- Clothing, Footwear, & Accessories

- Europe Sports Apparel Market

Europe Sports Apparel Market Size, Share, and Growth Forecast 2026 - 2033

Europe Sports Apparel Market by Product Type (Tops and T-shirts, Trousers and Tights, Shirts and T-shirts, Others), End User (Men, Women, Kids), by Distribution Channel (Online, Offline), and Regional Analysis for 2026 - 2033

Europe Sports Apparel Market Size and Trend Analysis

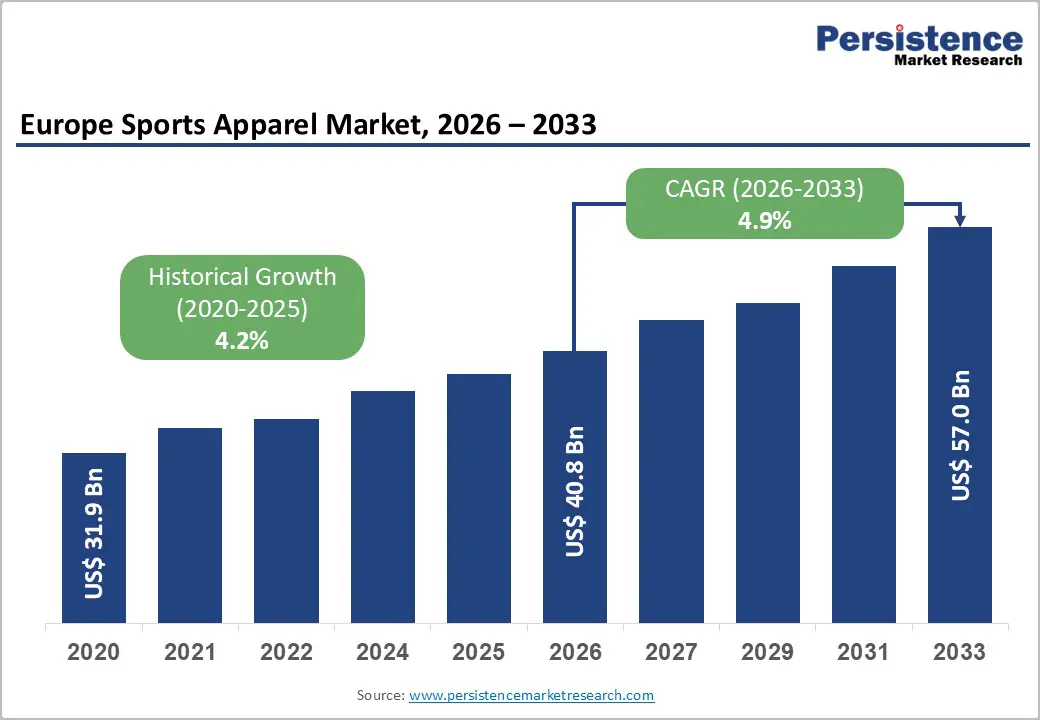

The Europe Sports Apparel market size is supposed to be valued at US$ 40.8 Billion in 2026 and is projected to reach US$ 57.0 Billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033.

The European sports apparel market's consistent and accelerating growth is underpinned by the continent's deepening health and fitness culture, the mainstreaming of athleisure as everyday fashion, and the growing adoption of premium performance fabrics by an increasingly health-conscious consumer base. The rise of direct-to-consumer digital platforms by leading brands including Nike, Inc., Adidas AG, and Puma SE is expanding consumer access to premium sports apparel across secondary European cities and lower-income demographic segments previously underserved by traditional retail channels, broadening the market's addressable consumer base throughout the forecast period.

