- Medical Devices

- Digital Stethoscope Market

Digital Stethoscope Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Digital Stethoscope Market by Product Type (Amplifying Stethoscope, Digitalization Stethoscope), Technology (Wireless Transmission System (Bluetooth), Integrated Chest-Piece System, Integrated Receiver Head-Piece System, Numerical Simulation and System Integration), End User (Hospitals, Clinics, Healthcare Institutes & Organizations, Home Care Settings, Others), and Regional Analysis from 2026 to 2033

Digital Stethoscope Market Share and Trends Analysis

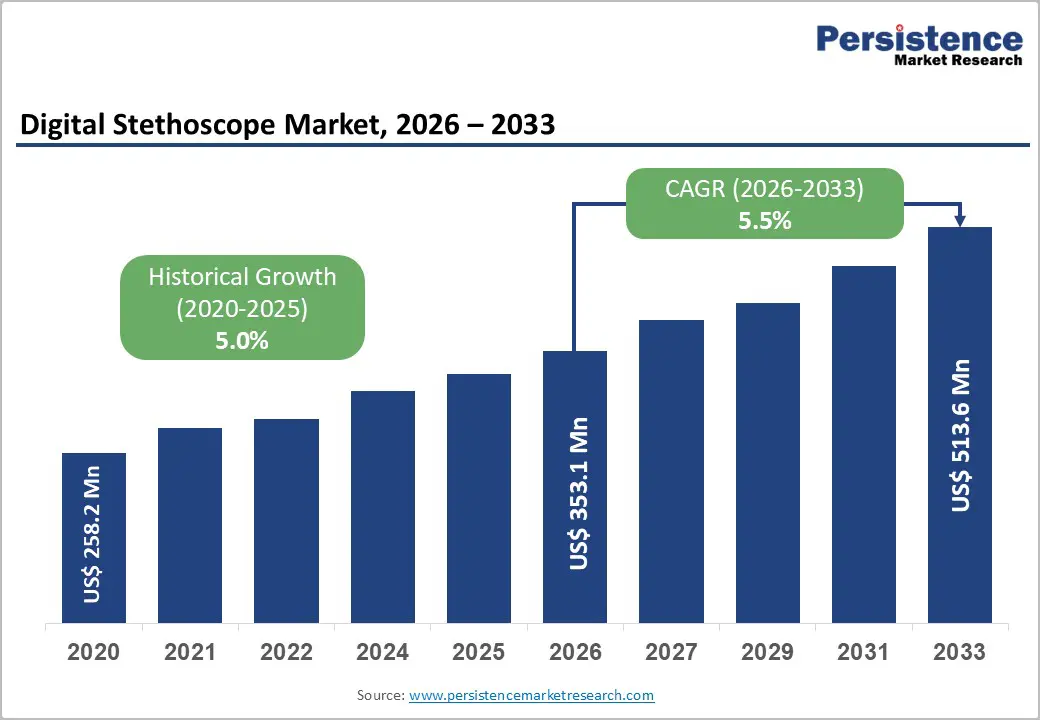

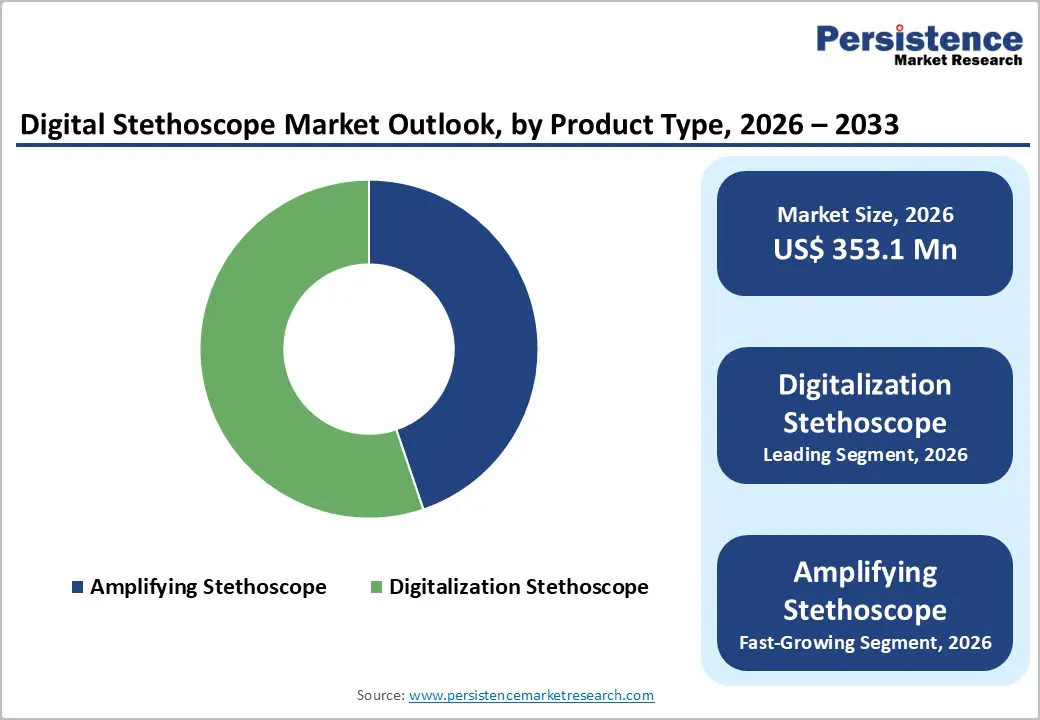

The global digital stethoscope market size is likely to be valued at US$ 353.1 million in 2026 to US$ 513.6 million by 2033 growing at a CAGR of 5.5% during the forecast period from 2026 to 2033.

