- Industrial Goods & Service

- Chest Freezer Market

Chest Freezer Market Size, Share, and Growth Forecast 2026 - 2033

Chest Freezer Market by Capacity (Below 200 Liters, 200-400 Liters, Above 400 Liters), Door Type (Solid Lift Door, Glass Sliding Door), Sales Channel (Online, Offline), End Use (Residential, Supermarkets & Hypermarkets, Restaurants & Hotels, Convenience Stores, Food Processing & Cold Storage, Pharmaceutical & Healthcare, Others), by Regional Analysis, 2026 - 2033

Chest Freezer Market Size and Trend Analysis

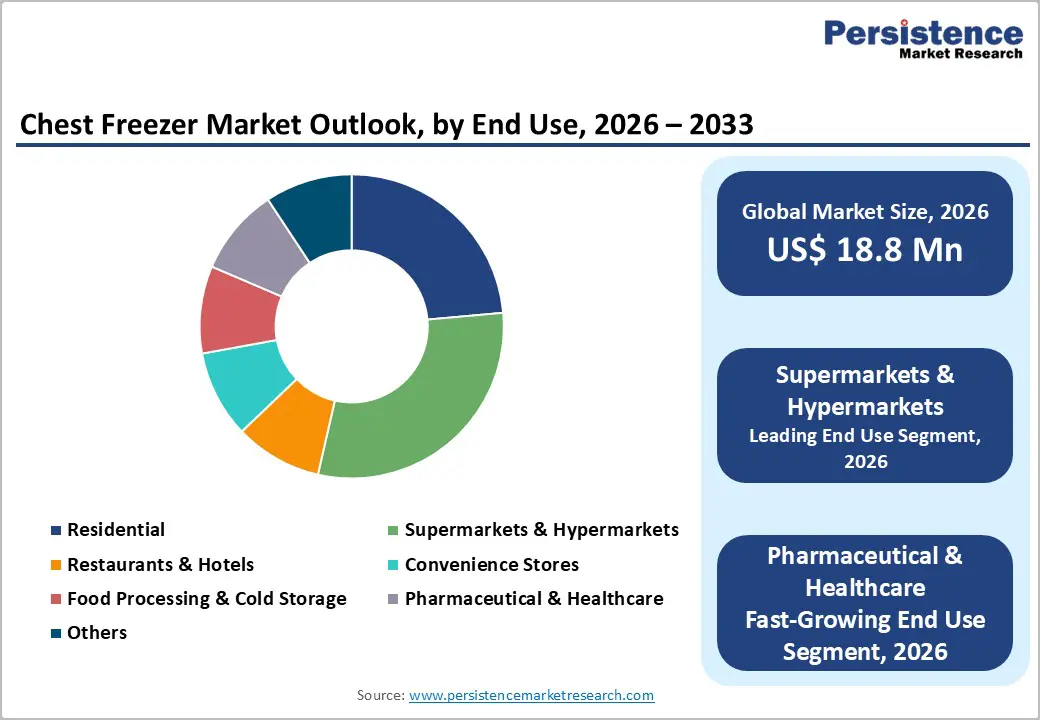

The global chest freezer market size is expected to be valued at US$ 18.8 Billion in 2026 and projected to reach US$ 30.2 Billion by 2033, growing at a CAGR of 7.0% between 2026 and 2033.

Robust demand for cold chain storage solutions, expanding food retail infrastructure in emerging economies, and rising consumer preference for bulk food purchasing are the primary forces driving sustained market growth.

The accelerating global cold chain investment, particularly across Asia Pacific, Latin America, and Middle East & Africa, is creating significant demand for chest freezers across both commercial and residential end-use segments. Simultaneously, increasing stringency of pharmaceutical cold storage requirements and the proliferation of organized food retail formats are reinforcing the relevance of chest freezers as essential refrigeration infrastructure. Energy-efficiency regulations and the transition to HFC-free refrigerants under the Kigali Amendment to the Montreal Protocol are further driving product innovation and replacement demand across established markets.