Key Market Highlights

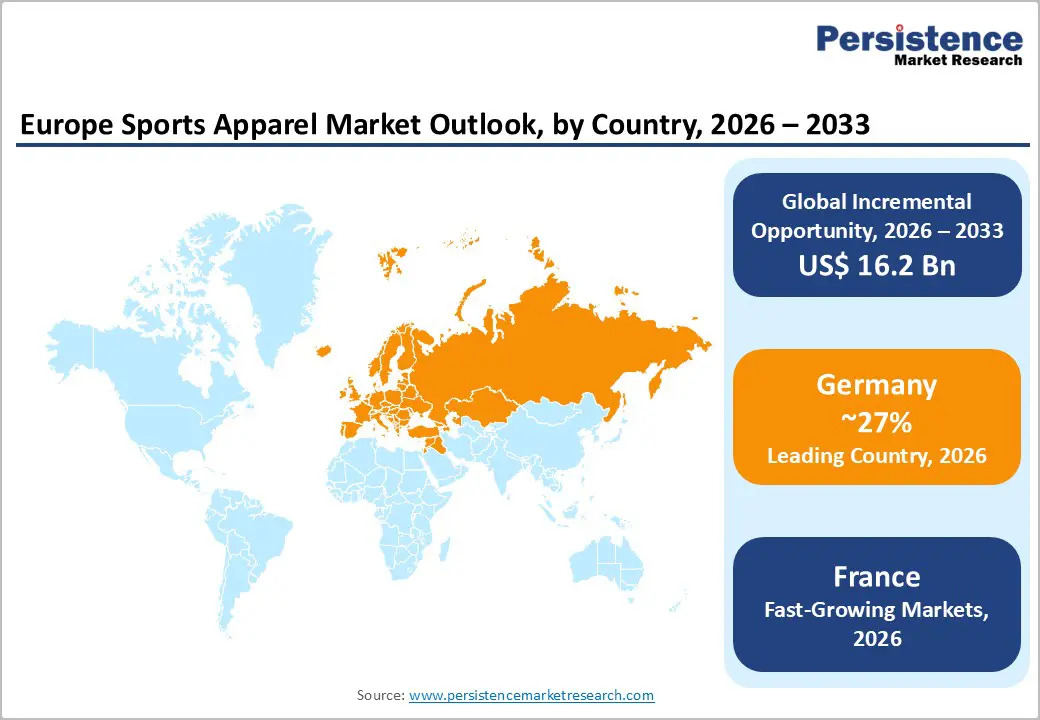

- Leading Country: Germany leads the European Sports Apparel market with a dominant 27% market share anchored by approximately 86,000 sports clubs.

- Fastest Growing Country: France is among the fastest-growing European markets with a projected 5.6% CAGR, driven by the Paris 2024 Olympic Games legacy on national sports participation, the CNOSF's record post-Games club registrations, and the government's Héritage Paris 2024 sports infrastructure investment program sustaining elevated active consumer base growth.

