- Food Ingredients & Additives

- Avocado-Based Products Market

Avocado-Based Products Market Size, Share, and Growth Forecast, 2026-2033

Avocado-Based Products Market by Nature (Organic, Conventional), Product Type (Avocado Puree, Avocado Oil, Avocado Powder), End-Use (Food & Beverage, Personal Care & Cosmetics, Nutraceuticals, Household), and Regional Analysis for 2026-2033

Avocado-Based Products Market Share and Trends Analysis

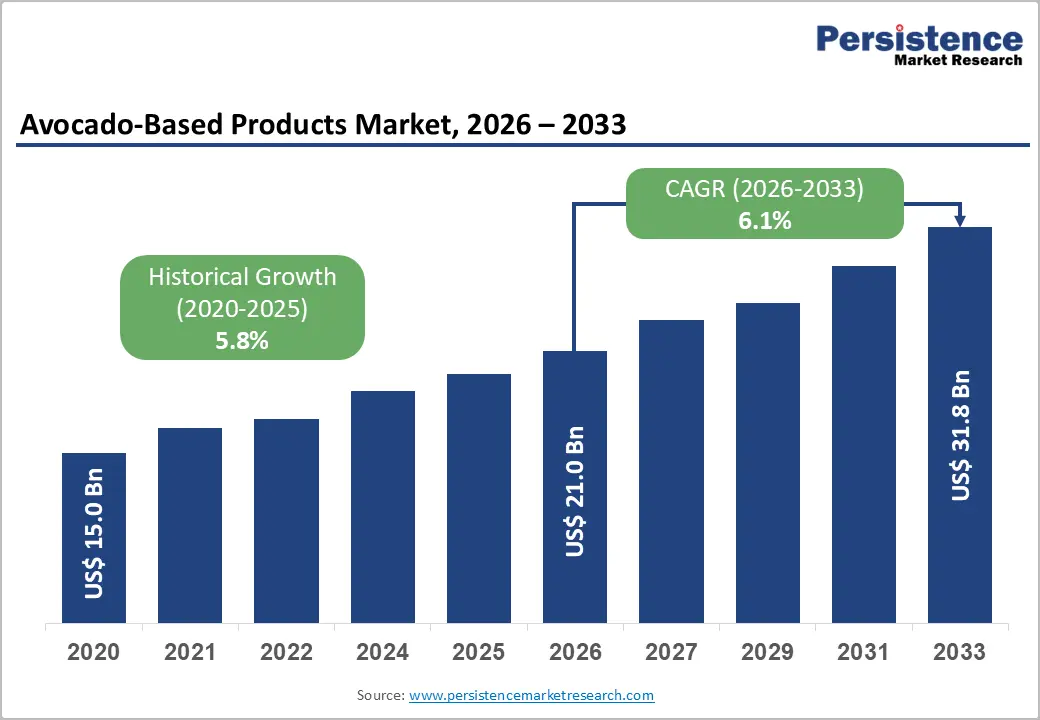

The global avocado-based products market size is likely to be valued at US$ 21.0 billion in 2026, and is projected to reach US$ 31.8 billion by 2033, growing at a CAGR of 6.1% during the forecast period 2026 - 2033. Market expansion is being driven by rising health-conscious consumption and the increasing preference for nutrient-dense, plant-derived ingredients across food and beverage categories.

Demand is also rising as avocado derivatives are gaining wider adoption in packaged foods, personal care formulations, and nutraceutical applications. Growing consumer focus on plant-based fats, clean-label positioning, and functional nutrition is reinforcing sustained volume growth across both developed and emerging markets. Improvements in avocado cultivation efficiency are strengthening output stability across key producing regions such as Latin America and the Asia Pacific. Advances in agricultural practices, post-harvest handling, and cold-chain logistics are supporting higher yields and reduced waste, thereby improving cost competitiveness. Regulatory recognition of avocado oil as a heart-healthy fat is continuing to enhance its acceptance in mainstream diets, while rising disposable incomes in emerging economies are supporting premium food and wellness product consumption.

