- Chipsets & Processors

- Chiplets Market

Chiplets Market Size, Share, and Growth Forecast, 2026 - 2033

Chiplets Market by Application (Data Center/AI Accelerators, Edge AI/Inference Accelerators, Others), Component (Processor Chiplets, Memory Chiplets, Others), Integration Technology, Customer, and Regional Analysis for 2026 - 2033

Chiplets Market Size and Trends Analysis

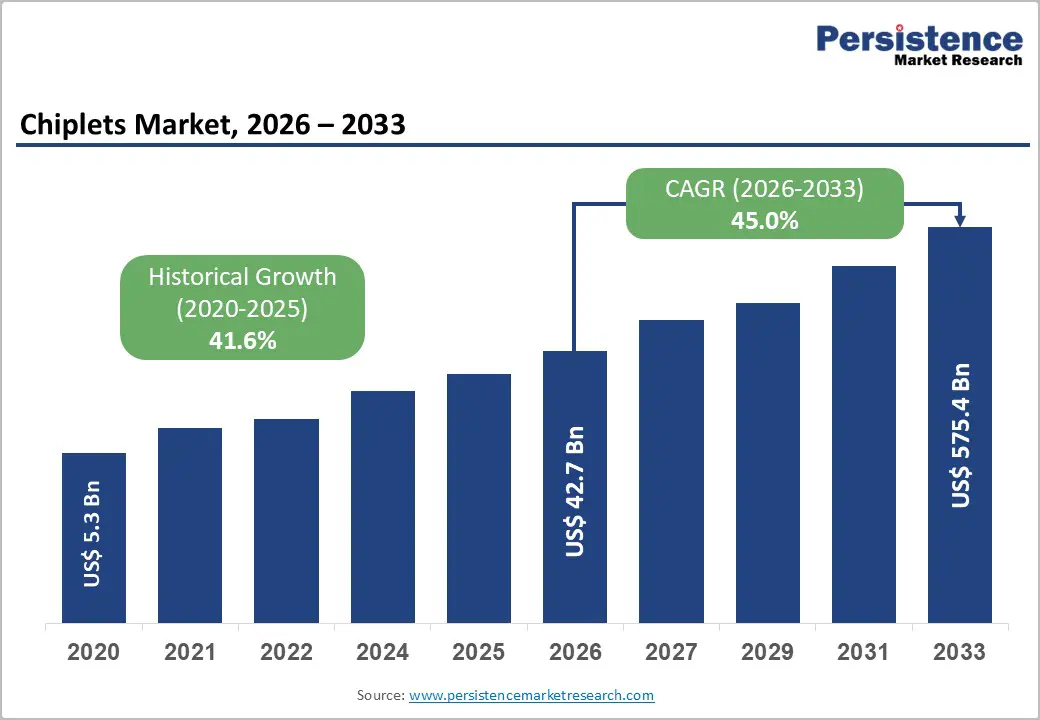

The global chiplets market size is likely to be valued at US$ 42.3 billion in 2026 and is expected to reach US$507.2 billion by 2033, growing at a CAGR of 42.6% between 2026 and 2033, driven by rising AI and hyperscale computing workloads, increasing demand for heterogeneous integration, and the industry-wide transition toward advanced packaging technologies.

Chiplet-based architectures are enabling semiconductor manufacturers to improve yield efficiency, optimize power consumption, and accelerate product development cycles while overcoming the limitations of monolithic chip scaling. The growing adoption of open interconnect standards and government-backed semiconductor localization initiatives is further strengthening long-term market expansion.

Key Industry Highlights:

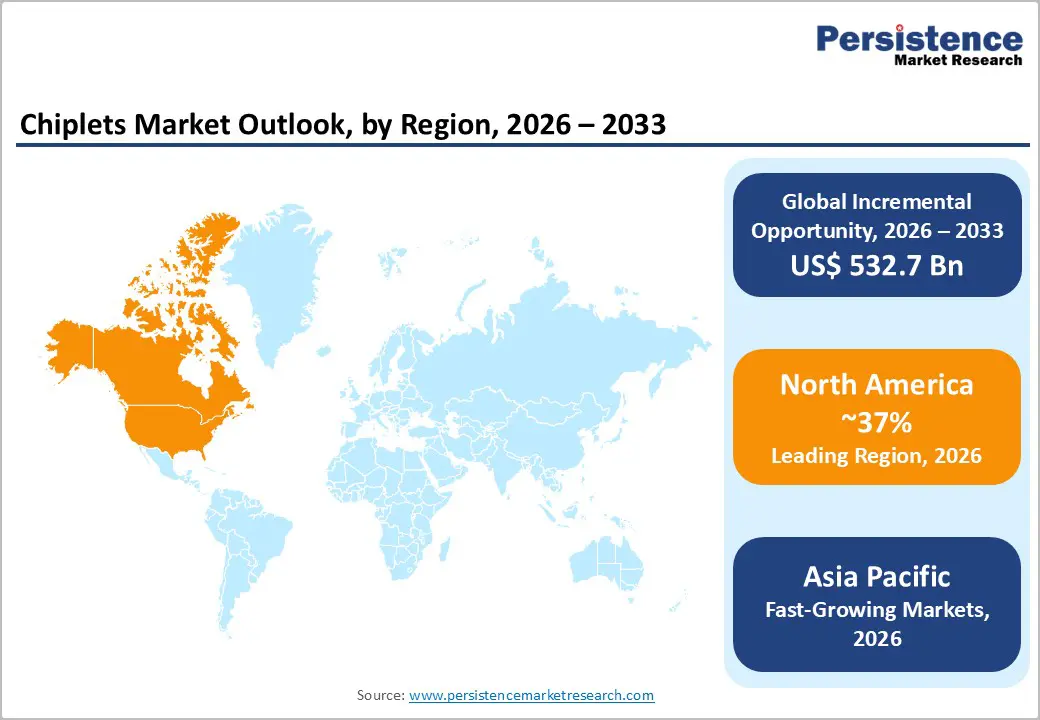

- Leading Region: Asia Pacific is projected to account for approximately 31.2% of the market share in 2026, due to strong semiconductor manufacturing, advanced packaging, and OSAT capabilities across Taiwan, South Korea, China, Japan, and ASEAN countries.

- Fastest-growing Region: Asia Pacific is projected to witness the fastest growth through 2033, supported by rising AI infrastructure investments, semiconductor localization initiatives, and expanding advanced packaging capacity in India, China, and Southeast Asia.

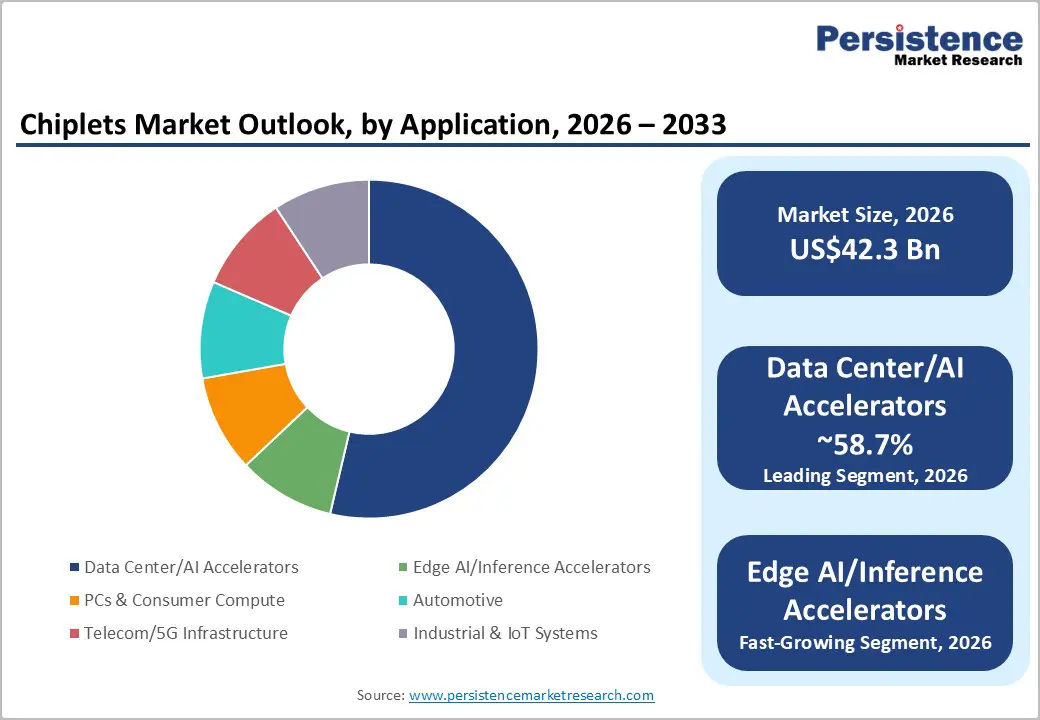

- Dominant Application: Data center/AI accelerators are anticipated to hold nearly 58.7% market share in 2026, due to increasing deployment of AI training systems, hyperscale cloud infrastructure, and high-performance computing platforms.

