- Processed Food

- Beef Market

Beef Market Size, Share, and Growth Forecast, 2026 – 2033

Beef Market by Slaughter Method (Kosher, Halal, Standard), Cut Type (Ground Beef, Roasts, Steaks, Brisket), Distribution Channel (Retail Sales, HoReCa, Butcher Shops, E-Commerce), and Regional Analysis 2026 – 2033

Beef Market Size and Trends Analysis

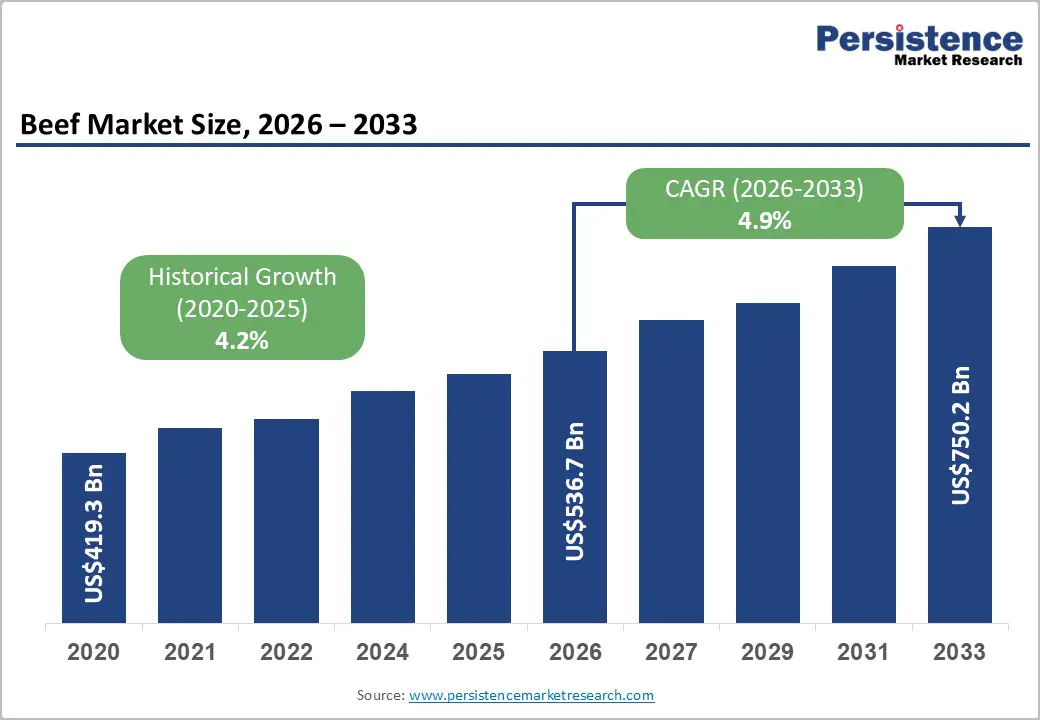

The global beef market size is likely to be valued at US$536.7 billion in 2026 and is expected to reach US$750.2 billion by 2033, growing at a CAGR of 4.9% during the forecast period from 2026 to 2033, driven by rising protein demand owing to urbanization that has accelerated convenience food adoption across emerging economies. Halal certification standards strengthen global supply chains while e-commerce platforms boost direct-to-consumer access. Advances in processing technology enhance product shelf life and traceability, positioning the market for sustained momentum. Advancements in precision livestock farming are expected to optimize supply chain efficiency and yield. Strategic integration of digital traceability platforms is expected to enhance trust in premium consumer brands globally. Shifting dietary preferences toward high-quality cuts is likely to accelerate specialized regional production investments steadily.

