- Power Generation, Transmission, & Distribution

- Distribution Substation Market

Distribution Substation Market Size, Share, and Growth Forecast 2026 - 2033

Distribution Substation Market by Product Type (Gas-insulated, Air-insulated, Hybrid Substations), Voltage (Low, Medium, High), Insulation (Solid, Liquid, Gas), Application (Industrial, Commercial, Utility), and Regional Analysis, 2026 - 2033

Distribution Substation Market Size and Trends Analysis

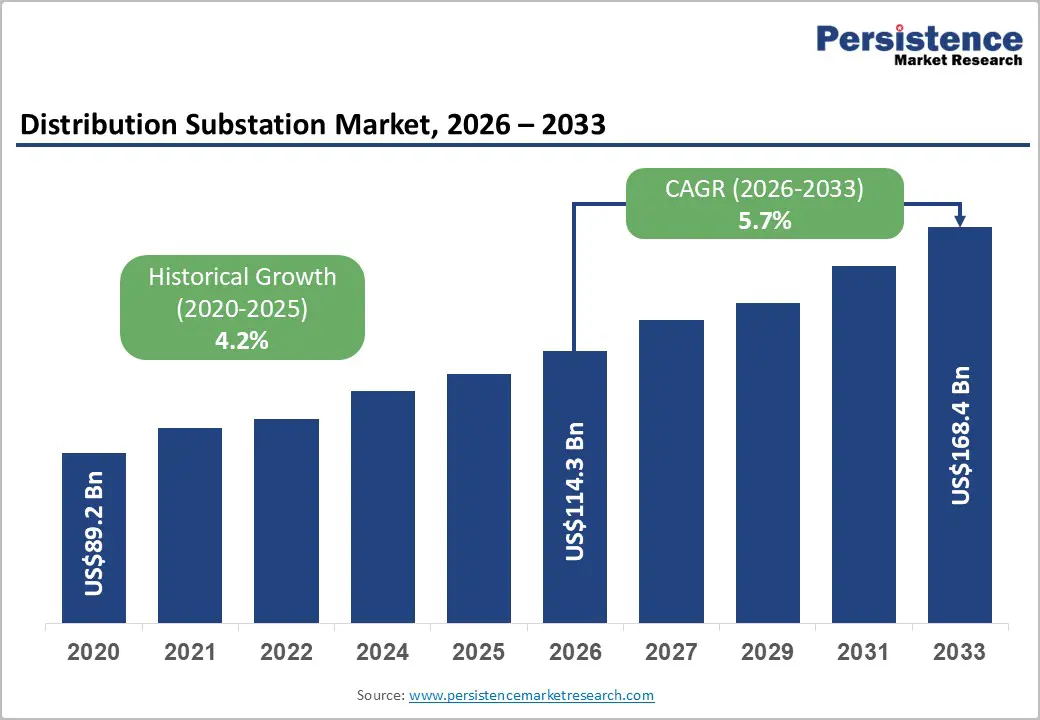

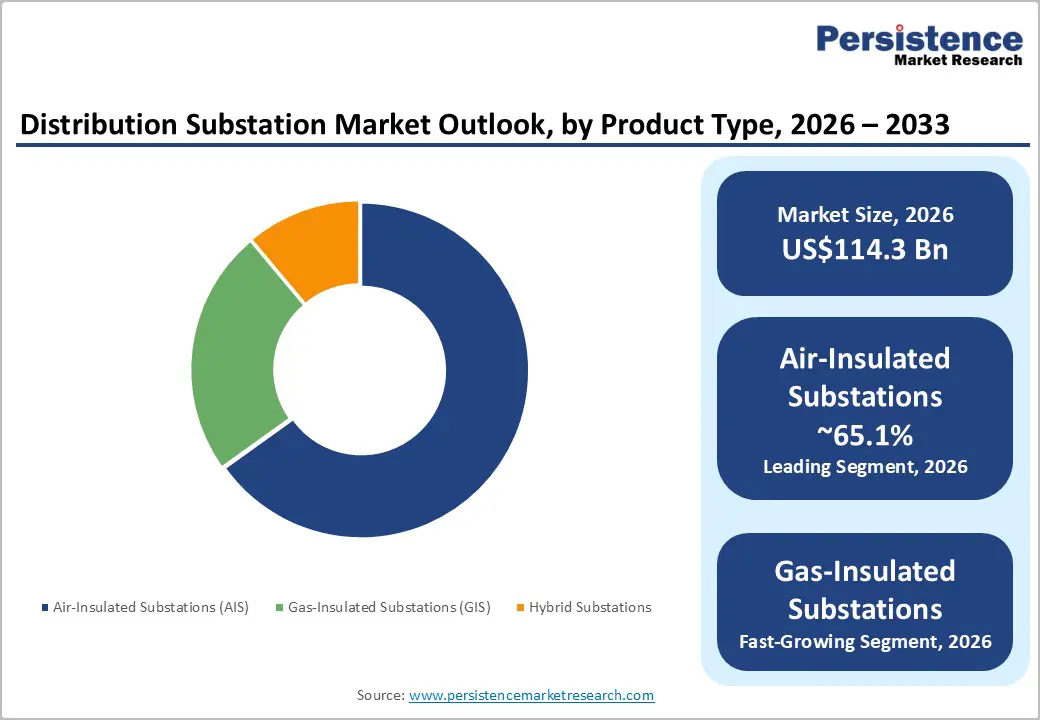

The global distribution substation market size is likely to be valued at US$114.3 billion in 2026 and is expected to reach US$168.4 billion by 2033, growing at a CAGR of 5.7% during the forecast period from 2026 to 2033, driven by rising electricity demand from urban expansion and industrial activity.