Key Industry Highlights

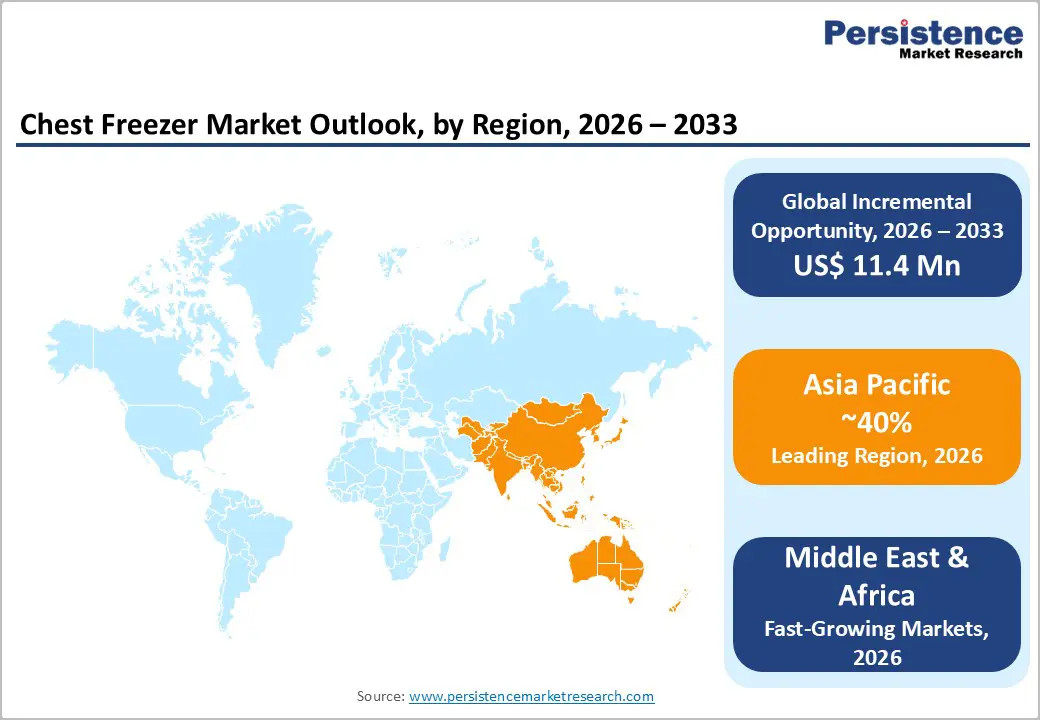

- Leading Region: Asia Pacific commands approximately 40% of global Chest Freezer market share in 2025, anchored by China's massive manufacturing base and growing organized food retail expansion across India, Vietnam, and Indonesia driving robust multi-year demand.

- Fastest Growing Region: The Middle East & Africa region is the fastest growing market, driven by rising cold chain infrastructure investment, expanding food retail networks under Saudi Vision 2030, and WHO-mandated vaccine cold storage programs across Sub-Saharan healthcare systems.

- Dominant Segment: The 200-400 Liters capacity segment leads with approximately 45% market share in 2025, preferred across convenience stores, small restaurants, pharmacies, and mid-size residential settings for its optimal balance of storage volume, footprint, and acquisition cost.

- Fastest Growing Segment: The Pharmaceutical & Healthcare end-use segment is the fastest growing category, driven by global vaccine distribution mandates, WHO cold storage standards, and expanding biologic drug supply chains requiring -20°C to -70°C certified chest freezer infrastructure.

- Key Market Opportunity: Tightening F-Gas regulations and energy efficiency mandates create strong demand for R-290-based inverter chest freezers with IoT monitoring capabilities, offering manufacturers premium pricing, regulatory compliance advantages, and long-term replacement cycle acceleration across global markets.

| Key Insights | Details |

|---|---|

| Chest Freezer Market Size (2026E) | US$ 18.8 Billion |

| Market Value Forecast (2033F) | US$ 30.2 Billion |

| Projected Growth CAGR (2026 - 2033) | 7.0% |

| Historical Market Growth (2020 - 2025) | 6.2% |

Market Dynamics

Drivers - Expanding Cold Chain Infrastructure and Organized Food Retail Growth

The rapid development of cold chain infrastructure across emerging and developed economies is a foundational growth driver for the chest freezer market. According to the Global Cold Chain Alliance (GCCA), global refrigerated warehouse capacity reached 719 million cubic meters in 2022, an increase of 6.4% over 2020 levels, driven by surging demand for temperature-controlled storage in food processing, retail, and pharmaceuticals. In parallel, the global organized food retail sector is expanding rapidly, with supermarket and hypermarket penetration growing significantly across India, Southeast Asia, and Africa. Large-format retail stores rely extensively on commercial chest freezers for frozen food display and back-of-store bulk storage. The World Bank estimates that post-harvest food losses in developing economies, often exceeding 30% of production, are prompting accelerated government investments in cold storage infrastructure, directly stimulating chest freezer procurement.

