- Pharmaceuticals

- Corticosteroid Market

Corticosteroid Market Size, Share, and Growth Forecast, 2026 - 2033

Corticosteroid Market by Product Type (Glucocorticoids, Mineralocorticoids), Route of Administration (Topical Route, Inhaled Forms, Oral Medications, Injectable), Application (Skin Allergies & Dermatological Disorders, Rheumatology Indications, Endocrinology, Respiratory Diseases, Gastroenterology, Others), and Regional Analysis for 2026 - 2033

Corticosteroid Market Share and Trends Analysis

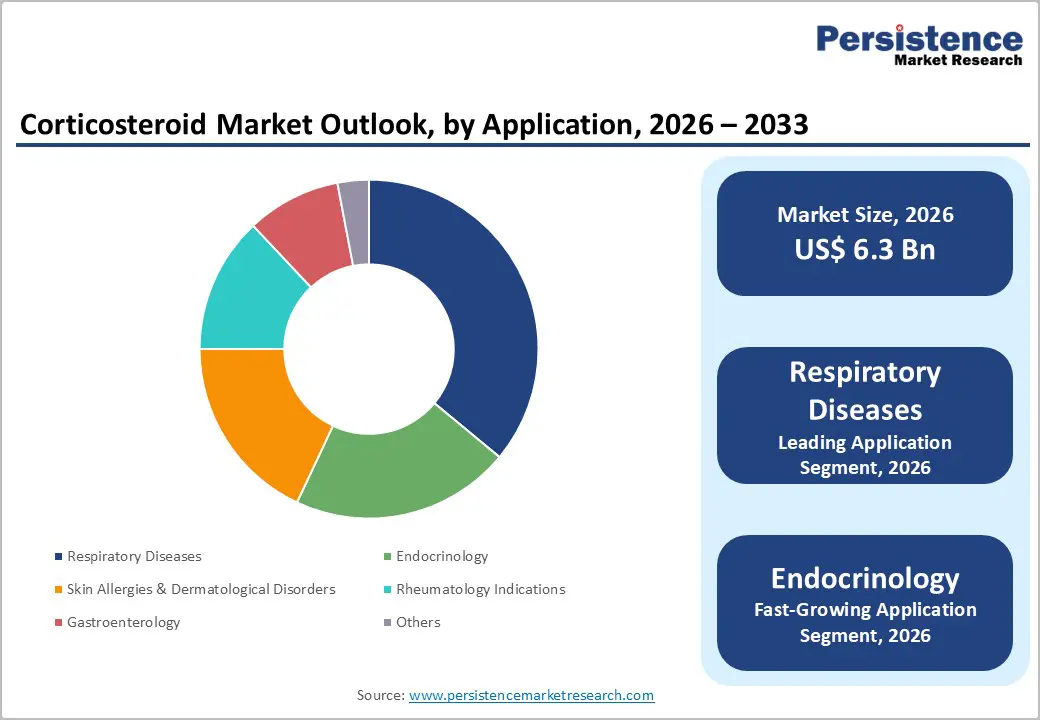

The global corticosteroid market size is likely to be valued at US$ 6.3 billion in 2026 and is estimated to reach US$ 9.1 billion by 2033, growing at a CAGR of 5.4% during the forecast period 2026 - 2033.

Market expansion is driven by the rising prevalence of inflammatory and autoimmune conditions and the increasing demand for effective anti-inflammatory therapies. Aging populations and higher chronic disease incidence amplify treatment adoption, as older patients show greater susceptibility to conditions treated with corticosteroids.

Enhanced clinical awareness among healthcare providers supports early diagnosis and timely prescriptions, sustaining use. Integration of digital health and telemedicine improves treatment monitoring, adherence and reduces hospital readmissions. Strengthened healthcare infrastructure, especially in outpatient and hospital settings, ensures consistent corticosteroid supply, enabling wider patient access and supporting long-term market growth.

Key Industry Highlights

- Leading Product Type: Glucocorticoids are set to hold around 68% market share in 2026, supported by clinical efficacy, treatment versatility, and broad provider acceptance.