Key Industry Highlights:

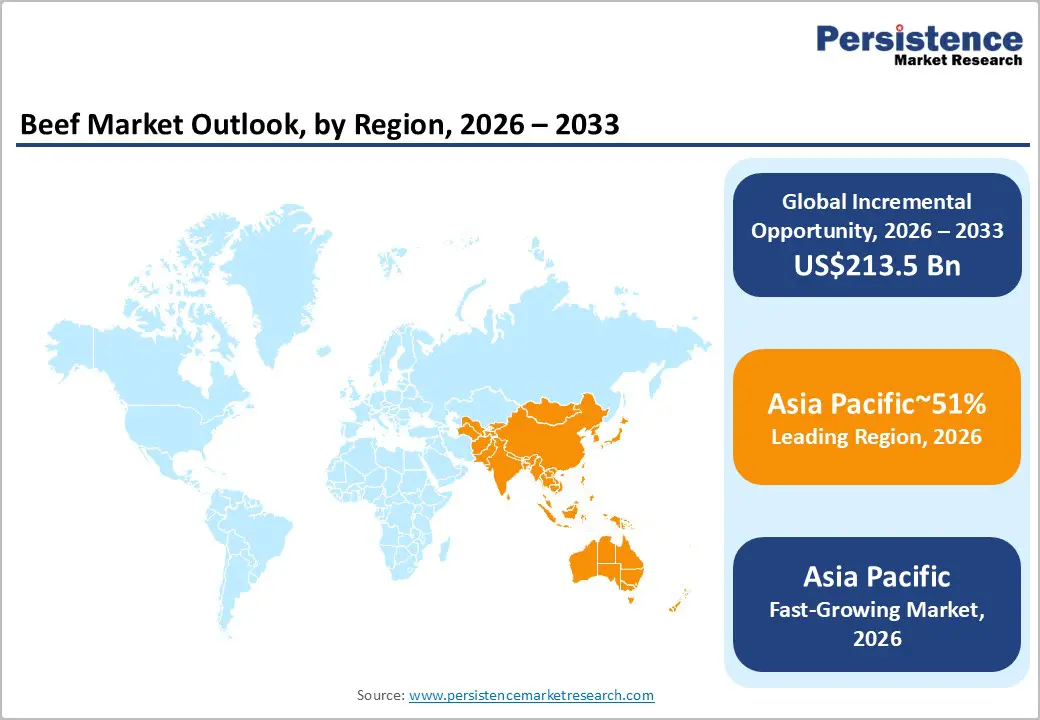

- Leading Region: Asia Pacific is projected to lead, accounting for approximately 51% share in 2026, supported by rapid urbanization, expanding disposable incomes, and modernized cold chain logistics.

- Fastest-growing Region: Asia Pacific is anticipated to grow fastest, driven by accelerating digital retail penetration, dietary transitions, and enhanced regional processing infrastructure.

