- Executive Summary

- Global DNA-based Skin Care Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Challenges

- Key Trends

- Product Lifecycle Analysis

- DNA-based Skin Care Market: Value Chain

- List of Raw Material Supplier

- List of Manufacturers

- List of Distributors

- Profitability Analysis

- Forecast Factors - Relevance and Impact

- Covid-19 Impact Assessment

- PESTLE Analysis

- Porter Five Force’s Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and End User Landscape

- Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- Global Parent Market Overview

- Price Trend Analysis, 2020 - 2033

- Key Highlights

- Key Factors Impacting Product Prices

- Prices By Product Type/Distribution Channel/End User

- Regional Prices and Product Preferences

- Global DNA-based Skin Care Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Market Size and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) Analysis and Forecast

- Historical Market Size Analysis, 2020-2025

- Current Market Size Forecast, 2026-2033

- Global DNA-based Skin Care Market Outlook: Product Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Product Type, 2020 - 2025

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Product Type, 2026 - 2033

- Serums

- Creams

- Others

- Market Attractiveness Analysis: Product Type

- Global DNA-based Skin Care Market Outlook: Distribution Channel

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Distribution Channel, 2020 - 2025

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Distribution Channel, 2026 - 2033

- Offline

- Online

- Market Attractiveness Analysis: Distribution Channel

- Global DNA-based Skin Care Market Outlook: End User

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By End User, 2020 - 2025

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By End User, 2026 - 2033

- Home Users

- Wellness Clinics

- Salons

- Market Attractiveness Analysis: End User

- Key Highlights

- Global DNA-based Skin Care Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Region, 2020 - 2025

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Region, 2026 - 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America DNA-based Skin Care Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Market, 2020 - 2025

- By Country

- By Product Type

- By Distribution Channel

- By End User

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Country, 2026 - 2033

- U.S.

- Canada

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Product Type, 2026 - 2033

- Serums

- Creams

- Others

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Distribution Channel, 2026 - 2033

- Offline

- Online

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By End User, 2026 - 2033

- Home Users

- Wellness Clinics

- Salons

- Market Attractiveness Analysis

- Europe DNA-based Skin Care Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Market, 2020 - 2025

- By Country

- By Product Type

- By Distribution Channel

- By End User

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Country, 2026 - 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Rest of Europe

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Product Type, 2026 - 2033

- Serums

- Creams

- Others

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Distribution Channel, 2026 - 2033

- Offline

- Online

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By End User, 2026 - 2033

- Home Users

- Wellness Clinics

- Salons

- Market Attractiveness Analysis

- East Asia DNA-based Skin Care Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Market, 2020 - 2025

- By Country

- By Product Type

- By Distribution Channel

- By End User

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Country, 2026 - 2033

- China

- Japan

- South Korea

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Product Type, 2026 - 2033

- Serums

- Creams

- Others

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Distribution Channel, 2026 - 2033

- Offline

- Online

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By End User, 2026 - 2033

- Home Users

- Wellness Clinics

- Salons

- Market Attractiveness Analysis

- South Asia & Oceania DNA-based Skin Care Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Market, 2020 - 2025

- By Country

- By Product Type

- By Distribution Channel

- By End User

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Country, 2026 - 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Product Type, 2026 - 2033

- Serums

- Creams

- Others

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Distribution Channel, 2026 - 2033

- Offline

- Online

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By End User, 2026 - 2033

- Home Users

- Wellness Clinics

- Salons

- Market Attractiveness Analysis

- Latin America DNA-based Skin Care Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Market, 2020 - 2025

- By Country

- By Product Type

- By Distribution Channel

- By End User

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Country, 2026 - 2033

- Brazil

- Mexico

- Rest of Latin America

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Product Type, 2026 - 2033

- Serums

- Creams

- Others

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Distribution Channel, 2026 - 2033

- Offline

- Online

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By End User, 2026 - 2033

- Home Users

- Wellness Clinics

- Salons

- Market Attractiveness Analysis

- Middle East & Africa DNA-based Skin Care Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Historical Market Size (US$ Bn) and Volume (Unit) Analysis By Market, 2020 - 2025

- By Country

- By Product Type

- By Distribution Channel

- By End User

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Country, 2026 - 2033

- GCC

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Product Type, 2026 - 2033

- Serums

- Creams

- Others

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By Distribution Channel, 2026 - 2033

- Offline

- Online

- Current Market Size (US$ Bn) and Volume (Unit) Forecast By End User, 2026 - 2033

- Home Users

- Wellness Clinics

- Salons

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Apparent Production Capacity

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- IMAGENE LABS PTE. LTD.

