- Processed Food

- Cream Cheese Market

Cream Cheese Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Cream Cheese Market is segmented by Source (Dairy-Based, Plant-Based), by Flavor (Plain, Savory Flavors, Sweet Flavors), End-user (Foodservice, Industrial / Food Manufacturing, Household / Retail), and Regional Analysis, 2026 - 2033

Cream Cheese Market Share and Trends Analysis

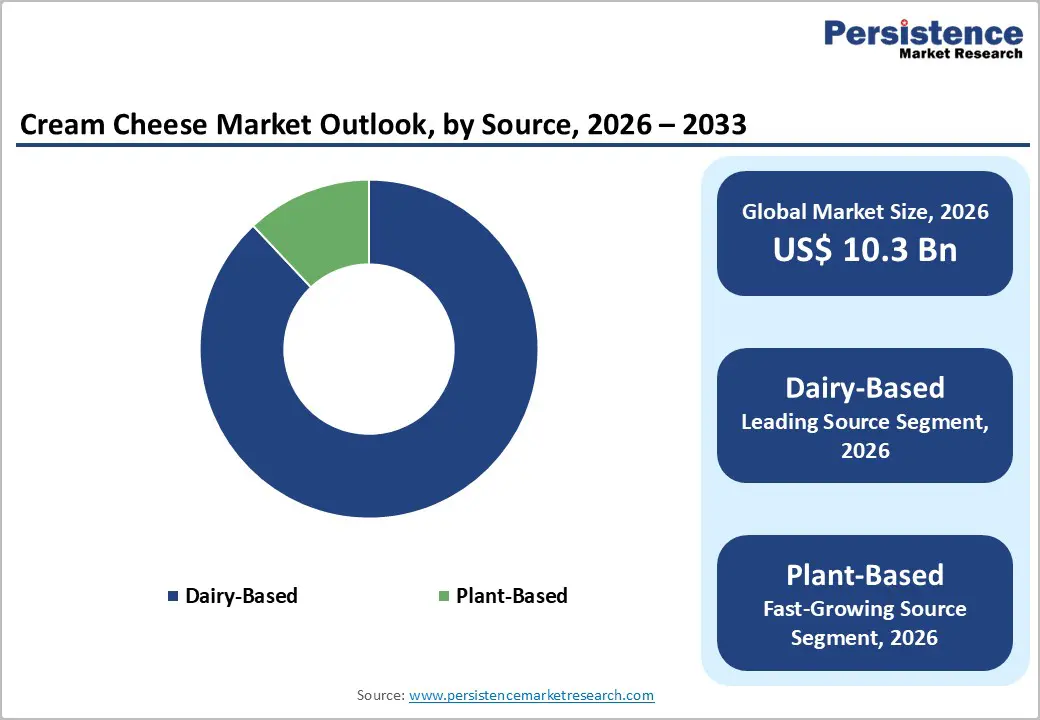

The global cream cheese market size is expected to be valued at US$ 10.3 billion in 2026 and projected to reach US$ 14.6 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033.

The market expansion is primarily underpinned by the surging popularity of westernized diets and the increasing versatility of cream cheese as a staple ingredient in both sweet and savory culinary applications. As a fundamental component in the booming global bakery and confectionery sectors, its demand is intrinsically linked to the rising consumption of cheesecakes, bagels, and premium frostings. Furthermore, the heightening consumer preference for convenient, protein-rich snacking options has encouraged dairy processors to innovate with portable formats and diverse flavor profiles, ensuring consistent market traction across both mature and emerging economies.

Key Industry Highlights:

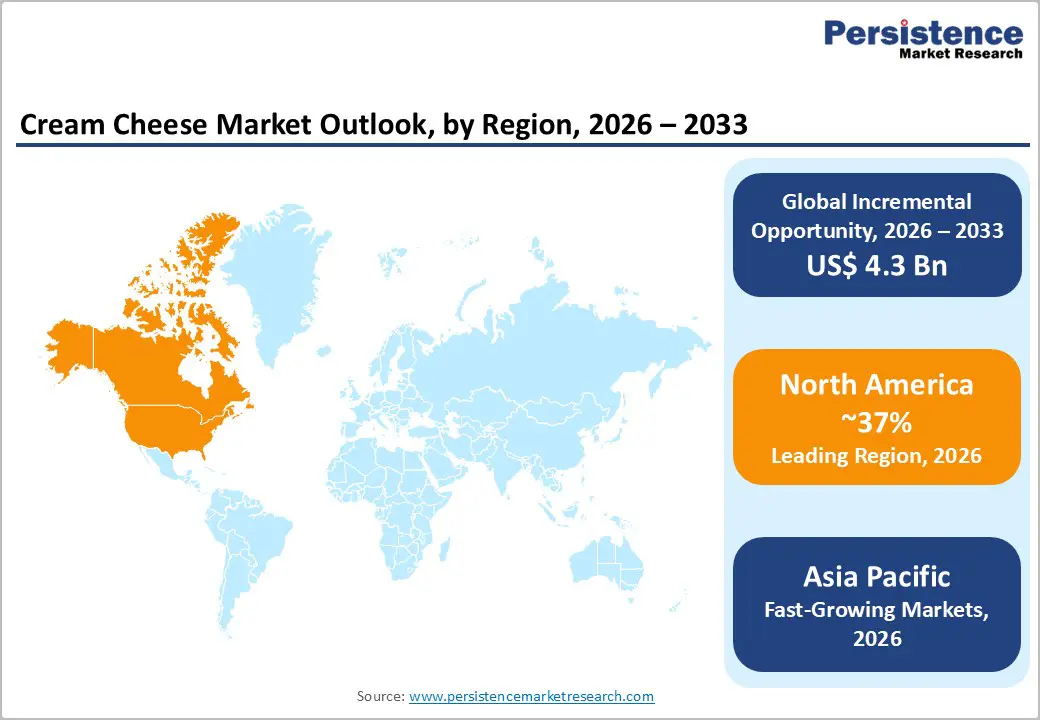

- Leading Region: North America, holding 37% market share, supported by strong bagel and cheesecake consumption culture, well-developed retail infrastructure, and the dominant presence of major dairy brands such as The Kraft Heinz Company.

- Fastest-Growing Region: Asia Pacific, driven by rapid westernization of diets, expanding café and bakery chains, and growing consumer interest in premium desserts like cheesecakes and cheese-based beverages.

- Fastest-Growing Source Segment: Plant-Based cream cheese is gaining strong traction due to rising vegan diets, lactose intolerance awareness, and innovations using almond, cashew, oat, and coconut-based formulations.

- Market Drivers: Expanding global demand for premium bakery and confectionery products is significantly increasing the use of cream cheese in pastries, desserts, and café-style breakfast menus.

- Opportunities: Development of functional cream cheese with probiotics and health-focused formulations offers new premium positioning opportunities in the growing gut-health and functional dairy segment.

- Key Developments: In February 2026, Philadelphia Cream Cheese launched the Really Philly Good brand platform developed by Johannes Leonardo to reposition cream cheese as an everyday kitchen staple. In July 2025, Cremeitalia introduced a range of bold-flavored cream cheese variants targeting evolving consumer demand for premium flavored dairy spreads.

| Key Insights | Details |

|---|---|

| Global Cream Cheese Market Size (2026E) | US$ 10.3 Bn |

| Market Value Forecast (2033F) | US$ 14.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Dynamics

Driver - Rising Demand for Premium Bakery and Confectionery Products

A primary driver of the cream cheese industry is its essential role in the global bakery market. The demand for indulgent, high-quality baked goods has increased significantly, especially in the post-pandemic era where consumers seek permissible indulgence. Cream cheese is a vital functional ingredient, offering the right texture and acidity for cheesecakes, pastries, and artisanal frostings. As global coffee shop chains and bakery franchises expand in developing regions, the demand for cream cheese-based spreads and fillings has grown. Companies like The Kraft Heinz Company, with its well-known Philadelphia brand, have successfully capitalized on this trend by partnering with foodservice leaders to incorporate cream cheese into mainstream breakfast and dessert menus worldwide.

Restraints - Rising Prevalence of Lactose Intolerance and Vegan Dietary Shifts

The growing awareness of lactose intolerance and the mainstreaming of veganism pose a substantial challenge to traditional dairy-based cream cheese consumption. Statistics from the National Institutes of Health (NIH) indicate that a significant percentage of the global population has a reduced ability to digest lactose, leading many to seek non-dairy alternatives. The plant-forward dietary shift, championed by organizations like the Vegan Society, has accelerated the demand for almond, cashew, and oat-based spreads. While dairy-based products still hold an 88% market share in 2025, the rapid growth of the Plant-Based segment led by innovators like Oatly Group AB and Danone S.A. directly competes for shelf space and consumer attention. This necessitates constant innovation from traditional dairy players to maintain their market dominance against increasingly sophisticated dairy-free mimics.

Opportunity - Expansion into the Functional and Probiotic Dairy Segment

There is a burgeoning opportunity for cream cheese to be positioned as a functional health food. As gut health becomes a top priority for global consumers, the integration of live active cultures and specific probiotic strains into cream cheese spreads is expected to generate significant demand. According to the World Gastroenterology Organisation, the probiotic market is expanding beyond supplements into everyday dairy staples. Manufacturers can capitalize on this by launching fortified cream cheese variants that offer immune-boosting or digestive benefits. This strategy is particularly effective in the Asia Pacific region, where there is a strong cultural affinity for fermented foods. By aligning cream cheese with the broader trend of food as medicine, companies can justify premium pricing and differentiate their products in a crowded retail landscape dominated by plain, unfortified options.

Category-wise Analysis

Source Insights

The Dairy-Based segment remains the dominant force in the market, capturing a substantial 88% market share in 2025. This leadership is attributed to the long-standing consumer trust in traditional dairy, its superior flavor profile, and its established role in traditional culinary recipes. Dairy cooperatives like Fonterra Co-operative Group and GCMMF (Amul) play a pivotal role in maintaining this dominance through massive production capacities and deep distribution networks. However, the Plant-Based segment is identified as the fastest growing segment through 2033. This rapid rise is fueled by the escalating number of flexitarian consumers and the increasing availability of high-quality dairy-free alternatives made from cashews, coconut oil, and soy, which are increasingly mimicking the sensory experience of traditional dairy cream cheese.

