- Executive Summary

- Global Biodegradable Polymer Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Food & Beverage Industry Overview

- Global Agriculture Industry Overview

- Global Healthcare Industry Overview

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 - 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Biodegradable Polymer Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Global Biodegradable Polymer Market Outlook: Product Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Product Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Starch-based Polymers

- Polylactic Acid (PLA)

- Polyhydroxy Alkanoates (PHA)

- Polyesters

- Others

- Market Attractiveness Analysis: Product Type

- Global Biodegradable Polymer Market Outlook: Application

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Application, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Packaging

- Agriculture

- Medical & Healthcare

- Textile & Fiber

- Consumer Goods

- Other

- Market Attractiveness Analysis: Application

- Global Biodegradable Polymer Market Outlook: End-use Industry

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by End-use Industry, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Food & Beverage

- Agriculture & Horticulture

- Healthcare & Medical

- Automotive

- Electronics & Consumer

- Textile & Apparel

- Market Attractiveness Analysis: End-use Industry

- Global Biodegradable Polymer Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Biodegradable Polymer Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Starch-based Polymers

- Polylactic Acid (PLA)

- Polyhydroxy Alkanoates (PHA)

- Polyesters

- Others

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Packaging

- Agriculture

- Medical & Healthcare

- Textile & Fiber

- Consumer Goods

- Other

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Food & Beverage

- Agriculture & Horticulture

- Healthcare & Medical

- Automotive

- Electronics & Consumer

- Textile & Apparel

- Europe Biodegradable Polymer Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Starch-based Polymers

- Polylactic Acid (PLA)

- Polyhydroxy Alkanoates (PHA)

- Polyesters

- Others

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Packaging

- Agriculture

- Medical & Healthcare

- Textile & Fiber

- Consumer Goods

- Other

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Food & Beverage

- Agriculture & Horticulture

- Healthcare & Medical

- Automotive

- Electronics & Consumer

- Textile & Apparel

- East Asia Biodegradable Polymer Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Starch-based Polymers

- Polylactic Acid (PLA)

- Polyhydroxy Alkanoates (PHA)

- Polyesters

- Others

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Packaging

- Agriculture

- Medical & Healthcare

- Textile & Fiber

- Consumer Goods

- Other

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Food & Beverage

- Agriculture & Horticulture

- Healthcare & Medical

- Automotive

- Electronics & Consumer

- Textile & Apparel

- South Asia & Oceania Biodegradable Polymer Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Starch-based Polymers

- Polylactic Acid (PLA)

- Polyhydroxy Alkanoates (PHA)

- Polyesters

- Others

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Packaging

- Agriculture

- Medical & Healthcare

- Textile & Fiber

- Consumer Goods

- Other

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Food & Beverage

- Agriculture & Horticulture

- Healthcare & Medical

- Automotive

- Electronics & Consumer

- Textile & Apparel

- Latin America Biodegradable Polymer Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Starch-based Polymers

- Polylactic Acid (PLA)

- Polyhydroxy Alkanoates (PHA)

- Polyesters

- Others

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Packaging

- Agriculture

- Medical & Healthcare

- Textile & Fiber

- Consumer Goods

- Other

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Food & Beverage

- Agriculture & Horticulture

- Healthcare & Medical

- Automotive

- Electronics & Consumer

- Textile & Apparel

- Middle East & Africa Biodegradable Polymer Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Starch-based Polymers

- Polylactic Acid (PLA)

- Polyhydroxy Alkanoates (PHA)

- Polyesters

- Others

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Packaging

- Agriculture

- Medical & Healthcare

- Textile & Fiber

- Consumer Goods

- Other

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Food & Beverage

- Agriculture & Horticulture

- Healthcare & Medical

- Automotive

- Electronics & Consumer

- Textile & Apparel

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- BASF SE

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- NatureWorks LLC

- Novamont S.p.A

- Corbion N.V.

- Mitsubishi Chemical Group

- Kaneka Corporation

- Biome Bioplastics Limited

- FKuR Kunststoff GmbH

- Braskem S.A.

- Kingfa Sci. & Tech. Co., Ltd.

- Bio On S.p.A.