- Overview

- Segments and Products

- Key Financials

- Market Developments

- Market Strategy

- Caligenix, Inc.

- EpigenCare Inc.

- Evergreen Life Ltd.

- The Skin Dna

- SKINSHIFT

- DNA Skin Institute

- Anake

- RGR Pharma Ltd.

- LifeNome Inc.

- ALLÉL

- Genetic Beauty

- SkinDNA

- Priori Skin Care

- La Biosthetique

- Note: List of companies is not exhaustive in nature. It is subject to further augmentation during course of research

- IMAGENE LABS PTE. LTD.

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Beauty & Personal Care

- DNA-based Skin Care Market

DNA-based Skin Care Market Size, Share, and Growth Forecast, 2026 - 2033

DNA-based Skin Care Market by Product Type (Serums, Creams, Others), Distribution Channel (Offline, Online), End-user (Home Users, Wellness Clinics, Salons), and Regional Analysis for 2026 - 2033

DNA-based Skin Care Market Size and Trends Analysis

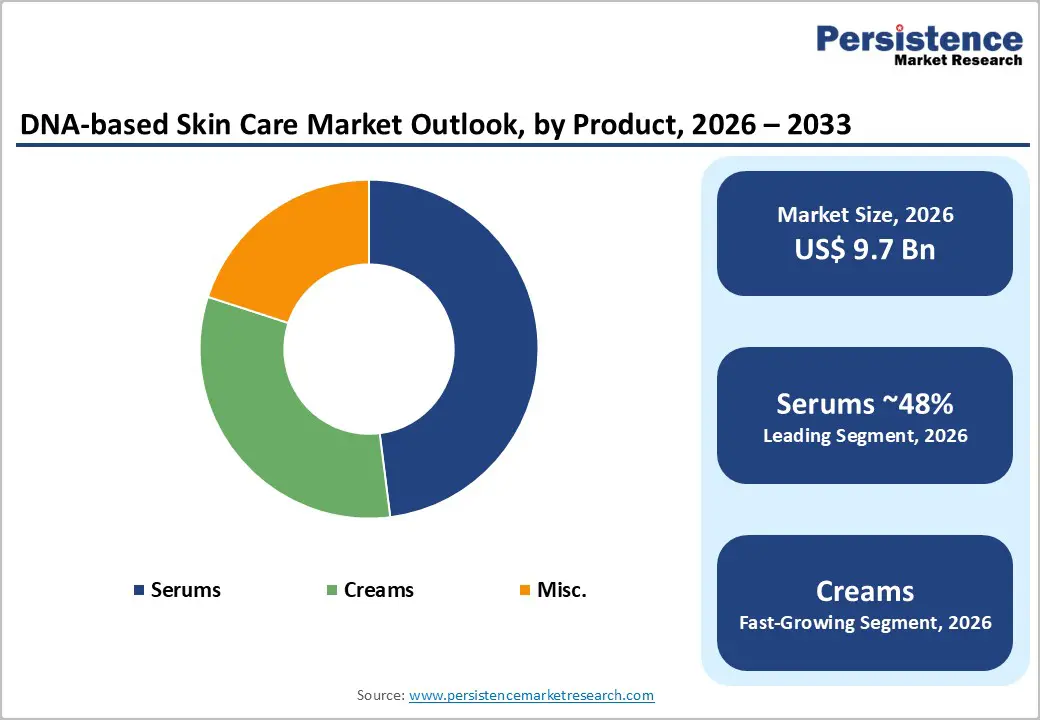

The global DNA-based skin care market size is likely to be valued at US$ 9.7 billion in 2026 and is projected to reach US$ 13.9 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033.

This trajectory builds upon a historical compound annual growth rate of 4.6% recorded from the base valuation of US$ 7.3 Bn, demonstrating the market's sustained commercial momentum. Key demand drivers include the accelerated adoption of consumer genomics platforms, integration of artificial intelligence in product formulation, and the broadening penetration of direct-to-consumer genetic testing kits across developed and emerging markets. The structural convergence of precision medicine principles and mainstream skincare is progressively shifting consumer expectations toward scientifically validated, genetically tailored beauty solutions, creating durable demand across both clinical and home-use settings.