- Fastest-Growing Product Type: Mineralocorticoids are likely to grow the fastest from 2026 to 2033, fueled by rising awareness of adrenal insufficiency

- Leading Application: Respiratory indications are anticipated to command around 36% of the market in 2026, driven by clinical guideline endorsement for asthma and COPD.

- Fastest-Growing Application: Endocrinology indications are expected to be the fastest-growing segment from 2026 to 2033, fueled by increasing awareness of adrenal insufficiency.

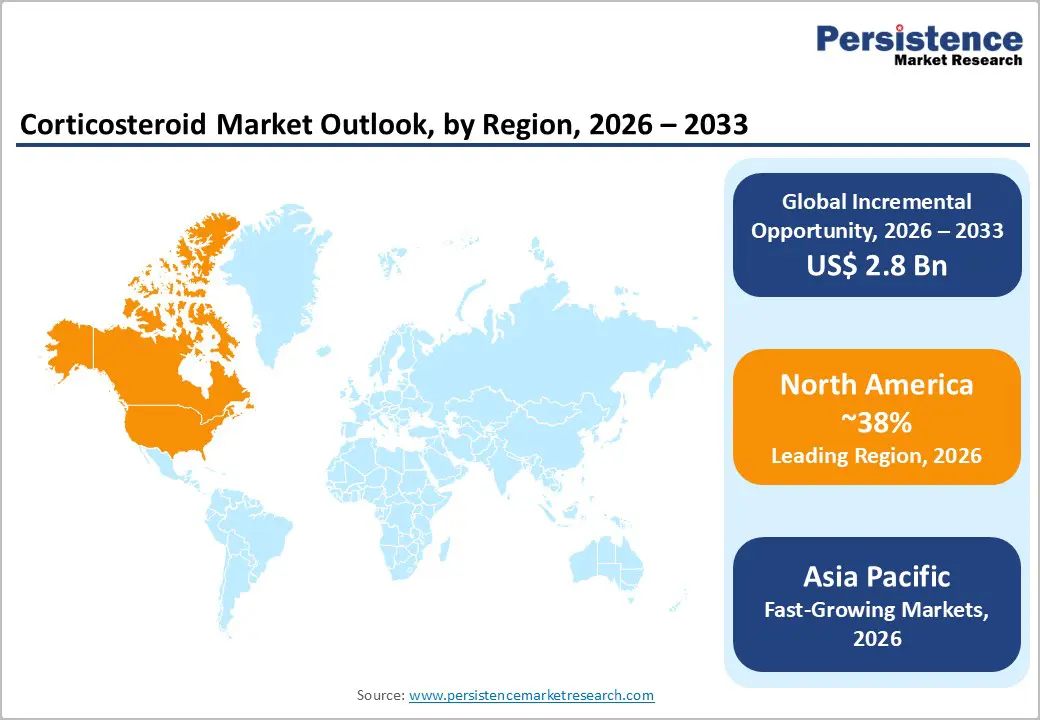

- Regional Leadership: North America is projected to capture nearly 38% market share in 2026, while Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, stimulated by rising disease prevalence and healthcare infrastructure investment.

- Competitive Environment and Innovation Trends: Key players such as Pfizer, GSK, Novartis, AstraZeneca, and Sanofi focus on formulation innovation, digital integration, geographic expansion, and strategic partnerships, enhancing adoption, differentiation, and long-term market scalability.

| Key Insights | Details |

|---|---|

| Corticosteroid Market Size (2026E) | US$ 6.3 Bn |

| Market Value Forecast (2033F) | US$ 9.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

DRO Analysis

Driver - Demographic Expansion and Chronic Disease Prevalence

The aging of populations in major economies drives structural increases in demand for corticosteroid therapy through enlargement of susceptible cohorts. Older adults, who represent a larger share of the demographic mix in the United States and other high-income regions, carry higher rates of musculoskeletal disorders, respiratory conditions, and autoimmune diseases requiring anti-inflammatory intervention; this trend expands patient volumes and stabilizes recurring treatment cycles over time.