- Toray Industries

- BASF SE

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Plastics, Polymers & Resins

- Biodegradable Polymer Market

Biodegradable Polymer Market Size, Share, and Growth Forecast 2026 - 2033

Biodegradable Polymer Market by Product Type (Starch-based Polymers, Polylactic Acid, Polyhydroxy Alkanoates, Polyesters, Others), Application (Packaging, Agriculture, Medical & Healthcare, Textile & Fiber, Consumer Goods, Other), End-use Industry (Food & Beverage, Agriculture & Horticulture, Healthcare & Medical, Automotive, Electronics & Consumer, Textile & Apparel), and Regional Analysis for 2026 - 2033

Biodegradable Polymer Market Size and Trend Analysis

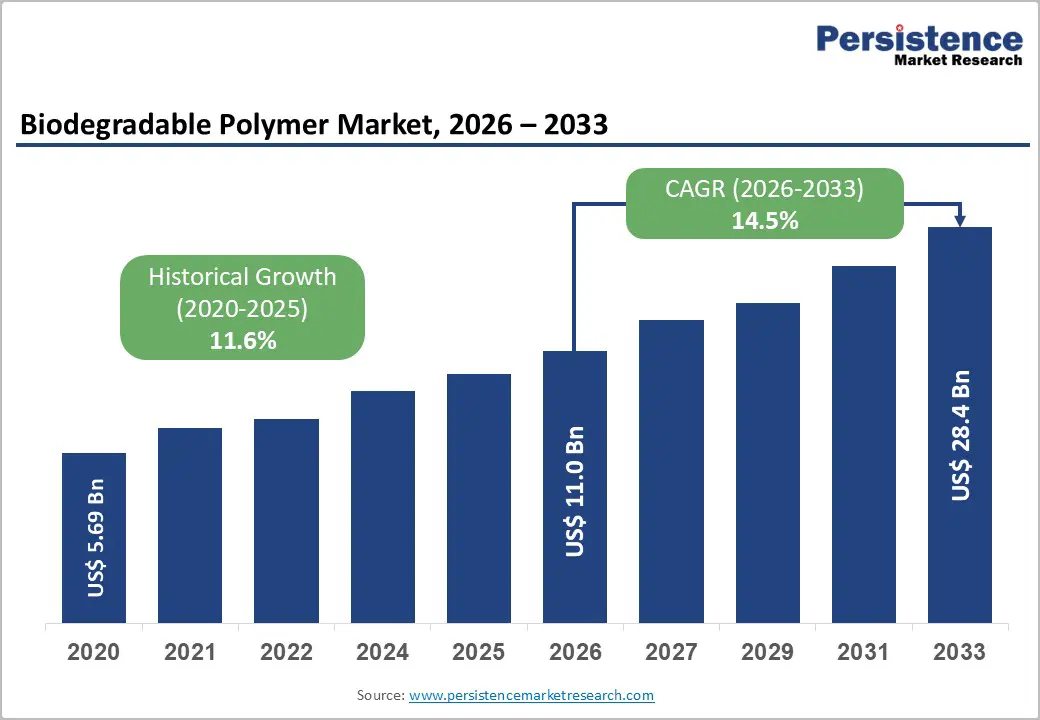

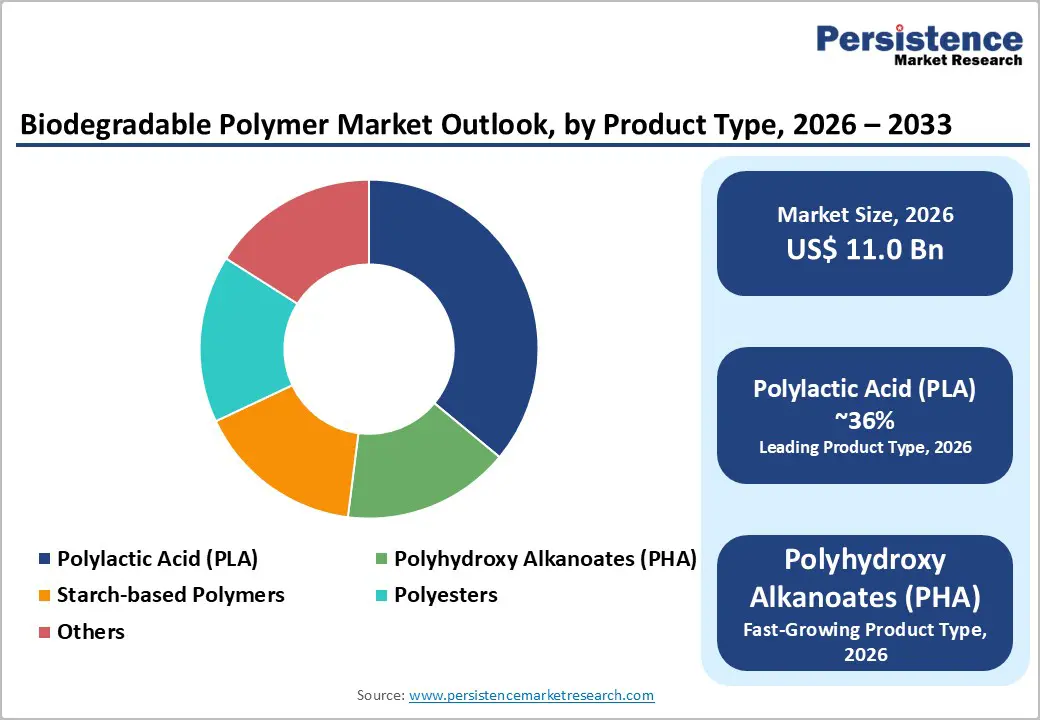

The global biodegradable polymer market is likely to be valued at US$ 11.0 billion in 2026 and is projected to reach US$ 28.4 billion by 2033, growing at a CAGR of 14.5% between 2026 and 2033.