Key Industry Highlights

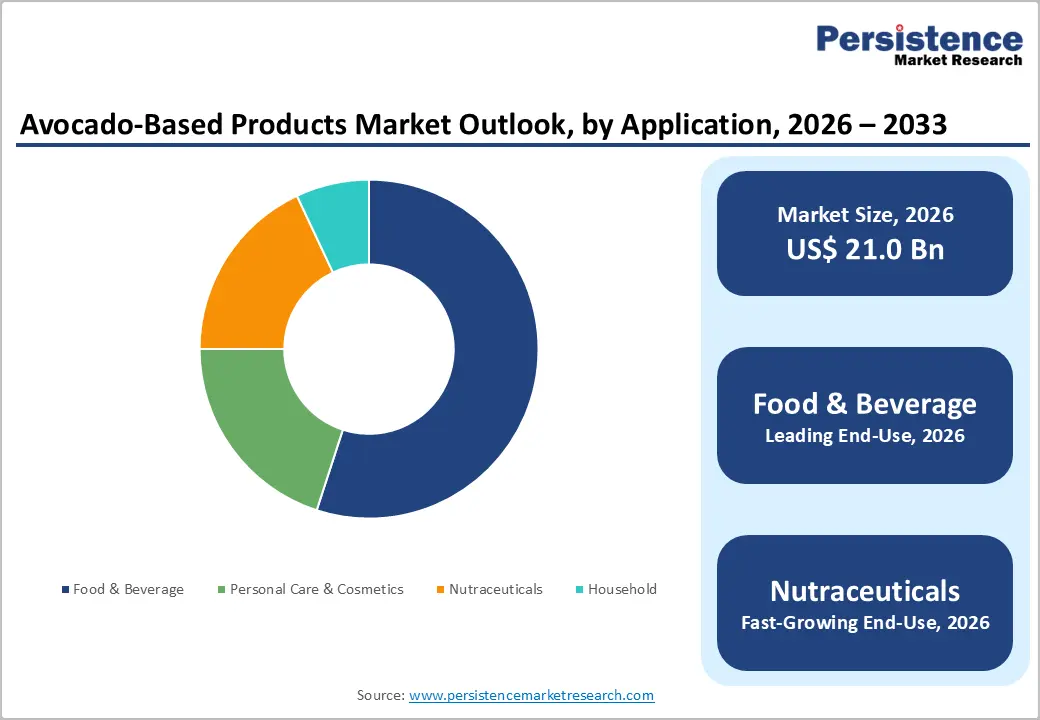

- Dominant End-Use: The food & beverage segment is projected to lead with around 55% revenue share in 2026, driven by the incorporation of natural ingredients in processed, ready-to-eat, and convenience foods.

- Leading Product: Avocado oil is expected to dominate with about 45% in 2026, while avocado powder is anticipated to be the fastest-growing with a 7.5% CAGR, driven by its versatility across food, personal care, and dietary supplements.

- High-Growth Application Area: Nutraceuticals are projected to register the fastest growth with 8.5% CAGR during 2026–2033, fueled by the rising adoption of plant-based and functional nutrition products.

