- Executive Summary

- Global Enterprise Mobility Management Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Enterprise IT Spending Trends

- Smartphone and Mobile Device Penetration

- Cloud Computing Adoption

- Cybersecurity Spending Growth

- Labor Market Mobility and Workforce Digitization

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis

- Price by Component

- Price Impact Factors

- Global Enterprise Mobility Management Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Global Enterprise Mobility Management Market Outlook: Component

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Component, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Component, 2026-2033

- Solutions

- Mobile Device Management (MDM)

- Mobile Content Management (MCM)

- Identity and Access Management (IAM)

- Mobile Application Management (MAM)

- Others

- Services

- Professional Services

- Managed Services

- Solutions

- Market Attractiveness Analysis: Component

- Global Enterprise Mobility Management Market Outlook: Deployment

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Deployment , 2020-2025

- Current Market Size (US$ Bn) Forecast, by Deployment , 2026-2033

- Cloud / SaaS

- On-Premises

- Hybrid

- Market Attractiveness Analysis: Deployment

- Global Enterprise Mobility Management Market Outlook: Industry

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Industry, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Industry, 2026-2033

- BFSI

- IT & Telecom

- Healthcare

- Government & Public Sector

- Retail & E-commerce

- Manufacturing

- Transportation & Logistics

- Energy & Utilities

- Others

- Market Attractiveness Analysis: Industry

- Global Enterprise Mobility Management Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Enterprise Mobility Management Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- North America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) Forecast, by Component, 2026-2033

- Solutions

- Mobile Device Management (MDM)

- Mobile Content Management (MCM)

- Identity and Access Management (IAM)

- Mobile Application Management (MAM)

- Others

- Services

- Professional Services

- Managed Services

- Solutions

- North America Market Size (US$ Bn) Forecast, by Deployment , 2026-2033

- Cloud / SaaS

- On-Premises

- Hybrid

- North America Market Size (US$ Bn) Forecast, by Industry, 2026-2033

- BFSI

- IT & Telecom

- Healthcare

- Government & Public Sector

- Retail & E-commerce

- Manufacturing

- Transportation & Logistics

- Energy & Utilities

- Others

- Europe Enterprise Mobility Management Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Europe Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) Forecast, by Component, 2026-2033

- Solutions

- Mobile Device Management (MDM)

- Mobile Content Management (MCM)

- Identity and Access Management (IAM)

- Mobile Application Management (MAM)

- Others

- Services

- Professional Services

- Managed Services

- Solutions

- Europe Market Size (US$ Bn) Forecast, by Deployment , 2026-2033

- Cloud / SaaS

- On-Premises

- Hybrid

- Europe Market Size (US$ Bn) Forecast, by Industry, 2026-2033

- BFSI

- IT & Telecom

- Healthcare

- Government & Public Sector

- Retail & E-commerce

- Manufacturing

- Transportation & Logistics

- Energy & Utilities

- Others

- East Asia Enterprise Mobility Management Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- East Asia Market Size (US$ Bn) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) Forecast, by Component, 2026-2033

- Solutions

- Mobile Device Management (MDM)

- Mobile Content Management (MCM)

- Identity and Access Management (IAM)

- Mobile Application Management (MAM)

- Others

- Services

- Professional Services

- Managed Services

- Solutions

- East Asia Market Size (US$ Bn) Forecast, by Deployment , 2026-2033

- Cloud / SaaS

- On-Premises

- Hybrid

- East Asia Market Size (US$ Bn) Forecast, by Industry, 2026-2033

- BFSI

- IT & Telecom

- Healthcare

- Government & Public Sector

- Retail & E-commerce

- Manufacturing

- Transportation & Logistics

- Energy & Utilities

- Others

- South Asia & Oceania Enterprise Mobility Management Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Component, 2026-2033

- Solutions

- Mobile Device Management (MDM)

- Mobile Content Management (MCM)

- Identity and Access Management (IAM)

- Mobile Application Management (MAM)