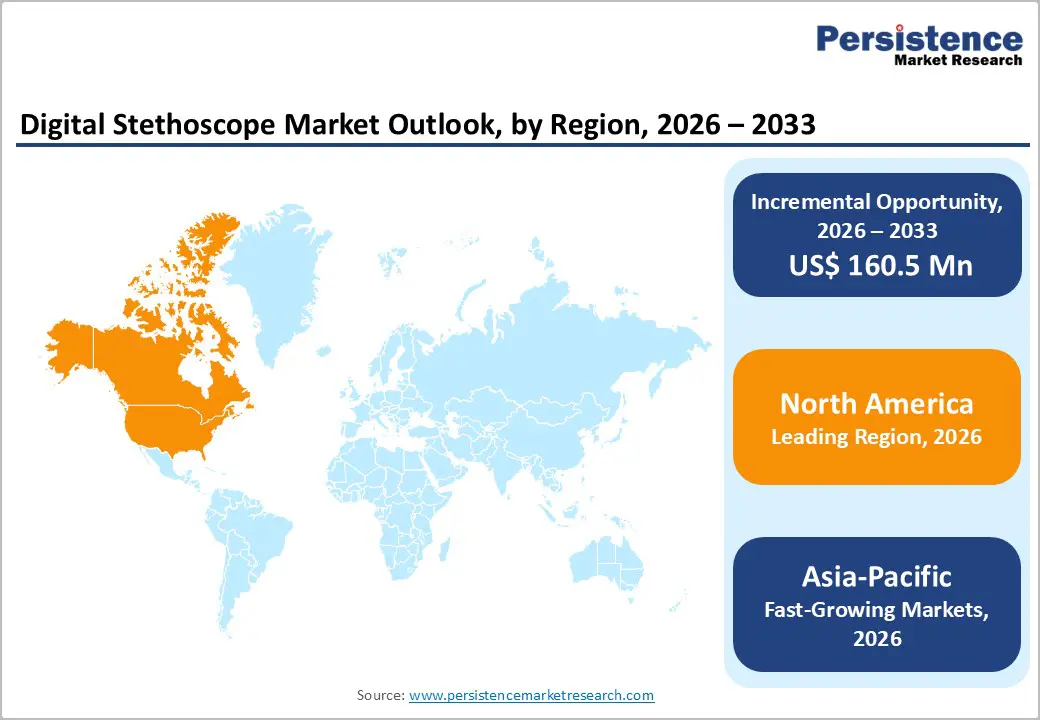

The global market is expanding steadily, driven by rising cardiovascular disease prevalence, increasing emergency admissions, and demand for rapid, accurate diagnostics. North America dominates due to advanced healthcare infrastructure and early technology adoption, whereas Asia-Pacific is the fastest-growing region, supported by expanding healthcare facilities, rising patient volumes, improved access, and greater awareness of early cardiac diagnosis.

Key Industry Highlights

- Dominant Segment: Digitalization stethoscopes represent a dominant share of the digital stethoscope market in 2025 with 55.2% share, driven by advanced signal processing, Bluetooth connectivity, sound recording, and integration with mobile devices. Their ability to support telemedicine, remote monitoring, and AI-assisted cardiac and pulmonary analysis accelerates adoption across hospitals and outpatient settings.

- Dominant Region: North America holds the largest market share in 2025 with 41.6% share, supported by advanced healthcare infrastructure, early adoption of digital diagnostics, and high cardiovascular disease prevalence. Asia-Pacific is the fastest-growing region, driven by expanding healthcare facilities, rising patient volumes, improved access to care, and increasing awareness of early cardiac assessment.

- Growth Indicators: Key growth drivers include the rising burden of cardiovascular and respiratory diseases, increasing emergency and critical care admissions, demand for rapid bedside diagnostics, the expansion of telehealth services, and technological advancements in digital auscultation and AI-based sound analysis.

- Market Opportunity: Major opportunities lie in AI-enabled diagnostic algorithms, wireless and cloud-connected stethoscopes, telemedicine integration, use in home healthcare and remote monitoring, and rapid adoption in emerging economies with strengthening digital health infrastructure.

| Global Market Attributes | Key Insights |

|---|---|

| Digital Stethoscope Market Size (2026E) | US$ 353.1 Mn |

| Market Value Forecast (2033F) | US$ 513.6 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.0% |

Market Dynamics

Driver: Rising prevalence of cardiovascular and respiratory diseases globally

