- Specialty & Fine Chemicals

- Elastomers Market

Elastomers Market Size, Share, and Growth Forecast 2026 - 2033

Elastomers Market by Product Type (Thermoset Elastomers, Thermoplastic Elastomers), Process (Injection Molding, Extrusion, Blow Molding, Compression Molding, Transfer Molding, Calendaring), Application (Tires & Tubes, Seals & Gaskets, Hoses & Belts, Adhesives & Sealants, Wire & Cable Insulation, Footwear Components, Medical Products, Others), Industry, and Regional Analysis, 2026 - 2033

Elastomers Market Size and Trend Analysis

The global elastomers market size is expected to be valued at US$ 111.5 billion in 2026 and projected to reach US$ 160.1 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033.

This robust expansion is driven by the convergence of three powerful structural forces: accelerating global vehicle production that demands high-performance elastomers for tires, seals, and vibration damping; a booming construction sector requiring EPDM and silicone-based sealing and waterproofing materials; and the rapid electrification of the automotive fleet, which has elevated demand for specialty thermoplastic elastomers capable of withstanding the unique thermal and chemical environments of battery systems.

According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production reached 93.5 million units in 2023 and has continued to recover toward pre-pandemic peak levels through 2024 - 2025, each vehicle incorporating an average of 70-80 kg of rubber and elastomeric components across tires, weather-strips, hoses, belts, and gaskets. Simultaneously, the global construction industry is forecast to invest over US$ 22 trillion annually by 2030, per Oxford Economics estimates, underpinning sustained structural demand for elastomers in building applications worldwide.

Key Industry Highlights:

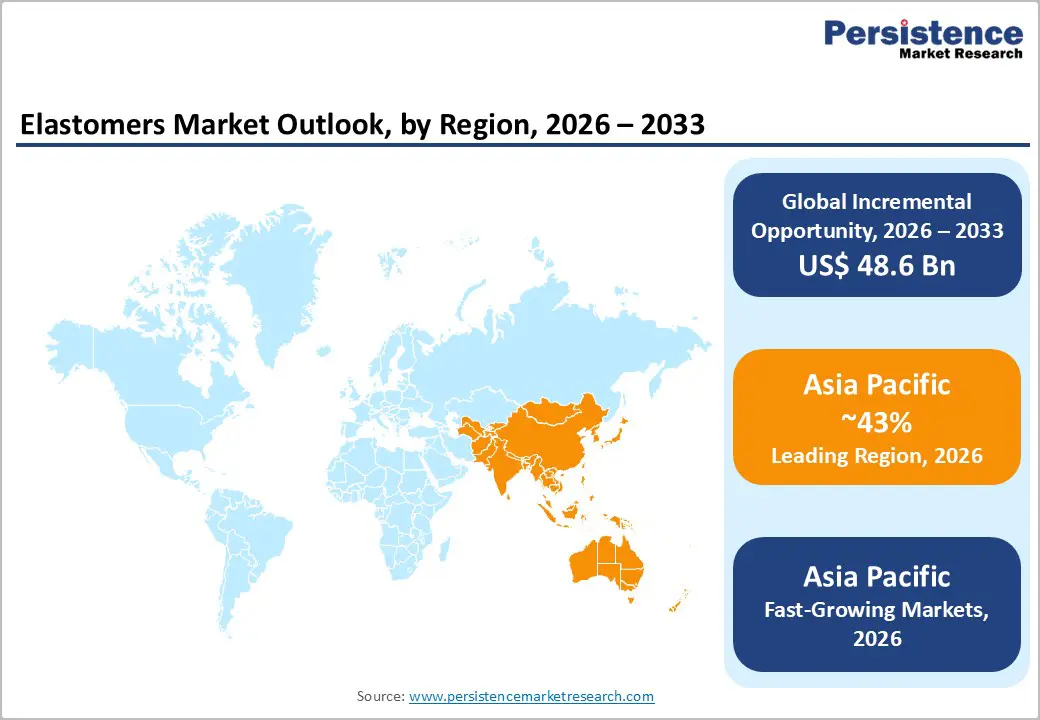

- Leading Region: Asia Pacific leads the global elastomers market with approximately 43% share in 2025, driven by China's position as the world's largest vehicle and EV producer, Southeast Asia's natural rubber plantations, and rapid construction-sector growth across India and ASEAN nations.