- Others

- Services

- Professional Services

- Managed Services

- Solutions

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Deployment , 2026-2033

- Cloud / SaaS

- On-Premises

- Hybrid

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Industry, 2026-2033

- BFSI

- IT & Telecom

- Healthcare

- Government & Public Sector

- Retail & E-commerce

- Manufacturing

- Transportation & Logistics

- Energy & Utilities

- Others

- Latin America Enterprise Mobility Management Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Latin America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) Forecast, by Component, 2026-2033

- Solutions

- Mobile Device Management (MDM)

- Mobile Content Management (MCM)

- Identity and Access Management (IAM)

- Mobile Application Management (MAM)

- Others

- Services

- Professional Services

- Managed Services

- Solutions

- Latin America Market Size (US$ Bn) Forecast, by Deployment , 2026-2033

- Cloud / SaaS

- On-Premises

- Hybrid

- Latin America Market Size (US$ Bn) Forecast, by Industry, 2026-2033

- BFSI

- IT & Telecom

- Healthcare

- Government & Public Sector

- Retail & E-commerce

- Manufacturing

- Transportation & Logistics

- Energy & Utilities

- Others

- Middle East & Africa Enterprise Mobility Management Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Middle East & Africa Market Size (US$ Bn) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) Forecast, by Component, 2026-2033

- Solutions

- Mobile Device Management (MDM)

- Mobile Content Management (MCM)

- Identity and Access Management (IAM)

- Mobile Application Management (MAM)

- Others

- Services

- Professional Services

- Managed Services

- Solutions

- Middle East & Africa Market Size (US$ Bn) Forecast, by Deployment , 2026-2033

- Cloud / SaaS

- On-Premises

- Hybrid

- Middle East & Africa Market Size (US$ Bn) Forecast, by Industry, 2026-2033

- BFSI

- IT & Telecom

- Healthcare

- Government & Public Sector

- Retail & E-commerce

- Manufacturing

- Transportation & Logistics

- Energy & Utilities

- Others

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Microsoft Corporation

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- VMware, Inc.

- IBM Corporation

- Citrix Systems

- Ivanti

- BlackBerry

- Cisco Systems, Inc.

- SAP SE

- Broadcom, Inc.

- Zoho Corporation Pvt. Ltd.

- Sophos

- Matrix42

- Others

- Microsoft Corporation

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Hardware & Software IT Services

- Enterprise Mobility Management Market

Enterprise Mobility Management Market Size, Share, and Growth Forecast, 2026 - 2033

Enterprise Mobility Management Market by Component (Solutions, Services), Deployment (Cloud / SaaS, On-Premises, Hybrid), Industry (BFSI, IT & Telecom, Healthcare, Government & Public Sector, Retail & E-commerce, Manufacturing, Transportation & Logistics, Energy & Utilities, Others), and Regional Analysis for 2026 - 2033