Cardiovascular diseases (CVDs), including heart attack and stroke, remain the leading cause of death worldwide, accounting for approximately 32 % of all global deaths in 2022, with an estimated 19.8 million deaths attributed to CVDs. Early detection improves outcomes; however, the absolute burden remains immense, driven by aging, lifestyle factors, and urbanization. In 2021, CVDs comprised the majority of noncommunicable disease fatalities, which themselves were responsible for 43 million deaths globally. The high and growing burden of CVD underscores the need for improved diagnostic tools like digital stethoscopes to facilitate early identification of cardiac abnormalities and guide timely clinical intervention.

Chronic respiratory diseases such as chronic obstructive pulmonary disease (COPD) also contribute significantly to global mortality. COPD alone was the fourth leading cause of death worldwide, causing 3.5 million deaths in 2021, and disproportionately affects people in low- and middle-income countries. Respiratory conditions frequently coincide with cardiovascular disorders, sharing common risk factors like tobacco use and environmental pollution. Together, CVDs and chronic respiratory illnesses contribute a substantial portion of the global disease burden. The increasing prevalence of these conditions drives demand for advanced auscultation technologies such as digital stethoscopes, which enhance clinicians’ ability to detect subtle heart and lung sounds, support remote monitoring, and improve diagnostic accuracy.

Restraints: High cost of digital stethoscopes compared to conventional acoustic models

One significant restraint in the digital stethoscope market is the higher cost compared to traditional acoustic models, which limits widespread adoption, especially in budget-constrained settings. Conventional acoustic stethoscopes typically cost between $20 and $160 (INR 1,600-INR 13,000), depending on quality, whereas high-quality digital models, such as the 3M Littmann CORE Digital Stethoscope and the Eko CORE 500 Digital Stethoscope, commonly range from $299 to $499 (INR 24,000-INR 40,000+) or more. This price differential is often two to three times higher, imposing a substantial financial burden on small clinics and practitioners, who must balance advanced technology against limited operational budgets.