Growth is further supported by large-scale renewable energy integration, which requires new substations for grid connectivity. Increasing investments in grid modernization are also spurring deployment across both developed and emerging economies.

Key Industry Highlights:

- Leading Product Type: Air-Insulated Substations (AIS), approximately 65.1% share in 2026, as they are cost-effective and easy to install.

- Dominant Application: Utility, nearly 39.6% share in 2026, because it is responsible for grid expansion and renewable integration.

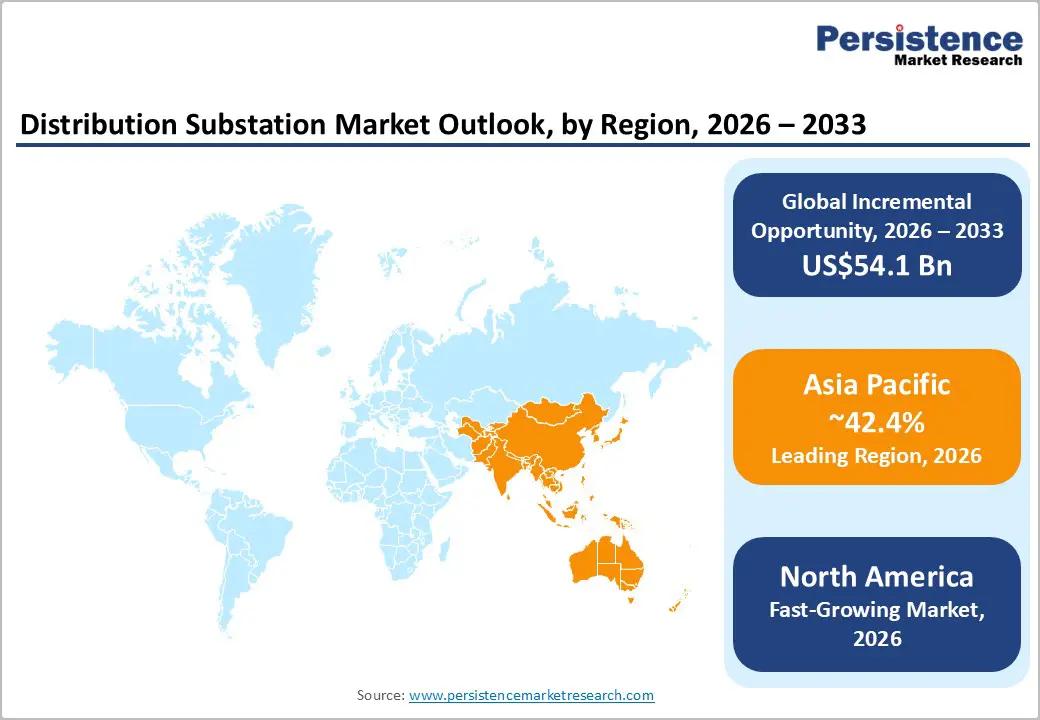

- Leading Region: Asia Pacific, with about 42.4% share in 2026, owing to large-scale grid expansion and rising electricity demand.