End-user Insights

The Plain flavor segment continues to hold the leading market share in 2025 due to its unparalleled versatility in both home and professional kitchens. It serves as the primary base for cheesecakes, frostings, and diverse cooking applications, making it a must-have item in the Industrial / Food Manufacturing sector. Conversely, Savory Flavors and Sweet Flavors are the fastest-growing segments in the retail space. This growth is driven by the rising demand for ready-to-use spreads that eliminate the need for additional seasoning. Innovation in this category is spearheaded by brands like Franklin Foods and Land O'Lakes Inc., which are consistently launching seasonal and limited-edition flavors to engage adventurous consumers and drive impulse purchases in supermarkets.

Regional Insights

North America Cream Cheese Market Trends and Insights

North America is the leading region in the global cream cheese market, holding a 37% market share in 2025. The region's leadership is underpinned by a deeply ingrained bagel culture and the high consumption of cheesecakes. The United States leads the region in terms of both production and consumption, with a highly developed retail infrastructure and a strong presence of global market leaders like The Kraft Heinz Company.

The innovation ecosystem in the U.S. is particularly focused on clean-label and artisanal cream cheese products. Regulatory frameworks managed by the Food and Drug Administration (FDA) ensure high safety and labeling standards, which fosters consumer trust. Furthermore, the region is a hub for plant-based innovation, with several startups and established dairy players launching oat and nut-based cream cheese alternatives to cater to the rising vegan population in major metropolitan areas. The high disposable income and the established habit of using cream cheese as a primary breakfast spread ensure that North America will maintain its dominant position throughout the forecast period.

Asia Pacific Cream Cheese Market Trends and Insights

Asia Pacific is identified as the fastest growing segment for the cream cheese market through 2032. This rapid expansion is primarily driven by the westernization of diets in China, India, and Japan. As the middle class expands and urbanization increases, there is a marked surge in the popularity of western-style bakeries and coffee chains. China is a major engine of growth, where the cheese-tea phenomenon and the increasing adoption of cheesecakes as premium desserts have created a massive demand for imported cream cheese.

Growth dynamics in India are also noteworthy, with local giants like GCMMF (Amul) launching affordable cream cheese spreads to tap into the urban breakfast market. The region benefits from significant manufacturing advantages and a young, adventurous population that is eager to experiment with international flavors. The expansion of modern retail chains and the booming e-commerce sector in Southeast Asia have made cream cheese more accessible to a wider demographic. As international players like Fonterra Co-operative Group increase their regional investments, the Asia Pacific region is poised to become a central pillar of the global cream cheese industry.

Competitive Landscape

The global cream cheese market exhibits a consolidated structure at the top tier, where a few multinational dairy giants hold significant influence over global supply chains and brand recognition. Companies like The Kraft Heinz Company, Lactalis Group, and Arla Foods amba dominate the retail and foodservice channels through massive marketing budgets and economies of scale. However, the market remains fragmented at the regional level, with local dairy cooperatives and artisanal players catering to specific cultural palates and farm-to-table trends. Key differentiators employed by market leaders include the mastery of specialized filtration technologies and the development of proprietary stabilizer systems that ensure consistent texture across various temperatures. Emerging business model trends show a shift toward co-innovation, where cream cheese producers collaborate with global bakery franchises to create customized flavor profiles and application-specific formulations, thereby securing long-term supply contracts.

Key Developments:

- In February 2026, Philadelphia Cream Cheese introduced a new brand platform titled Really Philly Good, developed by Johannes Leonardo. The campaign features 19 creative spots and introduces a new brand character, Phillyboy, aiming to reposition cream cheese as an everyday kitchen staple rather than just a breakfast spread.

- In July 2025, Cremeitalia, an Indian clean-label cheese brand, launched a new range of bold-flavored cream cheese variants, targeting evolving consumer preferences for innovative flavors and premium dairy spreads in the domestic market.

Companies Covered in Cream Cheese Market

- The Kraft Heinz Company

- Danone S.A.

- Royal FrieslandCampina N.V.

- Arla Foods amba

- Fonterra Co-operative Group

- Lactalis Group

- Saputo Inc.

- Oatly Group AB

- GCMMF

- Franklin Foods

- Land O'Lakes Inc.

- Others

Frequently Asked Questions

The global Cream Cheese market is projected to be valued at US$ 10.3 Bn in 2026.

Rising Demand for Premium Bakery and Confectionery Products is a major factor driving global Cream Cheese market.

The Global Cream Cheese market is poised to witness a CAGR of 5.1% between 2026 and 2033.

Expansion into the Functional and Probiotic Dairy Segment is a significant opportunity in the Cream Cheese market.

Major players in the Global Cream Cheese market include The Kraft Heinz Company, Danone S.A., Royal FrieslandCampina N.V., Arla Foods amba, Fonterra Co-operative Group, Lactalis Group, Saputo Inc. and others.