Rising life expectancy supports longer treatment horizons for chronic conditions, deepening lifetime pharmaceutical consumption. In 2025, about 76.4% of U.S. adults lived with at least one long-term chronic condition, reflecting broad base demand for symptomatic therapies across age groups.

Expanding prevalence of multiple chronic conditions intensifies operational pressure on providers and payers, extending corticosteroid usage across care settings. Providers adjust formularies and standard treatment protocols to address comorbid inflammatory states, smoothing adoption of corticosteroid regimens across acute flares and maintenance phases. A larger chronic disease population increases outpatient visits and prescriptions, lowering per-unit acquisition costs while expanding aggregate volume.

Insurers adjust reimbursement frameworks to account for persistent demand, embedding corticosteroids into chronic care pathways that influence utilization patterns. Epidemiologic trends push clinical decision-making toward early intervention and prophylactic control of inflammatory damage, reinforcing demand elasticity relative to population health burdens.

Technological Integration and Clinical Innovation

Technological integration drives growth by enhancing clinical workflows and expanding treatment accessibility. Telehealth platforms reduce access barriers for patients with mobility constraints or chronic conditions, supporting higher treatment initiation and follow-up rates. Electronic health records and secure data exchange streamline prescription adjustments, real-time monitoring, and dosing optimization. Digital analytics reduce administrative burden, improve operational efficiency, and support evidence-based decision-making.

Remote monitoring tools enable early identification of therapy-related complications, minimizing treatment disruptions. These systems expand provider capacity, strengthen geographic service coverage, and enable consistent patient engagement, creating structural improvements in therapy delivery and facilitating broader adoption across complex care settings.

Clinical innovation stimulates adoption through therapeutic differentiation and expanded clinical indications. Novel formulations and advanced delivery technologies improve pharmacokinetics, extend dosing intervals, and lower adverse event risks, increasing clinician confidence. Decision-support tools guide regimen selection according to patient risk profiles, enhancing use in complex cases. Real-world evidence generated through connected devices informs payer coverage decisions and reduces administrative friction.

Targeted clinician training accelerates adoption of best practices and optimizes outcomes. Biomarker-guided approaches refine patient selection, concentrating therapy in populations with highest benefit and cost-effectiveness, driving structural expansion in treatment utilization and operational efficiency across healthcare systems.

Restraint - Adverse Effect Profile and Clinical Risk Management

Widespread corticosteroid faces limitations due to a complex adverse effect profile, including immunosuppression, osteoporosis, hyperglycemia, and cardiovascular complications. These effects necessitate intensive clinical monitoring, dosage adjustments, and patient follow-up, increasing operational demands on healthcare providers. High-risk populations, including elderly patients and individuals with comorbidities, require tailored treatment plans, reducing broad prescription potential.

Adverse outcomes also trigger demand for supportive interventions, elevating overall treatment costs. Institutional protocols for managing side effects, combined with heightened physician caution, influence treatment duration and adoption patterns.

Clinical risk management adds economic and operational pressure on healthcare systems. Continuous patient monitoring, education programs, and adherence tracking require investment in skilled personnel and digital solutions. Regulatory compliance and adverse event reporting increase administrative responsibilities and operational overhead. Payers and providers may impose restrictions on coverage or treatment intensity to reduce liability exposure, affecting accessibility. Expansion into regions with limited monitoring infrastructure faces slower adoption, as providers prioritize safety and risk mitigation.

Price Sensitivity and Competitive Generic Landscape

Intense price sensitivity among healthcare providers and patients limits revenue potential and compresses profit margins for branded corticosteroid products. High out-of-pocket costs influence prescription decisions, encouraging substitution with lower-cost alternatives. Payers implement stringent reimbursement frameworks, promoting generics and discount programs, which intensify pricing pressure. Procurement departments in hospitals and pharmacies prioritize cost-effective options, impacting brand loyalty.