- Fastest-Growing Segment: Asia Pacific is also the fastest-growing region at approximately 6.3% CAGR through 2033, propelled by surging EV production requiring specialty EPDM and TPU, expanding infrastructure investment under India's National Infrastructure Pipeline, and growing specialty elastomers capacity across the region.

- Dominant Segment: Automotive and transportation is the dominant end-use segment, accounting for approximately 42% market share in 2025, consuming 70-80 kg of elastomers per vehicle across tires, seals, hoses, and vibration-damping components, supported by OICA-confirmed global vehicle production of 93.5 million units in 2023.

- Fastest Growing Segment: Thermoplastic elastomers are the fastest growing product segment, expanding at approximately 5.35% CAGR through 2033, driven by their recyclability, melt-processability, and premium positioning in EV battery sealing, medical devices, and high-performance consumer electronics applications.

- Key Opportunity: Bio-based and sustainable elastomers represent the most compelling market opportunity, as EU CBAM regulations, OEM sustainability commitments, and growing end-user demand for certified low-carbon materials create a premium-priced niche for ISCC PLUS-certified bio-EPDM, bio-SBR, and recyclable TPE product lines.

| Key Insights | Details |

|---|---|

| Elastomers Market Size (2026E) | US$ 111.5 Billion |

| Market Value Forecast (2033F) | US$ 160.1 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.3% |

| Historical Market Growth (2020 - 2025) | 4.6% CAGR |

DRO Analysis

Drivers - Automotive Sector Expansion and Electrification of Vehicles

The global automotive industry remains the dominant demand engine for the elastomers market, consuming elastomers across tires, seals, gaskets, hoses, belts, and vibration-dampening components. OICA data indicates global vehicle output recovered to 93.5 million units in 2023 and is expected to approach 100 million units annually by 2025-2026, as supply chain normalization and robust demand across Asia Pacific and North America support a full recovery. The accelerating transition to electric vehicles (EVs) is further amplifying elastomer demand for specialized applications. EV battery packs require EPDM-based thermal management gaskets, silicone seals, and TPU encapsulants that can withstand continuous operating temperatures and aggressive coolant chemistries. In 2024, global EV sales surpassed 17 million units per International Energy Agency (IEA) estimates, directly expanding elastomers demand across battery and drivetrain sealing applications, a segment expected to grow at above-market rates through 2033.

Urbanization and Infrastructure Investment Driving Construction Demand

Rapid urbanization in emerging economies is generating unprecedented demand for elastomers in building and construction applications, including EPDM roofing membranes, silicone window sealants, neoprene expansion joints, and TPO waterproofing sheets. According to the United Nations, approximately 68% of the world's population will reside in urban areas by 2050, with the greatest urbanization rates concentrated in Asia, Africa, and Latin America. The U.S. Infrastructure Investment and Jobs Act committed US$ 1.2 trillion to infrastructure through 2030, while India's National Infrastructure Pipeline targets over US$ 1.4 trillion in projects. EPDM's superior ozone, UV, and weather resistance, combined with its long service life of 40-50 years in roofing applications, makes it the material of choice across large-scale construction projects worldwide, representing one of the most durable structural demand pillars for the thermoset elastomers segment.

Restraints - Feedstock Volatility and Petrochemical Supply Chain Disruptions

The elastomers industry is acutely sensitive to feedstock cost volatility, as the majority of synthetic elastomers, including SBR, NBR, and EPDM, are derived from petrochemical monomers such as butadiene, styrene, acrylonitrile, and ethylene. In 2024-2025, Asian spot butadiene prices climbed approximately 67% on the back of cracker outages and supply disruptions, squeezing margins for emulsion-SBR producers and forcing pricing surcharges across the value chain. BASF SE implemented surcharges of 8-10 cents per pound on key diols to maintain margins. Such feedstock instability introduces cost uncertainty for downstream converters and end-users, creating resistance to volume commitments and constraining market growth, particularly among cost-sensitive SMEs in footwear, consumer goods, and construction.