Surging legislative mandates banning single-use plastics, combined with heightened corporate sustainability commitments and rapid advances in biopolymer processing technology, are collectively propelling market expansion. The European Union Single-Use Plastics Directive and analogous regulations across Asia-Pacific and North America have accelerated the substitution of conventional petroleum-based plastics with certified compostable alternatives. Growing consumer awareness of the environmental consequences of plastic pollution, alongside continuous cost reductions through scaled manufacturing of Polylactic Acid (PLA) and Polyhydroxy Alkanoates (PHA), further underpins demand.

Key Industry Highlights:

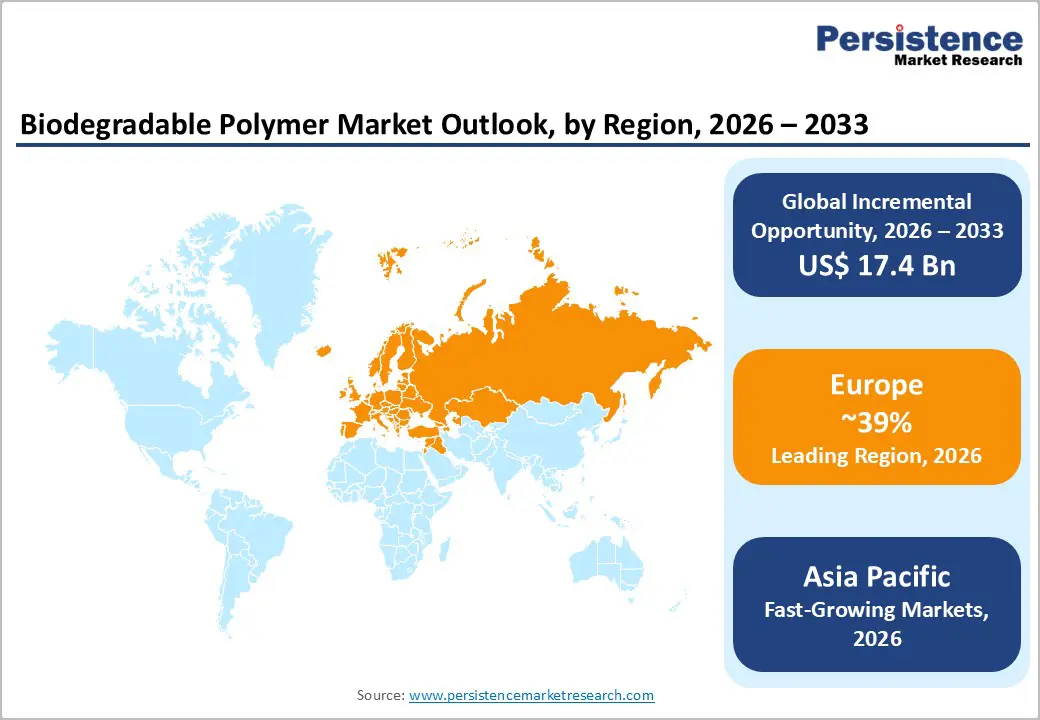

- Leading Region: Europe leads the global biodegradable polymer market, with 39% market share, driven by the EU Single-Use Plastics Directive, EN 13432 composting standards, and established industrial composting infrastructure, making it the highest-revenue regional market globally.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, propelled by China's national plastic ban, India's single-use plastic prohibition, expanding domestic PLA production, and abundant low-cost agricultural feedstocks in Thailand and Vietnam.

