- Home Care & Utilities

- Enameled Cookware Market

Enameled Cookware Market Size, Share, and Growth Forecast 2026 - 2033

Enameled cookware Market by Product Type (Ovens, Pots, Pans, Bakery Tray, Others), by Application (Residential, Commercial), by Distribution Channel (Online, Offline), by Regional Analysis, 2026 - 2033

Enameled Cookware Market Size and Trend Analysis

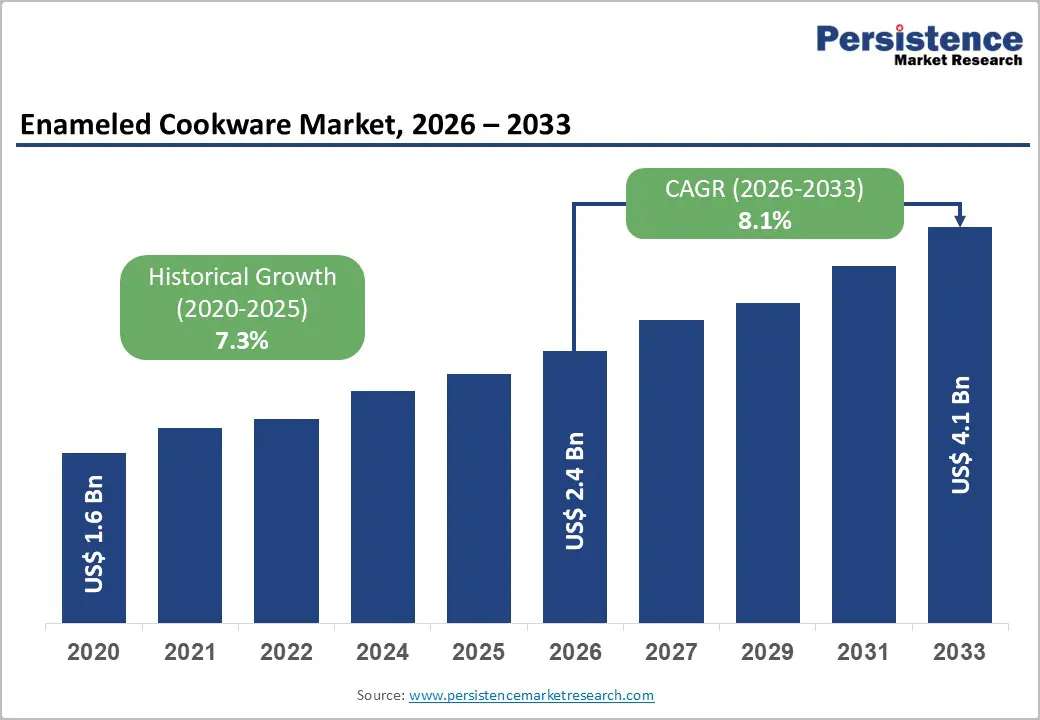

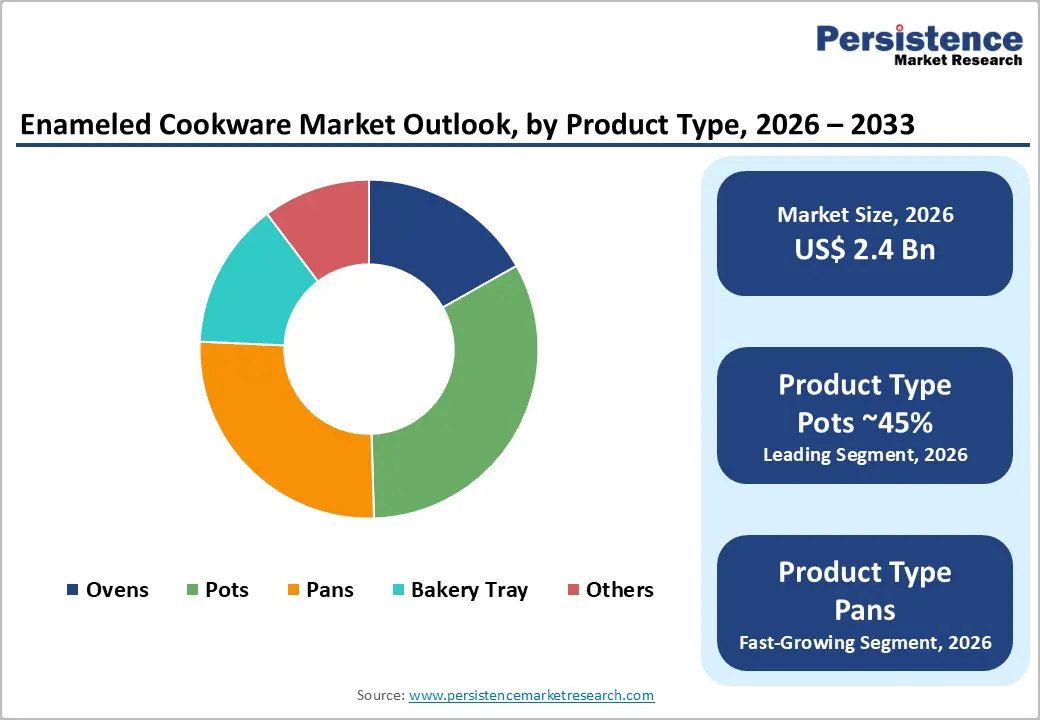

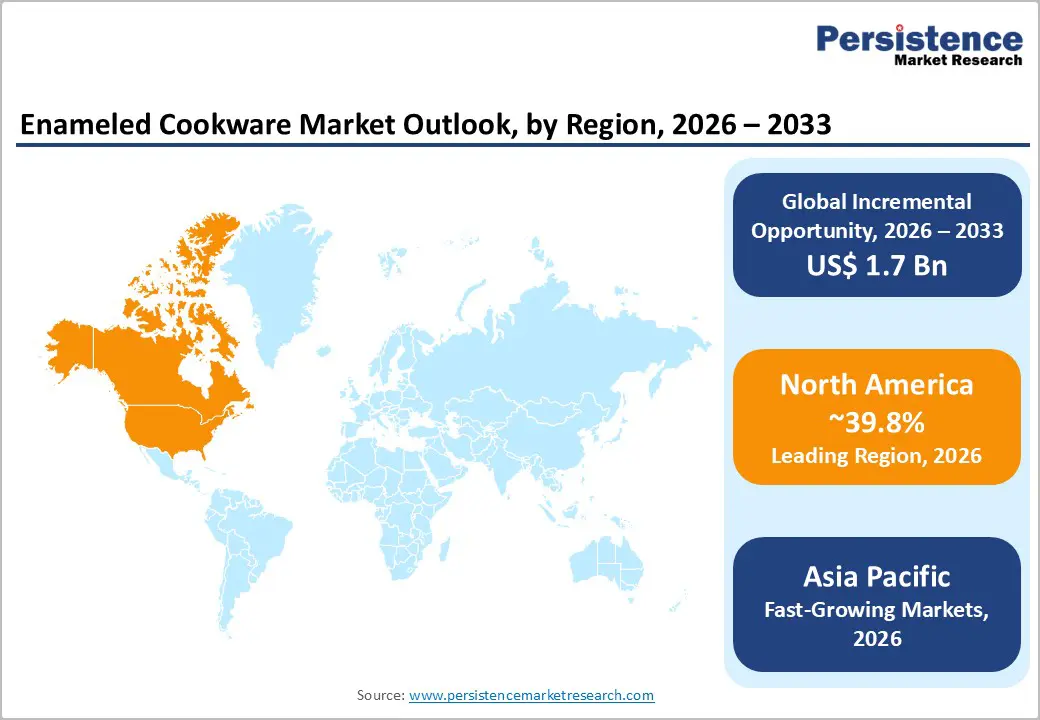

The global enameled cookware market size is likely to be valued at US$ 2.4 billion in 2026 and is expected to reach US$ 4.1 billion by 2033, growing at a CAGR of 8.1% during the forecast period from 2026 to 2033.

Rising consumer interest in premium, sustainable, and health-conscious cookware solutions remains the primary catalyst for market expansion. Sustained growth in residential home cooking trends, along with increasing awareness of the non-reactive properties of enameled cookware, continues to drive demand across both developed and developing markets. Moreover, innovations in enamel coating technologies and the expansion of e-commerce distribution channels are supporting a broader market reach and revenue growth.

Key Market Highlights

- Leading Region: North America holds the largest share of the enameled cookware market at approximately 39.8%, driven by affluent consumers, premium brand demand, and work-from-home trends.

- Fastest Growing Region: Asia Pacific, accounting for 32% of the global market, is the fastest-growing region, driven by rapid urbanization, rising disposable incomes, expanding middle-class populations, and increasing adoption of premium enameled cookware across residential and commercial segments.