Enterprise Mobility Management Market Size and Trends Analysis

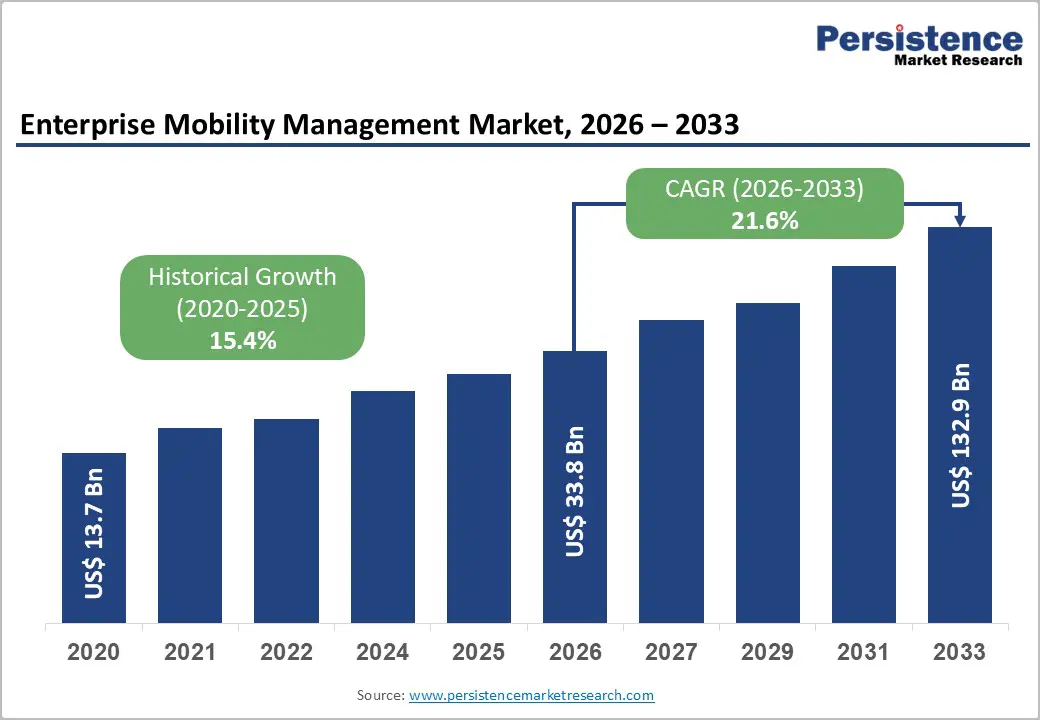

The global Enterprise Mobility Management Market size is projected to rise from US$33.8 Bn in 2026 to US$132.9 Bn by 2033. It is anticipated that the market will grow at a CAGR of 21.6% from 2026 to 2033, driven by accelerating adoption of remote and hybrid work, the proliferation of mobile and IoT endpoints, and tightening data protection regulations across major economies.

Enterprises are prioritizing unified control over devices, applications, and data to reduce cyber risk and improve productivity, driving higher spending on comprehensive mobility platforms. Sustained growth in BYOD policies and cloud-first IT architectures reinforces the need for scalable, policy-driven enterprise mobility management integrated with identity, security, and collaboration stacks.

Key Industry Highlights:

- Leading Solution: Mobile Device Management (MDM) dominates with over 37% market share in 2026, valued at more than US$ 9 Bn, driven by the need for centralized device control, security enforcement, and compliance monitoring. Mobile Application Management (MAM) is the fastest-growing, enabling app-level security and data separation in BYOD environments.

- Leading Deployment: On-Premises leads with over 40% share in 2026, valued at more than US$ 13.5 Bn, supported by strong enterprise demand for data control, regulatory compliance, and internal governance. Cloud/SaaS is the fastest-growing due to scalability, lower upfront costs, and seamless support for hybrid and remote work environments.