Regulatory Restrictions on Hazardous Substances in Elastomers

Tightening regulatory frameworks around hazardous substances in elastomers is creating significant compliance burdens and reformulation costs for manufacturers. The European Chemicals Agency (ECHA) has progressively restricted polycyclic aromatic hydrocarbons (PAHs) in SBR-based products under the EU REACH Regulation, requiring expensive formulation changes across tire, footwear, and industrial product lines. Similarly, growing regulatory pressure on per- and polyfluoroalkyl substances (PFAS) is impacting the fluoroelastomers segment, as these persistent compounds are targeted for phase-out across the EU, U.S. EPA, and other jurisdictions. Compliance with these evolving standards requires significant R&D investment, increases time-to-market for reformulated grades, and can disrupt established supply chains, tempering growth in premium specialty elastomer segments.

Opportunities - Thermoplastic Elastomers in Electric Vehicles and Lightweight Automotive Design

The global shift toward electric vehicles presents an exceptional growth opportunity for manufacturers of thermoplastic elastomers (TPEs), particularly Thermoplastic Polyurethanes (TPU), Thermoplastic Vulcanizates (TPV), and Thermoplastic Polyolefins (TPO). Unlike conventional thermoset rubbers, TPEs offer melt-processability on standard injection molding and extrusion equipment, design flexibility, and end-of-life recyclability, properties increasingly mandated by OEM sustainability commitments. Thermoplastic elastomers led the elastomers market with approximately 81.56% share in 2024 and are projected to expand at a CAGR of approximately 5.35% through 2030. Each battery electric vehicle (BEV) requires up to 20-30% more elastomeric sealing material per unit than a conventional ICE vehicle, due to battery enclosures, cooling circuit seals, and high-voltage cable insulation. In 2024, Dow Inc. launched bio-based NORDEL REN EPDM via ISCC PLUS-certified mass-balance feedstocks, specifically targeting automotive seals and infrastructure gaskets, signaling the direction of premium innovation in this space.

Bio-Based and Sustainable Elastomers for Green Manufacturing

Rising sustainability mandates from governments, OEMs, and institutional investors are creating a compelling commercial opportunity for bio-based and circular economy elastomers. ARLANXEO has been commercially producing Keltan Eco EPDM with bio-based ethylene sourced from Braskem since 2013, and in August 2025, launched ISCC PLUS-certified Keltan Eco-B and Eco-BC grades in India, offering bio-based EPDM alternatives with identical performance to conventional grades. Asahi Kasei Corporation announced in November 2025 the commercial sale of Asadene BR and Tufdene S-SBR produced via mass-balance methods from plastic waste and biomass for eco-friendly tire applications. With global carbon regulations such as the EU Carbon Border Adjustment Mechanism (CBAM) coming into effect, manufacturers that establish certified low-carbon elastomer product lines are positioned to capture premium-priced, sustainability-linked contracts across automotive, construction, and healthcare sectors through 2033.

Category-wise Analysis

Product Type Insights

Thermoset elastomers dominate the global elastomers market by product type, accounting for approximately 55% market share in 2025. This leadership is rooted in the breadth of thermoset applications and the irreplaceable performance characteristics of key grades. Natural rubber (NR) commands approximately 34% of the tire segment globally due to its unmatched tensile strength and fatigue resistance. Styrene-butadiene rubber (SBR) captured approximately 40.89% of the synthetic rubber market volume in 2025, supported by its cost-effectiveness as a natural rubber substitute in tire treads and footwear soles. EPDM is the fastest-growing thermoset, driven by EV thermal management and construction weatherproofing applications, valued at approximately US$ 5 billion in 2025 and growing at a CAGR of approximately 4.5% through 2033. Thermoplastic elastomers are the fastest-growing product segment overall, leveraging recyclability and processing advantages to displace thermosets in automotive interiors, consumer goods, and electronics applications.

Process Insights

Injection molding is the leading process in the elastomers market, holding approximately 38% market share in 2025. The dominance of injection molding is attributable to its precision, high throughput, and suitability for processing both thermoset and thermoplastic elastomers across the largest end-use segments: automotive, consumer goods, and electrical & electronics. Modern injection molding enables the production of complex, near-net-shape elastomeric components such as seals, gaskets, and vibration-damping mounts with minimal post-processing waste. The automotive sector's global pivot to just-in-time manufacturing further reinforces injection molding's preferred status, as it delivers consistent dimensional tolerances critical for engine seals and battery enclosure components. Extrusion is the fastest-growing process, driven by soaring demand for continuous profiles in wire and cable insulation, weather stripping, and construction sealing, applications that are scaling rapidly with global growth in EV and infrastructure investment.