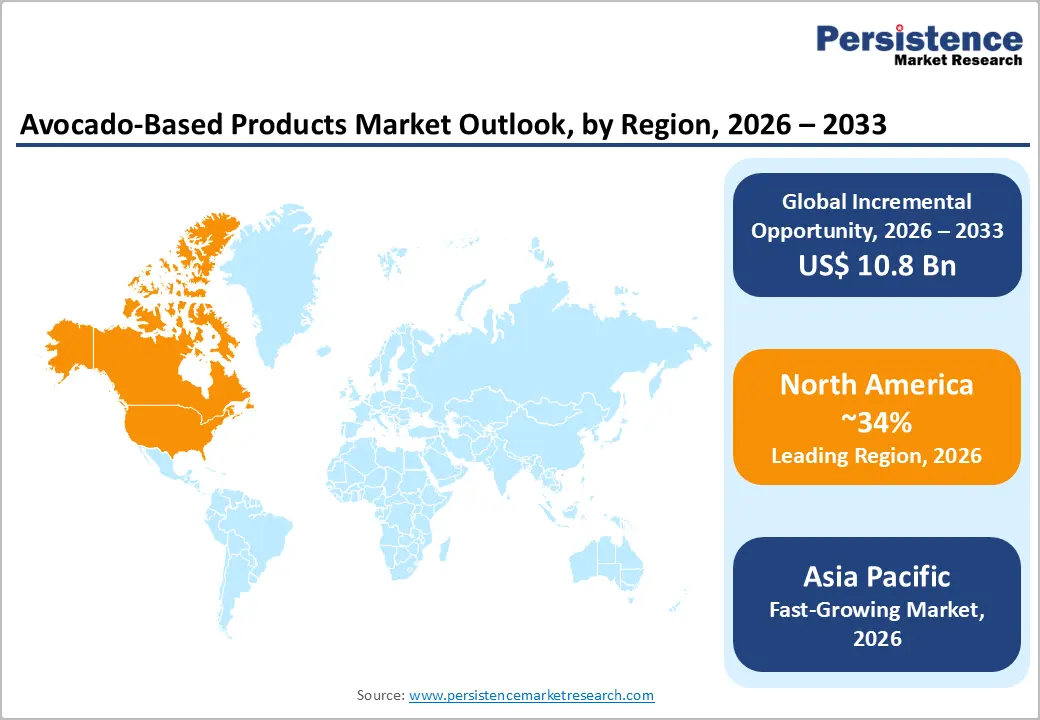

- Regional Leadership and Growth: North America is expected to lead with roughly 34% market share in 2026, owing to high per-capita consumption and advanced processing, while Asia Pacific is projected to be the fastest-growing market at 7.3% CAGR through 2033.

- Competitive and Investment Landscape: Investments are directed toward processing capacity expansion and sustainable sourcing, driven by the need to enhance supply-chain resilience and yield efficiency.

| Key Insights | Details |

|---|---|

| Avocado-Based Products Market Size (2026E) | US$21.0 Bn |

| Market Value Forecast (2033F) | US$ 31.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expanding Adoption of Avocado-Based Ingredients across Diverse Applications

Dietary preferences are increasingly shifting toward plant-based, nutrient-dense foods, positioning avocado-based products as a preferred source of monounsaturated fats, potassium, and antioxidants. The global avocado production exceeded 9 million metric tons in 2023, reflecting sustained consumption growth across both developed and emerging markets. Per-capita avocado consumption has been rising at an annual rate of 5–6% in North America and Europe, reinforcing mainstream dietary acceptance. This trend has directly increased the use of avocado puree and avocado oil in processed foods, functional beverages, and dietary supplements. As a result, manufacturers are benefiting from stronger demand visibility and improved long-term revenue stability. The expanding role of avocados across food systems continues to support value-added product innovation.

Beyond food and nutrition, avocado-based ingredients, particularly avocado oil, are gaining strong traction in premium skincare, haircare, and dermatological formulations due to their high oleic acid content and natural vitamin E profile. The Personal Care Products Council (PCPC) confirms that plant-derived emollients now account for over 35% of new cosmetic ingredient launches worldwide, accelerating commercial adoption. At the same time, advancements in cold-press extraction, spray-drying, and freeze-drying technologies have reduced post-harvest losses to below 10% since 2023. These efficiency improvements have lowered per-unit production costs and enabled scalable use of avocado powder and puree. These factors are strengthening margins while enhancing supply-chain resilience across end-use industries.

Supply Volatility and Cost Pressures across the Avocado Value Chain

Avocado cultivation is highly climate-dependent, with recurring droughts in major producing countries such as Mexico, Peru, and Chile periodically disrupting global supply availability. A recent report on climate risks highlighted yield volatility of ±20% annually in key avocado-growing regions, primarily due to increasing water scarcity and climate variability. Such fluctuations directly affect the consistency of raw material supply, creating uncertainty for processors and ingredient manufacturers. As a result, price volatility in fresh avocados and derived inputs remains a persistent challenge. This instability complicates procurement planning and limits the ability to secure long-term supply contracts. The impact is particularly pronounced for processors dependent on stable, high-quality inputs.

The organic avocado products face elevated production and compliance costs, driven by land transition requirements, traceability audits, and export-related regulatory obligations. According to industry estimates, organic certification increases production costs by 20–30% compared to conventional supply, reducing cost competitiveness. These higher input costs restrict the adoption of organic products in price-sensitive emerging markets and limit volume scalability. Small and mid-sized processors are especially affected, as thinner margins reduce their capacity to absorb cost fluctuations. These structural cost pressures are likely to constrain profitability prospects across the organic avocado segment. Such climate-induced supply volatility and compliance-driven cost inflation remain key limitations for the market.