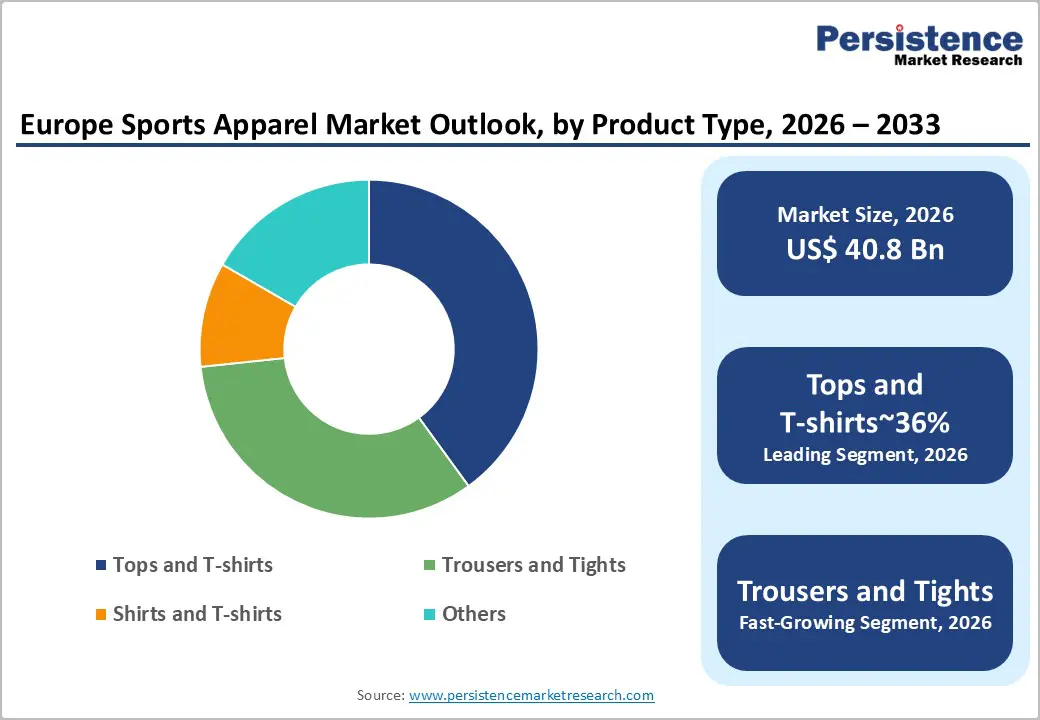

- Dominant Product Type: T-shirts dominate the Product Type segment with approximately 36% revenue share in 2026, confirmed as the leading product in European sports apparel by multiple data sources, driven by universal multi-sport applicability, high repurchase frequency, and premium technology branding across Nike Dri-FIT, Adidas AEROREADY, and Under Armour HeatGear performance collections.

- Growing Sales Channel: The online distribution channel is the fastest-growing segment, validated by Puma SE's e-commerce growing at 21.1% currency-adjusted in Q4 2024 and Adidas AG's expanding DTC digital platform, with European consumers increasingly shifting to brand websites and multi-brand platforms for convenience, personalization, and access to exclusive performance collections.

- Leading End-user: Women's sports apparel represents a significant growth opportunity, with 49.1% market share in 2026 growing at 6.4% CAGR, driven by record female sports participation, the yoga and barre fitness boom, and the fashion-performance convergence making sports leggings the dominant everyday apparel item for European women.

| Key Insights | Details |

|---|---|

|

Europe Sports Apparel Market Size (2026E) |

US$ 40.8 Billion |

|

Market Value Forecast (2033F) |

US$ 57.0 Billion |

|

Projected Growth CAGR (2026–2033) |

4.9% |

|

Historical Market Growth (2020–2025) |

4.2% |

Market Dynamics

Drivers - Rising Health and Fitness Consciousness Across Europe Driving Sustained Sports Apparel Demand

The structural and demographically broad shift toward active lifestyles across Europe, encompassing recreational running, gym fitness, yoga, cycling, team sports, and outdoor activities, is generating a durable and expanding consumer demand base for performance-oriented sports apparel that delivers technical functionality alongside contemporary aesthetics. The European Commission's Eurobarometer on Sport and Physical Activity has documented that approximately 44% of EU citizens exercise or play sport at least once a week, a figure that has risen steadily over the past decade driven by government public health campaigns, growing awareness of lifestyle disease prevention, and the cultural normalization of fitness as a social activity.

The World Health Organization (WHO)'s European regional office has consistently identified physical inactivity as the fourth leading risk factor for global mortality, motivating national governments across Germany, France, Italy, Spain, and the United Kingdom to implement funded physical activity promotion programs that expand organized sports participation and directly stimulate sports apparel procurement volumes. The Confederation of European Paper Industries (CEPI) analogy aside, it is the European Apparel and Textile Confederation (Euratex) that has confirmed the sports and activewear segment as the single highest-growth category within European apparel manufacturing, attracting significant brand and retailer investment in product development and distribution capacity expansion.

Athleisure Trend and Fashion-Performance Fusion Expanding the Addressable Sports Apparel Consumer Market

The global athleisure revolution, representing the cultural normalization of performance sportswear as versatile everyday fashion attire suitable for work, social engagement, and leisure in addition to athletic activity, is fundamentally expanding the addressable market for sports apparel across all European consumer demographics well beyond dedicated athletes. The rising popularity of athleisure is one of the most anticipated demand drivers for Europe sports apparel market. Consumers increasingly seek clothing combining sport functionality with stylish aesthetics that enables seamless transitions from gym sessions to casual social environments.