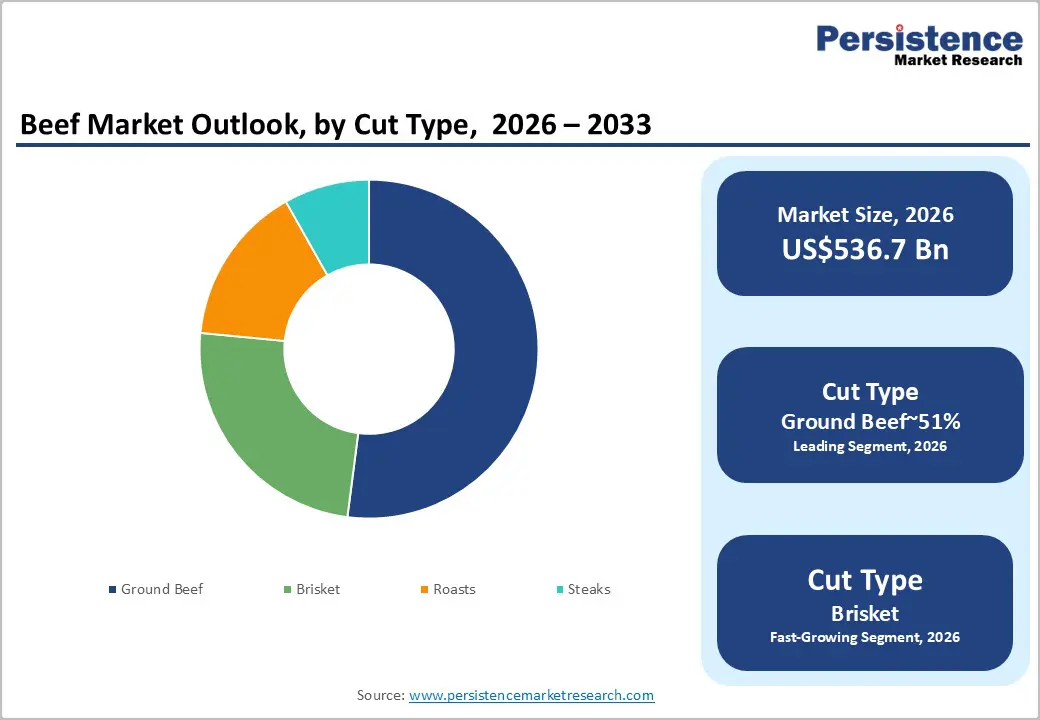

- Leading Cut Type: Ground beef is expected to lead, accounting for approximately 51% share in 2026, anchored by widespread culinary versatility, inherent affordability, and robust fast-food network integration.

- Leading Distribution Channel: Retail sales is anticipated to lead, holding approximately 52% share in 2026, driven by the proliferation of organized hypermarkets and improved shelf-life packaging technologies.

| Key Insights | Details |

|---|---|

| Beef Market Size (2026E) | US$536.7 Bn |

| Market Value Forecast (2033F) | US$750.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Escalating Demand for Halal-Certified Premium Protein

Rising global awareness regarding food safety and ethical slaughtering practices is driving the Halal segment expansion. Consumers are increasingly associating Halal certification with superior animal welfare and more stringent hygiene protocols. This perception shift is expected to bolster demand across both Islamic and non-Islamic demographic segments. Manufacturers are likely to prioritize Halal-compliant processing facilities to capture this rapidly widening consumer base. International trade protocols are also aligning to facilitate smoother cross-border movement of certified beef products.

Strategic focus from JBS S.A. with Friboi illustrates how major players are targeting specialized certifications. This brand is expected to expand its Halal-compliant production lines to serve growing Middle Eastern demand. Investment in traceable certification technology is likely to enhance consumer trust in Halal-labeled beef products. Market participants are anticipated to leverage these certifications to differentiate their portfolios in competitive retail environments. The integration of high-standard slaughter methods is set to define future quality benchmarks for the industry.

Advancements in Case-Ready Packaging for Retail Longevity

Innovative packaging technologies such as Modified Atmosphere Packaging (MAP) are revolutionizing the retail distribution of fresh beef. These advancements are expected to significantly extend the shelf life of premium cuts in supermarkets. Reduced spoilage rates are likely to improve profit margins for retailers and decrease consumer food waste. Vacuum-sealed skin packs are anticipated to gain popularity due to their superior visual appeal. Enhanced packaging is set to facilitate longer transport distances from processing hubs to urban centers.

Implementation of advanced preservation by Cargill with Sterling Silver Premium Meats demonstrates the shift toward high-end retail. This product line is expected to leverage specialized packaging to maintain color and moisture retention. Retailers are likely to favor such branded programs to reduce in-store butchery labor costs. Automation in the packaging process is anticipated to lower the risk of microbial contamination. These technological refinements are positioned to strengthen the dominance of the organized retail sales segment.

Barrier Analysis – Increasing Stringency of Environmental and Carbon Regulations

New governmental mandates targeting methane emissions from livestock are expected to increase operational costs for producers. Sustainability compliance is likely to require significant capital investment in waste management and carbon-neutral farming. These regulatory pressures are anticipated to constrain the profit margins of small to mid-sized ranches. Higher production costs are likely to be passed down the value chain to final consumers. Some regions are expected to implement carbon taxes on high-emission agricultural sectors by 2030.

Compliance initiatives from Marfrig with Viva reflect the industry's response to mounting environmental pressures and standards. This product line is expected to face higher certification costs to verify its carbon-neutral status. Increased scrutiny on land use for grazing is likely to limit horizontal production expansion. Producers are anticipated to struggle with the dual burden of high feed costs and regulation. These environmental factors are set to create a challenging pricing environment for entry-level beef.

