- Executive Summary

- Global Bauxite Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Prison Growth Outlook

- Global Crime Rates by Country

- Global Prison Population by Country

- Global Private Prison Market Growth Outlook

- Other Macro-economic Factors

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 - 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Bauxite Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Global Bauxite Market Outlook: Grade

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Grade, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Grade, 2026-2033

- Metallurgical-grade

- Refractory-grade

- Other Grade

- Market Attractiveness Analysis: Grade

- Global Bauxite Market Outlook: Application

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Application, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Alumina & Aluminum production

- Refractory

- Cement & Construction

- Abrasives

- Chemical industry

- Others

- Market Attractiveness Analysis: Application

- Global Bauxite Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Bauxite Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Grade, 2026-2033

- Metallurgical-grade

- Refractory-grade

- Other Grade

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Alumina & Aluminum production

- Refractory

- Cement & Construction

- Abrasives

- Chemical industry

- Others

- Europe Bauxite Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Grade, 2026-2033

- Metallurgical-grade

- Refractory-grade

- Other Grade

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Alumina & Aluminum production

- Refractory

- Cement & Construction

- Abrasives

- Chemical industry

- Others

- East Asia Bauxite Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Grade, 2026-2033

- Metallurgical-grade

- Refractory-grade

- Other Grade

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Alumina & Aluminum production

- Refractory

- Cement & Construction

- Abrasives

- Chemical industry

- Others

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by , 2026-2033

- South Asia & Oceania Bauxite Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Grade, 2026-2033

- Metallurgical-grade

- Refractory-grade

- Other Grade

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Alumina & Aluminum production

- Refractory

- Cement & Construction

- Abrasives

- Chemical industry

- Others

- Latin America Bauxite Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Grade, 2026-2033

- Metallurgical-grade

- Refractory-grade

- Other Grade

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Alumina & Aluminum production

- Refractory

- Cement & Construction

- Abrasives

- Chemical industry

- Others

- Middle East & Africa Bauxite Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Grade, 2026-2033

- Metallurgical-grade

- Refractory-grade

- Other Grade

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Application, 2026-2033

- Alumina & Aluminum production

- Refractory

- Cement & Construction

- Abrasives

- Chemical industry

- Others

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Alcoa Corporation

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Rio Tinto

- Aluminum Corporation of China Limited (CHALCO)

- Norsk Hydro ASA

- South32

- RusAL

- NALCO India

- Hindalco Industries Ltd.

- Emirates Global Aluminum PJSC

- Maaden

- PT ANTAM Tbk

- Ashapura Minechem Ltd

- Jamalco

- Vedanta Resources

- Bosai Minerals Group

- Alcoa Corporation

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Metals & Minerals

- Bauxite Market

Bauxite Market Size, Share, and Growth Forecast 2026 - 2033

Bauxite Market by Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Autonomous Vehicles, Automated Guided Vehicles), Application (Powertrain, Safety, Body Electronics, Chassis, Telematics & Infotainment), and Regional Analysis, 2026 - 2033