- Dominant Segment: Packaging is the dominant application segment, accounting for approximately 41% of market revenue, fueled by global single-use plastic bans, FMCG brand commitments, and rising demand for certified compostable food packaging solutions.

- Fastest Growing Segment: Polyhydroxy Alkanoates (PHA) is the fastest-growing product type segment, benefiting from second-generation feedstock innovations, improved fermentation efficiency, and expanding adoption in premium medical, food contact, and marine-degradable applications.

- Key Market Opportunity: Agricultural biodegradable mulch films represent a high-growth opportunity, with FAO estimating 2.5 million tons of annual plastic waste from conventional films, and China and EU actively mandating compostable alternatives across millions of cultivated hectares.

| Key Insights | Details |

|---|---|

| Biodegradable Polymer Market Size (2026E) | US$ 11.0 Bn |

| Market Value Forecast (2033F) | US$ 28.4 Bn |

| Projected Growth CAGR (2026 - 2033) | 14.5% |

| Historical Market Growth (2020 - 2025) | 11.6% |

Market Dynamics

Drivers - Rising Regulatory Pressure Against Single-Use Plastics Driving Rapid Adoption

Stringent global regulatory frameworks have become the most significant catalyst for expanding biodegradable polymer adoption. The European Union’s Single-Use Plastics Directive (SUPD), effective since July 2021, prohibits ten categories of single-use plastic products, prompting an immediate shift toward certified compostable and biodegradable alternatives. By 2023, more than 60 countries had implemented plastic bag levies, restrictions, or bans under various national policies. In the United States, states such as California, New York, and Colorado mandate compostable packaging for designated food service applications.

Similarly, India’s Plastic Waste Management Amendment Rules (2021) banned single-use plastic items below 75 microns, accelerating domestic production of starch-based and PLA materials. Collectively, these policies, supported by corporate EPR commitments, are reshaping procurement practices across packaging, retail, and food service sectors worldwide.

Expanding Application in the Medical and Healthcare Sector Fueling Technology Investment

The healthcare sector constitutes one of the most advanced and high-value application domains for biodegradable polymers. Critical medical products, including resorbable surgical sutures, drug-delivery matrices, bone-fixation implants, and tissue-engineering scaffolds, depend on biocompatible materials such as PLGA, PCL, and PHA derivatives. According to the FDA, bioabsorbable implants represent one of the fastest-growing categories within Class II medical devices.

The WHO has emphasized the increasing need for infection-resistant, single-use medical consumables in developing markets, a requirement well aligned with biodegradable solutions. The global rise in surgical procedures, estimated at approximately 313 million annually, continues to drive demand for absorbable biomaterials. Sustained R&D investment by companies such as Corbion N.V. and NatureWorks LLC further reinforces this strong growth trajectory.

Restraints - High Production Costs and Price Disparity Relative to Conventional Plastics

A major constraint on the widespread adoption of biodegradable polymers is the substantial cost premium relative to conventional petroleum-based plastics. As of 2024, commercial-grade PLA is priced at approximately USD 2,200-2,800 per metric ton, compared with USD 900-1,200 per metric ton for polyethylene.

The disparity is even more pronounced for PHA, which ranges from USD 4,000 to 6,000 per metric ton due to complex microbial fermentation requirements. These elevated production costs hinder large-scale substitution, particularly in price-sensitive segments such as agricultural mulch films and fast-moving consumer goods packaging, thereby limiting broader market penetration.

Inadequate Industrial Composting Infrastructure Limiting End-of-Life Value Proposition

The environmental benefits of biodegradable polymers are significantly constrained by the widespread lack of industrial composting infrastructure across most regions. According to the Ellen MacArthur Foundation, fewer than 10% of plastic packaging worldwide is successfully recycled or composted.