Smaller players compete aggressively on pricing, reducing differentiation opportunities. This environment forces manufacturers to focus on operational efficiency and strategic cost management to maintain profitability amid declining per-unit revenues.

Competition from generic equivalents amplifies market challenges. Patent expirations expand generic availability, driving volume-based price reductions. Multiple manufacturers offering therapeutically equivalent formulations create commoditized segments, limiting pricing power. Buyers leverage competitive bidding to secure favorable terms, weakening margins for all suppliers. High interchangeability accelerates adoption of generics, slowing branded product growth. Scale and supply chain efficiency determine competitiveness, as firms must optimize production costs while maintaining regulatory compliance.

Intense competition shapes investment priorities and operational strategies across the industry.

Opportunity - Emerging Market Expansion and Unmet Clinical Needs

Rapid economic growth and rising healthcare investment in emerging regions create significant expansion opportunities for corticosteroids. Urbanization and increasing household income expand access to specialized care, supporting adoption for chronic inflammatory and autoimmune conditions. US data indicate 4.6% of the population was diagnosed with autoimmune diseases in 2025, highlighting substantial unmet demand that mirrors trends in developing regions.

Health systems are improving diagnostic infrastructure and outpatient services, reducing time to therapy initiation. Insurance coverage expansion lowers out-of-pocket burdens, broadening treatment reach. Patient and clinician awareness campaigns drive therapy uptake, while streamlined regulatory frameworks enable faster entry of new corticosteroid formulations.

Persistent gaps in effective chronic disease management reinforce demand for corticosteroids. Conditions such as rheumatoid arthritis, asthma, and dermatological disorders maintain high prevalence without universally effective long-term solutions. Aging populations increase multi-morbidity, stressing current care protocols and elevating reliance on broad-spectrum agents. Limited access to biologics or specialists enhances corticosteroid utilization as default intervention.

Operationally, these agents provide immediate symptom control with predictable outcomes, sustaining prescriber preference. Growth in clinical trials focusing on safety optimization supports continued integration into standard treatment pathways. Expanding unmet needs sustain stable demand across acute and maintenance care settings.

Innovation in Formulation and Delivery Mechanisms

Market demand for advanced therapies positions novel formulation and delivery mechanisms as a key opportunity in the corticosteroids market. Improved formulations that reduce systemic exposure and enhance tolerability expand the prescriber pool by addressing side-effect and regimen complexity concerns. Targeted delivery systems, including inhaled, topical, and dry powder platforms, optimize pharmacokinetic efficiency, improving adherence and therapeutic outcomes.

Clinicians value predictable pharmacodynamics for chronic inflammatory and autoimmune conditions, supporting streamlined care pathways. Operational efficiency benefits arise from reduced administration time and lower resource requirements in clinical settings. Investment in formulation science drives product differentiation and strengthens market positioning, supporting broader adoption and growth.

Enhanced delivery mechanisms also create new demand channels by enabling therapy outside traditional clinical settings. Controlled-release systems and smart device interfaces improve patient convenience and long-term adherence, aligning with evolving care models. Prescription drug spending in the U.S. is projected to increase 9%-11% in 2025, reflecting rising therapy utilization and treatment intensity. Providers prioritize efficient delivery that minimizes dosing frequency and integrates into patient lifestyles.

Commercially, these innovations support premium pricing while meeting unmet clinical needs, driving adoption among payers and healthcare systems seeking cost-effective, high-adherence corticosteroid solutions.

Category-wise Analysis

Product Type Insights

Glucocorticoids are anticipated to secure around 68% of the corticosteroid market share in 2026, reflecting widespread clinical adoption for multiple indications, including respiratory, dermatological, and autoimmune conditions. Established efficacy in managing inflammation and immune dysregulation, supported by guidelines from the American College of Rheumatology and European Society of Endocrinology, drives physician preference. High patient adherence is enabled by oral, injectable, and inhaled formulations, while hospital pharmacies and outpatient clinics ensure accessibility. Extended-release and targeted formulations improve safety, and clinical education reinforces provider trust.

