- Industrial Goods & Service

- Crawler Excavators Market

Crawler Excavators Market Size, Share, and Growth Forecast 2026 - 2033

Crawler Excavators Market by Product Type (Standard Crawler Excavators, Mini/Compact Crawler Excavators, Long Reach Excavators, Demolition Excavators, Hybrid/Electric Crawler Excavators, Short Tail Swing Excavators), by Bucket Capacity (Small: 0.3-2.0 m³, Medium: 2.0-4.0 m³, Large: >4.0 m³), by Drive Type (Hydraulic Drive, Mechanical Drive), End-User (Construction Companies, Mining Companies, Rental Service Providers, Government & Municipal Bodies, Agriculture & Forestry Operators), and Regional Analysis, 2026 - 2033

Crawler Excavators Market Size and Trend Analysis

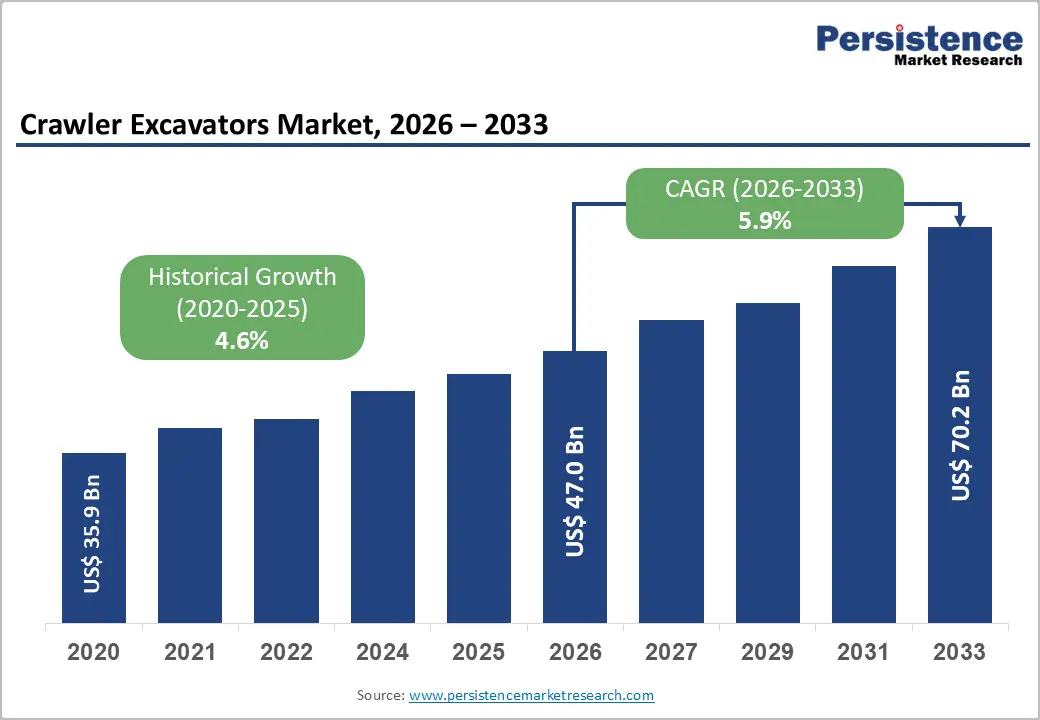

The global crawler excavators market size is likely to be valued at US$ 47.0 billion in 2026 and is expected to reach US$ 70.2 billion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033.

The market's sustained expansion is fundamentally driven by accelerating global infrastructure investment, encompassing road, rail, port, and urban development programmes, combined with the mining sector's sustained demand for heavy-duty earthmoving equipment and the rapid technological evolution toward hybrid and electric excavator platforms that is expanding addressable market opportunities into emission-regulated urban construction environments.

Key Industry Highlights:

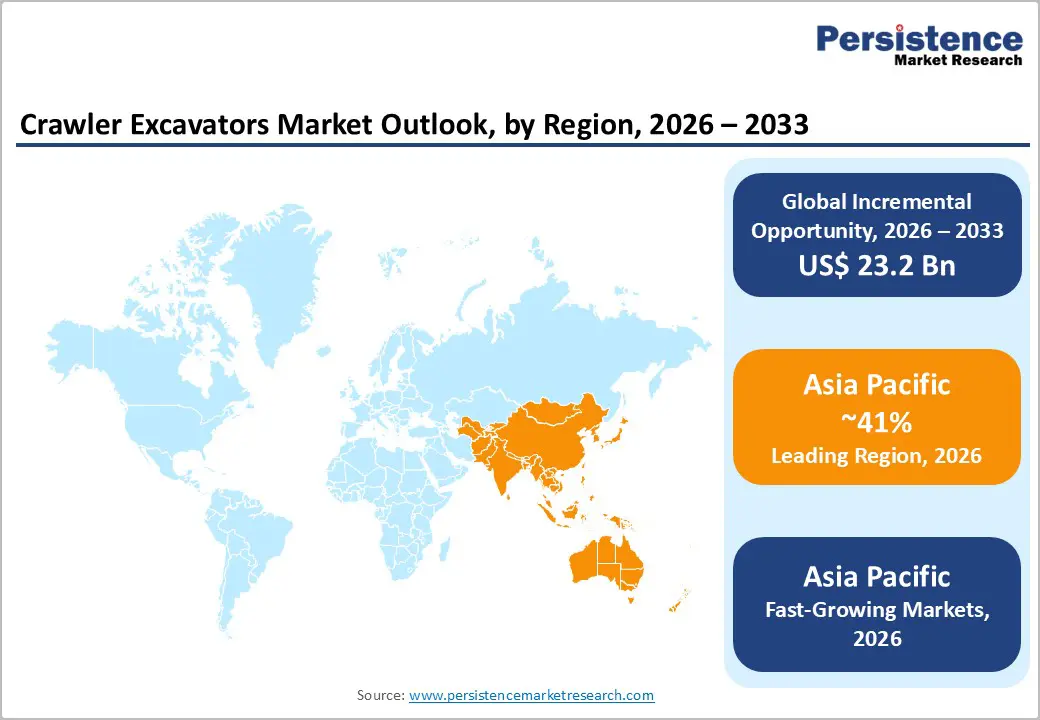

- Leading Region: Asia Pacific leads the global crawler excavators market holding 41% share, supported by strong demand in India and China. Companies like SANY Group, XCMG, and LiuGong drive growth through competitive pricing and expanding global networks.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with rising CAGR of 9.1%, driven by large infrastructure programs such as India’s National Infrastructure Pipeline, Indonesia’s strategic projects, and strong investment demand estimated by Asian Development Bank through 2030.

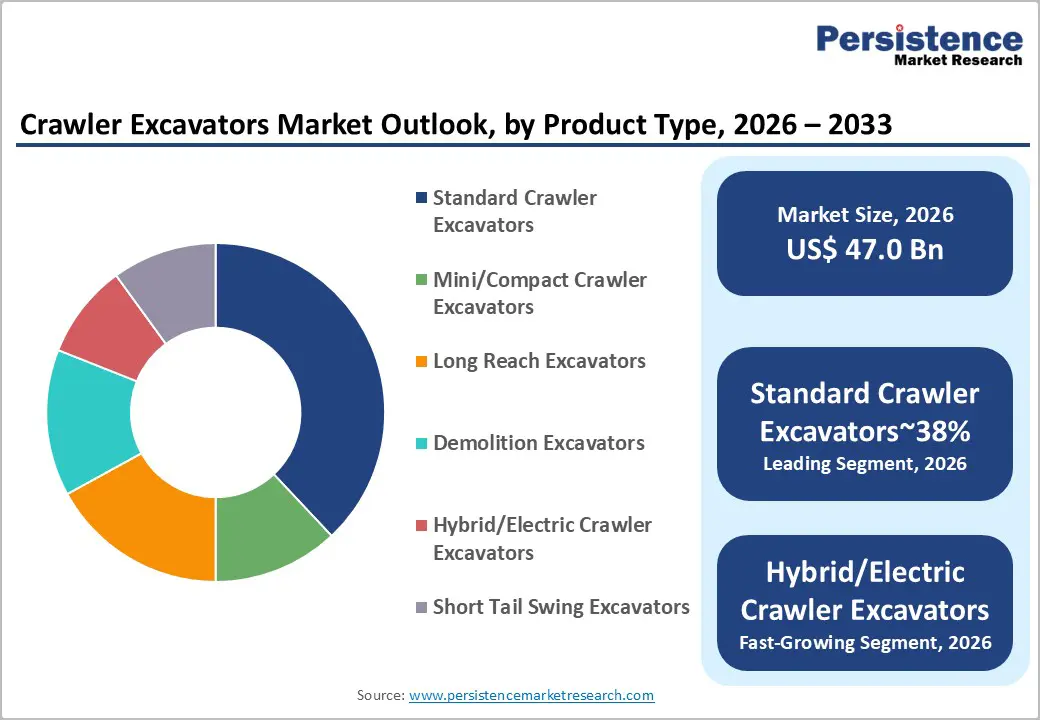

- Leading Segment: Standard crawler excavators dominate with around 38% share, especially the 18.1-25.0 tonne range. Their versatility supports applications like road construction, excavation, and quarrying, making them the most widely used equipment globally.