The high upfront investment required for digital stethoscopes also impacts procurement decisions in public health systems and emerging economies. A single digital unit can constitute a significant share of a clinician’s monthly income in lower-income regions, where monthly wages may be modest yet the device cost remains high. Beyond purchase price, healthcare organizations may incur additional expenses for software updates, battery replacements, or connectivity subscriptions associated with digital features, further discouraging adoption in cost-sensitive environments. Consequently, many facilities continue to rely on conventional acoustic devices despite the enhanced diagnostic capabilities of digital stethoscopes.

Opportunity: Integration of AI and machine learning for automated cardiac and lung sound analysis

The integration of artificial intelligence (AI) and machine learning (ML) into digital stethoscopes presents a significant opportunity to substantially enhance cardiac sound analysis. A clinical study reported that AI-augmented digital auscultation detected valvular heart disease in 94.1% of cases, compared with 41.2% detected by traditional stethoscopes used by clinicians, demonstrating a clear diagnostic advantage. AI models trained on heart sound recordings can identify murmurs and abnormalities with high sensitivity, enabling reliable early detection of conditions that might be missed by standard auscultation. This capability can lead to earlier interventions, reduce missed diagnoses, and improve patient outcomes in cardiovascular care.

AI and ML also significantly improve lung sound analysis, enabling automated detection and classification of respiratory abnormalities. Research on pediatric breath sound recordings has shown that AI algorithms achieve high detection performance for wheezes and crackles, with sensitivity and agreement rates comparable to those of physician assessments. In remote auscultation studies, AI-assisted systems demonstrated 97% sensitivity and 89% specificity in identifying abnormal heart sounds compared with face-to-face evaluation, reinforcing the technology’s robustness in real-world clinical settings. These results indicate that AI-enabled digital stethoscopes can support scalable, objective screening for both cardiac and pulmonary conditions, expanding access in diverse healthcare settings.

Category-wise Analysis

By Product Type Insights

Digital stethoscopes account for 48.8% of the global market in 2025, as they address growing clinical needs for accuracy, data capture, and remote care. Digital stethoscopes can amplify body sounds by up to 40 times, significantly improving the detection of faint cardiac murmurs and subtle lung abnormalities compared with acoustic devices, as demonstrated in peer-reviewed clinical studies indexed in the U.S. National Library of Medicine. The U.S. Centers for Disease Control and Prevention reports that over 695,000 deaths annually are attributed to heart disease in the United States, highlighting the need for precise auscultation. Digitalization of stethoscopes also enables sound recording, sharing, and telemedicine integration, aligning with government-backed digital health initiatives and increasing reliance on remote diagnostics across healthcare systems.

By Technology Insights

Integrated chest-piece systems hold the largest share of the digital stethoscope market, accounting for about 56.8%, because they incorporate amplification, noise reduction, and signal processing directly into the chest piece, providing consistent, high-fidelity sound capture without external modules. This self-contained design minimizes variability in auscultation quality across different environments, such as busy hospital wards or emergency rooms, and aligns closely with clinicians’ expectations of a traditional stethoscope while adding advanced digital capabilities. Integrated chest-piece systems also support features like amplification up to 40×, ECG recording, Bluetooth connectivity, and AI interpretation, enabling clearer detection of cardiac and pulmonary sounds and smoother integration into clinical workflows. Clinicians value their ergonomic familiarity, reliability, and usability, all factors that drive preference and adoption in high-volume clinical settings such as hospitals and specialty clinics, reinforcing their dominant position.

