- Executive Summary

- Global Chocolate Confectionery Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Mn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Challenges

- Key Trends

- COVID-19 Impact Analysis

- Forecast Factors – Relevance and Impact

- Value Added Insights

- Value Chain Analysis

- Key Market Players

- Regulatory Landscape

- PESTLE Analysis

- Porter’s Five Force Analysis

- Price Trend Analysis, 2025-2033

- Pricing Analysis, By Ingredient Base/Product Type

- Key Factors Impacting Product Prices

- Global Chocolate Confectionery Market Outlook

- Key Highlights

- Market Volume (Tons) Projections

- Market Size (US$ Mn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Mn) Analysis and Forecast

- Historical Market Size (US$ Mn) Analysis, 2020-2024

- Current Market Size (US$ Mn) Analysis and Forecast, 2025-2033

- Global Chocolate Confectionery Market Outlook: Ingredient Base

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis, By Ingredient Base, 2020-2024

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Ingredient Base, 2025-2033

- Dairy-based

- Vegan

- Market Attractiveness Analysis: Ingredient Base

- Global Chocolate Confectionery Market Outlook: Product Type

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis, By Product Type, 2020-2024

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Product Type, 2025-2033

- Bars

- Chips & Bites

- Truffles

- Pralines

- Bonbons

- Other

- Market Attractiveness Analysis: Product Type

- Global Chocolate Confectionery Market Outlook: Chocolate Type

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis, By Chocolate Type, 2020-2024

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Chocolate Type, 2025-2033

- Milk Chocolate

- Dark Chocolate

- White Chocolate

- Market Attractiveness Analysis: Chocolate Type

- Global Chocolate Confectionery Market Outlook: Sales Channel

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis, By Sales Channel, 2020-2024

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Sales Channel, 2025-2033

- B2B

- B2C

- Hypermarkets/Supermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

- Other

- Market Attractiveness Analysis: Sales Channel

- Key Highlights

- Global Chocolate Confectionery Market Outlook: Region

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis, By Region, 2020-2024

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Region, 2025-2033

- North America

- Latin America

- Europe

- East Asia

- South Asia and Oceania

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Chocolate Confectionery Market Outlook

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis, By Market, 2020-2024

- By Country

- By Ingredient Base

- By Product Type

- By Chocolate Type

- By Sales Channel

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Country, 2025-2033

- U.S.

- Canada

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Ingredient Base, 2025-2033

- Dairy-based

- Vegan

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Product Type, 2025-2033

- Bars

- Chips & Bites

- Truffles

- Pralines

- Bonbons

- Other

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Chocolate Type, 2025-2033

- Milk Chocolate

- Dark Chocolate

- White Chocolate

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Sales Channel, 2025-2033

- Hypermarkets/Supermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

- Other

- Market Attractiveness Analysis

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis, By Market, 2020-2024

- Europe Chocolate Confectionery Market Outlook

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis, By Market, 2020-2024

- By Country

- By Ingredient Base

- By Product Type

- By Chocolate Type

- By Sales Channel

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Country, 2025-2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Rest of Europe

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Ingredient Base, 2025-2033

- Dairy-based

- Vegan

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Product Type, 2025-2033

- Bars

- Chips & Bites

- Truffles

- Pralines

- Bonbons

- Other

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Chocolate Type, 2025-2033

- Milk Chocolate

- Dark Chocolate

- White Chocolate

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Sales Channel, 2025-2033

- Hypermarkets/Supermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

- Other

- Market Attractiveness Analysis

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis, By Market, 2020-2024

- East Asia Chocolate Confectionery Market Outlook:

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis, By Market, 2020-2024

- By Country

- By Ingredient Base

- By Product Type

- By Chocolate Type

- By Sales Channel

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Country, 2025-2033

- China

- Japan

- South Korea

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Ingredient Base, 2025-2033

- Dairy-based

- Vegan

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Product Type, 2025-2033

- Bars

- Chips & Bites

- Truffles

- Pralines

- Bonbons

- Other

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Chocolate Type, 2025-2033

- Milk Chocolate

- Dark Chocolate

- White Chocolate

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Sales Channel, 2025-2033

- Hypermarkets/Supermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

- Other

- Market Attractiveness Analysis

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis, By Market, 2020-2024

- South Asia & Oceania Chocolate Confectionery Market Outlook:

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis, By Market, 2020-2024

- By Country

- By Ingredient Base

- By Product Type

- By Chocolate Type

- By Sales Channel

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Country, 2025-2033

- India

- Indonesia

- Thailand

- Singapore

- ANZ

- Rest of South Asia & Oceania

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Ingredient Base, 2025-2033

- Dairy-based

- Vegan

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Product Type, 2025-2033

- Bars

- Chips & Bites

- Truffles

- Pralines

- Bonbons

- Other

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Chocolate Type, 2025-2033

- Milk Chocolate

- Dark Chocolate

- White Chocolate

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Sales Channel, 2025-2033

- Hypermarkets/Supermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

- Other

- Market Attractiveness Analysis

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis, By Market, 2020-2024

- Latin America Chocolate Confectionery Market Outlook:

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis, By Market, 2020-2024

- By Country

- By Ingredient Base

- By Product Type

- By Chocolate Type

- By Sales Channel

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Country, 2025-2033

- Brazil

- Mexico

- Rest of Latin America

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Ingredient Base, 2025-2033

- Dairy-based

- Vegan

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Product Type, 2025-2033

- Bars

- Chips & Bites

- Truffles

- Pralines

- Bonbons

- Other

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Chocolate Type, 2025-2033

- Milk Chocolate

- Dark Chocolate

- White Chocolate

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Sales Channel, 2025-2033

- Hypermarkets/Supermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

- Other

- Market Attractiveness Analysis

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis, By Market, 2020-2024

- Middle East & Africa Chocolate Confectionery Market Outlook:

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis, By Market, 2020-2024

- By Country

- By Ingredient Base

- By Product Type

- By Chocolate Type

- By Sales Channel

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Country, 2025-2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Ingredient Base, 2025-2033

- Dairy-based

- Vegan

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Product Type, 2025-2033

- Bars

- Chips & Bites

- Truffles

- Pralines

- Bonbons

- Other

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Chocolate Type, 2025-2033

- Milk Chocolate

- Dark Chocolate

- White Chocolate

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, By Sales Channel, 2025-2033

- Hypermarkets/Supermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

- Other

- Market Attractiveness Analysis

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis, By Market, 2020-2024

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details – Overview, Financials, Strategy, Recent Developments)

- Nestle S.A.

- Overview

- Segments and Product Type

- Key Financials

- Market Developments

- Market Strategy

- Mondelēz International, Inc

- The Hershey Company

- Barry Callebaut

- Mars, Inc.

- Ferrero Group

- Taza Chocolate

- Chocoladefabriken Lindt & Sprüngli AG

- Go Max Go Foods

- Divine Chocolate

- Hu Kitchen

- Montezuma's Chocolate

- Endangered Species Chocolate

- Wicked Cookies Ltd

- Others

- Nestle S.A.

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Processed Food

- Chocolate Confectionery Market

Chocolate Confectionery Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Chocolate Confectionery Market by Ingredient Base (Dairy-based, Vegan), by Product Type (Bars, Chips & Bites, Truffles, Praline, Bonbons, Others), by Chocolate Type (Milk, Dark, White), by Sales Channel (B2B, B2C), and Region for 2026 - 2033