- Fastest-Growing Segment: Hybrid and electric crawler excavators are the fastest-growing segment, offering fuel savings and lower emissions. Innovations from Volvo Construction Equipment and Tata Hitachi Construction Machinery highlight a strong industry focus on electrification and sustainability.

- Key Opportunity: Mining sector expansion and rising demand for critical minerals create long-term opportunities. According to the International Energy Agency, increasing mineral demand and exploration projects will drive sustained excavator procurement globally.

| Key Insights | Details |

|---|---|

| Crawler Excavators Market Size (2026E) | US$ 47.0 Billion |

| Market Value Forecast (2033F) | US$ 70.2 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.9% |

| Historical Market Growth (2020 - 2025) | 4.6% |

DRO Analysis

Drivers - Large-Scale Global Infrastructure Investment Programmes Generating Sustained Earthmoving Equipment Demand

A massive wave of public infrastructure investment across North America, Europe, Asia Pacific, and the Middle East is the strongest driver for the crawler excavators market. Every major project, whether roads, railways, ports, dams, or urban development, requires large-scale earthmoving, excavation, grading, and material handling, which crawler excavators are best suited to perform efficiently.

The U.S. Bipartisan Infrastructure Law allocates US$ 1.2 trillion for infrastructure, while India’s National Infrastructure Pipeline commits over INR111 lakh crore through 2025 across multiple sectors. Additionally, the Asian Development Bank estimates that Asia alone will require US$ 1.7 trillion annually in infrastructure investment through 2030. This sustained global investment pipeline ensures continuous demand for crawler excavators, making infrastructure development a long-term, stable growth engine for the market.

Mining Sector Revival and Mineral Exploration Expansion Driving Heavy-Duty Excavator Procurement

The steady growth of the global mining sector is creating strong demand for heavy-duty crawler excavators. Increasing consumption of coal, iron ore, copper, lithium, and other critical minerals, essential for industrial production and clean energy technologies, is driving mining activity worldwide. These operations require large excavators capable of handling high-intensity workloads in harsh environments. The International Energy Agency projects that demand for critical minerals could grow up to six times by 2040, significantly boosting mining investments.

Countries such as India, Indonesia, Australia, and several African nations are expanding exploration and extraction activities, supported by favourable policies like 100% FDI in mining in India. This ongoing expansion ensures continuous procurement and replacement of excavators, making mining one of the most stable and long-term demand drivers in the crawler excavators market.

Restraints - Stringent Emission Regulations and Diesel Engine Phase-Out Pressures Increasing Compliance Costs

Tightening emission regulations for off-road diesel engines are significantly increasing the cost of manufacturing crawler excavators. Standards such as EPA Tier 4 Final in the U.S., EU Stage V in Europe, and CPCB IV+ norms in India require advanced emission control technologies like Diesel Particulate Filters, Selective Catalytic Reduction systems, and Diesel Oxidation Catalysts. These additions raise production costs by thousands of dollars per unit, directly impacting equipment pricing.

As a result, entry-level machines become less affordable, particularly in price-sensitive regions like Southeast Asia, Africa, and Latin America. Many small contractors and fleet owners in these markets struggle to absorb the higher costs without financial support or subsidies. This creates a barrier to adoption and slows down market expansion, especially where access to financing and government incentives is limited.

Skilled Operator Shortage and High Total Cost of Ownership Constraining Market Penetration

A shortage of skilled crawler excavator operators is a major challenge affecting the industry globally. Construction companies are often unable to fully utilise equipment due to the lack of trained professionals, which discourages further fleet expansion. Surveys indicate that a large majority of construction firms face difficulty hiring qualified equipment operators, and this issue is consistent across developed and emerging markets.

In addition, the total cost of owning and operating crawler excavators, including fuel, maintenance, insurance, and wages, remains high. These costs put pressure on small and medium contractors, who make up the bulk of the customer base. As a result, many businesses delay equipment purchases or rely on rentals instead. This combination of labour shortages and high ownership costs continues to limit overall market growth potential.

Opportunities - Rapid Adoption of Hybrid and Electric Crawler Excavators Creating a High-Growth Premium Segment

The shift toward low-emission and zero-emission construction equipment is creating a strong growth opportunity in hybrid and electric crawler excavators. Governments are enforcing stricter environmental regulations, while companies are increasingly adopting ESG goals, driving demand for cleaner equipment. Hybrid excavators offer significant benefits, including 30% fuel savings and lower carbon emissions, making them attractive for cost-conscious and environmentally responsible operators.