Mineralocorticoids are expected to be the fastest-growing segment during the 2026 - 2033 forecast period, propelled by rising recognition of adrenal insufficiency and electrolyte imbalance management. Endocrine Society guidelines highlight precise supplementation for Addison’s disease and congenital adrenal hyperplasia, driving clinical adoption. Low-dose oral formulations and patient monitoring tools enhance therapeutic accuracy and adherence. Integration into hospital and outpatient endocrine programs expands access, while targeted clinician and patient education support early diagnosis and optimized therapy, fostering adoption and sustained growth across diverse healthcare settings.

Application Insights

Respiratory diseases are likely to be the leading segment with a projected 36% of the corticosteroid market share in 2026 due to well-documented efficacy in asthma, chronic obstructive pulmonary disease (COPD), and acute respiratory inflammation. Guidelines from the Global Initiative for Asthma and Global Initiative for Chronic Obstructive Lung Disease endorse corticosteroids as a core treatment. Physicians use inhaled, oral, and injectable formulations for acute and long-term management. Simplified dosing, digital monitoring, and telemedicine enhance adherence, while hospital pharmacies, outpatient clinics, and retail chains ensure treatment continuity.

Endocrinology is anticipated to be the fastest-growing segment from 2026 to 2033, fueled by rising awareness of adrenal disorders, congenital adrenal insufficiency, and corticosteroid replacement therapy. Early diagnosis and precise hormone management under Endocrine Society guidelines drive demand for tailored therapy. Hospital endocrinology units and specialty outpatient clinics expand access, while digital platforms support dose optimization, adherence monitoring, and side-effect tracking. Integration of precision medicine and biomarker-guided therapy enhances clinical acceptance, creating scalable commercial opportunities for endocrinology-focused corticosteroid treatments across diverse healthcare settings.

Regional Insights

North America Corticosteroid Market Trends

North America is expected to lead with an estimated 38% of the corticosteroid market share in 2026, supported by established healthcare infrastructure and advanced clinical capabilities. High prevalence of inflammatory, autoimmune, and respiratory conditions drives consistent demand for corticosteroid therapy. Well-structured hospital and outpatient networks ensure timely drug availability and streamline patient access. Clinical adoption is reinforced by guideline-based treatment protocols issued by major professional organizations.

Comprehensive insurance coverage and reimbursement frameworks reduce patient cost barriers. Integration of digital health platforms supports treatment monitoring, adherence, and follow-up care, enhancing therapy outcomes and strengthening market penetration.

Strong pharmaceutical innovation contributes to market dominance. Research investments focus on targeted, extended-release, and patient-friendly formulations, improving safety and therapeutic efficacy. Physicians rely on diverse corticosteroid delivery options, including oral, injectable, and inhaled forms, for tailored treatment strategies. High patient adherence and preference for established therapies sustain volume-based growth. Collaborative initiatives between hospitals, clinics, and specialty pharmacies optimize supply chains and reduce drug shortages.

Regulatory efficiency and streamlined approval processes accelerate new formulation adoption. Concentrated clinical education programs promote informed prescribing practices, reinforcing brand preference and long-term market stability.

Europe Corticosteroid Market Trends

Europe is projected to maintain a significant position in the corticosteroid market due to structured healthcare systems and strong clinical adoption across multiple therapeutic areas. Germany drives demand with advanced hospital networks and specialty outpatient services, ensuring consistent access to therapy. The United Kingdom demonstrates high uptake supported by national health frameworks and guideline-driven prescribing. France and Italy focus on integrated care pathways for chronic inflammatory and autoimmune conditions, enabling coordinated treatment. Extensive insurance coverage reduces patient cost barriers, supporting access to oral, injectable, and inhaled formulations.