Growth in Emerging Markets, Sustainability, and Private-Label Products

The avocado-based products market is benefiting from rapid growth in emerging markets, particularly in the Asia Pacific, where consumption is increasing rapidly across China, India, and ASEAN, supported by an explosion in urban populations over the last few decades and higher disposable incomes. Industry developments underline this trend, such as Sresta Natural Bioproducts Ltd. launching avocado powder under its 24 Mantra Organic brand in India, and Zhejiang Vegmax Biotech Co., Ltd. investing in large-scale spray-drying facilities in China to serve domestic and ASEAN markets, expanding local processing capacity and product availability. These initiatives highlight how emerging economies are becoming hubs for functional food and supplement innovations.

Sustainability considerations and private-label growth are creating new value streams across the industry. Westfalia Fruit entered Europe’s private-label segment through strategic avocado oil supply agreements with major retailer chains across 12 countries, enhancing market reach and shelf presence. SunOpta Inc.’s expansion of its Ontario processing facility to include avocado powder production reflects growing investment in ingredient sourcing to minimize import reliance and stabilize raw material costs. With the expansion of private-label avocado oils and spreads supported by third-party manufacturers serving global retail partners, these developments are driving innovation, improving profitability, and reinforcing differentiated value propositions across food, beverage, and wellness categories.

Category-wise Analysis

Nature Insights

Conventional avocado-based products are expected to continue their domination in the nature segment, accounting for approximately 45% of total market revenue in 2026, supported by economies of scale, lower raw material costs, and wide geographic availability. Conventional supply chains are preferred by foodservice operators and mass-market food manufacturers due to stable yields, consistent pricing, and established distribution networks. Industry developments have further strengthened this leadership: for example, Mission Produce expanded its avocado processing partnership with Westfalia Fruit to enhance conventional ingredient supply in North America, reinforcing availability across food and beverage and industrial channels. Conventional formats also benefit from broader application flexibility, from culinary oils to sauces and spreads, sustaining their dominant position.

Organic avocado-based products are projected to be the fastest-growing segment, expanding at an approximate CAGR of 7.5% through 2033, propelled by rising consumer demand for certified organic food and clean-label personal care products. Increased acceptance of premium pricing in developed regions such as Europe and North America supports margin expansion for organic variants. Companies like Chosen Foods launched new organic, cold-pressed avocado oils targeting health-conscious retail channels, boosting visibility for organic formats. Additionally, nutraceutical and cosmetics formulators are increasingly specifying organic inputs, accelerating adoption. Regulatory support and certification frameworks in developed markets further underpin growth prospects for organic avocado derivatives.

Product Type Insights

Avocado oil is slated to be the leading product type, accounting for over 45% of total market value in 2026, underpinned by its broad cross-industry use in food, cosmetics, and dietary supplements. Its versatility is reflected in strong demand from retail cooking oils, foodservice applications, and clean-label personal care formulations that leverage avocado oil’s nutritional profile and high smoke point. Recent industry developments reinforce this role: Fresh Del Monte acquired a majority stake in avocado oil producer Avolio, scaling global production capacity to meet rising demand and reduce waste by utilizing pulp that might otherwise be discarded. Similarly, Whole Foods Market and Chipotle Mexican Grill expanded avocado oil usage across their cooking oil portfolios, reflecting mainstream adoption in foodservice.

Avocado powder is set to be the fastest-growing product type, projected to grow at a 7.5% CAGR, driven by convenience, extended shelf life, and rising demand in functional beverages, bakery premixes, and nutraceutical capsules. Product innovation highlights this trend, such as OVAVO LTD’s launch of a finer-mesh avocado powder for meal replacement beverages and functional foods, positioning the format for premium applications. Avocado powder’s neutral taste and nutrient retention make it attractive for plant-based product developers. Such partnerships between avocado powder producers and food manufacturers for customized ingredient solutions in snacks and supplements have emerged, broadening adoption. This growth trajectory reflects the increasing role of powder formats in expanding application diversity.