- Leading Component: Processor chiplets are expected to account for approximately 43.5% of the market share in 2026, owing to strong demand for CPU and GPU compute dies in AI accelerators, data-center processors, and advanced heterogeneous computing systems.

DRO Analysis

Driver - Rapid Expansion of AI and High-Performance Computing Infrastructure

The increasing deployment of artificial intelligence (AI), machine learning, and high-performance computing (HPC) infrastructure is significantly accelerating demand for chiplet-based architectures. AI training and inference systems require higher compute density, faster memory bandwidth, and improved energy efficiency, making chiplets a preferred design approach.

Chiplet architectures allow manufacturers to separate compute, memory, and I/O functions into optimized dies that can be integrated within a single package. This improves manufacturing yield and reduces development costs compared with large monolithic dies. Advanced packaging platforms such as CoWoS, Foveros, and EMIB are increasingly used in AI accelerators and next-generation GPUs. Major semiconductor companies are now designing scalable chiplet ecosystems to support rack-scale AI systems, which is substantially increasing chiplet content per computing platform and strengthening long-term market demand.

Growing Adoption of Open Interconnect Standards and Heterogeneous Integration

The development of standardized chiplet interconnect frameworks is reducing integration complexity and accelerating ecosystem adoption. Open standards such as Universal Chiplet Interconnect Express (UCIe) are enabling interoperability between dies manufactured by different vendors and fabricated on different process nodes. The release of UCIe 3.0 significantly improved bandwidth performance and enhanced support for scalable multi-chip system architectures.

One of the primary challenges associated with chiplet deployment was vendor dependency and proprietary integration frameworks. The emergence of open standards is addressing these barriers by enabling semiconductor companies, foundries, IP providers, and OEMs to collaborate within shared design ecosystems. Heterogeneous integration is also enabling companies to combine analog, digital, memory, and accelerator chiplets within a single package, improving design flexibility and reducing time-to-market.

Restraint - High Packaging Costs and Increasing Design Complexity

Despite strong growth potential, chiplet adoption continues to face challenges related to advanced packaging costs, yield management, and system-level validation complexity. Chiplet-based systems require sophisticated packaging technologies such as silicon interposers, fine-pitch bonding, and advanced substrate integration, which increase manufacturing costs compared with conventional semiconductor packaging approaches.

Testing and validation requirements are also becoming more complex because multiple dies must operate reliably within a unified package architecture. Thermal management, signal integrity, power delivery, and die-to-die communication reliability remain major engineering challenges, particularly for AI and HPC workloads. These factors increase development timelines and raise capital expenditure requirements for semiconductor manufacturers and OSAT providers.

The economic impact is especially significant for lower-margin applications where customers may not be able to absorb the premium pricing associated with advanced packaging technologies. As a result, chiplet deployment currently remains concentrated in high-value applications such as AI accelerators, premium GPUs, and data-center processors. Broader commercialization across mass-market devices will depend on reductions in packaging costs and improvements in manufacturing scalability.

Opportunity - Localization of Advanced Packaging and Semiconductor Supply Chains

Government-backed semiconductor manufacturing programs are creating major opportunities for chiplet ecosystem expansion. Several countries are investing heavily in domestic semiconductor fabrication, advanced packaging, and OSAT infrastructure to reduce supply-chain dependence and strengthen technological sovereignty.

The U.S. has announced significant funding initiatives under semiconductor manufacturing and advanced packaging programs, while Europe is expanding investment in semiconductor pilot lines, advanced packaging, and AI-oriented chip development. Asia-Pacific countries are also accelerating packaging capacity expansion to support growing AI infrastructure demand.

These initiatives are creating opportunities across the semiconductor value chain, including advanced substrates, thermal management systems, packaging equipment, die-to-die interconnect technologies, and chiplet IP development. Companies capable of supporting localized semiconductor ecosystems are expected to benefit from long-term investment inflows and strategic government partnerships.

Expansion of Edge AI, Automotive Electronics, and Industrial Computing

The adoption of chiplets in edge AI, automotive electronics, and industrial automation is creating a second major growth cycle for the market. Automotive OEMs are increasingly integrating chiplet-based architectures into advanced driver-assistance systems (ADAS), autonomous driving platforms, and software-defined vehicle architectures due to their scalability and processing efficiency.