In the United States, the Biodegradable Products Institute reports that fewer than 200 industrial composting facilities accept certified compostable packaging. In the absence of proper composting conditions, these materials may persist in landfills for extended periods, diminishing their environmental credibility and discouraging adoption by brands concerned about greenwashing risks and growing consumer scrutiny.

Market Opportunities

Agricultural Sector as a High-Growth Frontier

The agricultural segment presents a compelling opportunity, particularly for biodegradable mulch films that eliminate costly plastic film retrieval and disposal at the end of growing seasons. Conventional low-density polyethylene (LDPE) mulch films generate approximately 2.5 million tons of plastic waste annually in global agriculture, per the Food and Agriculture Organization (FAO) of the United Nations.

The European Commission's revised Fertilizing Products Regulation (EU) 2019/1009 explicitly permits and promotes polymer-coated controlled-release fertilizers using biodegradable coatings, opening a new revenue stream for PHA and starch-blend manufacturers. In China, the Ministry of Agriculture and Rural Affairs launched a nationwide program to phase out residual agricultural plastic films by 2025, mandating the transition to certified biodegradable alternatives across 50 million hectares of cultivated land. These policy-driven demand pools offer biodegradable polymer producers a stable, long-term volume market with favorable governmental support.

Second-Generation Feedstock Innovation and PHA Fermentation Scale-Up

The advancement of second-generation and waste-based feedstocks for biopolymer production represents a transformative opportunity to overcome the cost-competitiveness barrier. Companies are increasingly leveraging industrial waste streams, methane, carbon dioxide, lignocellulosic biomass, and food-processing byproducts as low-cost carbon sources for PHA fermentation. Newlight Technologies in the U.S. has demonstrated commercial-scale production of PHA from greenhouse gas feedstocks.

The U.S. Department of Energy (DOE)'s Bioenergy Technologies Office (BETO) has allocated over USD 60 million in recent funding cycles toward advancing biopolymer manufacturing from non-food biomass. Concurrently, Kaneka Corporation has commercialized its PHBH polymer derived from plant oils, achieving lifecycle greenhouse gas reductions of over 50% versus conventional plastics. As fermentation yields improve and downstream purification costs decline, market participants positioned early in second-generation PHA and bio-PLA production stand to capture substantial margin advantages and expand into currently cost-restricted application segments.

Category-wise Analysis

Product Type Insights

Polylactic Acid (PLA) holds a leading position in the biodegradable polymer market, accounting for roughly 36% of global revenue. This prominence is attributed to its advanced industrial production capacity, broad regulatory acceptance for food-contact applications by both the FDA and the European Food Safety Authority, and its efficient compatibility with standard thermoplastic processing systems.

NatureWorks LLC, operating the world’s largest PLA manufacturing facility in Blair, Nebraska, with an annual capacity of 150,000 metric tons, has been instrumental in establishing PLA as the principal commercial biopolymer. PLA’s adaptability across rigid packaging, films, fibers, and foams, along with its significantly lower carbon footprint compared to petroleum-based plastics, reinforces its dominant market position, while advancements in stereocomplex PLA continue expanding its applicability in the automotive and electronics industries.

Application Insights

The Packaging segment maintains the leading position within the biodegradable polymer market, contributing approximately 41% of total global revenue. Is its dominance driven by the substantial worldwide consumption of single-use plastic packaging, amounting to more than 141 million metric tons annually, according to the OECD, along with increasingly stringent regulations aimed at reducing packaging waste.

Key sub-applications include flexible food packaging, compostable carry bags, rigid food-service containers, and multilayer barrier films. Major fast-moving consumer goods companies such as Nestlé, Unilever, and Danone have significantly expanded their use of certified compostable packaging, strengthening demand for PLA and starch-blend materials. As production volumes scale, the segment also benefits from notable cost-efficiency gains, reinforcing its sustained market leadership.

End-use Industry Insights

The Food & Beverage sector constitutes the leading end-use segment in the biodegradable polymer market, accounting for approximately 38% of overall demand. Is its dominance driven by the extensive use of single-use packaging across food retail, food service, and grocery applications, where biodegradable materials increasingly replace traditional plastic trays, cups, lids, cutlery, and flexible pouches. The European Commission’s Farm to Fork Strategy targets a 20% reduction in packaging use by 2030 and encourages the adoption of reusable and compostable solutions, thereby strengthening demand for biodegradable polymers within the industry.