Chocolate Confectionery Market Size and Trend Analysis

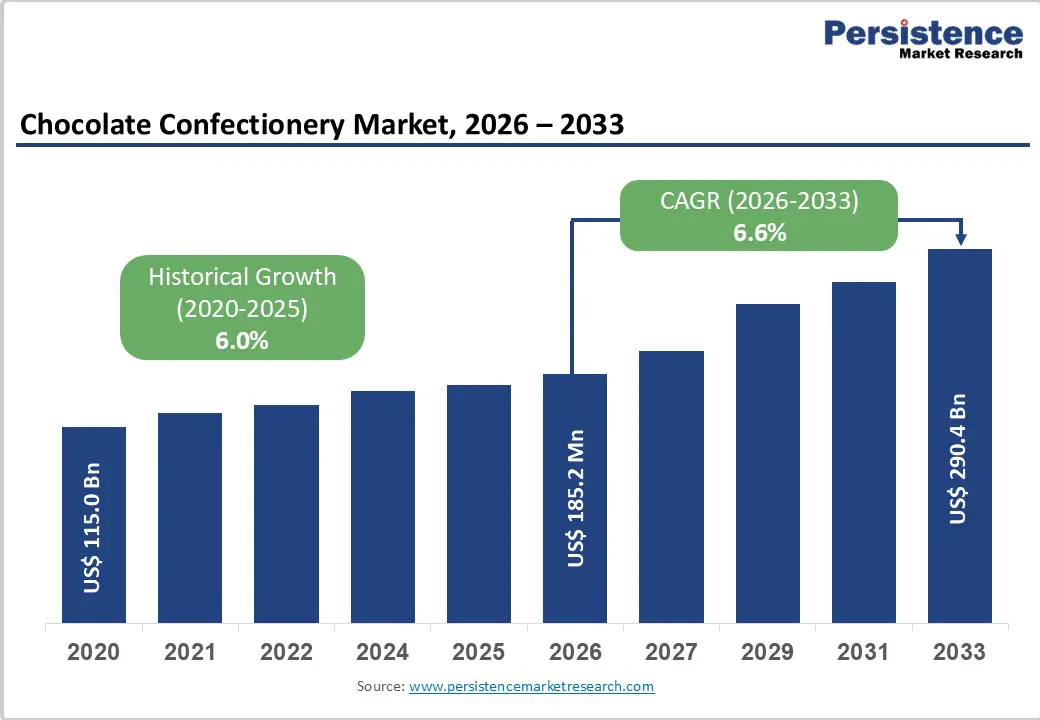

The global chocolate confectionery market is estimated to grow from US$185.2 billion in 2026 to US$290.4 billion by 2033. The market is projected to record a CAGR of 6.6% from 2026 to 2033. The chocolate confectionery market is a dynamic and continually evolving sector, offering a wide variety of chocolate-based products such as bars, truffles, pralines, and more. This segment is characterized by constant flavor experimentation, the rise of premium product lines, and the growing introduction of healthier alternatives that cater to shifting consumer preferences.

Driven by evolving consumer preferences and indulgence trends, the chocolate confectionery market is expanding worldwide. Rising demand for sweets, coupled with strategic marketing by leading industry players, continues to fuel this growth. A key driver is the increasing appetite for artisanal and premium chocolates, as consumers seek distinctive, high-quality products that deliver both uniqueness and superior taste. Moreover, the industry benefits from chocolate's adaptability as a constituent, facilitating the development of novel product combinations and the integration of unique flavours. Market expansion is bolstered by the expanding middle class, especially in emerging economies, where higher disposable incomes lead to increased spending on premium confectionery products. Furthermore, industry leaders' strategic partnerships, successful product introductions, and efficient promotional tactics significantly influence the market environment, stimulating competition and fostering innovation in the chocolate confectionery sector.

Key Industry Highlights

- Dominant Chocolate Type: Milk chocolate leads the chocolate confectionery market owing to its smooth texture, gentle sweetness, and universal appeal. Its adaptability across products such as bars, pralines, and snacks, combined with strong global branding, continues to strengthen its dominant position.