Key Industry Highlights:

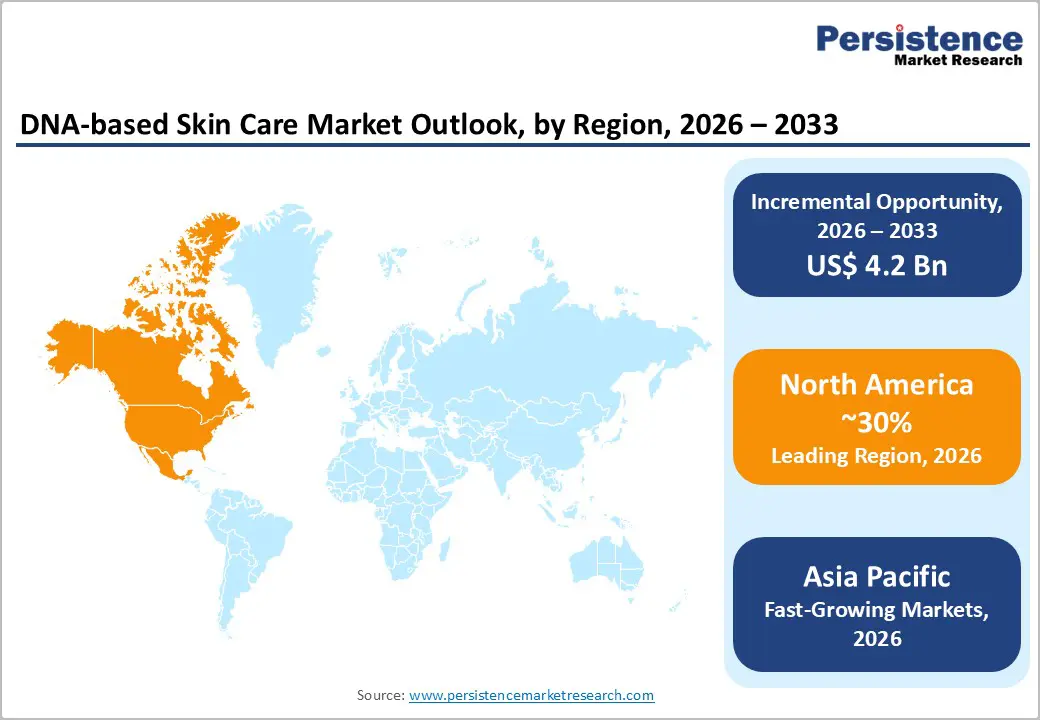

- North America Market Leadership: North America dominates the DNA-based Skin Care Market with approximately 30% share, driven by advanced consumer genomics infrastructure, high beauty spending, and strong direct-to-consumer adoption across the United States.

- Europe Regulatory-Driven Growth: Europe accounts for nearly 25% of the market, supported by stringent cosmetic safety regulations, GDPR-led data protection frameworks, and strong consumer preference for scientifically validated skincare solutions.

- East Asia Innovation Hub: East Asia holds around 23% share, fueled by government-backed genomics investments, strong skincare culture, and rapid innovation in countries such as South Korea, China, and Japan.

- Leading Product: Serums lead the market with approximately 48% share, owing to their high bioactive concentration and effectiveness in delivering targeted, DNA-driven skincare solutions.

- Fastest-Growing Product: Creams represent the fastest-growing product category, driven by their mass-market appeal, ease of use, and growing adoption among first-time users of personalised skincare.

- Dominant End-user: Home users account for about 62% of market demand, reflecting the widespread adoption of at-home DNA testing kits and digital platforms enabling personalised skincare regimens.

| Key Insights | Details |

|---|---|

|

Market DNA-based Skin Care Size (2026E) |

US$ 9.7 Bn |

|

Market Value Forecast (2033F) |

US$ 13.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.6% |

Market Dynamics

Drivers - Global Demographic Shifts and the Demand for Targeted Anti-Aging Solutions in the DNA-based Skin Care Market

Aging population cohorts across developed economies represent a powerful and structurally durable demand catalyst for the DNA-based Skin Care Market. According to the United Nations Department of Economic and Social Affairs, the proportion of the global population aged 60 years or over is projected to exceed 2.1 billion by mid-century, up from approximately 1 billion today.

This demographic transition sharpens demand for scientifically validated, precision-targeted anti-ageing solutions that go beyond conventional cosmetic claims. DNA-based formulations directly address this need by identifying individual genetic predispositions toward collagen degradation, moisture retention deficiencies, and chronological photoaging sensitivity.