Adidas AG, reporting FY2024 global revenues of €23.68 billion, and Puma SE, reporting FY2024 apparel revenues of €2.81 billion growing at a currency-adjusted 3.7%, have both strategically expanded their lifestyle and athleisure collections targeting fashion-conscious European consumers who prioritize versatile, performance-inspired apparel over conventional casual clothing. The Centre for the Promotion of Imports from developing countries (CBI), part of the Dutch Ministry of Foreign Affairs, confirmed that Europe's total fashion sportswear import value reached €11.7 billion with average annual growth of 4.6% between 2016 and 2021, confirming the sustained commercial scale of athleisure demand across European markets.

Restraints - Intense Price Competition from Fast-Fashion and Private-Label Brands Compressing Premium Brand Margins

The European sports apparel market faces mounting pricing pressure from fast-fashion retailers including H&M, Zara (Inditex), and Primark that have aggressively expanded into athletic and activewear product categories at significantly lower price points than established performance brands, attracting budget-conscious consumers and eroding the addressable premium market segment.

The European Fashion Industry Benchmark has noted that private-label activewear now constitutes a measurable and growing share of athletic apparel sales at major European supermarket and department store chains, directly competing with branded performance sportswear for the casual fitness consumer segment. For mid-tier sports apparel brands, this pricing environment is particularly challenging, compressing operating margins and limiting the investment capacity for product innovation and marketing that are required to maintain competitive differentiation against both premium and value-price alternatives.

Supply Chain Complexity and Raw Material Cost Inflation Impacting Profitability and Inventory Management

Europe sports apparel industry continues to navigate significant supply chain challenges, including elevated prices for technical performance textiles such as recycled polyester, elastane-nylon blends, and moisture-management finishes, that are compressing manufacturing cost structures and complicating inventory planning cycles. The European Central Bank (ECB) maintained elevated benchmark interest rates through much of 2024–2025 in response to persistent inflation, increasing the carrying cost of inventory for sports apparel brands managing broad product ranges across multiple seasonal collections.

The EU's mandatory Due Diligence Directive and Textile Labelling Regulation, requiring transparent supply chain documentation and material content disclosure, impose compliance overhead on sports apparel manufacturers sourcing materials across multi-country supply chains, adding administrative and audit costs that disproportionately affect smaller European brands relative to global multinationals with dedicated compliance infrastructure.

Opportunity - Women's Sports Apparel Segment Representing Europe's Highest-Growth Consumer Category

The women's segment is the single most commercially compelling growth opportunity in the Europe Sports Apparel market, driven by record female sports participation growth, the explosive popularity of women's fitness activities including yoga, barre, Pilates, and strength training, and the fashion-performance convergence that has made women's sports leggings and athletic tops the dominant everyday casual apparel choice across multiple European demographic groups. The demand for customized sports clothing among women participating regularly in sports is rising strongly, supported by Sport England findings that 63.1% of the population meets weekly physical activity targets, with female participation growing at an above-average rate.

Adidas AG's women's-dedicated product development programs, Lululemon Athletica Inc.'s European expansion strategy, and Puma SE's celebrity collaboration-based women's marketing approach, which drove apparel revenues to €2.81 billion in FY2024, collectively validate the enormous commercial scale of this demographic opportunity for sports apparel manufacturers investing in women-specific design innovation, inclusive sizing ranges, and digital-first marketing strategies targeting European female consumers across fitness and lifestyle categories.

Sustainability-Driven Innovation and Eco-Friendly Materials Creating Premium Positioning Opportunities

The accelerating adoption of sustainability credentials and circular economy principles in European sports apparel, driven by stringent EU regulatory requirements, mounting consumer environmental consciousness, and corporate ESG mandates from major European retailers, is creating a structurally growing commercial opportunity for brands that successfully integrate certified sustainable materials and transparent production practices into their sports apparel value chains. The EU's Green Deal Textile Strategy and the upcoming EU Ecodesign for Sustainable Products Regulation (ESPR), which will mandate minimum recycled content and durability standards for textiles sold in the EU market, are compelling all sports apparel market participants to invest in eco-design capabilities, recycled polyester sourcing, and closed-loop garment take-back programs.