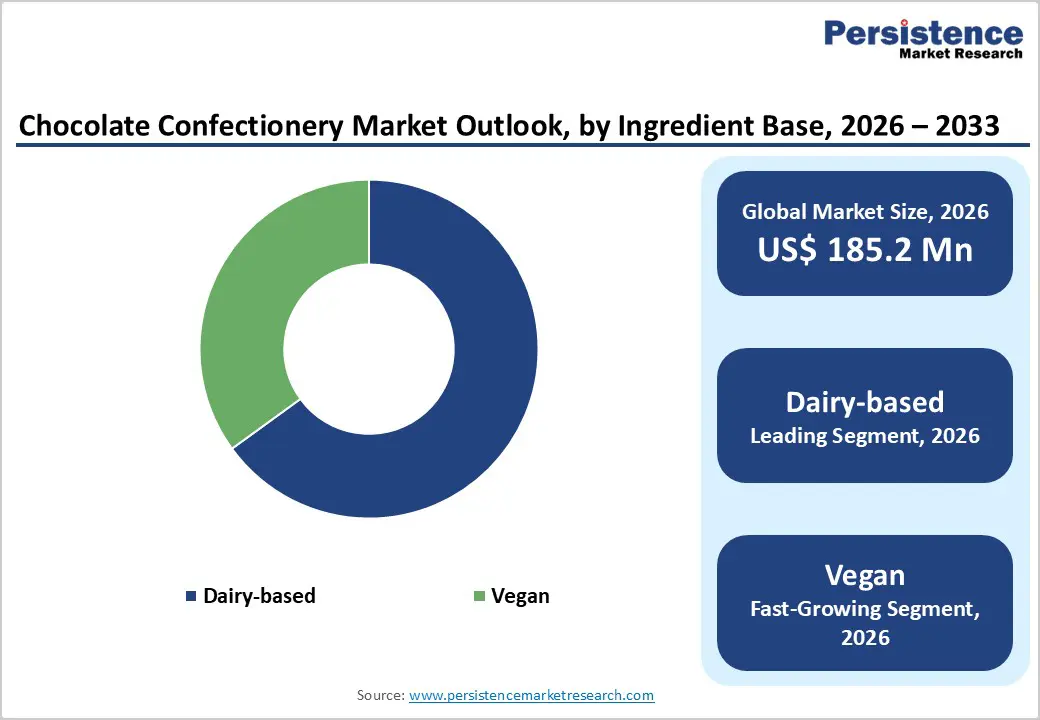

- Emerging Ingredient-based: Vegan chocolate is emerging as the fastest-growing segment in the confectionery market. Its expansion is driven by rising health consciousness, the popularity of plant-based diets, and increasing demand for sustainable alternatives, surpassing traditional dairy-based chocolate in global growth momentum.