The United States Census Bureau reports that all Baby Boomers will reach age 65 or older by 2030, creating the largest cohort of age-conscious consumers in history. This structural demographic pressure, compounded by higher disposable incomes among older consumer segments, reinforces demand for premium, genetically customised skincare solutions across North America, Europe, and East Asia.

Government-Backed Investment in Genomics and Beauty Science Infrastructure Supporting the DNA-based Skin Care Market

Public sector commitment to genomics-led beauty science infrastructure has created a materially enabling environment for the DNA-based Skin Care Market in high-priority regions. South Korea's Ministry of Health and Welfare, through its Innovative Growth Skin Health Basic Technology Development Project, committed KRW 7.1 billion to strengthen foundational cosmetics technologies and skin science capabilities.

The Korean government additionally allocated KRW 3.8 billion to support the construction of the Skin Genome Analysis Centre, a dedicated facility for the systematic collection and analysis of population-level skin genome data. These investments have produced new genetic databases linking hereditary characteristics to observable skin traits across diverse cohorts, equipping manufacturers with scientifically robust foundations for precision formulation.

The European Union's Cosmetics Regulation mandates centralised product notification via the EU Cosmetic Products Notification Portal and requires comprehensive product safety assessments before market entry, institutionalising a transparent and accountable regulatory framework that builds consumer trust and commercial credibility for DNA-informed products.

Restraint - High-Cost Structure and Consumer Affordability Constraints

The premium pricing architecture of DNA-based skincare products remains a significant structural barrier to widespread market penetration. Genetic testing kits, bioinformatics analysis, and bespoke product formulation collectively elevate end-user costs substantially above conventional skincare alternatives.

Consumers in price-sensitive markets and lower-income segments face material affordability constraints. Furthermore, the Federal Trade Commission has raised concerns regarding data security claims made by certain direct-to-consumer genetic testing firms, potentially compounding financial barriers with trust-related hesitation and deterring broader consumer participation.

Regulatory Ambiguity and Cross-Jurisdictional Data Privacy Compliance Complexity.

The absence of a universally standardised regulatory framework for direct-to-consumer genetic testing creates significant operational uncertainty for market participants. As the U.S. National Institutes of Health acknowledges, a substantial proportion of genetic tests reach consumers without independent validation of accuracy claims.

Layered privacy legislation, including GDPR in Europe, the California Consumer Privacy Act, and China's Personal Information Protection Law, imposes divergent data handling obligations across operating jurisdictions. For companies with multi-regional footprints, compliance costs are substantial, and any governance lapse risks financial penalties and reputational damage that can structurally constrain market scalability.

Opportunity- Artificial Intelligence Integration for Hyper-Personalised Genomic Formulation in the DNA-based Skin Care Market

The deployment of artificial intelligence within genomic skincare development represents one of the most commercially consequential opportunities for the DNA-based Skin Care Market. AI algorithms can process large volumes of genetic, environmental, and lifestyle data simultaneously, enabling the development of individualized formulations at materially reduced research timelines.

Multiple leading players are actively deploying AI-powered platforms that generate real-time skincare recommendations calibrated to individual DNA profiles. The synergy between machine learning and genomic databases enables manufacturers to identify novel biomarkers linked to skin conditions such as hyperpigmentation, sensitivity syndromes, and collagen deficiency with unprecedented precision.

This technological convergence is compressing product development cycles, accelerating time-to-market for precision formulations, and creating new consumer engagement touchpoints through digital channels. Companies that invest early in proprietary AI-genomics platforms are positioned to build defensible data moats that translate into durable competitive advantage within the DNA-based Skin Care Market.

Direct-to-Consumer Digital Channels for Penetrating Underpenetrated Geographies in the DNA-based Skin Care Market

Emerging economies across the Asia Pacific, the Middle East, and Latin America represent significant unmet demand for science-backed personalised skincare. As smartphone penetration deepens and e-commerce infrastructure matures in these geographies, companies in the DNA-based Skin Care Market can leverage direct-to-consumer digital models to access first-time buyers of genomic beauty products efficiently, mandates from public-sector and multinational private-sector procurement programs globally.

The proliferation of affordable at-home DNA testing kits is progressively lowering the market entry threshold for new consumer cohorts. Nations with large, digitally active populations and accelerating beauty consciousness present compelling demand corridors for brands with scalable genomic testing and formulation capabilities. Direct-to-consumer platforms eliminate distribution intermediaries, enabling competitive pricing while sustaining healthy margin structures. This dual capability of addressing cost barriers and expanding geographic reach simultaneously creates a strategically important pathway for participant growth within the DNA-based Skin Care Market.