Bauxite Market Size and Trend Analysis

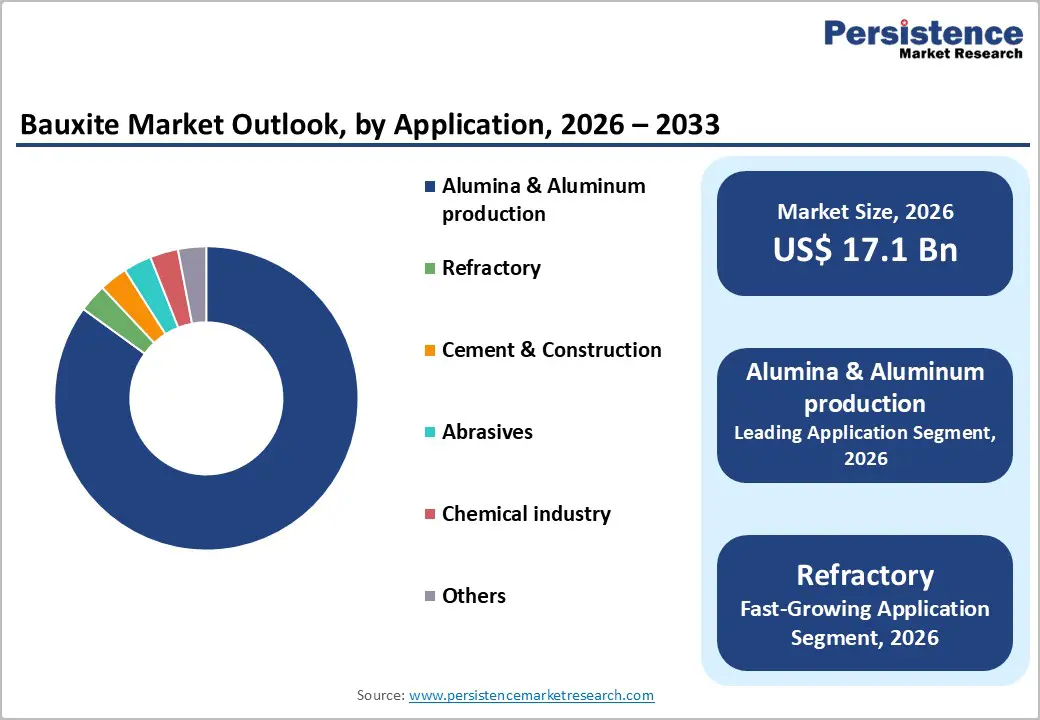

The global bauxite market size is expected to be valued at US$ 17.1 billion in 2026 and projected to reach US$ 21.3 billion by 2033, growing at a CAGR of 3.2% between 2026 and 2033.

The global market is experiencing robust growth driven by accelerating aluminum demand from electric vehicle manufacturing and renewable energy infrastructure development. Electric vehicles require 20-30% more aluminum than conventional internal combustion engine vehicles, and industry projections indicate that EV sales will reach approximately 40 million vehicles by 2030, directly translating into increased bauxite consumption. Additionally, the global renewable energy transition is amplifying demand for lightweight aluminum components in solar panels, wind turbines, and energy storage systems, further solidifying bauxite’s strategic importance in the emerging green economy.

Key Industry Highlights:

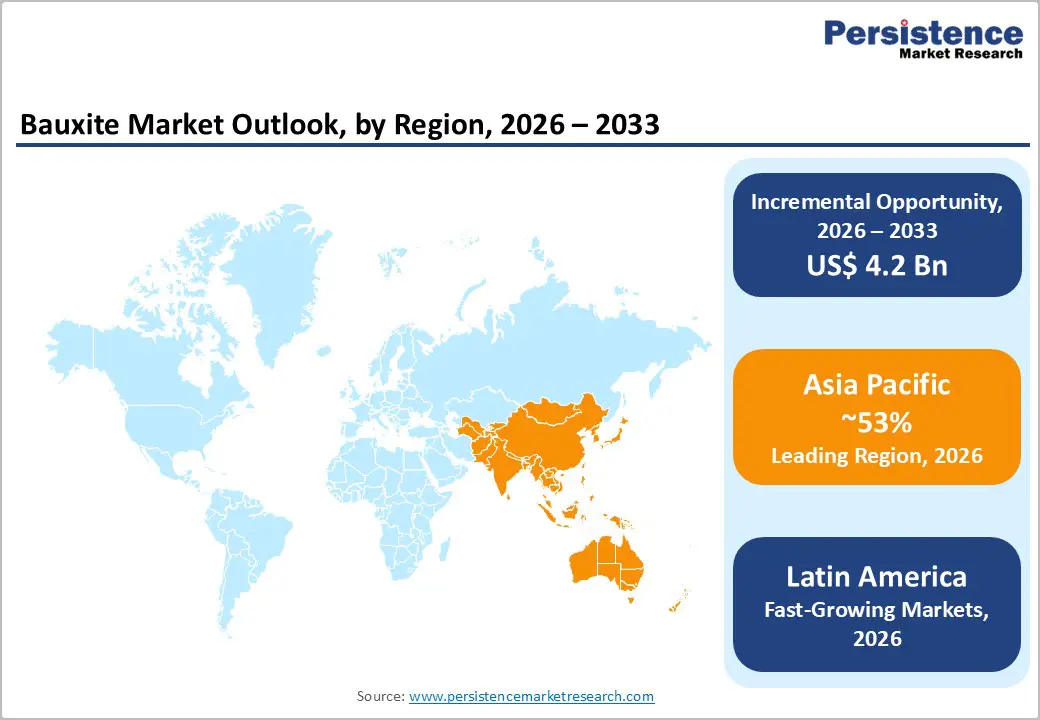

- Leading Region: Asia Pacific dominates bauxite consumption with approximately 53% global market share in 2024 driven by China’s aluminum manufacturing dominance and India’s infrastructure expansion initiatives.

- Fastest-Growing Region: Latin America is the fastest-growing regional market segment, projected to expand at approximately 4% CAGR, supported by Brazil’s growth in aluminum production and investment in domestic processing capacity and infrastructure development.

- Dominant Segment: Metallurgical-grade bauxite represents the dominant product segment, commanding approximately 85% market share in 2025, with sustained dominance supported by aluminum production’s persistent market centrality across transportation, construction, and emerging renewable energy applications.

- Fastest-Growing Segment: Refractory-grade bauxite applications are the fastest-growing segment, expanding at approximately 4.7% CAGR through 2032, driven by growth in electric arc furnace steel production and industrial demand for high-temperature-resistant materials in cement and glass manufacturing.

- Key Market Opportunity: Electric vehicle electrification and renewable energy infrastructure development represent the principal market opportunity, generating estimated incremental aluminum demand exceeding 10 million tonnes annually by 2030 and directly increasing bauxite consumption requirements.

| Key Insights | Details |

|---|---|

| Bauxite Market Size (2026E) | US$ 17.1 billion |

| Market Value Forecast (2033F) | US$ 21.3 billion |

| Projected Growth CAGR (2026 - 2033) | 3.2% |

| Historical Market Growth (2020 - 2025) | 2.4% |

Market Dynamics

Drivers - Surging Demand from Electric Vehicle and Renewable Energy Sectors

The electrification of global transportation and the accelerated adoption of renewable energy technologies represent transformative drivers for bauxite demand. International energy agencies project that global electric vehicle sales will reach approximately 42 million units by 2030, compared to around 9-10 million units in 2021. Each EV contains an average of 200-250 pounds of aluminum compared to approximately 150 pounds in traditional internal combustion engine vehicles.

The automotive industry alone is expected to account for over 40% of aluminum demand growth this decade. Furthermore, the integration of aluminum in solar photovoltaic panels and wind turbine components is creating substantial additional demand streams, as renewable energy infrastructure requires massive quantities of lightweight, corrosion-resistant materials. These converging trends position bauxite as an essential feedstock for meeting the material demands of the global energy transition.

Infrastructure Development and Urbanization in Emerging Economies

Emerging economies across the Asia Pacific, Latin America, and Africa are undertaking unprecedented infrastructure expansion initiatives that fundamentally depend on aluminum-intensive materials. Government programs such as India’s Housing for All initiative, China’s New Silk Road infrastructure projects, and Brazil’s urban development initiatives are driving robust construction demand. Global infrastructure investment is projected to exceed 4 trillion USD annually by 2030, with aluminum accounting for a significant share of material requirements in bridge construction, railway systems, aerospace components, and high-rise building frameworks.

The Asian Development Bank estimates that the Asia Pacific alone requires approximately 1.7 trillion USD in infrastructure investment through 2030, substantially benefiting aluminum producers and bauxite suppliers. Additionally, urbanization rates in developing nations continue to exceed 3% annually, driving ongoing demand for residential and commercial construction materials, where aluminum plays an increasingly critical role.