Strengthening Competition from Alternative Protein Sources

The rapid development of plant-based and lab-grown meat substitutes is challenging traditional beef's market share. Younger demographics are increasingly likely to adopt "flexitarian" diets to reduce their environmental footprint. These alternative products are expected to achieve price parity with mid-tier beef cuts within several years. Improvements in the texture and flavor of meat substitutes are anticipated to enhance consumer acceptance. Traditional beef producers are likely to lose shelf space to high-tech protein innovators.

Strategic responses from Minerva Foods with Ana Paula Black Angus emphasize the need for distinct premium positioning. This product is expected to counter alternative proteins by highlighting natural origin and superior culinary attributes. However, the rise of meat analogs is likely to saturate the ground beef and patty segments. Retailers are anticipated to reallocate refrigerated space to accommodate the growing variety of vegan options. This competitive pressure is positioned to limit the growth potential of conventional beef commodities.

Opportunity Analysis – Growth of E-Commerce and D2C Subscription Models

The shift toward online grocery shopping is creating new avenues for specialized beef purveyors to reach consumers. Direct-to-consumer (D2C) platforms are expected to allow producers to capture higher margins by bypassing traditional wholesalers. Subscription-based models are likely to foster brand loyalty through curated selections of premium beef cuts. Improvements in last-mile cold chain logistics are anticipated to ensure the delivery of high-quality products. This digital transition is set to unlock significant value in the high-end artisanal beef segment.

Digital expansion by Omaha Steaks with Private Reserve illustrates the potential of high-touch online retail experiences. This brand is expected to utilize advanced logistics to maintain its lead in the premium home-delivery market. Personalized marketing algorithms are likely to increase the frequency of high-value beef purchases among tech-savvy users. Consumers are anticipated to value the convenience of scheduled deliveries for specialized cuts such as brisket. The e-commerce channel is positioned to be a primary growth engine for luxury beef.

Rising Demand for Value-Added and Pre-Seasoned Beef

Busy urban lifestyles are fueling the demand for convenient, ready-to-cook beef products in retail settings. Pre-marinated and pre-sliced offerings reduce preparation complexity, embedding convenience premiums into pricing structures and enhancing per-unit margins. Retailers are reallocating shelf space toward deli and heat-and-eat formats, reshaping in-store merchandising economics and cold-chain utilization. These value-added products are likely to command higher price points than raw, unprocessed meat cuts. Retailers are anticipated to expand their deli and heat-and-eat sections to capitalize on this trend. Innovation in marinade flavors is set to attract a more diverse consumer demographic.

Product diversification from Hormel Foods with Always Tender showcases the shift toward consumer-ready convenience solutions. This product line is expected to expand its variety of pre-seasoned beef tips and roasts. Manufacturers are likely to invest in steam-in-bag technologies to simplify the home cooking process. Enhanced convenience is anticipated to protect beef's share of the dinner plate against faster-cooking alternatives. These innovations reduce cooking variability while aligning with evolving food safety and labeling regulations governing processed meat categories. The value-added segment is set to offer the most significant margin expansion opportunities for processors.

Category–wise Analysis

Cut Type Insights

Ground beef is expected to lead, accounting for approximately 51% share in 2026, underpinned by its essential role in global food service and retail affordability. This segment is likely to maintain dominance as consumers prioritize versatile protein sources that fit diverse culinary traditions. High-volume demand from the burger industry is anticipated to sustain consistent production levels across major processing hubs. Strategic branding from Tyson Foods with Star Ranch Angus illustrates how manufacturers are elevating the quality perception of ground products. This product is expected to satisfy consumer requirements for both lean content and flavor consistency. Increased utilization of ground beef in prepared meal kits is likely to further solidify its market position.

Brisket is expected to be the fastest-growing segment, driven by the global expansion of artisanal barbecue culture and slow-cooking culinary trends. This cut is anticipated to witness surging demand as specialized smokehouses proliferate across non-traditional markets like Europe and Asia. The rise of home-smoking enthusiasts is likely to drive premium retail sales for high-marbling brisket varieties. Product offerings from Cargill with Rumba Meats are expected to capture this growth by targeting specific ethnic and specialty cooking segments. Enhanced vacuum packaging is likely to facilitate the global distribution of large brisket cuts to specialized retailers. This segment is positioned to benefit from a shift toward "nose-to-tail" consumption and premiumized comfort foods.