Category-wise Analysis

Product Type Insights

Serums command the dominant position within the product type, accounting for approximately 48% of total product-type revenue. This leadership is directly attributable to the high bioactive concentration that serum formulations deliver, enabling targeted genetic interventions at the cellular level. DNA-informed serums are specifically engineered to address genetic predispositions toward collagen depletion, oxidative stress vulnerability, and UV-induced photodamage sensitivity, making them the preferred product format among scientifically engaged consumers seeking precision-driven outcomes.

The positioning of serums at the premium end of the skincare spectrum is structurally aligned with the value proposition of DNA-based customisation. Consumers investing in genetic profiling and personalised formulations naturally gravitate toward high-performance, concentrated delivery systems.

Creams represent the fastest-growing product type within the DNA-based Skin Care Market, driven by broader demographic accessibility and the familiarity of daily-use cream formats for mainstream consumer segments transitioning from conventional to DNA-informed skincare. Unlike serums, which carry a perception of clinical specialisation, creams occupy a comfortable, habitual format that lowers the adoption barrier for first-time buyers of personalised genomic products.

Industry Insights

Home users represent the largest end-use category in the DNA-based Skin Care Market, holding approximately 62% of the total segment share. The structural shift toward at-home genomic testing, catalysed by the widespread commercial availability of direct-to-consumer DNA kits, has fundamentally democratized access to personalised skincare recommendations without requiring clinical intermediation. Consumers can now obtain actionable genetic insights and receive customised product regimens directly through digital platforms.

Wellness Clinics represent the fastest-growing end-use segment in the DNA-based Skin Care Market, reflecting the accelerating convergence of clinical health services and precision aesthetic dermatology. Clinics are progressively integrating DNA-based skincare protocols into their service portfolios, providing clients with genetically tailored treatments that combine diagnostic precision with professional-grade formulations. This clinical integration substantially elevates the scientific credibility of DNA-based skincare within health-conscious, high-spending consumer segments.

Regional Insights and Trends

East Asia DNA-based Skin Care Market Trends

East Asia accounts for approximately 23% of the global DNA-based skin care market, underpinned by a region with deep cultural affinity for skincare science and sustained government investment in genomics and beauty technology. South Korea has emerged as a particularly dynamic innovation hub within this regional cluster. South Korea's cosmetics exports reached a record US$ 11.43 billion, supported by government regulatory alignment, safety assessment reforms, and strategic K-beauty global promotion initiatives. The Korean Ministry of Health and Welfare's KRW 7.1 billion commitment to the Innovative Growth Skin Health Basic Technology Development Project and the KRW 3.8 billion investment in the Skin Genome Analysis Centre collectively signal a deliberate national strategy to position South Korea at the forefront of precision beauty science.

China's Personal Information Protection Law and Japan's Act on Protection of Personal Information establish regulatory parameters for genetic data collection and processing in consumer applications, directly influencing product architecture and data governance frameworks for market participants operating across the region. The competitive landscape within East Asia is characterised by high intensity, with global multinationals and agile local genomics startups contesting market positioning across precision beauty categories.

Local brands are deploying mobile-first platforms and regionally adapted, affordable testing kits that address the specific genetic and dermatological profiles of Asian consumer cohorts. China, Japan, and South Korea each present distinct regulatory environments, distribution ecosystems, and consumer preference profiles that necessitate differentiated market entry and product localisation strategies within the DNA-based Skin Care Market.

North America DNA-based Skin care Market Trends

North America holds the largest regional share of the global DNA-based skin care market at approximately 30%, reflecting the region's advanced consumer genomics infrastructure, high per-capita beauty expenditure, and robust direct-to-consumer retail ecosystem. The U.S. Food and Drug Administration's regulatory posture requires premarket review and clinical-level safety communications for direct-to-consumer genetic tests, creating a compliance-intensive but credibility-enhancing environment for market participants. The Genetic Information Nondiscrimination Act provides legal guardrails preventing the misuse of consumer genetic data in insurance and employment contexts, establishing a foundational trust framework that supports consumer willingness to engage with DNA-based skincare products.

The Federal Trade Commission actively monitors marketing claims made by genomic testing and skincare companies, enforcing substantiation standards that discipline the market and protect consumer interests while raising barriers to entry for scientifically unsubstantiated competitors. Investment activity across North America remains robust, with multiple venture and growth-stage funding rounds completed by genomics-informed skincare firms targeting both mass-market and clinical precision segments. The region's combination of regulatory clarity, high consumer health and beauty awareness, and well-developed capital markets infrastructure continues to make it the most commercially mature and competitively developed geography in the DNA-based Skin Care Market.