Restraints - Environmental Regulations and Sustainability Compliance Costs

The global mining industry faces escalating environmental regulations that increase operational complexity and capital expenditure for bauxite producers. The European Union’s proposed Carbon Border Adjustment Mechanism targets high-carbon aluminum imports, effectively creating price differentials that disadvantage bauxite operations with elevated carbon footprints. Environmental compliance costs related to land rehabilitation, water management, and greenhouse gas emissions reduction have increased by approximately 15-20% in the past three years across major producing regions.

Additionally, bauxite mining’s association with deforestation, particularly in tropical regions, has prompted international financial institutions to impose stricter lending criteria for mining expansion projects. Social license pressures from indigenous communities and environmental advocacy groups have delayed or cancelled multiple mining projects, with notable examples including permit challenges in Guinea and Australia that have affected regional production timelines.

Supply Chain Bottlenecks and Geopolitical Uncertainties

Bauxite supply chains face unprecedented disruptions from weather-related constraints, port congestion, and escalating geopolitical tensions. Guinea, which supplies approximately one-third of China’s bauxite imports and dominates global export markets, experiences significant seasonal volatility with monthly export volumes declining by approximately 19% during wet seasons due to flooding and transportation infrastructure limitations.

Guinea is advancing its strategy to limit raw bauxite exports and accelerate domestic alumina processing as part of a broader industrialization push. The government has launched construction of the $1.2 billion WCAG alumina refinery in Boké, aimed at producing about 1.2 million tonnes of alumina annually and deepening value addition within the country’s aluminium value chain. This project is a cornerstone of Guinea’s shift away from exporting unprocessed bauxite toward increasing local beneficiation and export of higher-value alumina.

Shipping delays, container shortages, and elevated freight costs have increased bauxite transportation expenses by 25-30% since 2022. The concentration of global bauxite supplies in a limited number of producing nations, with Guinea and Australia accounting for approximately 55% of global production, creates vulnerability to regional disruptions, political instability, or infrastructure failures that could rapidly constrain global aluminum supply chains, as seen when Australia in 2022 banned alumina and bauxite exports to Russia to restrict raw material flows amid geopolitical tensions, disrupting traditional trade patterns and underscoring supply-chain sensitivity to export controls.

Opportunity - Circular Economy Integration and Recycled Aluminum Growth

The global aluminum recycling industry presents transformative opportunities for bauxite market diversification and value chain optimization. Secondary aluminum production requires only 5% of the energy needed for primary aluminum production from bauxite, creating substantial economic and environmental incentives for increased recycling. Approximately 75% of all aluminum ever produced remains in active use today, demonstrating the material’s recyclability and longevity. Aluminum recycling rates exceed 90% in the automotive and construction sectors, with significant potential for expansion in consumer goods and packaging applications.

Major aluminum producers, including Rio Tinto, are expanding recycled aluminum capacity, with Rio Tinto adding 30,000 tonnes of new recycling capacity at its Arvida facility, scheduled for commissioning by Q4 2025. This circular economy transition creates opportunities for bauxite producers to position themselves as stewards of sustainable material value chains while maintaining demand for bauxite-derived primary aluminum to supplement recycled stocks, as global consumption continues to expand at approximately 3.5% annually.

Advanced Processing Technologies and Low-Carbon Refining Solutions

Technological breakthroughs in bauxite beneficiation and alumina refining present substantial commercial opportunities for market participants embracing innovation-driven competitive positioning. Artificial intelligence-powered ore sorting technologies now enable mining operations to achieve selective extraction improvements of 15-20% compared to conventional methods, while simultaneously reducing waste and environmental impact.

Low-carbon refining technologies that utilize hydrogen-powered calcination processes and integrate renewable energy are emerging as viable solutions to address carbon intensity concerns that increasingly influence purchasing decisions by downstream aluminum smelters and end-use manufacturers. Companies investing in green alumina production methods are positioning themselves to capture premium pricing from sustainability-conscious industrial buyers, while also accessing expanded financing opportunities from development finance institutions that prioritize energy transition compatibility. The estimated addressable market for low-carbon aluminum products is projected to expand from its current specialized niche applications to approximately 35-40% of total aluminum demand by 2035, creating substantial growth opportunities for bauxite suppliers that advance sustainability credentials.