Application Insights

Tires and tubes represent the leading application in the global elastomers market, commanding approximately 36% market share in 2025. The tire segment is the single largest consumer of both natural rubber and synthetic elastomers globally, as each standard passenger vehicle tire requires approximately 7-8 kg of rubber, and a commercial truck tire may incorporate over 20 kg of rubber compounds. The World Rubber Industry Organization estimates global tire production exceeded 2.3 billion units in 2023, reflecting the scale of elastomer consumption in this segment. High-performance tire grades incorporating solution-polymerized SBR (S-SBR) with functionalized chain ends are gaining share, driven by EV manufacturers' requirements for low rolling resistance and extended mileage. Seals and gaskets is the fastest-growing application through 2033, underpinned by the dramatic expansion of EV battery systems, industrial equipment, and healthcare device manufacturing, all of which require high-precision elastomeric sealing solutions.

Industry Insights

Automotive and transportation is the dominant end-use industry in the global elastomers market, accounting for approximately 42% market share in 2025. The automotive sector's demand encompasses tires, weather-strips, door seals, engine mounts, cooling system hoses, fuel system components, and increasingly complex EV-specific thermal and electrical management materials. OICA data confirm that global vehicle output reached 93.5 million units in 2023, and each vehicle incorporates 70-80 kg of rubber content on average, across thermoset and thermoplastic elastomers. Thermoset elastomers led the automotive elastomer market with approximately 65.67% market share in 2024. Healthcare and medical is the fastest-growing end-use industry through 2033, driven by surging demand for medical-grade silicone, polyisoprene, and TPU in gloves, catheters, drug delivery devices, and wearable health monitoring equipment, a segment commanding significant price premiums over commodity grades.

Regional Insights

North America Elastomers Market Trends and Insights

North America is a critical innovation and technology hub in the global elastomers market, with the United States anchoring demand from its large automotive OEM and tier-1 supplier base, robust construction activity, and rapidly expanding EV manufacturing ecosystem. The U.S. Inflation Reduction Act (IRA) and CHIPS and Science Act are channeling hundreds of billions in manufacturing investment into the U.S., each new facility incorporating elastomers in sealing, insulation, and vibration management applications. The U.S. EPA's evolving PFAS restrictions are simultaneously spurring intensive R&D into fluoroelastomer alternatives, driving innovation across specialty seal and gasket applications.

In September 2025, Kumho Petrochemical secured US$ 200 million to build a 40 ktpa solution-SBR line targeting Q3 2027 start-up, reinforcing North America’s position as a destination for elastomer capacity expansion. North America also leads globally in bio-based elastomer development; Bridgestone received a US$5 million U.S. Department of Energy grant to develop a 10 ktpa bio-butadiene demonstration plant in Tennessee, targeting a 2027 start-up and signaling a strategic shift toward securing renewable feedstock supply.

Europe Elastomers Market Trends and Insights

Europe is the second-largest regional elastomers market, with Germany, the United Kingdom, France, and Spain forming the demand core. Germany's automotive industry, home to Volkswagen, BMW, Mercedes-Benz, and major tier-1 suppliers, remains Europe's primary consumer of elastomers, absorbing significant volumes of EPDM, NBR, and TPE for sealing, powertrain, and EV applications. The EU's REACH regulation and the EU Green Deal are dual regulatory forces reshaping elastomer product development, accelerating the transition toward bio-based, PFAS-free, and recyclable grades. In July 2024, Dow Inc. introduced NORDEL REN, a bio-EPDM with a 39% lower carbon footprint, targeting automotive seals and construction gaskets in the European market.

The European Commission’s Carbon Border Adjustment Mechanism (CBAM) is further incentivizing domestic elastomer producers to invest in low-carbon production, as imported elastomers from high-emission sources will face carbon cost adjustments. In May 2025, Lanxess AG sold its Urethane Systems business to UBE Corporation for EUR 460 million, completing a strategic refocus toward higher-margin specialty additives and reinforcing the trend toward concentration among European elastomer leaders.