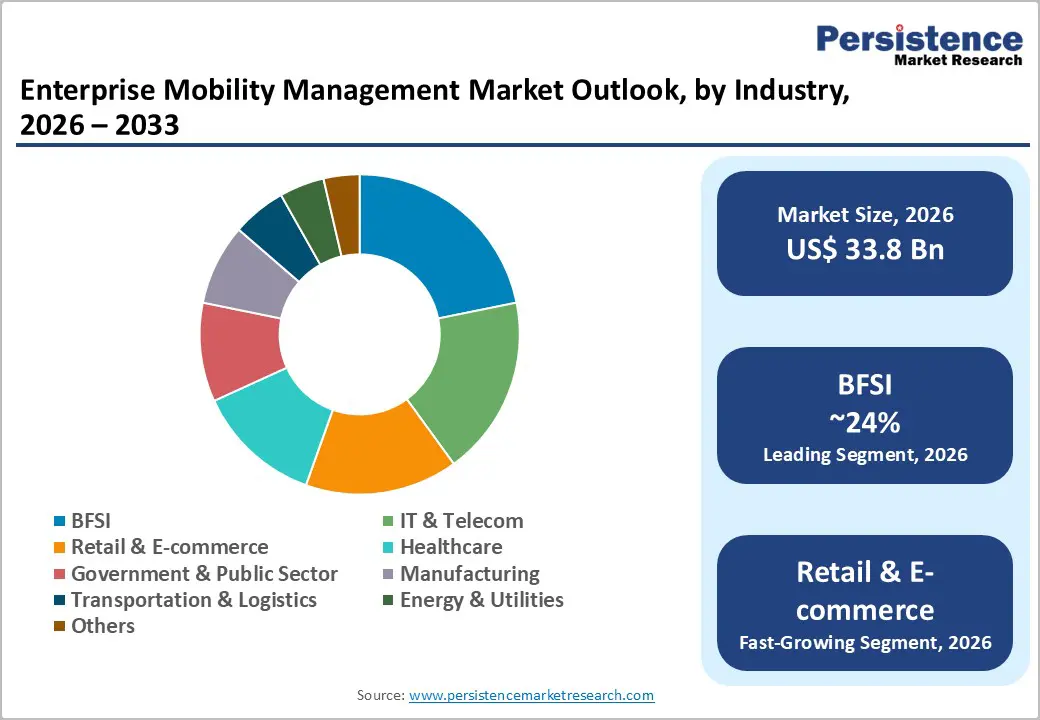

- Leading Vertical: BFSI holds the largest market share at over 24% in 2026, valued at more than US$ 8.1 Bn, driven by stringent compliance requirements and the need to secure high-value financial data. Retail & E-commerce is the fastest-growing, fueled by mobile-driven operations, omnichannel strategies, and rising digital customer engagement.