Edge AI devices, including industrial vision systems, telecom edge servers, smart cameras, robotics platforms, and intelligent IoT infrastructure, require compact and energy-efficient semiconductor designs. Chiplets allow manufacturers to customize performance while reducing design complexity and improving lifecycle flexibility.

Industrial applications also benefit from modular semiconductor architectures as they support long operational lifecycles and regional supply-chain diversification. Emerging semiconductor manufacturing investments in India, Southeast Asia, and other developing regions are expected to strengthen packaging capacity and support wider adoption of chiplet-enabled computing systems across industrial and embedded applications.

Category-wise Analysis

Application Insights

Data center and AI accelerators are anticipated to account for nearly 58.7% of the market share in 2026, making them the leading application segment. Rising investments in generative AI, hyperscale cloud infrastructure, and HPC platforms are driving the adoption of chiplet-based GPUs and AI accelerators. Companies such as NVIDIA, AMD, and Intel are increasingly integrating compute dies, HBM stacks, and I/O chiplets within advanced packaging platforms such as CoWoS and Foveros to improve scalability and energy efficiency.

Hyperscalers, including Microsoft, Google, and Amazon, are deploying AI clusters that require high-bandwidth and modular semiconductor architectures. Continued expansion of AI training and inference workloads is expected to sustain strong demand for chiplet-enabled accelerator systems throughout the forecast period.

Edge AI and inference accelerators are anticipated to witness the fastest growth during the forecast period due to increasing deployment of AI-enabled edge devices across automotive, telecom, industrial automation, and consumer electronics sectors. Chiplets enable compact integration of NPUs, memory, and connectivity modules while improving power efficiency and reducing latency.

Examples include AI PCs, smart surveillance systems, factory automation controllers, and autonomous driving platforms. Growing adoption of edge AI infrastructure, industrial IoT, and 5G-enabled devices is expected to significantly accelerate demand for modular chiplet architectures in real-time inference applications.

Component Insights

Processor chiplets are anticipated to hold approximately 43.5% of the market share in 2026, making them the leading component category. CPU and GPU compute dies remain central to AI accelerators, HPC systems, and data-center processors because they deliver the highest computational value within advanced package architectures.

Companies such as AMD and Intel are increasingly adopting multi-die processor designs to improve yield efficiency, scalability, and thermal management. NVIDIA’s AI GPUs and AMD’s EPYC processors are prominent examples of chiplet-enabled compute platforms driving growth across hyperscale and enterprise computing environments.

Memory chiplets are anticipated to be the fastest-growing component segment during the forecast period, supported by rising adoption of HBM and advanced cache dielets in AI and HPC applications. Increasing AI model complexity is creating strong demand for high-bandwidth and low-latency memory integration.

HBM stacks integrated alongside GPU and accelerator chiplets are becoming critical in AI servers and large language model training systems. Companies such as Samsung, Micron, and SK hynix are expanding advanced memory solutions to support next-generation AI infrastructure. Growing use of HBM-enabled AI accelerators is expected to significantly strengthen demand for memory chiplets over the coming years.

Regional Insights

North America Chiplets Market Trends

North America remains a major hub for chiplet innovation, AI infrastructure, and advanced semiconductor packaging. Strong investments in AI computing, semiconductor manufacturing, and packaging localization are supporting regional market growth.

U.S. Chiplets Market Trends

The U.S. dominates the North America Chiplets Market due to strong investments in AI infrastructure, semiconductor manufacturing, and advanced packaging technologies. Government-backed semiconductor initiatives are accelerating domestic chip fabrication and packaging expansion. Companies such as Intel, NVIDIA, AMD, Broadcom, Synopsys, and Cadence are actively developing chiplet-enabled AI and HPC platforms.

The country also leads in hyperscale cloud infrastructure, with Microsoft, Google, Amazon, and Meta investing heavily in AI server deployments. Increasing adoption of AI accelerators, high-bandwidth memory integration, and advanced packaging solutions is expected to sustain strong market growth.

Canada Chiplets Market Trends

Canada is gradually strengthening its semiconductor ecosystem through investments in AI research, quantum computing, and advanced semiconductor design. The country benefits from growing collaboration between research institutions and semiconductor companies focused on AI processing and edge computing technologies.

Demand for chiplet-enabled systems is increasing across data analytics, telecommunications, and industrial automation applications. Canada’s growing AI startup ecosystem is also supporting regional innovation in next-generation semiconductor architectures.