Regional Insights

North America Digital Stethoscope Market Trends

North America dominates the digital stethoscope market, accounting for 41.6% of the market in 2025, owing to its advanced healthcare infrastructure, widespread telehealth adoption, and high healthcare IT investment. In the United States, telemedicine usage is substantial: approximately 20% of adults used telehealth services in 2021, with even higher use among older adults, reflecting strong demand for remote diagnostics. This digital-first healthcare environment supports tools like digital stethoscopes that integrate with telemedicine platforms, enabling remote auscultation. Additionally, the region has a high burden of chronic diseases, including cardiovascular and respiratory conditions, which increases demand for precise diagnostic tools. Favorable reimbursement policies for remote care and robust regulatory support further accelerate adoption, reinforcing North America’s leadership in the digital stethoscope market.

Europe Digital Stethoscope Market Trends

Europe is a significant region in the digital stethoscope market because it features robust healthcare systems, a high prevalence of chronic diseases, and strong support for digital health policy. Europe accounts for a substantial share of global adoption of digital diagnostic devices, with countries such as Germany, the United Kingdom, and France leading in the deployment and integration of advanced auscultation tools. The region’s aging population and high burden of cardiovascular diseases drive demand for early and precise diagnostics, as reflected in the EU’s cardiovascular death rate of 343.4 per 100,000 in 2021, underscoring the clinical need for improved monitoring. Additionally, Europe’s regulatory frameworks and digital health strategies promote innovation, data interoperability, and telehealth uptake, supporting broader adoption of digital stethoscopes in hospitals and community care.

Asia Pacific Digital Stethoscope Market Trends

Asia-Pacific is the fastest-growing region in the digital stethoscope market, driven by the rapid expansion of healthcare infrastructure, the rising burden of cardiovascular and respiratory diseases, and the increasing adoption of digital health technologies. The World Health Organization reports that over three-quarters of global cardiovascular deaths occur in low- and middle-income countries, many within the Asia Pacific, driving demand for accessible diagnostics. In India alone, CVD prevalence increased to an estimated 54.5 million cases of heart failure in 2019, reflecting substantial clinical need for improved early screening tools. Expanding laboratory networks, growing numbers of trained clinicians, and government initiatives supporting telemedicine (such as India’s Telemedicine Practice Guidelines) further accelerate uptake. These factors position the Asia Pacific as the fastest-growing market for digital stethoscopes, especially in community and remote care settings.

Competitive Landscape

Leading digital stethoscope companies focus on high-fidelity, AI-enabled, and connected diagnostic devices. Investments target wireless, telemedicine-compatible stethoscopes, integration with electronic health records, and improved signal processing. R&D emphasizes sound clarity, usability, and clinical accuracy, while collaborations with hospitals and telehealth providers enhance adoption, drive innovation, expand cardiac and pulmonary diagnostic applications, and strengthen global market reach.

Key Industry Developments:

- In September 2025, Doctors at Imperial College London developed an AI-powered stethoscope that could detect major heart conditions including heart failure, atrial fibrillation, and valve disease in just 15 seconds, based on trial results from about 12,000 UK patients; the device doubled heart failure detection rates and significantly increased diagnoses of other serious cardiac issues compared with standard exams.

- In September 2025, AI-enabled digital stethoscopes developed by Eko Health marked a historic advance in early heart disease detection, as the TRICORDER trial demonstrated significantly higher diagnosis rates compared with standard care in routine exams.

Companies Covered in Digital Stethoscope Market

- FarmaSino Pharmaceuticals

- Contec Medical Systems

- Hefny Pharma Group

- Eko Health Inc.

- 3M

- Think Labs Medical LLC

- TeleSensi

- American Diagnostics

- EKuore

- Hill-Rom

- Others

Frequently Asked Questions

The global digital stethoscope market is projected to be valued at US$ 353.1 million in 2026.

Rising cardiovascular and respiratory diseases, telemedicine adoption, demand for accurate diagnostics, and technological advancements drive growth.

The global digital stethoscope market is poised to witness a CAGR of 5.5% between 2026 and 2033.

AI integration, telemedicine, wireless connectivity, home monitoring, and emerging economies offer significant digital stethoscope market opportunities.

FarmaSino Pharmaceuticals, Contec Medical Systems, Hefny Pharma Group, Eko Health Inc., 3M, Think Labs Medical LLC.