Nike Inc.'s Move to Zero initiative, targeting at least 75% recycled polyester content across its performance collections, and Adidas AG's commitment to replacing all virgin polyester with recycled alternatives by 2024 demonstrate the leading brands' strategic response to this regulatory and consumer demand-driven sustainability imperative. Smaller European specialist brands including Hummel International and Errea Sport S.p.A. are building differentiated market positions around certified sustainable production, attracting environmentally conscious European consumers willing to pay measurable price premiums for verifiably responsible sports apparel.

Category-wise Analysis

Product Type Insights

Tops and T-shirts lead the European Sports Apparel market by product type, accounting for approximately 36% of total product type segment revenue in 2026, a position consistently confirmed across multiple Sports tops and performance T-shirts command market leadership through their universal applicability across virtually every sport and fitness discipline, from football and rugby to running, gym training, cycling, and yoga, and their role as the foundational garment layer in any athlete's apparel wardrobe.

The CBI's analysis of European fashion sportswear imports confirmed that knitwear performance tops represent one of the largest individual sub-segments by import value, reflecting the high volume and frequent repurchase rates that characterize the tops category. Nike's Dri-FIT, Adidas AG's AEROREADY, and Under Armour's HeatGear performance top platforms are the three most commercially visible technology-branded sports top collections in the European market, each commanding premium price points that sustain disproportionate revenue share relative to unit volume. Trousers and Tights represent the second-largest category, driven primarily by female athleisure adoption and the explosive popularity of performance leggings across yoga, running, and casual wear contexts.

End-user Insights

The Men's segment leads the Europe sports apparel market by end-user, accounting for approximately 51% of total segment revenue in 2026, sustained by men's historically higher absolute sports participation volumes across organized team sports, competitive athletics, and gym fitness, and by the higher average selling prices commanded by technical performance garments in the men's segment across football, cycling, and outdoor sports. Germany's approximately 86,000 sports clubs, the majority of which are male-participation-dominated football, athletics, and gymnastics organizations, drive consistent institutional sports kit procurement that underpins the men's segment's revenue leadership.

The Women's segment is growing at the highest CAGR within the end-user category, achieving 49.1% share in 2026 and projected growth at 6.4% CAGR through the forecast period. The Kids segment is an important and steadily growing category, driven by school sports programs, growing parental investment in youth athletic development, and the expanding youth football, gymnastics, and swimming participation infrastructure across Germany, France, Italy, and Spain.

Distribution Channel Insights

The offline distribution channel remains the leading segment in the European Sports Apparel market by distribution channel, accounting for approximately 62% of total channel revenue in 2026, reflecting the European consumer's strong preference for in-store product testing, size assessment, and personal fitting, particularly for technically specified performance apparel. Specialist sports retailers, including Intersport International Corporation, Decathlon Group, and national sporting goods chains, maintain dominant offline distribution positions, leveraging their trained store staff and broad multi-brand product ranges to serve European consumers seeking expert guidance across sports apparel performance specifications.

Decathlon Group in particular, with over 1,700 stores globally and a deep European retail footprint, has built Europe's most accessible sports apparel offline distribution network, combining competitive pricing with broad category coverage across all sports disciplines and consumer demographics. The Online channel is the fastest-growing distribution segment, driven by the accelerating shift to direct-to-consumer brand websites, multi-brand platforms, and mobile commerce, with Puma SE's e-commerce growing 21.1% currency-adjusted in Q4 2024, confirming the channel's above-average revenue growth trajectory through the forecast period.