- Dominant Segment: Pots and Dutch ovens lead the product category with ~45% market share, driven by versatility, superior heat retention, and multi-functional cooking applications.

- Fastest-Growing Segment: Online retail channels, which represent 38% of overall distribution, are growing at a ~9% CAGR, outpacing offline channels due to convenience, competitive pricing, and same-day delivery.

- Key Market Opportunity: E-commerce growth and emerging market penetration in Asia Pacific and Latin America offer substantial potential for the adoption of premium enameled cookware.

| Key Insights | Details |

|---|---|

|

Enameled Cookware Market Size (2026E) |

US$ 2.4 Billion |

|

Market Value Forecast (2033F) |

US$ 4.1 Billion |

|

Projected Growth CAGR (2026-2033) |

8.1% |

|

Historical Market Growth (2020-2025) |

7.3% |

Market Dynamics

Market Growth Drivers

Rising Home Cooking Adoption and Increasing Consumer Focus on Health, Safety, and Ingredient Transparency

Consumer cooking habits have shifted notably, with a growing share of households in developed economies reporting increased home cooking over the past year. This trend is strongly linked to rising health awareness, interest in culinary experimentation, and the desire to manage ingredient quality and nutritional intake. As consumers prioritize safer cooking environments, durable cookware has become an essential kitchen investment rather than a discretionary purchase.

Enameled cookware benefits from this shift due to its PFAS-free, non-reactive surface, which aligns with toxin-free cooking preferences. Social media influence, celebrity chef endorsements, and cooking-focused digital content have amplified awareness of the advantages of premium cookware. Consumers increasingly favor products that combine performance, durability, and visual appeal, supporting sustained demand across residential segments globally.

Advancements in Enamel Coating Technologies and Expanding Product Innovation Strategies

Manufacturers are actively investing in advanced enamel coating technologies to improve durability, chip resistance, and heat retention, extending overall product lifespan. Innovations such as vibrant color palettes, enhanced thermal performance, and induction compatibility are helping brands address diverse cooking habits and modern kitchen requirements. These improvements strengthen product differentiation and encourage repeat purchases in competitive markets.

The introduction of lightweight enameled cookware variants has reduced traditional usability barriers associated with cast-iron products. Expanded portfolios now include pots, pans, Dutch ovens, baking trays, and specialty cookware, allowing brands to target multiple price tiers. Ergonomic handles, precision-fit lids, and refined design elements further enhance usability and consumer satisfaction.

Market Restraints

High Manufacturing Costs, Energy-Intensive Production Processes, and Limited Scalability of Enamel Cookware Manufacturing

The production of enameled cookware involves complex, multi-stage processes including repeated coating applications, high-temperature kiln firing, detailed quality inspections, and surface finishing. These steps significantly increase raw material consumption, energy usage, and labor costs compared to conventional cookware manufacturing. As a result, higher production expenses are reflected in final retail prices, limiting affordability in price-sensitive and emerging markets.

Furthermore, the requirement for specialized technical expertise and precision-controlled facilities restricts rapid capacity expansion. Limited access to advanced coating infrastructure and skilled labor creates scalability challenges and supply chain vulnerabilities, particularly in regions with developing kitchenware manufacturing ecosystems, thereby constraining broader market growth potential.

Durability-Related Performance Concerns and Intensifying Competition from Alternative Cookware Materials

Despite ongoing product enhancements, enamel chipping and surface degradation remain persistent concerns impacting long-term consumer satisfaction and brand trust. Factors such as improper handling, thermal shock, and extended usage can accelerate coating wear, increasing replacement frequency and generating unfavorable consumer feedback. These issues pose challenges for maintaining consistent brand perception in competitive markets.

Enameled cookware faces strong competition from ceramic-coated nonstick cookware products, stainless steel cookware, and other non-toxic alternatives that offer perceived functional parity at lower price points. Regulatory initiatives restricting PFAS-containing cookware formulations further compel manufacturers to undertake costly reformulation and supply chain adjustments to sustain market access.

Market Opportunities

Digital Consumer Engagement Channels

Online retail channels are emerging as the fastest-growing distribution avenue for enameled cookware, supported by rising digital adoption and improving logistics infrastructure. E-commerce platforms allow consumers to compare products, access verified reviews, and benefit from faster delivery options, significantly shortening purchase decision cycles. Direct-to-consumer brands are leveraging lower distribution costs to offer competitively priced products, bundled accessories, and exclusive designs without traditional retail markups.