Europe DNA-based Skin Care Market Trends

Europe accounts for approximately 25% of the Global DNA-based Skin Care Market, supported by one of the world's most rigorous cosmetics regulatory frameworks and a consumer base with a pronounced preference for science-backed, transparent, and ethically produced beauty formulations. The EU Cosmetics Regulation mandates that all products placed on the European market undergo comprehensive product safety assessments and be registered through the EU Cosmetic Products Notification Portal, ensuring consistent standards of formulation safety and ingredient transparency. These regulatory requirements are structurally aligned with the scientific value propositions of DNA-based skincare, creating a favourable market environment for credible precision beauty brands.

The General Data Protection Regulation classifies genetic data as a "special category" of personal data, imposing specific and stringent data processing obligations on companies offering DNA-based skincare diagnostics and services across EU member states. While these obligations create compliance overhead, they also meaningfully strengthen consumer confidence in genetic data stewardship, which is a material purchase-decision factor for European consumers. European consumers demonstrate consistent willingness to pay premium prices for personalised, clean, and ethically sourced beauty solutions. Investment from entities outside the European Union into regional DNA skincare ventures has further intensified competitive dynamics and broadened the product diversity available within the DNA-based Skin Care Market across the European geography.

Competitive Landscape

The global DNA-based skin care market is moderately consolidated, dominated by a few specialised players who lead through innovation in genetic analysis and personalised skincare solutions.

Companies like IMAGENE LABS PTE. LTD., Caligenix, Inc., EpigenCare Inc., Evergreen Life Ltd., The Skin Dna, and SKINSHIFT are at the forefront, offering advanced DNA or epigenetic-based testing and tailored product recommendations. These players leverage technology, R&D, and digital platforms to deliver personalised regimens, creating strong brand differentiation. While some smaller and emerging firms operate in niche segments, the market is primarily shaped by these key innovators. Strategic partnerships, continuous product development, and consumer-focused personalisation remain the main competitive levels. Overall, the landscape reflects a moderately consolidated market were innovation and scientific credibility drive leadership.

Key Industry Developments:

- March 16, 2026, PROLLENIUM® launched VAMP™ Advanced, a patent-pending topical bio-revitalising solution enriched with high-purity PDRN (salmon DNA fragments) along with vitamins, amino acids, minerals, and hyaluronic acid. The product is designed to improve skin tonicity, elasticity, hydration, and reduce visible signs of ageing. This launch highlights the growing trend of integrating DNA-derived ingredients in skin care formulations for personalised and science-backed skin rejuvenation.

- March 16, 2026, Boldpurity® launched SkinReset™ PDRN Serum, a DNA-fragment (Polydeoxyribonucleotide) based product designed to stimulate fibroblast proliferation and activate the skin’s natural repair processes at the cellular level. This launch underscores the growing adoption of DNA-derived ingredients in skincare formulations, emphasising precise molecular delivery and in-house R&D control to enhance skin rejuvenation and combat cellular ageing.

Companies Covered in DNA-based Skin Care Market

- IMAGENE LABS PTE. LTD.

- Caligenix, Inc.

- EpigenCare Inc.

- Evergreen Life Ltd.

- The Skin Dna

- SKINSHIFT

- DNA Skin Institute

- Anake

- RGR Pharma Ltd.

- LifeNome Inc.

- ALLÉL

- Genetic Beauty

- SkinDNA

- Priori Skin Care

- La Biosthetique

Frequently Asked Questions

The global DNA-based Skin Care Market is projected to be valued at US$ 9.7 Bn in 2026.

The Serums segment is expected to account for approximately 48% of the Global DNA-based Skin Care Market by Product Type in 2026.

The market is expected to witness a CAGR of 5.3% from 2026 to 2033.

The DNA-based Skin Care Market is driven by rising aging populations demanding targeted anti-aging solutions and increasing government investments in genomics and beauty science infrastructure enabling precision skincare innovation.

Key opportunities in the DNA-based Skin Care Market include AI-driven hyper-personalized genomic formulations and the expansion of direct-to-consumer digital channels to penetrate emerging and underpenetrated markets.

Key players in the DNA-based Skin Care Market include IMAGENE LABS PTE. LTD., Caligenix, Inc., EpigenCare Inc., Evergreen Life Ltd., The Skin Dna, and SKINSHIFT.