In the United States, food service operators serving more than 1 million establishments are transitioning to BPI-certified compostable service ware to align with municipal composting regulations. Collectively, regulatory pressures, sustainability commitments, and consumer expectations reinforce the sector’s position as the primary volume driver through the forecast period.

Regional Insights

North America Biodegradable Polymer Trends

North America represents a mature yet rapidly evolving market for biodegradable polymers, supported by progressive state-level legislation and a strong innovation ecosystem. California’s Senate Bill 54, enacted in 2022, mandates that all single-use plastic packaging sold in the state be recyclable or compostable by 2032, establishing the most ambitious packaging regulation in the United States. CalRecycle administers the associated certification framework, directly stimulating demand for certified biodegradable materials.

Canada’s federal Single-Use Plastics Prohibition Regulations, effective since December 2022, further expand regional consumption. The presence of leading producers such as NatureWorks LLC, Braskem, and Novamont, combined with significant corporate and venture-backed R&D investment through the U.S. DOE Bioenergy Technologies Office, ensures that North America maintains its innovation leadership despite increasing production scale in the Asia Pacific.

Europe Biodegradable Polymer Trends

Europe holds the largest share of the global biodegradable polymer market, supported by the region’s comprehensive regulatory framework governing sustainable packaging and biobased materials. The EU Single-Use Plastics Directive and the proposed Packaging and Packaging Waste Regulation establish mandatory compostability and recycled-content standards that reinforce market expansion. Germany benefits from an extensive industrial composting network of more than 1,000 certified facilities, while France’s AGEC Law mandates compostable formats for several consumer applications, creating direct demand.

Europe also hosts prominent domestic biopolymer producers such as Novamont S.p.A. and Bio On S.p.A., with Spain expanding composting capacity and the UK incentivizing bio-alternatives through its Plastic Packaging Tax levied on packaging with insufficient recycled content. Harmonized standards under EN 13432 further reduce fragmentation and facilitate cross-border trade.

Asia Pacific Biodegradable Polymer Trends

Asia Pacific is the fastest-growing regional market for biodegradable polymers, driven by large-scale regulatory measures, expanding manufacturing capacity, and increasing sustainability awareness among middle-income consumers. China’s 2020 policy on controlling plastic pollution established a phased national ban on non-degradable single-use plastics, with full implementation targeted for 2026, while the region continues to strengthen its PLA production base through facilities such as Total Corbion PLA’s 75,000 MT/year plant in Thailand, reinforcing Asia’s dual role as both a production and consumption hub.

Japan is advancing high-performance PHA and PBS-based biopolymers for automotive and electronics applications. At the same time, India’s prohibition on single-use plastics has accelerated domestic investment in PLA and starch-blend manufacturing. Additionally, ASEAN economies benefit from abundant agricultural feedstocks, enhancing long-term regional competitiveness in bio-based monomer production.

Competitive Landscape

The global biodegradable polymer market demonstrates a moderately consolidated structure, dominated by a limited group of technology-intensive producers such as NatureWorks LLC, BASF SE, Novamont S.p.A., and Corbion N.V., each holding notable intellectual property and production advantages. Market leaders differentiate themselves through proprietary fermentation technologies, adherence to certified compostability standards, and integrated feedstock-to-polymer value chains. Strategic priorities include expanding capacity through greenfield developments and joint ventures, diversifying geographically across the Asia Pacific region, and strengthening portfolios in high-margin medical and agricultural applications. Emerging models, including polymer-as-a-service and municipal closed-loop composting partnerships, are gaining momentum, while mid-tier firms are increasingly specializing in PHA- or starch-based segments to avoid direct competition.

Key Developments:

- November 2025: BASF expanded global biodegradable polymer-related supply by inaugurating increased Alkyl Polyglucosides (APG) production capacity at its Bangpakong, Thailand site to strengthen regional sustainable surfactant supply.

- March 2025: NatureWorks enhanced its Ingeo™ biopolymer portfolio by launching the Ingeo Extend platform and the new Ingeo Extend 4950D grade, enabling faster biodegradability and improved manufacturing efficiency for BOPLA films at lower production costs.