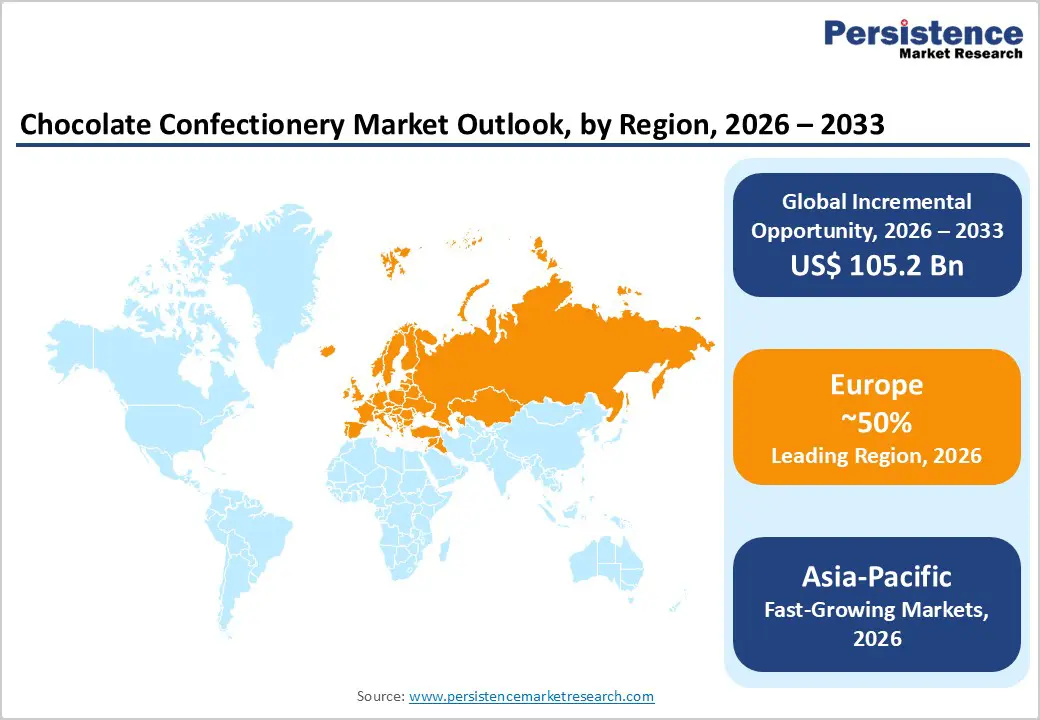

- Dominant Region: Europe leads the chocolate confectionery market thanks to its high per-capita consumption, deep-rooted cultural love for indulgent treats, and the dominance of global giants such as Hershey, Mars, and Lindt. Strong premiumization trends, innovation in healthier varieties, and robust retail networks further secure their market leadership.

- Investment Strategy: Growing demand for premium chocolates, an expanding gifting culture, and rising urban consumption highlight strong investment prospects in the chocolate confectionery market. Innovation in health-centric products, growth in digital retail, and increasing interest in sustainable, unique offerings further strengthen long-term market potential for committed brands.

| Key Insights | Details |

|---|---|

|

Chocolate Confectionery Market Size (2026E) |

US$ 185.2 Bn |

|

Market Value Forecast (2033F) |

US$ 290.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.0% |

Market Dynamics

Driver - Shifting Consumer Tastes Driving a Move Toward More Modern and Innovative Choices

Consumer preferences in the chocolate confectionery industry are shifting toward contemporary, health-aligned, and premium choices. Modern buyers increasingly look for reduced-sugar, vegan, plant-based, and high-cocoa chocolates that offer indulgence without compromising wellness goals. Interest in bold, global flavors is rising as consumers seek unique taste experiences inspired by diverse cultures. Brands now experiment with ingredients such as matcha, chilli, sea salt, and botanicals to stand out. For example, many artisanal chocolatiers have introduced orange-infused dark chocolate or chilli-spiked bars to cater to adventurous palates. This evolution reflects a broader desire for variety, authenticity, and elevated sensory satisfaction.

Lifestyle trends, digital influence, and ethical awareness are also redefining chocolate choices. Younger consumers prefer visually appealing chocolates discovered through social media, driving demand for ruby chocolate, textural inclusions, and handcrafted designs. Personalization is growing, with brands offering customizable assortments or flavor combinations. At the same time, value-driven purchasing is rising, with buyers choosing chocolates made from sustainably sourced cacao or fair-trade practices. For example, some brands now highlight cacao origins and support farming communities through transparent labelling. This fusion of ethics, aesthetics, and personalization reflects how contemporary consumers align chocolate consumption with identity, values, and emotional experiences.

The incorporation of cutting-edge technologies, such as 3D printing to produce customized confectionery or distinctive manufacturing processes, enhances the industry's ability to engage and captivate customers. By fostering a culture of innovation, businesses can both acquire and retain clients, thereby generating a demand cycle that drives market expansion.