Rising Pharmaceutical Cold Storage Demand and Vaccine Distribution Requirements

The global pharmaceutical industry's growing need for temperature-controlled storage is emerging as a high-value demand driver for commercial chest freezers. The World Health Organization (WHO) guidelines require vaccines and temperature-sensitive biologics to be stored within strict ranges as low as -70°C to -20°C, necessitating ultra-low temperature (ULT) and standard chest freezer infrastructure across healthcare facilities, distribution hubs, and pharmacies globally. The global vaccine market is projected to exceed US$ 100 billion by 2028 according to the International Federation of Pharmaceutical Manufacturers & Associations (IFPMA), underpinning sustained demand for WHO-prequalified pharmaceutical chest freezers. Hoshizaki and Liebherr Group have both expanded their medical-grade chest freezer portfolios in response to this growing end-use segment, reflecting robust industry investment in pharmaceutical-grade cold storage.

Restraints - High Energy Consumption and Rising Electricity Costs

Chest freezers are among the highest energy-consuming household and commercial appliances, with standard commercial units consuming between 400 and 900 kWh annually. As electricity prices surged across Europe and North America, with EU average household electricity prices reaching €0.28/kWh in 2023 according to Eurostat, operational cost sensitivity has intensified, deterring price-sensitive residential and small commercial buyers from upgrading or expanding their freezer inventory. Energy labeling regulations under the EU Energy Label Regulation (EU) 2021/341 are also creating compliance cost pressures for manufacturers producing lower-efficiency models.

Refrigerant Transition Costs and Regulatory Compliance Complexity

The phasedown of high-global-warming-potential (GWP) hydrofluorocarbon (HFC) refrigerants under the Kigali Amendment to the Montreal Protocol is compelling manufacturers to redesign existing product lines to accommodate natural refrigerants such as R-290 (propane) and CO2 (R-744). The transition requires significant capital investment in new compressor technology, flammability safety engineering, and revised manufacturing processes. The U.S. EPA's AIM Act mandates an 85% reduction in HFC consumption by 2036, adding compliance urgency. Smaller manufacturers face proportionally higher transition costs, potentially consolidating market share among well-capitalized tier-1 players.

Opportunities - Adoption of Natural Refrigerants and Energy-Efficient Inverter Compressor Technology

The global shift toward natural refrigerant-based chest freezers, particularly using R-290 (hydrocarbon propane), presents a transformative product innovation opportunity for manufacturers. R-290 has a Global Warming Potential (GWP) of 3 compared to over 1,400 for HFC-134a, offering a compelling environmental advantage. The European Commission's F-Gas Regulation revision (2024) is accelerating market adoption of hydrocarbon-based systems across EU member states. Simultaneously, inverter compressor technology reduces chest freezer energy consumption by 30-40% compared to conventional fixed-speed models, qualifying products for premium energy efficiency ratings. Haier Group and Midea Group have already launched R-290-based inverter chest freezer lines targeting EU and North American markets, establishing a competitive benchmark for industry-wide adoption. Manufacturers investing in this technology are positioned to command premium pricing and accelerated regulatory compliance.

Rapid Expansion of E-Commerce Food Delivery and Dark Store Cold Storage

The explosive growth of online grocery delivery and the proliferation of dark stores, dedicated urban micro-fulfillment centers for rapid e-commerce food delivery, is creating a new, high-growth demand category for commercial chest freezers. According to the Food and Agriculture Organization (FAO), online grocery sales accounted for approximately 11% of total global food retail revenues in 2023, a figure expected to surpass 20% by 2030 in major urban markets. Each dark store typically operates 10-40 chest freezer units for frozen goods storage, representing a significant per-site equipment investment. Zomato's Blinkit in India, Getir in Europe, and DoorDash in the U.S. are aggressively expanding dark store networks, directly amplifying commercial chest freezer procurement volumes. Manufacturers offering compact, glass-door chest freezer models optimized for small-footprint micro-fulfillment environments are strongly positioned to capture this emerging demand segment.

Category-wise Analysis

Capacity Insights

The 200-400 Liters capacity segment is the leading category in the global chest freezer market, commanding approximately 45% of total market share in 2025. This capacity range offers an optimal balance between storage volume, installation footprint, and acquisition cost, making it the preferred choice across a broad spectrum of end-use settings, including convenience stores, small restaurants, pharmacies, and mid-size residential households. Units in this range typically accommodate 150-320 kg of frozen goods, providing sufficient storage for weekly or bi-weekly bulk purchasing by residential users and daily restocking by small food service operators. Compliance with energy efficiency standards is also more cost-effectively achieved in this mid-range capacity segment. The Above 400 Liters segment is the fastest growing category, driven by hypermarket, food processing, and pharmaceutical cold storage expansion requiring large-capacity bulk freezer solutions.