- November 2023: BASF expanded its biodegradable polymers portfolio by launching BVERDE GP 790 L, a readily biodegradable, 79 % biobased anti-redeposition polymer that enhances sustainability without compromising performance in detergent formulations.

Top Companies in the Biodegradable Polymer Market

- NatureWorks LLC (Minnetonka, U.S.) is the world's largest dedicated PLA producer and a pioneering force in the commercial bioplastics industry. Its Ingeo™ PLA brand is the benchmark material for compostable packaging globally. With the Thailand facility now operational, NatureWorks commands over 225,000 MT/year of combined PLA capacity. The company's strong feedstock partnerships, extensive application-development support, and first-mover brand recognition in PLA make it the de facto market leader in revenue, portfolio breadth, and customer base.

- BASF SE (Ludwigshafen, Germany) operates one of the broadest biodegradable polymer portfolios globally, encompassing its certified compostable ecoflex® (PBAT) and ecovio® (PLA/PBAT blend) product lines, widely used in agricultural films, shopping bags, and food service packaging. The company's global chemical distribution infrastructure, regulatory expertise across key markets, and sustained R&D investment across biopolymers and chemical recycling position it as a multi-segment leader with unparalleled geographic reach.

- Novamont S.p.A. (Novara, Italy), a developer of the proprietary Mater-Bi® starch-biopolymer technology platform, is a pioneer in commercial-scale starch-based biodegradable plastics. The company holds over 100 patents globally and has established the Matrìca joint venture bio-refinery with Versalis (Eni) in Porto Torres, Sardinia, for integrated bio-based chemical and polymer production. Novamont's leadership in certified compostable shopping bags and food caddy liners, particularly in Italy and across the EU, reflects its unmatched influence in the European regulatory and commercial ecosystem.

Companies Covered in Biodegradable Polymer Market

- BASF SE

- NatureWorks LLC

- Novamont S.p.A.

- Corbion N.V.

- Mitsubishi Chemical Group

- Kaneka Corporation

- Biome Bioplastics Limited

- FKuR Kunststoff GmbH

- Braskem S.A.

- Kingfa Sci. & Tech. Co., Ltd.

- Bio On S.p.A.

- Toray Industries

- Total Corbion PLA

- Newlight Technologies

- Danimer Scientific

Frequently Asked Questions

The global Biodegradable Polymer market is valued at US$ 11.0 Bn in 2026 and is projected to reach US$ 28.4 Bn by 2033, expanding at a compound annual growth rate (CAGR) of 14.5% during the forecast period of 2026-2033. The market was valued at US$ 5.7 Bn in 2020, reflecting a historical CAGR of 11.6% between 2020 and 2025.

The primary demand drivers include increasingly stringent global regulatory mandates against single-use plastics, such as the EU Single-Use Plastics Directive, India's Plastic Waste Management Amendment Rules, and U.S. state-level packaging legislation, alongside growing corporate sustainability commitments under extended producer responsibility frameworks.

Polylactic Acid (PLA) is the leading product type segment, accounting for approximately 36% of total market revenue. Its dominance is attributable to mature commercial production infrastructure led by NatureWorks LLC, broad regulatory approval for food-contact applications by the FDA and EFSA, and demonstrated lifecycle sustainability advantages.

Europe is the leading regional market for biodegradable polymers, with 39% market share, supported by the world's most comprehensive regulatory ecosystem, including the EU Single-Use Plastics Directive, the proposed Packaging and Packaging Waste Regulation (PPWR), and national laws such as France's AGEC Law and the UK's Plastic Packaging Tax.

The most significant near- to medium-term growth opportunity lies in the agricultural sector, particularly for certified biodegradable mulch films and controlled-release fertilizer coatings. Conventional agricultural plastic films generate approximately 2.5 million tons of plastic waste annually (FAO), and both China and the EU have implemented targeted policy mandates for compostable alternatives.

The key companies operating in the global Biodegradable Polymer market include BASF SE, NatureWorks LLC, Novamont S.p.A., Corbion N.V., Mitsubishi Chemical Group, Kaneka Corporation, Biome Bioplastics Limited, FKuR Kunststoff GmbH, Braskem S.A., Kingfa Sci. & Tech. Co., Ltd., Bio On S.p.A., Toray Industries, Total Corbion PLA, Newlight Technologies, and Danimer Scientific, among others.