Restraints - Unpredictable Fluctuation in Cacao Prices

A major challenge for the chocolate confectionery industry is the significant and unpredictable fluctuation in cacao prices, which disrupts stability across the entire supply chain. Because cocoa is the primary ingredient in chocolate, even small shifts in its cost can have immediate effects on production budgets, retail pricing, and overall profitability. This volatility has intensified in recent years, driven by environmental stressors, inherent structural issues within key producing regions, and various socio-economic pressures that collectively amplify instability in sourcing and pricing.

The instability of cocoa prices creates significant difficulties for chocolate manufacturers, as sudden increases in raw-material costs quickly elevate production expenses and narrow profit margins. This challenge is intensified by the industry’s strong dependence on cocoa sourced from West Africa, a region frequently affected by extreme weather patterns, crop diseases, and inconsistent harvests. Alongside environmental pressures, social and economic issues such as labor hardships, limited farming infrastructure, and broader community vulnerabilities further disrupt the reliability of the cocoa supply. Together, these factors heighten uncertainty across the chocolate confectionery value chain and increase long-term operational risks for producers.

Opportunity - Growing Demand for Premium and Artisanal Chocolates

The global chocolate confectionery industry is benefiting significantly from the growing consumer appetite for premium, artisanal, and handcrafted chocolates. As preferences evolve, there is a marked shift toward chocolates that offer superior quality, unique flavor profiles, and a sense of sophistication. Consumers in developed markets increasingly view chocolate not just as a sweet treat but as a form of luxury, an indulgence that carries aesthetic, sensory, and emotional value. This elevation of chocolate from a simple confection to an artisanal experience is opening new avenues for market expansion, particularly for brands that emphasize craftsmanship, storytelling, and refined presentation.

The rising demand for high-end and handcrafted chocolates also allows producers to differentiate their offerings and attract consumers who willingly pay a premium for exceptional quality. Artisanal chocolates, often made with meticulous attention to detail, rare ingredients, and origin-specific cacao, appeal to buyers seeking distinctive and memorable experiences. Brands that successfully position themselves in this premium segment can leverage consumers’ growing interest in unique flavors, single-origin varieties, and limited-edition creations. As spending patterns continue to favor luxury indulgences, chocolate manufacturers can broaden their premium portfolios, strengthen customer loyalty, and capture a niche audience that values not only taste but also the craft, heritage, and narrative behind each product.

Category-wise Analysis

By Ingredient-base, Dairy-based chocolate confectioneries lead the chocolate confectionery market

Dairy ingredients are extensively incorporated into chocolate confectionery because they significantly influence the product’s taste, texture, and handling properties during production. Whole and skimmed milk powders add the creamy, velvety mouthfeel characteristic of milk and white chocolates, while also shaping viscosity, melting behavior, and conching performance to achieve the ideal final consistency. Whole milk powder enriches chocolate with its natural milk fat and contributes subtle, caramelized flavors from the Maillard reaction, enhancing overall depth. Additionally, many regulatory standards mandate a minimum level of dairy solids in milk and white chocolate formulations, reinforcing their essential role.

Beyond enhancing flavor and texture, dairy ingredients also contribute to better product stability and improved cost efficiency in chocolate confectionery. Skimmed milk powder imparts the characteristic milky notes while influencing particle size distribution, resulting in a smoother texture and more consistent flow during processing. Buttermilk powder is commonly used as a cost-effective alternative, delivering a pleasant dairy flavor and helping reduce viscosity due to its natural phospholipid content. Milk powders are preferred over liquid milk because the moisture in liquid milk would cause the chocolate to seize, creating an undesirable gritty texture, making powdered dairy essential for proper manufacturing performance. Additionally, the use of different milk powders allows producers to fine-tune sensory qualities such as creaminess and sweetness, providing greater flexibility for diverse chocolate applications.