Europe Chiplets Market Trends

Europe is strengthening its semiconductor ecosystem through industrial policies focused on supply-chain resilience, advanced packaging, and semiconductor innovation. The region is emphasizing automotive electronics, industrial AI, and research-driven chip development.

Germany Chiplets Market Trends

Germany leads the European market due to its strong automotive semiconductor industry and industrial automation sector. Investments in AI-driven manufacturing and advanced automotive electronics are increasing the demand for chiplet-based systems.

U.K. Chiplets Market Trends

The U.K. is focusing on semiconductor research, AI chip design, and advanced computing technologies. The country benefits from strong R&D capabilities and a growing interest in heterogeneous integration technologies.

France and Spain Chiplets Market Trends

France and Spain are expanding investments in semiconductor research programs, automotive electronics, and photonics technologies. Government support for semiconductor innovation is expected to strengthen long-term regional competitiveness.

Asia Pacific Chiplets Market Trends

Asia Pacific is expected to be the largest and fastest-growing regional market, accounting for approximately 31.2% of market share in 2026. The region dominates semiconductor manufacturing, advanced packaging, and OSAT operations.

Taiwan Chiplets Market Trends

Taiwan remains central to the global chiplet ecosystem because of its leadership in semiconductor foundry operations and advanced packaging technologies. The country plays a critical role in AI accelerator manufacturing, CoWoS packaging, and heterogeneous integration systems.

Strong demand from global AI infrastructure providers continues to support the expansion of advanced packaging capacity across Taiwan’s semiconductor industry.

China Chiplets Market Trends

China is investing heavily in semiconductor self-sufficiency, AI infrastructure, and domestic chip manufacturing. Rising AI server deployments and government support are strengthening regional demand.

Japan Chiplets Market Trends

Japan is focusing on advanced semiconductor manufacturing and next-generation chip technologies through major investments in high-end fabrication and packaging capabilities.

Competitive Landscape

The global Chiplets Market remains moderately fragmented at the semiconductor design level, while advanced packaging capacity remains comparatively concentrated among a limited number of global providers. Leading companies are competing through packaging innovation, interconnect standards, heterogeneous integration capabilities, and ecosystem partnerships.

Key market participants are focusing on advanced packaging innovation, ecosystem collaboration, and regional capacity expansion. Open interoperability standards, AI-focused product development, and strategic partnerships with hyperscalers and OEMs are becoming central competitive strategies. Companies are also investing heavily in localization initiatives to improve supply-chain resilience and support long-term semiconductor independence.

Key Industry Developments:

- In August 2025, the UCIe Consortium released UCIe 3.0, introducing higher bandwidth capabilities and improved interoperability standards for multi-chip and chiplet-based semiconductor architectures, strengthening ecosystem-wide adoption of heterogeneous integration technologies.

- In May 2025, NVIDIA Corporation launched NVLink Fusion, a semi-custom AI infrastructure platform designed to support scalable chiplet-style architectures and multi-vendor AI system integration through partnerships with MediaTek, Marvell, Synopsys, Cadence, and Qualcomm.

Companies Covered in Chiplets Market

- Taiwan Semiconductor Manufacturing Company (TSMC)

- NVIDIA Corporation

- Advanced Micro Devices (AMD)

- Intel Corporation

- Samsung Electronics

- ASE Technology Holding Co., Ltd.

- Amkor Technology, Inc.

- Broadcom Inc.

- Qualcomm Incorporated

- Marvell Technology, Inc.

- Micron Technology, Inc.

- SK hynix Inc.

- Synopsys, Inc.

- Cadence Design Systems, Inc.

- Arm Holdings plc

- IBM Corporation

Frequently Asked Questions

The global Chiplets Market is anticipated to be valued at approximately US$ 42.3 billion in 2026.

The Chiplets Market is projected to reach nearly US$ 507.2 billion by 2033.

Key trends include rising adoption of AI accelerators, increasing use of advanced packaging technologies such as 2.5D and 3D stacking, expansion of HBM-integrated architectures, growth of edge AI computing, and wider adoption of open interconnect standards such as UCIe.

Data Center/AI Accelerators represent the leading application segment, accounting for approximately 58.7% of the market share due to strong demand for AI training and hyperscale computing infrastructure.

The Chiplets Market is expected to grow at a CAGR of 42.6% between 2026 and 2033.

Major companies include TSMC, NVIDIA, AMD, Intel Corporation, and Samsung Electronics.