End Use Insights

Food & beverage is likely to remain the dominant end-use industry, commanding an estimated 55% of the avocado-based products market revenue share in 2026, driven by processed foods, sauces, spreads, and ready-to-eat meals that incorporate avocado derivatives for flavor, nutritional fortification, and clean-label positioning. Institutional foodservice segments also contribute steadily as operators seek healthier fat alternatives and premium ingredient profiles. Industry activity demonstrates how foodservice and retail are accelerating adoption: Avocados From Mexico introduced a new line of avocado-based snacks and sauces, targeting broader dietary occasions and younger consumer cohorts, expanding use cases beyond traditional applications.

Nutraceuticals represent the fastest-growing end-use segment, expanding at an approximate 7.8% CAGR through 2033, supported by increasing clinical recognition of cardiovascular and metabolic health benefits associated with avocado-derived fats and phytochemicals. This growth is reinforced by product launches that position avocado ingredients in targeted wellness categories, such as Herbalife Nutrition’s launch of an avocado powder-based smoothie mix for sports nutrition and heart health. The segment’s expansion is also supported by a rising pipeline of functional formulations incorporating avocado extracts for anti-inflammatory and antioxidant support. Rising consumer interest in plant-based nutraceutical interventions further drives demand in both developed and emerging markets.

Regional Insights

North America Avocado-Based Products Market Trends

North America is likely to lead with approximately 34% of the avocado-based products market share in 2026, led by the United States, which remains the world’s largest avocado consumer. High per-capita intake, deep penetration across foodservice, and widespread use of avocado oil and puree in packaged foods underpin stable demand. Clear regulatory frameworks for food, dietary supplements, and personal care enable faster commercialization of new formulations. Government-backed specialty crop programs and sustainability-linked incentives support water efficiency, post-harvest infrastructure, and domestic value-added processing, reinforcing supply reliability. Strong import linkages with Latin America further strengthen year-round availability and cost stability.

The market maturity in North America is increasingly defined by scale-driven processing investments, sourcing aligned with environmental, social, & governance (ESG) standards and mandates, and foodservice-led adoption. Large food chains such as Chipotle Mexican Grill and Sweetgreen expanded their use of avocado oil, reflecting mainstream acceptance of healthier fats. On the supply side, Mission Produce and Westfalia Fruit expanded U.S. ripening and processing capacities, improving traceability and shelf-life management. Institutional investors continue to favor avocado value chains due to transparent sourcing and sustainability metrics. These factors collectively sustain North America’s leadership position.

Europe Avocado-Based Products Market Trends

Europe accounts for a major share of global revenues, positioning itself as the second-largest regional market for avocado-based products through 2033. The demand for these ingredients is concentrated in Germany, the U.K., France, and Spain, supported by strong consumer preference for clean-label, organic, and plant-based products. Harmonized regional regulations enable consistent quality standards across food, cosmetics, and nutraceutical applications. Policy alignment under the European Union (EU) Farm to Fork Strategy and the Common Agricultural Policy (CAP) promotes organic agriculture, traceability, and reduced environmental impact. Spain’s geographic proximity to cultivation zones reinforces its role as a key regional processing and distribution hub.

The avocado-based products market growth in Europe is increasingly driven by premiumization, private-label expansion, and processing optimization rather than volume consumption alone. Leading European retailers expanded private-label avocado oil, spreads, and functional food offerings, improving price accessibility without compromising quality. Westfalia Fruit strengthened private-label supply partnerships across multiple European markets, supporting consistent sourcing. Investments in cold-pressed oil and puree processing facilities in Spain enhanced efficiency and compliance. These developments position Europe as a stable, high-value market with strong regulatory backing.

Asia Pacific Avocado-Based Products Market Trends

Asia Pacific is projected to be the fastest-growing regional market for avocado-based products during the 2026-2033 forecast period and is expected to expand at an estimated CAGR of 7.3%. Growth is being driven by rising demand in China, India, and Southeast Asia for plant-based processed foods and beverages, supported by rapid urbanization and gradual dietary westernization. Increasing consumer awareness of functional nutrition is accelerating avocado adoption across food, beverage, and wellness categories. Although per-capita consumption remains lower than in North America and Europe, the addressable consumer base is expanding quickly due to population scale and rising disposable incomes. Government support for food processing, cold-chain development, and value-added agriculture is continuing to improve processing feasibility and cost competitiveness, particularly in India and ASEAN economies.