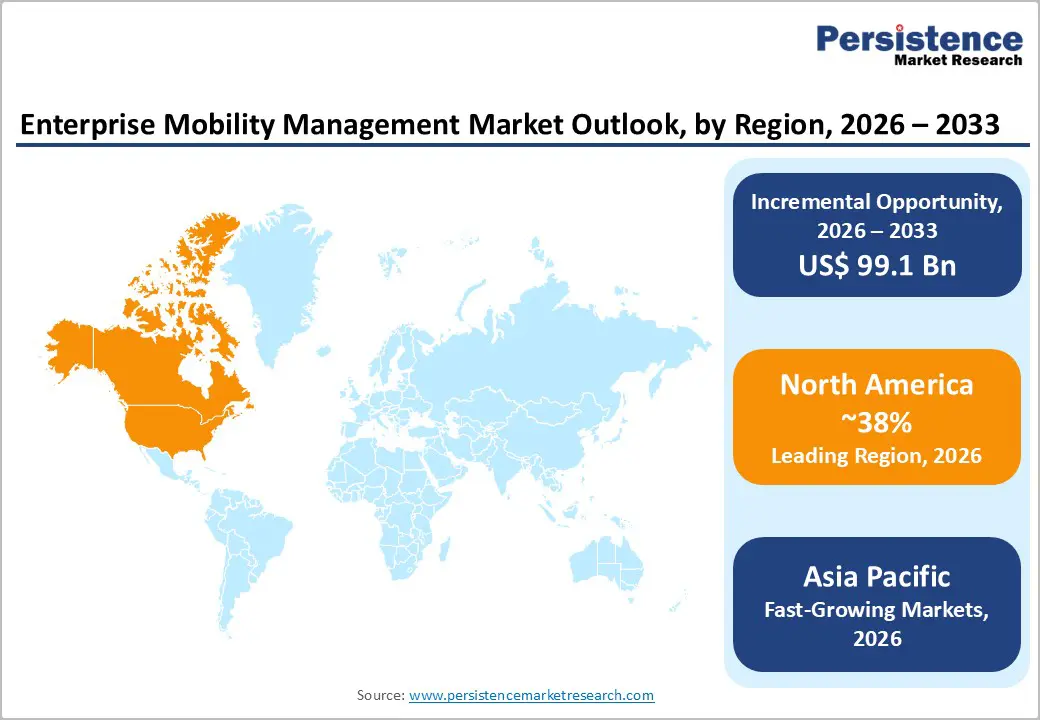

- Leading Region: North America leads with over 38% share in 2026, valued at US$ 12.8 Bn, supported by advanced IT infrastructure, early cloud adoption, and strong regulatory frameworks. Asia Pacific is the fastest-growing region with a CAGR of 25.9%, driven by rapid digitalization, increasing smartphone penetration, and expanding adoption of cloud-based enterprise solutions.

| Key Insights | Details |

|---|---|

|

Enterprise Mobility Management Market Size (2026E) |

US$33.8 Bn |

|

Market Value Forecast (2033F) |

US$132.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

21.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

15.4% |

Market Dynamics

Driver - Explosive Proliferation of Mobile Devices and BYOD Culture

The rapid shift to hybrid and remote work has made mobile device support a foundational part of enterprise IT strategies. Over 95% of organizations now allow some form of personal device use for work, and roughly 82% have formal BYOD policies in place, reflecting how mainstream BYOD has become. Smartphones account for over 50% of total BYOD device usage, emphasizing their dominance as employee endpoints. This widespread reliance on personal devices has driven investment in unified endpoint and mobile device management solutions to provide secure access, remote wipe, policy enforcement, and corporate data containerization. As workplace mobility becomes the standard rather than an exception, EMM platforms are increasingly seen as essential infrastructure rather than optional tools.

Surging Cybersecurity Threats on Mobile Endpoints

Rising volumes of cyber threats targeting endpoints, including mobile devices, are a major catalyst for EMM adoption. According to endpoint security research, around 90% of cyberattacks and 70% of data breaches originate from compromised endpoint devices, underscoring the danger unmanaged devices pose to enterprise environments. Many organizations report significant portions of their endpoints remain unmanaged, creating blind spots that attackers exploit. Mobile devices, in particular, are heavily targeted by phishing and malware campaigns, making robust management and threat-detection capabilities vital. These threat dynamics are prompting enterprises to deploy EMM platforms with integrated security controls such as real-time compliance checks and automated remediation to protect corporate resources.

Restraint - High Integration Complexity and Legacy System Incompatibility

Enterprise Mobility Management (EMM) adoption faces a technical challenge: integrating modern mobility platforms with existing enterprise infrastructure, especially legacy ERP and operational systems that lack standardized APIs for seamless connectivity. Enterprises with diverse device types and platforms often face extended deployment cycles and increased integration costs due to the need for custom adapters or middleware. As organizations continue to manage a growing number of mobile endpoints, notably with formal BYOD programs present in over 80% of organizations, ensuring consistent policy enforcement across heterogeneous devices increases architectural complexity and reduces IT agility.

Employee Privacy Concerns and Cultural Resistance

Privacy and employee acceptance remain significant restraints to EMM and BYOD adoption, particularly when personal devices are subject to corporate monitoring or controls. Studies on mobile security risks show that a substantial proportion of organizations report vulnerabilities in mobile devices and applications, underscoring why IT leaders remain cautious about corporate visibility into employee-owned endpoints. Broader workforce studies, such as the (ISC)² Cybersecurity Workforce Study, reveal persistent talent shortages and skills gaps in cybersecurity teams globally, with over 90% of cybersecurity teams reporting one or more skills gaps that hamper the effective implementation of mobility security best practices and reinforce cultural resistance to stricter device controls.

Opportunity - Expansion of Unified Endpoint Management and AI-Driven Security

Enterprises increasingly want a single control plane for smartphones, tablets, laptops, and IoT devices, allowing consistent policy orchestration and streamlined administration. Vendors that extend their platforms with analytics, machine learning-based anomaly detection, and automated remediation can differentiate strongly, as security teams struggle to keep pace with sophisticated mobile malware and phishing campaigns. As more organizations modernize device fleets and consolidate tools, there is substantial growth potential for solutions that integrate mobility, endpoint security, identity, and configuration management into cohesive, cloud-delivered offerings.