Category-wise Analysis

Grade Insights

Metallurgical-grade bauxite dominates the global bauxite market, accounting for nearly 85% of total consumption, due to its critical role in primary aluminum production. With high alumina content and favorable alumina-to-silica ratios, this grade enables efficient processing through the Bayer process, lowering energy intensity and improving yield economics. Demand for metallurgical-grade bauxite remains structurally strong as aluminum consumption expands across transportation, construction, packaging, and electrical applications. The concentration of high-quality reserves in resource-rich countries underpins long-term supply security, while limited substitution possibilities reinforce its strategic importance. As global aluminum output continues to rise in response to electrification and infrastructure development, metallurgical-grade bauxite will remain the fundamental feedstock shaping market volumes and pricing dynamics.

Application Insights

Alumina and aluminum production represent the single most influential application segment in the bauxite market, consuming approximately 85% of global bauxite output. Bauxite serves as the indispensable raw material for alumina refining, which directly feeds primary aluminum smelting, creating a strong and linear demand relationship. Growth in this segment is driven by rising aluminum intensity in electric vehicles, renewable energy systems, power transmission, and lightweight construction materials. Ongoing capacity expansions in alumina refineries and aluminum smelters across Asia further strengthen consumption momentum. Given aluminum’s limited substitutes and its central role in decarbonization-oriented industries, alumina and aluminum production will continue to dictate bauxite demand trends throughout the forecast period.

Regional Insights

North America Bauxite Market Trends and Insights

North America’s bauxite market is shaped by strong downstream aluminum consumption and structurally limited domestic bauxite production, resulting in sustained reliance on imported raw materials. Aluminum demand is concentrated across transportation, aerospace, packaging, and construction sectors, where lightweighting, durability, and recyclability remain critical material attributes. The United States represents the primary demand center, with bauxite and alumina imports sourced largely from the Caribbean, Africa, and Australia through long-established trade corridors.

Regional market growth is projected to outpace the global average during the forecast period, supported by accelerated electrification of the automotive fleet and recovery in commercial aerospace manufacturing. Infrastructure modernization programs and steady commercial construction activity further underpin aluminum usage in structural components, façades, and building systems. Beverage packaging also represents a stable demand pillar, as aluminum cans continue to gain share over alternative materials due to sustainability and recycling advantages. Overall, North America’s bauxite market dynamics are driven less by mining expansion and more by downstream aluminum demand growth, supply security considerations, and evolving trade dependencies.

Europe Bauxite Market Trends and Insights

Europe’s bauxite market reflects mature demand conditions combined with increasingly stringent environmental and regulatory requirements that significantly influence sourcing and competitive dynamics. Aluminum consumption is concentrated in automotive manufacturing, aerospace production, renewable energy systems, and specialized construction applications, with growth increasingly skewed toward low-carbon and lightweight solutions. While overall aluminum demand growth remains moderate, electric vehicle production and renewable energy deployment are generating structurally higher aluminum intensity per unit of output.

The region is heavily dependent on imported bauxite and alumina, with limited domestic mining activity, making supply chain resilience a strategic concern. Regulatory frameworks, including carbon pricing mechanisms and sustainability disclosure mandates, are reshaping procurement strategies in favor of lower-emission material sources. At the same time, Europe’s strong circular economy ecosystem is expanding secondary aluminum production, with high recycling penetration in transportation and construction applications. This shift is moderating long-term growth in primary aluminum demand, positioning recycling and low-carbon sourcing as central competitive factors within the regional bauxite market.

Asia Pacific Bauxite Market Trends and Insights

Asia Pacific dominates global bauxite consumption patterns, accounting for approximately 53% of total bauxite demand in 2025 and expanding at a projected CAGR of approximately 4.2% through 2033, substantially outpacing global average growth rates. China is the region’s dominant demand center, consuming approximately 60-65% of total Asian bauxite volumes through its massive integrated aluminum production complex, which encompasses bauxite mining, alumina refining, and aluminum smelting operations. China’s bauxite imports reached approximately 103 million tonnes in the first half of 2025, reflecting extraordinary demand intensity from construction, automotive, electrical, and infrastructure sectors supporting urbanization and industrial expansion.