- Fast-growing Region: North America, spurred by aging infrastructure replacement and surging power demand from data centers.

- Recent Exhibit: In March 2025, at DISTRIBUTECH 2025, Siemens exhibited digital substation solutions focused on integrating intelligent protection relays and advanced control systems. At the same event, Siemens also demonstrated its Xcelerator portfolio, including Gridscale X and Electrification X, which empower utilities to address grid challenges with real-time data, digital twin technologies, and AI.

DRO Analysis

Driver - Increasing Grid Modernization Activities

Power grids in several regions are decades old, built long before the era of digital controls. Traditional substation controllers have relied on fixed logic, programmed once and rarely updated. This is now changing steadily. Grid modernization integrates sensors, connectivity, AI, and edge computing into transmission and distribution infrastructure. It enables the grid to predict equipment failure before outages occur and detects physical and cyber threats at substations within seconds.

At the Conference of the Electric Power Supply Industry (CEPSI) 2025, Huawei launched its AI-based Intelligent Substation Solution. It connects the entire station through a unified IoT network where inspection videos from robots and drones are transmitted in real time. In a striking 2024 example, when 60 data centers in Virginia tripped to generators simultaneously, it was grid monitoring and automated controls that prevented a wide outage.

Rise of Distributed Energy Resources

The speedy growth of rooftop solar, wind farms, and battery storage is fundamentally changing how power flows through the grid. Distributed Energy Resources (DERs) connected at the distribution level have reformed power flow patterns, transforming distribution line flows from unidirectional to multidirectional. It can feed energy back to the transmission system and trigger voltage rise issues at substations.

Substations must now dynamically manage these variable, bidirectional energy flows. The Federal Energy Regulatory Commission (FERC) Order 2222 enables DER participation in electricity markets. A 2023 U.S. Department of Energy (DOE) report noted that current Virtual Power Plant (VPP) capacity ranges between 30 and 60 GW, with projections of 60 to 80 GW by 2030. This expansion of DER integration demands advanced substation controls that traditional designs simply cannot provide.

Restraint - Exposure to Harsh Weather and Environmental Degradation

Outdoor distribution substations face constant stress from the natural environment, and the damage is often cumulative and hard to detect early. Corrosion is a prominent problem with outdoor switchgear, particularly when wind-driven rain enters joints and assemblies, worsening over time without regular cleaning, inspection, and repainting. Outdoor switchgear in substations is subject not only to weather-related ambient conditions but also to heat generated by neighboring equipment.

During extreme heat events, it can cause insulation and adhesive failures as well as lead to complete equipment failure. Real-world events validate this risk. Storm Ingunn in 2024 caused transmission line failures in Norway, while flash floods in Sydney left substations submerged and disrupted power supply. These repeated environmental stresses shorten equipment life, drive up maintenance costs, and complicate long-term grid planning.

Opportunity - Transition to Fully Digital Substations with AI-Based Remote Monitoring

The shift from analog to digital is changing how substations operate. Digital substations replace traditional copper wiring with fiber-optic communication and IEC 61850-compliant Intelligent Electronic Devices (IEDs), resulting in high efficiency, reliability, and interoperability. The process bus digitizes analog measurements from primary equipment and transmits data to protective relays via fiber-optic cables, enabling quick and accurate fault response.

On the AI side, edge computing and lightweight AI models are increasingly used to filter and process real-time data. Machine learning, including CNNs and LSTMs, has also advanced from exploratory modeling to deployment-ready applications for fault classification and health indexing. One Energy Enterprises recently energized a fully digital and plug-and-play substation, marking a practical milestone in open-architecture digital substation deployment.

Emergence of Space-Efficient and Quickly Deployable Substation Designs

Land scarcity in urban areas is pushing utilities toward compact substation formats. Gas-Insulated Substations (GIS) reduces footprint by 70 to 90% compared to conventional air-insulated installations and fits easily into basements, rooftops, or underground vaults. It significantly eliminates pollution flashovers caused by dust, humidity, or industrial contaminants. Integrated GIS combines circuit breakers, disconnectors, busbars, and instrument transformers into pre-assembled, factory-tested modules, thereby reducing on-site installation time and commissioning risk.