Industry-Specific, Compliance-Ready Mobility Solutions

Delivering verticalized EMM solutions tailored to sectors with strict regulatory and operational requirements. For example, in healthcare, providers need HIPAA-compliant mobile access to electronic health records and secure messaging between clinicians, while BFSI institutions must safeguard financial data and maintain audit-ready logs for regulators. Government and public sector organizations also demand sovereign cloud options, high-assurance encryption, and support for specialized devices. Vendors that build industry-specific templates, pre-configured policies, and integrations with core vertical applications accelerate deployment and reduce compliance risk for customers, positioning themselves for outsized growth as mobility matures in these regulated domains.

Category-wise Analysis

Component Insights

Mobile Device Management (MDM) dominates the market, capturing more than 37% market share of solutions in 2026 with a value exceeding US$ 9 Bn. This dominance is driven by enterprises’ critical need to secure and manage a growing fleet of corporate and personal devices. MDM solutions provide centralized control over device configuration, security policies, and compliance monitoring, which is essential in hybrid work environments. Organizations are prioritizing data protection, remote device management, and threat prevention, making MDM a foundational EMM component. Integration with existing IT systems and productivity tools further strengthens its adoption.

Mobile Application Management (MAM) is expected to grow rapidly as enterprises increasingly rely on mobile apps for business processes. It addresses the need to control app access, secure sensitive data, and enforce compliance without managing the entire device. With the rise of BYOD and remote work policies, businesses are focusing on app-level security, containerization, and app distribution to reduce risk. The growing use of SaaS applications and cloud-based workflows also fuels adoption. Organizations value MAM for its ability to separate personal and corporate app environments while maintaining data integrity.

Deployment Insights

On-Premises holds over 40% market share in 2026, with a value exceeding US$ 13.5 Bn, due to enterprise requirements for data control, security, and regulatory compliance. Many large organizations prefer on-premises deployments to maintain full control over sensitive information and to ensure compliance with industry-specific regulations. It offers customizable policies, integration with internal IT infrastructure, and reduced dependency on third-party providers. They are particularly favored by sectors like BFSI and government, where data sovereignty and audit readiness are critical. This deployment method supports enterprises with strict internal governance needs.

Cloud / SaaS is expected to grow rapidly due to its scalability, flexibility, and lower upfront costs. Organizations adopting hybrid or remote work models benefit from easy deployment, automatic updates, and global accessibility. It reduces IT management overhead while enabling quick onboarding of new devices and users. The ability to integrate with cloud productivity suites and SaaS applications makes this model attractive for fast-growing businesses. The trend towards AI-driven analytics and cloud-based security monitoring further accelerates adoption.

Industry Insights

BFSI commands the largest market share at over 24% in 2026, with a value exceeding US$ 8.1 Bn, due to stringent regulatory requirements and the need to safeguard financial data. Banks, insurance companies, and fintech firms require audit-ready logs, secure messaging, and encrypted mobile access for sensitive operations. High-value transactions, compliance mandates such as data protection regulations, and risk mitigation strategies make EMM critical in the BFSI sector. Organizations also rely on EMM to provide seamless access while minimizing security breaches.

Retail & E-commerce is expected to grow at the highest rate due to rapid digitization, mobile-driven sales, and customer engagement needs. Mobile devices are integral for inventory management, point-of-sale operations, and personalized marketing campaigns. It enables secure access to applications, protects sensitive customer data, and supports seamless operational workflows. The rise of omnichannel retail strategies and mobile workforce management increases the reliance on cloud-based and mobile-centric management platforms. Retailers also prioritize flexible deployment models that support fast expansion and seasonal fluctuations.