By Product type, Chocolate bars dominate the product type, showing impeccable growth due to their convenient and portable format

Chocolate bars dominate the market, accounting for more than 40% of all chocolate confectionery product types, due to their most convenient, versatile, and widely accessible format. Chocolate bars' dominance is driven by strong consumer appeal and practical advantages for manufacturers. They offer exceptional versatility, with options spanning various cocoa percentages, diverse flavor combinations, rich fillings, and price levels ranging from affordable everyday treats to luxury-crafted bars. Their convenient, portable format makes them ideal for impulse purchases, quick snacking, and on-the-go consumption. This ease of use, paired with their universal availability, gives chocolate bars an edge over more elaborate confectionery formats. Additionally, bars serve as a prime platform for experimentation and innovation. Manufacturers can rapidly introduce new textures, flavor inclusions, limited-edition variants, and seasonal offerings, keeping consumers engaged with fresh experiences and appealing to evolving taste preferences. Their widespread presence across retail channels, including supermarkets, convenience stores, vending machines, and online platforms, further amplifies their visibility and accessibility.

Chocolate bars are efficient and cost-effective to manufacture at scale, which strengthens their prevalence in the market. The streamlined production process allows companies to maintain consistent quality while keeping costs manageable, enabling both mass-market brands and premium chocolatiers to compete effectively. Bars also retain strong seasonal relevance, as limited-edition festive designs and flavors enjoy high demand during holidays and celebration periods. Collectively, these advantages, consumer-driven preferences, manufacturing efficiency, product flexibility, and broad retail reach make chocolate bars the most commercially successful and widely consumed product type within the chocolate confectionery industry.

Regional Insights

Europe Chocolate Confectionery Market Trends

Europe is expected to maintain the largest share of around 50% in the global chocolate confectionery market, supported by several strong such as strong shift toward premiumization, increasingly choosing high-quality, artisanal, single-origin, and luxury chocolate products, with Western Europe showcasing particularly strong preference for premium brands and ethically sourced cocoa offerings. This emphasis on sustainability and transparency reflects rising consumer expectations for responsible production. As a result, manufacturers are investing more heavily in craftsmanship, innovative flavor pairings, and enhanced textures to keep pace with evolving tastes and maintain engagement within a mature yet highly innovation-driven market.

Europe’s strong market position is further reinforced by its highly developed retail landscape, which includes extensive supermarket networks, specialty chocolate boutiques, convenience stores, and well-established e-commerce platforms. Leading chocolate manufacturers consistently invest in impactful marketing strategies, seasonal product launches, and continuous innovation to maintain high levels of consumer engagement. Combined with the region’s longstanding cultural appreciation of chocolate valued both as an everyday indulgence and a celebratory treat, these factors firmly anchor Europe’s leadership in the global chocolate confectionery sector. Its quick adoption of new trends and its influence on global consumer preferences ensure that Europe remains a major force shaping the future direction of the industry.

South Asia & Pacific Chocolate Confectionery Market Trends

South Asia and the Pacific region are projected to experience the fastest growth in the global chocolate confectionery market, driven by a combination of demographic and economic shifts. The region is home to a large, youthful, and increasingly affluent population, with a rapidly expanding middle class whose rising disposable incomes have broadened the customer base for chocolate products. As economic conditions improve, consumers begin to explore premium, international, and specialty chocolate varieties that were once considered luxuries. This shift reflects an evolving lifestyle in which chocolate is viewed not only as a treat but also as an aspirational indulgence.

Additionally, the diverse culinary traditions of South Asia and the Pacific offer chocolate manufacturers a unique opportunity to tailor products to local tastes. Flavors inspired by regional ingredients—such as cardamom, coconut, masala chai, matcha, or tropical fruits allow brands to create culturally resonant products that appeal to local consumers. The growing influence of Western food culture, coupled with digital exposure through social media and global e-commerce, has accelerated curiosity and acceptance of chocolate confectionery across these markets. For example, in India and Indonesia, major brands have successfully launched fusion chocolates combining traditional spices and fruits with classic milk chocolate, attracting young consumers seeking novelty and culturally familiar flavors.