Asia Pacific Elastomers Market Trends and Insights

Asia Pacific is the leading region in the global elastomers market, commanding approximately 43% market share in 2025, anchored by China's dominant rubber processing and automotive manufacturing base. Asia Pacific is also the fastest-growing region, projected to expand at a CAGR of approximately 6.3% between 2026 and 2033, driven by rapid industrialization, infrastructure investment, and EV adoption across China, India, and ASEAN nations.

China is the world’s largest vehicle market, producing over 30 million vehicles annually in 2023-2024, and the global leader in EV manufacturing, with over 9 million new energy vehicles (NEVs) produced domestically in 2023 per the China Association of Automobile Manufacturers (CAAM). Each NEV consumes significant volumes of EPDM, silicone, and TPU for battery thermal management and high-voltage cable insulation, structurally elevating specialty elastomers demand. Southeast Asia’s rubber plantation estates, led by Thailand, Indonesia, and Malaysia, supply approximately 90% of the world’s natural rubber, anchoring the region’s raw material advantage.

India is emerging as a high-growth elastomers market, supported by investments in the National Infrastructure Pipeline and a rapidly expanding domestic automotive sector. In August 2025, ARLANXEO launched Keltan Eco-B and Eco-BC bio-based EPDM grades in India, reflecting growing end-user awareness of sustainability. Japan’s advanced electronics and automotive sectors drive high-value demand for specialty elastomers, with companies such as JSR Corporation, Zeon Corporation, and Kumho Petrochemical investing in next-generation functionalized SBR and specialty TPE grades targeting EV applications across the Asia Pacific region.

Competitive Landscape

The global elastomers market exhibits a moderately fragmented structure, with a mix of multinational chemical companies and regional producers contributing to overall supply. While leading players command significant production capacity, the presence of numerous mid-sized and local manufacturers intensifies competition, particularly in commodity elastomer segments. High capital requirements, technological expertise, and established customer relationships act as entry barriers, though not sufficient to prevent regional capacity additions.

From a strategic perspective, companies are increasingly focusing on portfolio optimization, divesting low-margin commodity assets to prioritize specialty and high-performance elastomers. Investments in bio-based and recycled-content materials are gaining traction to meet evolving regulatory requirements and sustainability commitments from automotive and industrial customers. Additionally, manufacturers are expanding production capacities in Asia Pacific to align with rising demand from electric vehicles and infrastructure sectors. Competitive differentiation is further driven by advanced polymer technologies, global supply chain integration, and long-term contracts, while emerging Asian players are strengthening their position in cost-competitive segments.

Key Developments

- March 2026: Axtra3D launched three new high-performance elastomer materials for the North American market and opened pre-orders for its Axtra workflow, enhancing durability, flexibility, and production efficiency in industrial and additive manufacturing applications.

- August 2025: ARLANXEO launched ISCC PLUS-certified Keltan Eco-B and Eco-BC bio-based EPDM grades in India, offering identical performance to conventional rubbers while meeting automotive OEM and regulatory sustainability requirements in South Asia.

- May 2025: Lanxess AG completed the sale of its Urethane Systems business to UBE Corporation for EUR 460 million, marking a strategic transition toward specialty additives and higher-margin specialty chemicals, completing a multi-year portfolio refocusing program.

Companies Covered in Elastomers Market

- ExxonMobil Corporation

- SABIC

- Dow Inc.

- BASF SE

- Lanxess AG

- Arlanxeo

- Kumho Petrochemical

- LG Chem

- JSR Corporation

- Zeon Corporation

- TSRC Corporation

- Sinopec

- PetroChina Company Limited

- Versalis S.p.A.

- Dynasol Group

- Asahi Kasei Corporation

- Zeon Corporation

- Kraton Corporation

- Celanese Corporation

Frequently Asked Questions

The global elastomers market is valued at US$ 111.5 billion in 2026 and is projected to reach US$ 160.1 billion by 2033 at a CAGR of 5.3%.

Growth is driven by automotive production recovery, rising EV demand, and increasing construction and industrial activities globally.

Asia Pacific leads the market with around 43% share, supported by strong automotive, rubber production, and industrial demand.

The key opportunity lies in bio-based and sustainable elastomers driven by regulatory pressure and OEM sustainability commitments.

Key players include ExxonMobil Corporation, SABIC, Dow Inc., BASF SE, Lanxess AG, Arlanxeo, and others competing on technology and global supply.