Door Type Insights

Solid Lift Door chest freezers represent the dominant door type category, accounting for approximately 62% of global market share in 2025. Solid lid models are preferred for residential, back-of-store commercial, and food processing applications primarily because of their superior thermal insulation performance. Solid lids minimize cold air loss during access compared to glass sliding door alternatives, resulting in lower energy consumption and reduced compressor cycling. This energy efficiency advantage is particularly relevant in markets with high electricity costs or strict energy labeling requirements. Solid lid chest freezers also offer greater structural durability and resistance to environmental condensation, making them preferred for high-humidity environments including food processing facilities and marine applications. Glass Sliding Door models are the fastest growing door type, gaining rapid traction in supermarkets, convenience stores, and dark store micro-fulfillment operations where frozen food visibility directly influences impulse purchase rates.

Sales Channel Insights

The Offline sales channel remains dominant in the global chest freezer market, representing approximately 68% of total revenue share in 2025. Offline channels, encompassing specialty appliance retailers, electrical wholesale distributors, home improvement stores, and direct B2B sales, continue to lead because chest freezers are large, high-consideration purchases that buyers typically evaluate physically before committing. Commercial buyers such as supermarket chains, food processing companies, and healthcare institutions overwhelmingly procure through direct manufacturer sales representatives and authorized distributors due to the need for product customization, after-sales service agreements, and volume pricing negotiations. The Online channel is the fastest growing sales channel, expanding rapidly as e-commerce platforms, including Amazon and Flipkart improve logistics capabilities for large appliance delivery, and residential buyers increasingly conduct research and purchases digitally.

End-user Insights

The Supermarkets & Hypermarkets end-use segment is the leading category in the global chest freezer market, commanding approximately 28% of total revenue share in 2025. Large-format food retail stores are among the most intensive purchasers of commercial chest freezers globally, deploying glass-lid display units for frozen food merchandising and solid-lid back-room units for bulk inventory storage. The Food Marketing Institute (FMI) reports that frozen food category sales in U.S. supermarkets exceeded US$ 72 billion in 2023, underscoring the indispensability of chest freezer infrastructure in food retail operations. Globally, supermarket and hypermarket outlet counts continue to grow, particularly across Asia Pacific and Latin America, creating sustained replacement and new installation demand. The Pharmaceutical & Healthcare end-use segment is the fastest growing, driven by vaccine distribution mandates and growing biologic drug storage requirements across global healthcare systems.

Regional Insights

North America Chest Freezer Market Trends and Insights

North America is the second-largest regional market for chest freezers, characterized by high appliance ownership rates, robust food retail infrastructure, and progressive energy efficiency standards. The U.S. Department of Energy (DOE) enforces strict minimum efficiency standards for residential and commercial freezers under 10 CFR Parts 430 and 431, compelling continuous product improvement cycles. U.S. frozen food retail sales have demonstrated sustained resilience, with the American Frozen Food Institute (AFFI) reporting that 9 in 10 U.S. households regularly purchase frozen foods, sustaining residential chest freezer demand across all income segments.

The rapid expansion of dark stores operated by companies such as DoorDash and Gopuff across major U.S. metropolitan areas is generating new commercial chest freezer procurement demand. Canada's grocery retail expansion, particularly Loblaw Companies' and Empire Company's capital expenditure programs targeting store modernization, is driving commercial freezer replacement upgrades. The U.S. EPA's AIM Act transition timeline is actively reshaping refrigerant selection, incentivizing R-290 and CO2 product development among regional OEMs.

Europe Chest Freezer Market Trends and Insights

Europe represents a mature yet innovation-driven chest freezer market, shaped by the world's most stringent appliance energy efficiency regulations and accelerating adoption of natural refrigerant technologies. The EU Ecodesign Regulation (EU) 2019/2016 and revised Energy Labelling Regulation (EU) 2021/341 have systematically raised minimum performance thresholds, compelling manufacturers in Germany, France, and the United Kingdom to invest in inverter compressor and natural refrigerant platforms. Liebherr Group and Electrolux AB have both launched R-290-based commercial chest freezer ranges targeting the EU institutional food service market.