Country Insights

Germany Sports Apparel Market Trends

Germany is the leading national market within the European sports apparel industry, generating a dominant 27% share of total European sports apparel revenues, anchored by the country's deeply embedded sporting culture, the world's largest concentrated base of organized sports clubs at approximately 86,000 across the nation per Statista, and its position as the global headquarters of two of the world's largest sports apparel brands, Adidas AG (Herzogenaurach) and Puma SE (Herzogenaurach). The country's robust economy sustains above-average consumer willingness to invest in premium performance sports apparel, and its diverse retail infrastructure, spanning specialist sports chains, brand mono-stores, and a rapidly growing online market, ensures broad product accessibility across all consumer demographics.

Germany's football-dominated sports culture, with the German Football Association (DFB) governing over 7 million registered members across 25,000 clubs, generates consistent and large-volume sports apparel procurement for both amateur club kit and consumer replica wear markets. The country's growing interest in running, cycling, and outdoor sports, driven by national fitness promotion initiatives and a health-conscious urban professional demographic, is expanding demand for technical performance apparel beyond traditional team sports categories. Adidas AG's FY2024 global revenues of €23.68 billion and its continued European brand investment reinforce Germany's dual role as the continent's largest sports apparel consumer market and its most influential brand development ecosystem.

Italy Sports Apparel Market Trends

Italy is a commercially significant and culturally distinctive sports apparel market within Europe, shaped by the country's powerful fashion industry heritage, centered in Milan as a global luxury and fashion capital, that cultivates consumer demand for sports apparel that seamlessly integrates performance functionality with premium aesthetic design. Italian consumers demonstrate above-average willingness to purchase premium-priced sports apparel collections that blend technical performance credentials with distinctive Italian design language, creating a commercially attractive opportunity for both global performance brands and Italy's own specialized sports apparel manufacturers, including Errea Sport S.p.A. and Kappa, which are internationally recognized for their technical teamwear and stylish performance collections. The CBI's European fashion sportswear market analysis confirmed Italy as one of the largest national markets within Europe's €11.7 billion fashion sportswear import value framework.

Italy's strong football culture, administered by the Federazione Italiana Giuoco Calcio (FIGC), one of Europe's largest national football federations by club membership, generates substantial domestic demand for performance football apparel and official club replica kits from leading global and domestic brands. The country's growing cycling participation base, particularly in road cycling, mountain biking, and the dedicated amateur sportive race community that participates in iconic events including the L'Eroica and Gran Fondo circuit, drives specialized technical cycling apparel demand across compression, aerodynamic, and thermal protection garment categories. The EU's ESPR textile regulation and Green Deal textile strategy are particularly impactful in Italy, where manufacturers face compliance requirements that accelerate investment in certified sustainable production processes and recycled performance fabric sourcing.

France Sports Apparel Market Trends

France is one of Europe's largest and fastest-growing sports apparel markets, with the country's position as the world's foremost global sports events host, anchoring Paris 2024 Olympic Games, Tour de France, Roland Garros, and the UEFA Euro schedule, generating unparalleled live sports engagement, aspirational athletic identity, and sustained sports apparel retail demand across a broad cross-section of the French population. France's sportswear market generated approximately US$ 10.9 billion in 2026 revenues and is projected to grow at a CAGR of 5.9% through the forecast period, making it one of Europe's highest-growth national sports apparel markets. Paris' identity as both a global fashion capital and Olympic Games host city uniquely amplifies the fashion-performance convergence trend, compelling French consumers to seek sports apparel that meets both technical performance and elevated design standards simultaneously.

The Paris 2024 Olympic and Paralympic Games generated a documented legacy effect on French sports participation and sports apparel consumption, with the French National Olympic and Sports Committee (CNOSF) reporting record sports club registrations in the months following the Games across cycling, swimming, athletics, and team sports disciplines. The French government's Héritage Paris 2024 sports participation legacy program is sustaining elevated investment in grassroots sports infrastructure and organized sports participation promotion, directly expanding the active consumer base for performance sports apparel brands operating in the French market. Decathlon Group, headquartered in Villeneuve-d'Ascq, France, serves as the dominant domestic sports apparel retailer, combining its manufacturing scale, owned-brand product range, and extensive store network across France to offer accessible sports apparel across every price tier and sports category.

