capabilities reduce approval timelines and minimize redesign risk for global launches. As sustainability reporting becomes more standardized, recyclable pencil packaging is anticipated to maintain its leadership position, supported by scalability, regulatory compliance, and broad consumer acceptance.

Refillable systems are likely to be the fastest-growing product type as brand sustainability commitments and consumer acceptance of circular consumption models intensify. These systems deliver superior lifetime economics by reducing packaging material per use and enabling recurring refill purchases, which improve both environmental metrics and long-term revenue potential. Growth is most pronounced in premium and prestige eyeliner and kajal segments, where consumers demonstrate a higher willingness to pay for durable outer housings paired with replaceable cores.

Modular tooling platforms and standardized refill cartridges allow brands to update external aesthetics, such as colorways or limited editions, without redesigning core mechanisms. Several prestige brands have introduced refill-compatible eye products as part of broader circular beauty portfolios, using refill launches to strengthen brand loyalty. Ongoing supplier innovation is addressing technical challenges related to core retention, sharpening compatibility, and mechanical durability, gradually lowering adoption barriers for mid-tier price segments and supporting sustained share expansion.

End-user Insights

Cosmetics brands are expected to account for the majority of market demand, holding a 57.5% share, and are anticipated to remain the dominant end-user segment throughout the forecast period. Their leadership stems from control over product innovation pipelines, marketing investment, and global SKU strategies. Large multinational brands favor standardized packaging specifications across regions, driving high-volume procurement of recyclable and premium pencil formats that can be deployed consistently across North America, Europe, and Asia Pacific.

Supplier selection increasingly prioritizes global manufacturing reach, decorative sophistication, and verified sustainability credentials, resulting in demand consolidation among established converters capable of serving multiple markets. The dominance of cosmetics brands is further reinforced by frequent premium eyeliner and kajal launches, where packaging quality, tactile feel, and visual differentiation play a direct role in consumer purchasing decisions. As eye-makeup continues to be positioned as an accessible luxury category, brand-led demand for high-performance packaging is expected to remain structurally strong.

Brand-driven sustainability initiatives, including refill clubs, in-store return schemes, and subscription-based refill services, are likely to be the fastest-growing end-user segment and are anticipated to gain material share over the medium term. These programs reposition packaging from a single-use component into an ongoing engagement platform, improving customer lifetime value while reducing waste intensity per product sold.

Digitally native and prestige brands are leading adoption, leveraging direct-to-consumer channels to integrate refill purchasing with loyalty programs and personalized marketing. Early implementations demonstrate higher repeat purchase rates and improved margin stability when refill pricing and logistics are well-structured. As regulatory scrutiny and consumer expectations around waste reduction increase, sustainability-focused end-user programs are expected to transition from niche initiatives to core brand strategies, creating sustained demand for refill-compatible eyeliner and kajal packaging systems.

Regional Insights

North America Eyeliner and Kajal Sculpting Pencil Packaging Market Trends - Prestige Beauty Premiumization and Refillable Innovation

North America is expected to be the largest regional market, accounting for an estimated 33.7% of global value, supported by a high concentration of global cosmetics brand headquarters, a strong prestige beauty ecosystem, and an advanced omnichannel retail infrastructure. The U.S. dominates regional demand, driven by high per-capita spending on premium cosmetics, rapid product refresh cycles, and the growing influence of direct-to-consumer and specialty beauty retailers. Canada contributes steady growth, particularly in clean-beauty and sustainability-positioned eye-makeup categories, where packaging transparency and recyclability strongly influence purchase decisions.

Premiumization remains a central growth driver, reinforced by innovation-led launches from multinational brand groups such as Estée Lauder Companies and L’Oréal USA, which have increasingly prioritized recyclable and refill-compatible eyeliner and brow products across prestige portfolios. Several U.S. prestige brands have piloted refillable eye products through selective retail and online channels, using refill formats to support loyalty programs and sustainability storytelling.

Retailers such as Sephora and Ulta Beauty have amplified this shift by highlighting recyclable materials and refill concepts within curated “clean” and “responsible beauty” assortments. Regulatory pressure at the federal level remains moderate; however, state-level initiatives, particularly in California and the Northeast, along with voluntary industry commitments, are accelerating the transition toward higher recycled content and mono-material designs. In response, packaging suppliers operating in North America are investing in high-precision decoration, digital printing, and refill mechanics to meet both branding and compliance needs. Integrated global suppliers with U.S. manufacturing or finishing capabilities are increasingly favored, as they enable rapid commercialization while ensuring alignment with evolving sustainability standards across international markets.

Europe Eyeliner and Kajal Sculpting Pencil Packaging Market Trends - Regulation-Driven Eco-Design and Refillable Pencil Leadership

Europe accounts for a substantial share of global market value, underpinned by strong prestige cosmetics demand and the region’s leadership in sustainability regulation and packaging innovation. Germany functions as a key manufacturing and converter hub, hosting several specialized pencil and cosmetic packaging suppliers with advanced engineering and material expertise. France and the U.K. lead in premium brand innovation, driven by globally influential beauty houses and strong consumer preference for high-quality, design-led packaging. Southern European markets, including Spain, continue to record steady growth in mid-premium segments, supported by expanding specialty retail and private-label activity.