Social commerce, influencer marketing, and live product demonstrations further enhance consumer trust and conversion rates. Omnichannel strategies integrating online ordering with local store pickup are gaining traction. Expanding mobile internet penetration in emerging economies is enabling rural and semi-urban consumers to access premium cookware brands, widening the overall addressable market.

Strong Growth Potential Across Emerging Economies and Expanding Middle-Class Consumer Base

Emerging markets, particularly in the Asia Pacific, offer significant opportunities for the enameled cookware industry due to rapid urbanization, rising disposable incomes, and evolving lifestyle preferences. Countries such as China, India, and ASEAN nations are witnessing increased demand for premium, durable, and visually appealing kitchenware as middle-class households prioritize long-term value and cooking quality.

The expansion of hospitality, food service, and commercial kitchen segments in developing economies is further driving demand for high-performance cookware. Exposure to global culinary trends and the influence of celebrity chefs is driving aspirational demand for premium brands. Strategic collaborations between international manufacturers and regional distributors are accelerating market penetration and revenue growth across underserved regions.

Category-wise Insights

Product Type Analysis

Pots and Dutch ovens represent the leading product category in the enameled cookware market, accounting for approximately 45% of total demand. Their dominance is driven by versatility, superior heat retention, and suitability for multiple cooking methods such as braising, baking, roasting, and slow cooking. Enameled cast-iron Dutch ovens are especially favored for their induction-compatibility, oven safety, and long service life, appealing to both residential users and professional cooks.

Secondary categories, including frying pans, baking trays, grill pans, and specialty cookware, are emerging as the fastest-growing segments. Product innovation focused on ergonomic designs, lighter-weight constructions, and category-specific performance features is accelerating adoption. Rising consumer interest in diversified cooking styles and specialized kitchen tools continues to support steady expansion across these non-core product segments.

Application Analysis

The residential segment dominates the enameled cookware market, accounting for approximately 62% of the market, supported by consumer focus on kitchen aesthetics, cooking performance, and long-term durability. Home cooks increasingly view premium cookware as both functional tools and design elements, reinforcing higher-value purchasing decisions. Growth in home renovation activity and lifestyle shifts toward home-centered living further strengthen residential demand.

Commercial applications, including restaurants, hotels, catering services, and institutional kitchens, represent the fastest-growing segment. Expansion is supported by recovery in hospitality, rising premium dining concepts, and food service growth in emerging markets. Commercial buyers emphasize durability, thermal efficiency, and lifecycle cost efficiency, driving increasing adoption of high-performance enameled cookware in professional kitchen environments.

Distribution Channel Analysis

Offline retail channels continue to lead the enameled cookware market, accounting for approximately 62% of total sales. Specialty kitchen stores, department stores, and brand-owned outlets remain critical for premium cookware purchases, as consumers value physical product inspection, weight assessment, and in-person guidance when making high-value buying decisions. Hypermarkets also contribute through bundled offerings and convenience-driven purchases.

Online retail is the fastest-growing distribution channel, expanding at a CAGR close to 9%. E-commerce platforms offer broader brand access, transparent price comparisons, and verified consumer reviews, enhancing buyer confidence. Direct-to-consumer models and omnichannel strategies, including click-and-collect and in-store fulfillment, are further improving accessibility and accelerating digital channel adoption globally.

Regional Insights

North America Enameled Cookware Trends

The North American market, led by the United States, accounts for approximately 39.8% of the global enameled cookware market, driven by a mature, affluent consumer base with sustained demand for premium cookware. Work-from-home trends and increased time spent at home have led 68% of households to undertake kitchen remodels and cookware upgrades. Heritage brands like Le Creuset and Lodge Manufacturing dominate through brand recognition, quality, and established retail networks. Innovation-focused players such as FINEX Cast Iron Cookware Co. and Borough Furnace capture niche premium segments with superior craftsmanship and design aesthetics.

Canada and Mexico serve as secondary markets with growing middle-class populations and expanding e-commerce adoption. Rising awareness of health-conscious and eco-friendly cookware drives premium enameled cookware uptake. Strategic partnerships between global manufacturers and regional retailers, coupled with efficient logistics and digital payment systems, further support market expansion and accessibility across North America.