The electric construction equipment segment is expected to grow rapidly, with strong demand in urban areas with emission restrictions. Leading manufacturers are already investing in this space, launching advanced hybrid and electric models to capture this high-value segment. These machines typically command higher prices and better margins, making them a strategic focus area for OEMs aiming to strengthen profitability and meet future regulatory requirements.

Telematics Integration, Fleet Management Technology, and Rental Business Model Expansion

The growing use of telematics, IoT-enabled systems, and AI-driven fleet management tools is transforming the crawler excavators market. These technologies allow operators to monitor equipment performance, predict maintenance needs, and optimise fuel usage, leading to improved efficiency and lower operating costs. As a result, buyers are increasingly prioritising machines with built-in connectivity features.

This trend is particularly strong among rental companies and small contractors, who focus on maximising equipment utilisation and reducing downtime. In markets like India, a large share of buyers comes from rental and small contractor segments, making digital capabilities a key purchasing factor. At the same time, the global shift toward equipment rental models is gaining momentum, as businesses prefer flexible access over ownership. This creates new revenue opportunities for manufacturers through connected services and long-term customer engagement.

Category-wise Analysis

Product Type Insights

Standard Crawler Excavators lead the product segment with around 38% market share, mainly due to their versatility and reliability across a wide range of applications. These machines are commonly used in residential construction, road development, industrial projects, and large-scale infrastructure works, making them essential for most construction activities. The 18.1-25.0 tonne category is especially popular in key markets like India, as it offers the right balance between power and flexibility for diverse job requirements.

Leading manufacturers such as Caterpillar, Komatsu, and SANY provide advanced models with improved fuel efficiency, better hydraulic performance, and integrated digital features. Their ability to serve different customer segments, from government projects to private contractors and rental companies, helps maintain their strong market position. Continuous innovation in performance and technology ensures that standard crawler excavators remain the preferred choice across global markets.

Bucket Capacity Insights

The medium bucket capacity segment (2.0-4.0 m³) holds the largest market share at approximately 46%, driven by its balance between productivity and flexibility. This range is widely used in various applications such as road construction, pipeline installation, foundation work, and mid-scale mining operations. These activities represent a significant portion of global construction work, ensuring consistent demand for medium-capacity machines.

Contractors prefer this segment because it offers efficient material handling without compromising on operational control. Data from major economies shows that mid-scale construction projects account for the largest share of total activity, directly supporting the dominance of this segment. Additionally, these machines are suitable for both urban and semi-urban environments, making them highly adaptable. Their ability to perform efficiently across multiple applications ensures that the medium bucket capacity segment continues to lead the market.

Drive Type Insights

Hydraulic drive systems dominate the crawler excavators market with an overwhelming 92% share, due to their superior performance and efficiency. These systems provide high torque, smooth operation, and precise control, which are essential for handling complex excavation tasks. Hydraulic technology allows operators to control multiple functions, such as lifting, digging, swinging, and travelling, simultaneously with accuracy and ease.

This level of control cannot be matched by mechanical systems at a similar cost level. Leading component manufacturers continue to improve hydraulic efficiency through innovations like variable displacement pumps and load-sensing systems. These advancements enhance fuel efficiency and overall machine performance. As a result, hydraulic systems remain the preferred choice for manufacturers and users alike. Their proven reliability and continuous technological improvements ensure their continued dominance in the crawler excavators market.

End-user Insights

Construction companies are the largest end-users of crawler excavators, accounting for around 44% of total market demand. These companies use excavators across a wide range of projects, including residential buildings, infrastructure development, and industrial construction. Large firms operate extensive fleets and maintain long-term relationships with equipment manufacturers, while small and medium contractors drive volume demand through frequent purchases and rentals.

In markets like India, smaller contractors form a significant portion of buyers, making them a key target segment for manufacturers. Their purchasing decisions are influenced by project demand, financing options, and equipment efficiency. Mining companies represent the second-largest segment, typically purchasing high-capacity excavators for large-scale operations. Due to their need for heavy-duty equipment, mining companies contribute higher revenue per transaction, making them an important and profitable customer group in the market.

Regional Insights

North America Crawler Excavators Market Trends

North America is a mature yet steadily growing market for crawler excavators, supported by large infrastructure investment programs. The U.S. Bipartisan Infrastructure Law, with funding of US$ 1.2 trillion, is driving demand across transportation, water, and energy projects. Government agencies and contractors are actively investing in equipment to support long-term development plans. Canada is also contributing through housing and infrastructure initiatives.