India’s accelerating bauxite production, rising from 23 million tonnes in 2023 to 24 million tonnes in 2025, reflects government initiatives to promote domestic aluminum production through expanded smelter capacity and integrated mining operations. India’s National Aluminium Company Limited is undertaking substantial capacity expansion initiatives, including planned aluminum smelter expansion of 0.5 MTPA and supporting bauxite mining development at Pottangi, scheduled for operational commencement by mid-2026.

Vietnam, Indonesia, and Malaysia are emerging as increasingly significant bauxite producers and aluminum processors, attracted by government policies promoting mineral beneficiation and downstream value-addition. Australia, positioning itself as the world’s second-largest bauxite exporter, maintains strategic supply relationships with Asian processors through long-term supply contracts and joint venture partnerships. Indonesia’s domestic alumina refining expansion, with companies including Bintan Alumina establishing 2-4 million tonnes annual refining capacity, is stimulating incremental bauxite demand while creating opportunities for regional backward integration.

Competitive Landscape

The global bauxite market demonstrates a moderately concentrated structure, where a small group of large-scale producers accounts for a significant share of global output, while numerous regional and country-specific operators maintain competitive relevance. Market leadership is primarily supported by access to high-grade reserves, scale advantages, established logistics infrastructure, and long-term supply relationships with alumina refineries and aluminum smelters. Despite concentration at the top, competitive intensity is increasing as new capacity additions and brownfield expansions strengthen supply diversity, particularly in resource-rich regions.

Competition is increasingly shaped by cost efficiency, technological capability, and vertical integration strategies rather than pricing alone. Producers are investing in automation, advanced beneficiation, and digital mining technologies to improve recovery rates and lower operating costs. Vertical integration across mining, refining, and smelting is widely adopted to enhance margin stability and supply security. Sustainability performance has become a critical differentiator, with producers focusing on emissions reduction, responsible mining practices, and ESG compliance to meet evolving customer and regulatory expectations.

Key Market Developments

- November 2025: Rio Tinto completed record annual bauxite production at its Australian operations, achieving approximately 58.7 million metric tons in 2024 while advancing expansion initiatives including the Norman Creek access project at Weipa and the Kangwinan project scheduled for development.

- October 2025: India’s bauxite exports increased 67.6% year-on-year, reaching ~405,000 tonnes during January-September 2025, supported by higher domestic production and capacity expansion, indicating improved supply availability and declining import dependence.

- September 2025: Guinea’s bauxite exports reached 39.41 million metric tonnes in Q3 2025, representing 23% growth compared to Q3 2024, demonstrating the country’s dominant position as global bauxite supply foundation despite seasonal and regulatory challenges.

Companies Covered in Bauxite Market

- Alcoa Corporation

- Rio Tinto

- Aluminum Corporation of China Limited (CHALCO)

- Norsk Hydro ASA

- South32

- RusAL

- NALCO India

- Hindalco Industries Ltd.

- Emirates Global Aluminum PJSC

- Maaden

- PT ANTAM Tbk

- Ashapura Minechem Ltd

- Jamalco

- Vedanta Resources

- Bosai Minerals Group

Frequently Asked Questions

The global bauxite market is projected to reach US$ 17.1 billion in 2026, driven by rising aluminum demand from electric vehicles and renewable energy infrastructure.

Growth is driven by electric vehicle production, renewable energy expansion, rapid urbanization, and increasing aluminum use in construction and infrastructure.

Asia Pacific leads global consumption, supported by China’s aluminum manufacturing scale and India’s infrastructure-led demand growth.

Electric vehicle electrification and renewable energy projects present the key opportunity by driving sustained incremental aluminum demand.

Alcoa Corporation, Rio Tinto, Aluminum Corporation of China Limited (CHALCO), Norsk Hydro ASA, South32, and RusAL are the leading companies in global bauxite market.