Regional Insights

North America Enterprise Mobility Management Market Trends

North America holds over 38% share in 2026, reaching US$ 12.8 Bn value, driven by its mature IT infrastructure and early cloud adoption. The United States alone represents over 75% of the regional market, with enterprises deploying cloud-based EMM solutions to manage laptops, tablets, and smartphones in hybrid work environments. Compliance frameworks like HIPAA, CCPA, and SOX continue to sustain strong demand, reinforced by the U.S. National Cybersecurity Strategy's promotion of endpoint security investments. Leading vendors, including Microsoft Corporation, IBM Corporation, and Cisco Systems, Inc., continuously advance unified endpoint management technologies. Enterprises are steadily investing in securing an increasingly mobile-first workforce, reflecting sustained market momentum.

Asia Pacific Enterprise Mobility Management Market Trends

Asia Pacific is expected to grow at a significant rate with a CAGR of 25.9%, underpinned by rapid digitalization, expanding mobile broadband coverage, and increasing smartphone adoption. Enterprises in these markets are leveraging mobility to support distributed workforces, digitally enabled manufacturing operations, and data-driven customer engagement, creating strong demand for scalable and cost-effective EMM solutions. In countries such as India and Indonesia, the surge in small and mid-sized businesses adopting cloud-based collaboration and productivity tools further drives the adoption of cloud-delivered mobility management. Japan and South Korea, with advanced manufacturing and technology sectors, are focusing on integrating mobility with industrial IoT and smart factory initiatives, requiring tight security and device management across operational and IT environments.

Europe Enterprise Mobility Management Market Trends

Europe is expected to hold more than 26% share by 2026, with growth anchored by stringent data protection regulations such as GDPR, which mandate secure mobile endpoint management. Germany leads the region, with accelerated EMM adoption in manufacturing and financial services, while the EU Cyber Resilience Act (to be implemented by 2027) drives modernization of connected devices. The UK, France, and Spain, where hybrid work adoption and cloud investments are accelerating platform deployment. Vendors like VMware, with its Workspace ONE refresh featuring AI-driven compliance enforcement, exemplify solutions balancing GDPR requirements with operational efficiency. European enterprises are adopting EMM to ensure regulatory compliance while enabling agile, distributed operations.

Competitive Landscape

The enterprise mobility management market is moderately concentrated, with a group of large technology vendors holding a significant share alongside a long tail of specialized and regional providers. Market leaders differentiate themselves through the breadth of platform capabilities, deep integration with operating systems and productivity suites, and strong security and compliance features. Vendors are expanding unified endpoint management offerings, embedding zero-trust principles, and leveraging AI for threat detection and automation.

Key Industry Developments

- In September 2025, BlackBerry Limited announced that its BlackBerry Unified Endpoint Management is the first MDM solution certified by the German Federal Office for Information Security (BSI) for securing government iOS and Samsung Knox devices. The certification confirms compliance with high Common Criteria assurance standards, strengthening secure mobile data and communication capabilities.

Companies Covered in Enterprise Mobility Management Market

- Microsoft Corporation

- VMware, Inc.

- IBM Corporation

- Citrix Systems

- Ivanti

- BlackBerry

- Cisco Systems, Inc.

- SAP SE

- Broadcom, Inc.

- Zoho Corporation Pvt. Ltd.

- Sophos

- Matrix42

- Others

Frequently Asked Questions

The global market is projected to be valued at US$33.8 Bn in 2026.

The rising need to securely manage mobile devices, applications, and data across distributed workforces, and growing cybersecurity threats are key driver of the market. drivers

The market is expected to witness a CAGR of 21.6% from 2026 to 2033.

Integration with advanced technologies like AI and zero-trust security is creating strong growth opportunities.

Microsoft Corporation, VMware, Inc., IBM Corporation, Citrix Systems, Ivanti, BlackBerry, Cisco Systems, Inc., SAP SE, Broadcom, Inc. are among the leading key players.