Beyond urban use, modular and containerized substations are gaining traction for rapid deployment. Siemens Energy provides GIS units that can be installed underground or commissioned in prefabricated container modules for space savings, speedy project delivery, and minimal visual impact. These features make them well-suited for emergency restoration, remote area electrification, and temporary grid reinforcement.

Category-wise Analysis

Product Type Insights

Air-Insulated Substations (AIS) are predicted to lead with a share of approximately 65.1% in 2026, as they are simple to design and cost less to build. They use air as the insulation medium, so they do not require expensive gases or sealed enclosures. This reduces both installation and maintenance complexity. Utilities in developing countries prefer AIS for large-scale grid expansion where land is available. Another key reason is easy maintenance and fault detection. Components are visible and accessible, so repairs can be done quickly without specialized handling.

Gas-Insulated Substations (GIS) are estimated to be the fastest-growing segment in the forecast period, as these solve space constraints in urban areas. These use SF6 gas for insulation, which allows very compact designs. GIS can reduce space requirements by up to 90% compared to AIS. This makes them suitable for cities where land is expensive or unavailable. Urban grid modernization is a key driver. Governments are investing in underground and indoor substations to improve reliability and aesthetics.

Application Insights

The utility segment is anticipated to dominate with a share of nearly 39.6% in 2026, as it owns and operates national and regional power grids. Distribution substations are a core part of its infrastructure. Every increase in electricity demand leads to new substation installations or upgrades by utilities. Government-led electrification and grid strengthening programs are the main drivers. For example, India’s Revamped Distribution Sector Scheme (RDSS) focuses on improving power distribution infrastructure.

The commercial segment is expected to remain in the second position in 2026, owing to rising electricity demand from large buildings and energy-intensive facilities. This includes malls, airports, hospitals, IT parks, and data centers. These facilities require reliable and high-quality power, which often demands dedicated substations. Data centers are a key example. Companies such as Amazon Web Services and Microsoft are extending their data center networks globally. Each facility requires dedicated substations to handle high loads and ensure uptime. In various cases, on-site or nearby distribution substations are built to meet these requirements.

Regional Insights

Asia Pacific Distribution Substation Market Trends

Asia Pacific is anticipated to lead in 2026 with a share of nearly 42.4%, as it is still building and extending its power distribution network at a large scale. Several countries in the region are adding new substations instead of only upgrading old ones, which creates continuous demand. Ongoing urban growth and industrial zones also require new distribution infrastructure. Government-backed electrification programs play a key role. For example, India and Southeast Asian nations have focused on rural electrification and grid strengthening. According to the International Energy Agency (IEA), Asia accounts for the largest share of global electricity demand growth, which increases the demand for new substations.

China Distribution Substation Market Trends

China will likely lead Asia Pacific in 2026 with a share of around 34.7%. The focus in the country has shifted from just expansion to grid modernization and ultra-reliable networks. It is now investing heavily in smart grids and digital substations. State-backed companies such as State Grid Corporation of China are deploying advanced substations to handle renewable integration and long-distance transmission. The country has also built large Ultra-High Voltage (UHV) networks, which require high-capacity substations at multiple nodes.

India Distribution Substation Market Trends

In 2026, India is projected to account for a share of approximately 29.1%, boosted by government schemes and rising electricity demand. Programs such as the Revamped Distribution Sector Scheme are focused on improving distribution infrastructure, including substations. Organizations, including Power Grid Corporation of India Limited, and state utilities are extending substation capacity to reduce losses and improve reliability. According to the Central Electricity Authority, peak power demand in India crossed 240 GW in 2024, showing high pressure on the grid.

North America Distribution Substation Market Trends

North America is predicted to be the fastest-growing market in 2026 with a share of approximately 28.7%, pushed by grid modernization rather than new electrification. Much of the existing infrastructure is old and requires replacement. This creates steady demand for substation upgrades. Government funding is a key factor. The U.S. government has allocated billions under infrastructure and clean energy programs to improve grid resilience. Reports from the U.S. Department of Energy (DOE) highlight investments in smart grids, wildfire-resistant systems, and substation automation.