Regional growth momentum is being shaped by manufacturing scale-up, localized product development, and export-oriented strategies. Indian food and wellness brands are increasingly incorporating avocado powder and avocado oil into functional foods and dietary supplements that are targeting urban consumers seeking clean-label and plant-based nutrition. In China, investment in spray-drying and oil extraction facilities is expanding under modern agricultural industrial park programs, which are strengthening domestic processing capacity and reducing reliance on imports. Several ASEAN countries are also introducing incentives to support processed food exports, which is improving regional integration into global supply chains. Together, these developments are positioning the Asia Pacific as the primary growth engine of the global avocado-based products market over the forecast period.

Competitive Landscape

The global avocado-based products market is remaining moderately fragmented, with multinational agribusiness firms and vertically integrated growers continuing to play a central role in shaping supply and pricing dynamics. Leading companies such as Mission Produce, Calavo Growers, Westfalia Fruit, Olivado Group, and AVOCOOP are maintaining significant market presence through integrated sourcing, processing, and distribution networks. Competition is primarily centered on supply reliability, quality consistency, and end-to-end traceability, which are becoming critical purchasing criteria for food, personal care, and nutraceutical manufacturers. Product portfolios are increasingly covering avocado oil, avocado puree, and avocado powder applications, enabling suppliers to serve diversified demand across multiple end-use industries. Ongoing investment in processing capacity, cold-chain infrastructure, and sustainability programs is strengthening competitive positioning and supporting long-term contract relationships with global buyers.

Alongside large players, regional and niche producers are continuing to complement the competitive landscape by focusing on organic-certified products, private-label manufacturing, and specialty ingredient segments. Producers operating close to major cultivation hubs are benefiting from lower logistics costs and improved access to fresher raw materials, which is enhancing margins and product quality. High entry barriers, including climate variability, certification compliance, and logistics complexity, are limiting the pace of new market entry. Smaller firms are increasingly participating through business-to-business ingredient supply partnerships rather than branded consumer channels.

Key Industry Developments

- In January 2026, Mission Produce announced the acquisition of Calavo Growers in a cash-and-stock deal valued at approximately US$ 430 million, with the deal expected to close by August 2026. The transaction expands Mission’s North American scale and adds Calavo’s prepared foods portfolio, including guacamole and dips.

- In May 2025, Chosen Foods launched four new avocado oil-based dressings – Zesty Italian, Homestyle Balsamic, Greek Artichoke, and Strawberry Pistachio – plus reformulated Classic Ranch, Steakhouse Caesar, and Lemon Garlic, using 100% pure avocado oil, premium vinegars/herbs, and pear juice.

The products aim to transform the salad dressing category amid consumer dissatisfaction. - In March 2025, Fresh Del Monte Produce acquired a majority stake in Avolio, an avocado oil producer, to expand into specialty ingredients. The move enables the conversion of surplus avocados into premium oil, reducing food waste, supporting circular economy goals and positioning Del Monte as a leader in sustainable avocado oil production.

Companies Covered in Avocado-Based Products Market

- Westfalia Fruit

- Calavo Growers

- Olivado Group

- Mission Produce

- Grupo Bimbo

- Simplot Global Food

- Salud Foodgroup

- La Tourangelle

- Spectrum Organics

- Sesajal S.A. de C.V.

- Mount Kenya Fresh Produce

- Proteco Oils

Frequently Asked Questions

The global avocado-based products market is projected to reach US$ 21.0 billion in 2026.

Rising adoption of plant-based and functional nutrition, increasing use of avocado oil in cosmetics, and improvements in processing efficiency and supply chains are key market drivers.

The market is poised to witness a CAGR of 6.1% from 2026 to 2033.

The opportunities include rapid growth in Asia Pacific functional foods, expansion of private-label avocado oils and powders, and sustainability-driven innovations such as waste upcycling.

Mission Produce Inc., Calavo Growers Inc., Westfalia Fruit, Olivado Group, and AVOCOOP are few of the key players in the market.