Distribution Channel Insights

Retail sales are anticipated to lead, holding approximately 52% share in 2026, driven by the consolidation of organized grocery chains and improvements in cold chain logistics. This channel is expected to dominate as modern hypermarkets offer consumers a wider variety of specialized cuts and branded beef programs. The proliferation of private-label beef brands is likely to increase price competition while maintaining high-quality standards for shoppers. Market engagement from Hormel Foods with Applegate Naturals illustrates the trend toward providing clean-label, retail-ready beef options. This product line is expected to attract health-conscious consumers through transparent sourcing information on physical retail shelves. Enhanced in-store experiences and butcher counters are anticipated to maintain high foot traffic.

E-commerce is expected to be the fastest-growing segment, driven by the acceleration of digital grocery adoption and the rise of premium meat subscription boxes. This channel is anticipated to thrive as consumers seek the convenience of home delivery for bulky or specialized beef orders. High-end producers are likely to utilize digital platforms to communicate their unique brand stories and farm-to-table origins directly to buyers. The digital strategy of Omaha Steaks with King Cut demonstrates how e-commerce can facilitate the sale of ultra-premium, oversized beef portions. This brand is expected to leverage sophisticated cold-shipping technology to ensure product integrity across long delivery distances. Online platforms are likely to become the primary discovery point for artisanal and grass-fed beef varieties.

Regional Insights

Asia Pacific Beef Market Trends

Asia Pacific is expected to remain the leading regional market, accounting for approximately 51% share in 2026, supported by the massive scale of consumption in China and Southeast Asia. This region is expected to drive global demand as rising disposable incomes allow millions of households to transition toward high-protein diets. The expansion of cold chain infrastructure is likely to enable the distribution of fresh beef into previously underserved inland provinces. Market penetration by the Australian Agricultural Company (AACo) with Darling Downs illustrates the regional focus on high-quality imported beef to satisfy luxury demand. This brand is expected to expand its presence in high-end Asian hospitality sectors as tourism recovers. The region's dominance is anticipated to be further bolstered by favorable trade agreements with major beef-exporting nations.

China is expected to act as the primary country anchor, shaping the overall momentum of the Asia Pacific beef sector. The Chinese government is expected to implement stricter food safety regulations that favor large, traceable international beef suppliers. This regulatory environment is likely to drive investment in high-tech processing facilities within the country’s borders. Engagement from JBS S.A. with Friboi in the Chinese market demonstrates the importance of large-scale export partnerships to meet local supply gaps. This company is expected to leverage its extensive distribution network to navigate evolving Chinese import protocols. Continued urbanization in China is anticipated to sustain the high demand for ground beef in the expanding fast-food sector.

North America Beef Market Trends

North America is expected to remain a mature and structurally stable regional market, with demand primarily anchored in established retail and food service sectors. This region is expected to focus on premiumization and the growth of specialized beef categories such as organic and grass-fed. Replacement cycles in the processing industry are likely to involve the adoption of advanced automation to combat labor shortages. Strategic positioning by Tyson Foods with Open Prairie Natural Meats reflects the regional shift toward antibiotic-free and sustainable beef products. This product line is expected to capture the growing "conscious consumer" segment in major US metropolitan areas. The market is anticipated to maintain steady volumes through a high-frequency consumption culture and robust domestic production.

The U.S. is expected to serve as the regional anchor, dictating trends in production efficiency and retail innovation. The U.S. beef industry is likely to lead the adoption of precision livestock farming to improve herd health and environmental outcomes. Regulatory updates regarding "Product of U.S." labeling are expected to influence consumer purchasing behavior toward domestic brands. Activities from Cargill with BeefUp Sustainability demonstrate the country’s commitment to reducing the carbon footprint of intensive beef production. This initiative is expected to involve large-scale partnerships with cattle ranchers to implement regenerative agricultural practices. The U.S. market is set to remain the global benchmark for high-quality, grain-fed beef standards.