Innovation in formulations and treatment delivery supports market performance. Extended-release and targeted corticosteroids improve safety and adherence, reinforcing physician preference. Spain and the Netherlands emphasize digital health platforms for remote monitoring and telemedicine, optimizing therapy outcomes. Collaborative programs among clinics, hospitals, and pharmacies streamline supply chains and maintain product availability. Clinical education initiatives promote early diagnosis and precision dosing, while prevalence of autoimmune and inflammatory disorders sustains adoption across therapeutic areas.

Asia Pacific Corticosteroid Market Trends

Asia Pacific is forecasted to be the fastest-growing market for corticosteroid market between 2026 and 2033, stimulated by rising prevalence of chronic inflammatory and autoimmune conditions and expanding healthcare infrastructure. China demonstrates significant growth potential due to government investments in hospital expansions and specialty care programs. India shows rapid adoption driven by increasing patient awareness and improving insurance coverage. Urbanization and rising middle-class populations create demand for advanced treatment options.

Japan experiences steady uptake supported by technologically advanced hospitals and established clinical networks. South Korea demonstrates growth through integration of digital health solutions and telemedicine for treatment monitoring and adherence.

Healthcare system modernization supports rapid market expansion. Hospital networks in China and India implement corticosteroid therapy protocols aligned with international guidelines, enhancing clinical adoption. Pharmaceutical companies introduce cost-effective formulations targeting underserved regions, increasing accessibility. Specialty clinics in Japan and South Korea focus on endocrine and respiratory care, improving patient outcomes and therapy adherence.

Digital platforms track dosing, monitor side effects, and provide remote consultation, facilitating efficient care delivery. Collaborative programs between manufacturers, clinics, and pharmacies optimize supply chains, ensuring consistent availability. Market penetration is strengthened by clinician education initiatives promoting early diagnosis and precise therapy management.

Competitive Landscape

The global corticosteroid market exhibits a moderately consolidated structure, with several multinational pharmaceutical companies holding significant shares alongside smaller specialty firms. Leading players include Pfizer, GlaxoSmithKline, Novartis, and AstraZeneca, collectively accounting for a substantial portion of market revenue.

Market concentration is high in developed regions due to regulatory stringency, brand recognition, and established distribution networks, whereas emerging markets show a more fragmented competitive environment with domestic manufacturers and generic producers. Competitive positioning is influenced by innovation in formulations, delivery methods, and clinical evidence generation, which allows companies to differentiate offerings and strengthen provider trust.

Key Developments

- In October 2026, telehealth brand Hims & Hers and Starface veterans launched an at home investigational acne corticosteroid injection trial with an acne injection pen designed to deliver intralesional steroid therapy directly to inflammatory lesions outside clinical settings.

- In June 2025, Harrow announced acquisition of exclusive U.S. commercial rights for BYQLOVI™ (clobetasol propionate ophthalmic suspension) 0.05%, a newly approved corticosteroid for post-operative inflammation and pain management following ocular surgery.

- In May 2025, Eton Pharmaceuticals announced U.S. FDA approval for KHINDIVI™ (hydrocortisone) oral solution, a corticosteroid indicated for replacement therapy in pediatric patients with adrenocortical insufficiency, marking the first FDA-approved hydrocortisone liquid designed for accurate dosing in children.

Companies Covered in Corticosteroid Market

- Pfizer

- GlaxoSmithKline

- Novartis

- AstraZeneca

- Sanofi

- Bayer

- Mylan (Viatris)

- Eli Lilly

- Teva Pharmaceuticals

- Chugai Pharmaceutical

- Servier

- Fresenius Kabi

- Hikma Pharmaceuticals

- Sun Pharmaceutical Industries

- Ipsen

Frequently Asked Questions

The corticosteroid market is projected to reach US$ 6.3 billion in 2026.

Rising prevalence of inflammatory, autoimmune, and respiratory conditions drives demand for effective corticosteroid therapies.

The corticosteroid market is poised to witness a CAGR of 5.4% from 2026 to 2033.

Expansion of targeted, extended-release, and patient-friendly corticosteroid formulations presents significant market opportunities.

Some key market players include Pfizer, GlaxoSmithKline, Novartis, AstraZeneca, Sanofi, and Bayer.