Together, these dynamics of economic growth, rising aspiration, cultural adaptation, and digital influence position South Asia and the Pacific as the most rapidly expanding and opportunity-rich region for the chocolate confectionery industry.

Market Competitive Landscape

To secure and maintain a strong share of the global chocolate confectionery market, leading companies employ a wide range of strategic initiatives. One of the most critical strategies is continuous product innovation. Major players such as Mars, Mondelez International, Ferrero Group, Hershey’s, and Nestlé invest heavily in research and development to create new flavors, textures, formats, and packaging concepts. This commitment to innovation enables them to stay ahead of shifting consumer preferences, strengthen brand loyalty, and consistently excite the market with fresh and appealing chocolate offerings.

Equally important is the use of strategic marketing to reinforce brand presence and expand market reach. Through deliberate brand positioning, extensive advertising campaigns, and clear communication of product benefits, dominant chocolate brands cultivate strong emotional connections with consumers. A prime example is Hershey’s, which has successfully positioned itself as an enduring symbol of American culture and tradition—an approach that has significantly contributed to its widespread popularity and strong market influence.

In addition, leading companies prioritize global expansion to diversify their customer base and reduce dependence on individual regional markets. Ferrero Group, for instance, has strategically expanded through major acquisitions, including Ferrara Candy Company and Nestlé’s U.S. confectionery division. Such expansions allow these firms to broaden their product portfolios, tap into new consumer demographics, and strengthen their resilience against market volatility across different regions. The strategy of premiumization, innovation, and geographic diversification positioned Nestlé well for continued momentum into 2026.

Key Industry Developments:

- In February 2026, Nestlé demonstrated resilient growth in 2025 despite a challenging global environment marked by inflation in raw materials like cocoa and currency headwinds

- In February 2026, Puratos, a global leader in bakery, patisserie, and chocolate ingredients, announced that it will soon launch the world's first chocolate product for professionals containing cultured cocoa, becoming the first company to bring this breakthrough innovation to market.

- In October 2025, Ritter Sport established itself as one of the fastest-growing brands in the UK block chocolate category, with 20 squares sold every minute as of late 2025.

- In July 2025, Türkiye’s chocolate confectionery exports surge by 61%. The country achieved triple-digit growth in exports to key markets such as Belgium, Germany, the United States, France, the United Kingdom, Poland, Jordan, Hungary, Romania, Belarus, Lithuania, Australia, Norway, Czechia and Ukraine.

- In February 2025, Nestlé launched premium KitKat tablets featuring creamy, marbled, and layered chocolate to tap into the premium, shareable, and in-home consumption market.

Companies Covered in Chocolate Confectionery Market

- Nestlé S.A.

- Mondelēz International, Inc

- The Hershey Company

- Barry Callebaut

- Mars, Inc.

- Ferrero Group

- Taza Chocolate

- Chocoladefabriken Lindt & Sprüngli AG

- Go Max Go Foods

- Divine Chocolate

- Hu Kitchen

- Montezuma's Chocolate

- Endangered Species Chocolate

- Wicked Cookies Ltd

- Others

Frequently Asked Questions

The global Chocolate Confectionery market is projected to be valued at US$ 185.2 Bn in 2026.

Higher disposable incomes, rising demand for premium chocolate, innovative flavor development, habitual consumption, loyal customer bases, and a growing focus on indulgent but healthier chocolate choices are fueling market growth.

The Global Chocolate Confectionery market is expected to witness a CAGR of 6.6% between 2026 and 2033

Growing demand for premium chocolates, innovative flavor developments, health‑focused formulations, sustainable sourcing, expanding e‑commerce, and rising interest in artisanal, culturally inspired chocolate products.

A few major players in the Global Chocolate Confectionery market include Nestle S.A., The Hershey Company, Mars, Inc., Ferrero Group and Mondelēz International.