U.S. Distribution Substation Market Trends

A share of nearly 66.3% is expected to be held by the U.S. in 2026, backed by aging infrastructure and new demand sources. Several substations are over 40 years old and require replacement or upgrades. Renewable energy integration is a prominent factor. Large solar and wind projects require new grid connections. According to the U.S. Energy Information Administration, renewables are contributing an increasing share of electricity generation, which requires grid expansion and new substations.

Europe Distribution Substation Market Trends

Europe will likely witness steady growth in the forecast period with a share of nearly 17.5% in 2026, because most of its grid infrastructure is already developed. Growth comes mainly from upgrades and modernization rather than new installations. The region is focused on energy transition. Countries are replacing fossil fuel-based systems with renewables. This requires upgrading substations to handle variable power flows. According to the European Commission, grid investments are important to meet climate targets.

Germany Distribution Substation Market Trends

Germany is projected to register a substantial share of approximately 32.4% in 2026, bolstered by its energy transition policy. The country is phasing out nuclear and coal, while increasing wind and solar capacity. This creates demand for upgraded substations. Grid operators are further investing in digital and automated substations to manage renewable variability. Organizations such as Bundesnetzagentur oversee grid expansion and approve infrastructure projects.

U.K. Distribution Substation Market Trends

A share of around 15.8% is predicted to be held by the U.K. in 2026, owing to offshore wind expansion. The country is one of the largest offshore wind markets, and each project demands substations for grid connection. Companies such as National Grid plc are investing in upgrading substations to handle new renewable inputs. The government’s net-zero targets are also pushing grid modernization. Cities, including London, are adopting GIS substations to manage space constraints. While the market is not expanding as fast as Asia Pacific or North America, ongoing renewable projects and grid upgrades are ensuring stable growth.

Competitive Landscape

The global distribution substation market is fragmented with the presence of multinational electrical equipment manufacturers, regional engineering firms, and specialized grid infrastructure providers. Large companies such as ABB, Siemens Energy, Schneider Electric, Hitachi Energy, and Eaton hold significant positions. However, no single company dominates the market globally as utilities typically award projects through competitive bidding and often favor local suppliers for grid expansion projects.

Competition has shifted beyond traditional transformers and switchgear toward digital substations, automation systems, and predictive maintenance capabilities. Vendors are constantly differentiating themselves through IEC 61850-based digital platforms, AI-supported monitoring, remote asset management, and smart-grid integration rather than hardware alone. This trend has strengthened the position of companies with unique software and automation portfolios.

Key Industry Developments:

- In February 2026, Siemens Smart Infrastructure introduced SIPROTEC V, the virtualized version of the proven SIPROTEC 5 protection and control device. It supports centralized operation of up to 60 virtual Intelligent Electronic Devices (IEDs) within a single substation server, reducing space requirements by approximately 45%.

- In February 2026, GE Vernova completed the acquisition of the remaining 50% stake of Prolec GE from Xignux. The deal would strengthen GE Vernova's position in global grid markets, with Prolec GE expected to contribute to the company's 2026 financial guidance and growth projections through 2028.

- In February 2026, Xcel Energy and GE Vernova signed a landmark Strategic Alliance Agreement aimed at advancing a shared vision for reliable and sustainable energy. The two companies plan to collaborate on developments in AI, grid modernization, and joint research & development.

Companies Covered in Distribution Substation Market

- ABB

- CG Power and Industrial Solutions

- Eaton

- Efacec

- General Electric

- Hitachi Energy

- L&T Electrical and Automation

- Locamation

- Open System International

- Rockwell Automation

- Schneider Electric

- Siemens Energy

- Texas Instruments

- Tesco Automation

Frequently Asked Questions

The global distribution substation market is projected to be valued at US$114.3 billion in 2026.

The distribution substation market is expected to reach US$168.4 billion by 2033.

Key market trends include the shift toward digital substations and rising adoption of GIS in urban areas.

Air-insulated substations are expected to be the leading product type with a share of nearly 65.1% in 2026, owing to simple maintenance and easy fault detection.

The distribution substation market is expected to grow at a CAGR of 5.7% from 2026 to 2033.

ABB, CG Power and Industrial Solutions, Eaton, and Efacec are a few key market players.