Germany's organized food retail sector, dominated by chains such as ALDI, LIDL, and REWE, drives consistent commercial chest freezer replacement cycles. Spain's expanding food processing export industry, as the EU's largest fresh food exporter by value, is generating parallel cold storage infrastructure demand. The UK's National Health Service (NHS) pharmaceutical cold storage expansion programs are supporting demand for WHO-compliant medical-grade chest freezers across hospital and community pharmacy networks.

Asia Pacific Chest Freezer Market Trends and Insights

Asia Pacific is the leading regional market for chest freezers, commanding approximately 40% of global revenue share in 2025, anchored by China's dominance as both the world's largest manufacturer and consumer of chest freezer units. China produced over 35 million refrigeration appliance units in 2023, according to the China Household Electrical Appliances Association (CHEAA), with chest freezers representing a significant share of output. Companies including Haier, Midea, Hisense, and Aucma operate large-scale domestic manufacturing facilities, enabling competitive global exports.

India is the fastest growing sub-market within the region, projected to expand at a CAGR exceeding 9% during 2026-2033, driven by rapid organized food retail growth under government schemes such as PM Kisan Sampada Yojana targeting food processing infrastructure. The Reserve Bank of India reports rising rural household income levels that are enabling first-time chest freezer purchases, particularly for domestic milk and meat storage. Japan's market, led by Panasonic Corporation and Hoshizaki Corporation, remains a premium technology leader in energy-efficient and IoT-connected commercial chest freezer solutions serving the country's highly sophisticated food service sector.

Competitive Landscape

The global chest freezer market demonstrates a moderately consolidated structure, with a group of large multinational appliance manufacturers accounting for a significant share of global sales. These companies leverage large-scale manufacturing, extensive supply chains, and established distribution networks to maintain competitive positions across residential and commercial refrigeration segments. At the same time, several regional appliance brands and specialized refrigeration manufacturers contribute to market competition by focusing on price-sensitive markets and localized product offerings.

Competition is increasingly shaped by technology innovation, energy efficiency improvements, and expansion into emerging markets. Manufacturers are investing in environmentally friendly refrigerants, inverter compressor technologies, and smart monitoring systems to enhance product performance and meet evolving energy regulations. Strategic priorities also include strengthening distribution channels, expanding manufacturing capacity in high-growth regions, and diversifying product portfolios to serve sectors such as food retail, hospitality, pharmaceuticals, and cold chain logistics. Additionally, companies are exploring service-based models, including equipment rental and leasing programs, to broaden customer access and generate recurring revenue streams.

Key Developments:

- June 2025: Elanpro introduced an innovative chest freezer with dual-condenser technology, designed to deliver faster freezing, improved cooling efficiency, and stable temperature control, helping preserve food quality and nutrition for commercial storage applications.

- April 2023: Elista entered the chest freezer segment with a new range of commercial freezers offering 100-500 litre capacities, including convertible, combi, and visible cooler variants designed for households, retail stores, and food service storage applications.

Companies Covered in Chest Freezer Market

- Haier Group Corporation

- Toshiba Corporation

- Whirlpool Corporation

- GE Appliances (Haier Group)

- Electrolux AB

- Danby Products

- Hisense Group

- AHT Cooling Systems GmbH

- Midea Group

- Hoshizaki Corporation

- Panasonic Corporation

- Aucma Co., Ltd.

- Liebherr Group

- Vestfrost Solutions A/S

- Godrej Appliances

- Haier Biomedical

- Carrier Global Corporation

- Metalfrio Solutions

Frequently Asked Questions

The global Chest Freezer market is estimated to reach US$ 18.8 Billion in 2026 and is projected to grow to US$ 30.2 Billion by 2033 at a CAGR of 7.0%.

Expansion of cold chain infrastructure, growth of organized food retail, increasing pharmaceutical cold storage demand, and the rise of e-commerce dark stores are the primary demand drivers.

Asia Pacific leads the global Chest Freezer market with around 40% revenue share, supported by strong manufacturing capacity and rising demand in emerging economies.

The key opportunity lies in the development of energy-efficient R-290 natural refrigerant inverter chest freezers with IoT-enabled temperature monitoring.

Key players include Haier Group Corporation, Midea Group, Hisense Group, Electrolux AB, Liebherr Group, Hoshizaki Corporation, Panasonic Corporation, Whirlpool Corporation, AHT Cooling Systems, and Godrej Appliances.