Europe Enameled Cookware Trends

Europe is a key region for enameled cookware, supported by deep culinary traditions, brand heritage, and aesthetic design preferences. Germany, France, the UK, and Spain are primary contributors. France is the fastest-growing market in Europe, supported by heritage brands like Le Creuset and Staub. Consumers increasingly demand eco-friendly, non-toxic, and sustainable cookware solutions that align with stringent EU regulatory standards.

European buyers perceive premium cookware as long-term investments and kitchen décor, supporting higher price points. The region benefits from a mature retail ecosystem combining specialty boutiques and expanding e-commerce platforms. Manufacturers adhering to advanced production standards and sustainable supply chains gain competitive advantages. The market is expected to grow at a CAGR of 9.2% over the forecast period, driven by health-conscious consumption and the adoption of premium products.

Asia Pacific Enameled Cookware Trends

The Asia Pacific market, accounting for approximately 32% of the global enameled cookware industry, exhibits the highest growth potential. China and India are the primary growth engines, driven by urbanization, rising disposable incomes, and the expansion of the middle class. Consumers are increasingly drawn to premium, durable, and visually appealing cookware for health-conscious and aesthetically driven cooking practices. SUPOR, a leading Chinese manufacturer, holds a significant regional share, complemented by international brands like Le Creuset, Tramontina, and Cuisinart expanding through local partnerships.

E-commerce adoption is robust, particularly in urban centers, with digital platforms gradually reaching rural communities via mobile internet penetration. The expanding hospitality and foodservice sector, including hotels, restaurants, and catering operations, further drives demand for commercial cookware. Competitive manufacturing advantages, including lower labor costs and technological capabilities, enable regional players to compete on both innovation and pricing, accelerating overall market growth in the Asia Pacific.

Competitive Landscape

The enameled cookware market exhibits a moderately fragmented structure, with leadership concentrated among heritage brands and emerging niche players targeting premium segments. Established manufacturers leverage brand heritage, consistent quality, and wide distribution networks to maintain market dominance. Differentiation strategies focus on craftsmanship, design innovation, and sustainability credentials, supporting premium pricing and fostering strong customer loyalty across diverse demographic groups.

Emerging and mid-tier competitors are gaining traction through superior design aesthetics, artisanal manufacturing, and effective digital marketing targeting younger consumers. R&D investments emphasize chip-resistant enamel, lightweight products, induction compatibility, and expanded color options. Strategic initiatives include geographic expansion, product diversification, direct-to-consumer channels, and influencer collaborations to boost visibility and engagement.

Key Market Developments

- In December 2024, GreenPan, a leading non-toxic cookware innovator, achieved NSF certification for its ceramic nonstick coating technology, strengthening market positioning in the rapidly expanding health-conscious cookware segment and differentiating the brand through third-party safety validation.

- In August 2024, Meyer Corporation, a global cookware manufacturer, unveiled an award-winning product design featuring innovative handle technology and enhanced ergonomic characteristics, winning the 2021 Red Dot Award for product design excellence and reinforcing its commitment to design-driven market differentiation.

- In June 2024, Multiple U.S. states, including Connecticut, Colorado, and Vermont, enacted legislation restricting PFAS chemical use in cookware products effective 2026, catalyzing industry-wide reformulation initiatives and creating market opportunities for manufacturers offering certified PFAS-free enameled cookware alternatives.

Companies Covered in Enameled Cookware Market

- Le Creuset

- Staub

- Lodge Manufacturing

- Tramontina

- Cuisinart

- Emile Henry

- Martha Stewart Collection

- Great Jones

- Rachael Ray

- Victoria Cookware

- FINEX Cast Iron Cookware Co.

- GreenPan

- Meyer Corporation

- Borough Furnace

- SUPOR

Frequently Asked Questions

The global enameled cookware market is expected to reach US$ 4.1 Billion by 2033, growing at a CAGR of 8.1% from 2026 to 2033.

Rising home cooking trends (58% of households), health-conscious consumers preferring PFAS-free non-reactive cookware, aesthetic and colorful designs, durability, and social media influence are key growth drivers.

Pots and Dutch ovens lead with ~45% market share, valued for versatility, heat retention, induction compatibility, and multi-functional cooking applications.

North America holds the largest regional share at approximately 39.8%, supported by affluent consumers, premium brand demand, and work-from-home trends.

E-commerce expansion and emerging market penetration in Asia Pacific and Latin America offer significant growth potential for premium cookware brands.