Competitive Landscape

Europe sports apparel market is moderately consolidated at the premium tier, with Adidas AG, Nike, Inc., Puma SE, and Decathlon Group collectively commanding the largest aggregate market shares through brand equity, retail scale, and product portfolio breadth. Market leaders differentiate through proprietary fabric technologies, Adidas AG's AEROREADY, Nike's Dri-FIT ADV, and Under Armour's HeatGear, combined with elite athlete and team sponsorship programs that deliver continuous brand visibility across Europe's most-watched sports.

Emerging business model trends include direct-to-consumer digital subscription services, personalized sports apparel programs powered by body-scanning apps, and certified sustainable product lines targeting European regulatory compliance. Mid-tier specialists including Hummel International, Errea Sport S.p.A., and Mizuno Corporation compete effectively through sport-specific technical expertise and club-level teamwear partnership programs that major brands are less nimble in serving.

Key Developments:

- In January 2025: Puma SE was identified as the most prominent brand across Europe's top 10 football leagues, surpassing Nike and Adidas, with kitting deals spanning multiple elite clubs, reinforcing its dominant position in the high-visibility European football apparel market.

- In March 2025: Nike, Inc. launched an expanded sustainable sports apparel collection incorporating at least 75% recycled polyester content across its European performance range, aligned with its Move to Zero environmental commitment and targeting EU Green Deal textile compliance requirements.

- In 2024: Adidas AG reported FY2024 global revenues of €23.68 billion, with its European region remaining the company's largest and most commercially significant market, supported by expanded DTC digital investment and renewed high-profile club sponsorship activations across Bundesliga, Serie A, and Ligue 1.

Companies Covered in Europe Sports Apparel Market

- Adidas AG

- Nike Inc.

- Puma SE

- Under Armor Inc.

- Decathlon Group

- ASICS Corporation

- New Balance Athletics, Inc.

- Reebok International Ltd.

- Columbia Sportswear Company

- Lululemon Athletica Inc.

- Hummel International

- Mizuno Corporation

- Errea Sport S.p.A.

- Intersport International Corporation

- Kappa

Frequently Asked Questions

Europe Sports Apparel market is estimated to be valued at US$ 40.8 Billion in 2026 and is projected to reach US$ 57.0 Billion by 2033, registering a forecast CAGR of 4.9% between 2026 and 2033. The market recorded a historical growth rate of 4.2% CAGR between 2020 and 2025, supported by rising health consciousness, athleisure adoption, and expanding women's sports participation across Europe.

The key growth drivers are Europe's structurally expanding fitness culture, with the European Commission's Eurobarometer documenting 44% of EU citizens exercising weekly, and the global athleisure trend normalized by Adidas AG's €23.68 billion FY2024 revenues and CBI's confirmed €11.7 billion European fashion sportswear import value growing at 4.6% annually. Government physical activity mandates and brand DTC digital investment further sustain consistent consumer demand expansion.

Tops and T-shirts lead the Product Type category with approximately 36% revenue share in 2026, confirmed as the leading product segment across European sports apparel analyses. Their leadership reflects universal multi-sport applicability, high repurchase frequency, and premium technology branding through Nike's Dri-FIT, Adidas' AEROREADY, and Under Armour's HeatGear collections that sustain above-average average selling prices across the European retail landscape.

Germany leads the European Sports Apparel market with a dominant 27% share anchored by approximately 86,000 sports clubs documented by Statista, the global headquarters of Adidas AG and Puma SE, Europe's largest organized football federation infrastructure, and the highest per-capita premium sportswear investment driven by Germany's robust economy and deeply embedded sporting culture.

The most significant opportunity is the women's sports apparel segment, with GMInsights documenting European women's sportswear at 49.1% market share in 2024 growing at 6.4% CAGR. Record female sports participation, the yoga and barre fitness boom, Paris 2024 Olympic legacy effects on women's athletics enrollment, and the fashion-performance convergence in leggings and tops collectively create Europe's highest-incremental-revenue consumer demographic for sports apparel brand investment.