Regulatory frameworks across the European Union place significant emphasis on recyclability, eco-design, material reduction, and reporting, directly shaping eyeliner and kajal packaging specifications. Initiatives linked to extended producer responsibility and upcoming packaging waste regulations have accelerated the adoption of mono-material constructions, FSC-certified wood pencils, and refillable systems. Major European beauty groups, including LVMH and L’Oréal, have publicly committed to reducing virgin plastic use and scaling refill formats, influencing supplier requirements and accelerating investment in compliant tooling and materials.

These regulatory pressures increase short-term compliance costs but create durable competitive advantages for early adopters of recyclable and refillable designs. Investment activity in the region is focused on securing PCR feedstock, advancing decorative techniques compatible with sustainable substrates, and developing retrofit-ready refill mechanisms that can be deployed across multiple brands. Ongoing consolidation activity targets niche players with expertise in decoration, eco-materials, or mechanical innovation, reinforcing Europe’s position as a global center for premium, regulation-ready cosmetic pencil packaging.

Asia Pacific Eyeliner and Kajal Sculpting Pencil Packaging Market Trends - High-Volume Manufacturing and Rapid SKU Expansion

Asia Pacific is expected to be the fastest-growing regional market, driven by rising cosmetics consumption, expanding middle-class populations, and the region’s role as a global manufacturing backbone for beauty packaging. China and India generate high volumes through rapid SKU proliferation, mass-market eyeliner adoption, and strong domestic brand activity, while Japan sustains demand for high-precision, premium packaging with a focus on performance, durability, and aesthetic refinement. ASEAN markets serve a dual role as cost-competitive manufacturing hubs and fast-emerging consumer markets for eye makeup products.

Growth across the region is supported by accelerating e-commerce penetration, influencer-led product launches, and short innovation cycles, particularly among digitally native Chinese and Southeast Asian brands. Global and regional contract manufacturers in China, South Korea, and Taiwan continue to expand capacity for cosmetic pencil components, supplying both local brands and international multinationals. Japanese brands, known for technical precision, have influenced regional expectations around sharpening performance, core stability, and smooth application, indirectly raising quality benchmarks across Asia Pacific.

Regulatory standards vary significantly across the region, creating short-term flexibility for scalable production while encouraging gradual upgrades toward PCR use and mono-material compliance. Multinational brands operating in Asia Pacific increasingly apply global sustainability specifications to locally produced SKUs, driving technology transfer and supplier capability upgrades. Investment is flowing into refill tooling platforms, localized decoration capacity, and certification infrastructure, reinforcing Asia Pacific’s dual role as both a high-growth demand engine and a critical supply base for recyclable and refill-compatible eyeliner and kajal packaging worldwide.

Competitive Landscape

The global eyeliner and kajal sculpting pencil packaging market exhibits a mixed competitive structure. Large global converters dominate premium and export-oriented volumes through integrated services spanning tooling, decoration, and sustainability certification. Alongside these players, a fragmented group of regional manufacturers supplies local brands and mass-market segments with cost-competitive solutions. Overall concentration is moderate, with competitive advantage increasingly defined by sustainability credentials, design integration, and global manufacturing reach.

Recent strategic activity includes the introduction of refillable and mono-material cosmetic stick and pencil solutions, expanded exhibition of sustainable color cosmetic packaging concepts at international trade events, and the development of connected packaging platforms integrating digital engagement with refillable formats. These developments underscore a sector-wide focus on circularity, premium engagement, and technology-enabled differentiation.

Leading strategies emphasize sustainability leadership, modular refill platforms, and premium decorative capabilities. Market leaders bundle design, certification, and global supply to reduce client risk, while smaller competitors focus on cost efficiency, regional responsiveness, and niche decoration expertise.

Key Industry Developments

- In February 2025, Sulapac introduced Flow 1.8, a bio-based extrusion material designed to offer an eco-friendly alternative for cosmetic pencil packaging that reduces reliance on traditional plastics, supporting biodegradable and low-carbon production formats.

- In April 2025, L’Oréal partnered with Urban Decay to co-develop sustainable eyeliner pencils with the aim of reducing plastic usage in pencil packaging by 50%, reinforcing industry momentum toward recyclable and high-performance green formats.

Companies Covered in Eyeliner and Kajal Sculpting Pencil Packaging Market

- Albéa Group

- HCT Group

- AptarGroup

- Quadpack

- Anomatic

- Schwan Cosmetics

- Intercos Group

- Chromavis Fareva

- Faber-Castell Cosmetics

- Kolmar Korea

- Taiki Group

- Yonwoo (a Quadpack company)

- APC Packaging

- Lumson

- Baralan

- Libo Cosmetics

- Cosmei (PENN Group)

- Alkos Group

Frequently Asked Questions

The global eyeliner and kajal sculpting pencil packaging market is likely to be valued at US$168.9 million in 2026.

By 2033, the eyeliner and kajal sculpting pencil packaging market is expected to reach US$269.4 million.

Key trends include the rapid adoption of recyclable mono-material pencil designs, growing deployment of refillable eyeliner and kajal systems, increased use of post-consumer recycled (PCR) plastics, and the rising demand for premium decoration and customization to support brand differentiation across global launches.

Recyclable pencil packaging is the leading product segment, accounting for 46.8% market share, driven by broad brand acceptance, retailer support, and alignment with global recyclability requirements.

The market is projected to grow at a CAGR of 6.9% between 2026 and 2033.

Major players with strong cosmetic pencil packaging portfolios include Albéa Group, HCT Group, AptarGroup, Quadpack, and Anomatic.