In addition, the region is leading in the adoption of hybrid and electric excavators due to strict environmental regulations and emission control policies. Equipment manufacturers are focusing on innovation, introducing advanced and sustainable machines to meet regulatory requirements. The strong presence of rental companies further supports market growth, as contractors increasingly prefer flexible equipment access. Overall, North America continues to offer stable growth opportunities driven by policy support and technological advancement.

Europe Crawler Excavators Market Trends

Europe’s crawler excavators market is shaped by strict environmental regulations and a strong focus on sustainability. Emission standards such as EU Stage V have increased the demand for advanced, low-emission equipment, pushing manufacturers to invest in hybrid and electric technologies. Countries like Germany, France, and the UK are key markets, driven by ongoing infrastructure maintenance, residential construction, and renewable energy projects. Excavators are widely used in wind farm construction and other green energy developments.

European manufacturers are focusing on innovation, introducing new technologies to stay competitive in this highly regulated environment. Government initiatives supporting sustainability and infrastructure investment continue to drive demand. At the same time, future regulations are expected to further tighten emission norms, encouraging faster adoption of clean technologies. This makes Europe a technologically advanced and environmentally driven market for crawler excavators.

Asia Pacific Crawler Excavators Market Trends

Asia Pacific is the largest and fastest-growing market for crawler excavators, driven by strong construction and mining activity across major economies. Countries such as China, India, Japan, and Australia contribute significantly to global demand. While China remains the largest market, growth in India and Southeast Asia is accelerating due to infrastructure development and government investment programs.

India, in particular, is witnessing strong growth supported by road construction, railway expansion, and mining sector development. ASEAN countries are also investing heavily in infrastructure, creating new opportunities for equipment manufacturers. Meanwhile, Australia’s mining industry continues to generate demand for high-capacity excavators. Regional manufacturers are expanding their presence globally, offering competitive pricing and strong product performance. Overall, Asia Pacific remains the key growth engine for the global crawler excavators market.

Competitive Landscape

The global crawler excavators market is moderately consolidated, with a few major players holding significant market share. Leading companies such as Caterpillar, Komatsu, Hitachi, Volvo, Liebherr, and SANY dominate the market through strong product portfolios and global distribution networks. At the same time, Chinese manufacturers are gaining traction by offering cost-effective solutions, especially in emerging markets. Competition is driven by factors such as product performance, emission compliance, digital features, and after-sales service support.

Manufacturers are increasingly focusing on innovation, developing hybrid and electric models, as well as integrating advanced technologies like telematics and automation. New business models, including equipment leasing and subscription services, are also emerging. These strategies help companies attract a wider customer base and create long-term revenue streams. Overall, the competitive landscape is evolving with a strong focus on technology and customer-centric solutions.

Key Developments:

- September 2024: Volvo Construction Equipment introduced hybrid EC400 and EC500 crawler excavators designed to improve fuel efficiency and reduce CO2 emissions. These models target emission-regulated markets in Europe and North America, supporting sustainable construction and lower operating costs.

- January 2025: Tata Hitachi launched the EX 210LC Electric excavator at BAUMA Conexpo India, offering zero tailpipe emissions and lower operating costs. The launch aligns with India’s sustainability goals and increasing demand for eco-friendly construction equipment solutions.

- March 2025: SANY Group announced a new manufacturing facility in Indonesia to expand its global footprint. The move aims to strengthen its presence in ASEAN markets by enabling localized production, reducing lead times, and lowering import costs.

Companies Covered in Crawler Excavators Market

- Caterpillar Inc.

- Komatsu Ltd.

- Hitachi Construction Machinery

- Volvo Construction Equipment

- Liebherr Group

- SANY Group

- XCMG Group

- Hyundai Construction Equipment

- Doosan Infracore

- Kobelco Construction Machinery

- Deere & Company

- CNH Industrial

- JCB

- Kubota Corporation

- LiuGong Machinery

- Tata Hitachi Construction Machinery

- Sumitomo Construction Machinery

- Zoomlion Heavy Industry

- Takeuchi Manufacturing Co., Ltd.

Frequently Asked Questions

The global Crawler Excavators Market is projected to reach US$ 70.2 billion by 2033, growing at a CAGR of 5.9% from 2026.

Key demand drivers include large-scale infrastructure investments, mining sector expansion, and increasing adoption of hybrid and electric excavators.

Standard crawler excavators lead the market with around 38% share due to their versatility across applications.

Asia Pacific dominates the global market, driven by strong demand from India and China.

The main growth opportunity lies in hybrid and electric crawler excavators, driven by emission regulations and fuel efficiency benefits.

Leading companies include Caterpillar Inc., Komatsu Ltd., Hitachi Construction Machinery, Volvo Construction Equipment, and SANY Group.