Europe Beef Market Trends

Europe is expected to remain a mature and structurally stable regional market, with demand primarily anchored in high-quality standards and local geographical indications. This region is expected to experience a shift toward high-value, lower-volume consumption as environmental concerns influence dietary habits. Stringent EU regulations regarding animal welfare and chemical residues are likely to favor local producers with transparent supply chains. Participation from Minerva Foods with Casal Verde illustrates the focus on meeting European demands for ethically sourced, grass-fed beef from South America. This brand is expected to navigate complex EU import quotas through high-compliance certification programs. The market is anticipated to see growth in pre-packaged, portion-controlled cuts to suit smaller household sizes.

Germany is expected to be the country anchor for the European market, driven by its large population and central role in regional logistics. German consumers are likely to prioritize transparency and regionality when selecting beef products in retail settings. The expansion of discounter chains with high-quality fresh meat departments is expected to keep beef accessible to a wide demographic. Collaboration between local processors and Vion Food Group with Simmental Pur highlights the importance of regional breed heritage in the German market. This product line is expected to leverage its "local origin" status to maintain a competitive edge over non-European imports. Ireland anchors regional momentum through high per-capita consumption and export leadership. Industry structures facilitate Poland-like growth in value terms. WH Group with Smithfield EU Beef invests in sustainable ranching.

Competitive Landscape

The global beef market is characterized by a highly consolidated structure at the processing level, where a small number of multinational corporations control the majority of global trade volumes. These leading players maintain their dominance through extensive vertical integration, spanning from feedlot management to branded retail distribution. High capital requirements for modern slaughter facilities and cold chain logistics create significant barriers to entry for new competitors. Market leadership from JBS S.A., with Swift and Cargill with Sterling Silver, establishes global benchmarks for scale, food safety, and supply chain efficiency. These companies are expected to continue their dominance by acquiring smaller, specialized producers to diversify their premium portfolios.

Leading players exert influence through technology footprints like AI optimization and procurement leverage with ranchers. JBS S.A., with Friboi Premium, sets benchmarks in yield efficiency, while Tyson Foods, with Jimmy Dean Beef, commands brand equity in retail. Cargill with Angus Beef and Marfrig Global Foods with Swift Premium establish ecosystem standards via partnerships. These dynamics anchor supply stability amid shortages. Procurement relationships with global fast-food giants and major hypermarkets further solidify the influence of these industry titans.

Key Industry Developments:

- In March 2026, JBS SA announced an investment of £127 million (US$170.26 million) to expand a meat plant in Texas. This expansion enhances JBS's production capacity in the U.S., allowing it to better capture high-value market segments despite broader industry supply contractions.

- In February 2026, the Indian beef industry reached a milestone with Allana Group being recognized as the nation's top exporter of buffalo meat (carabeef). The group's dominance underscores India's role as a primary global supplier of affordable protein, particularly to Southeast Asia and Middle Eastern markets.

Companies Covered in Beef Market

- JBS S.A.

- Tyson Foods, Inc.

- Cargill, Inc.

- WH Group Limited

- Marfrig Global Foods

- Minerva Foods

- Danish Crown

- Vion Food Group

- NH Foods Ltd.

- Hormel Foods Corporation

- National Beef Packing Company

- BRF S.A.

- American Foods Group, LLC

- Agri Beef Co.

- Meyer Natural Foods

- Australian Agricultural Company

Frequently Asked Questions

The global beef market is likely to be valued at US$ 536.7 billion in 2026. It is expected to reach a value of US$750.2 billion by the year 2033.

The primary driver is the escalating demand for high-quality protein in emerging economies, combined with the global expansion of Halal-certified products. Improvements in cold chain logistics and the proliferation of quick-service restaurants also significantly contribute to market momentum.

The market is projected to grow at a CAGR of 4.9% during the forecast period from 2026 to 2033. This follows a historical growth rate of 4.2% recorded between 2020 and 2025.

Asia Pacific is the leading region in the global market. It is projected to account for approximately 51% of the total market share in 2026.

Major players include JBS S.A., Cargill, Inc., Tyson Foods, Inc., and Marfrig Global Foods. Other significant contributors are Minerva Foods, National Beef, and the Australian Agricultural Company.