- Automotive Components & Materials

- Aviation Lubricants Market

Aviation Lubricants Market Size, Share, and Growth Forecast 2026 - 2033

Aviation Lubricants Market by Product Type (Engine Oil, Hydraulic Fluid, Grease, Special Lubricants & Additives, Turbine Oil, Piston Oil, Bearing Oil), Technology (Synthetic, Semi-synthetic, Mineral, Bio-based), Aircraft Type (Commercial Aviation, Military Aviation, Business & General Aviation, Helicopters), End-user (OEM, MRO), and Regional Analysis, 2026 - 2033

Aviation Lubricants Market Size and Trend Analysis

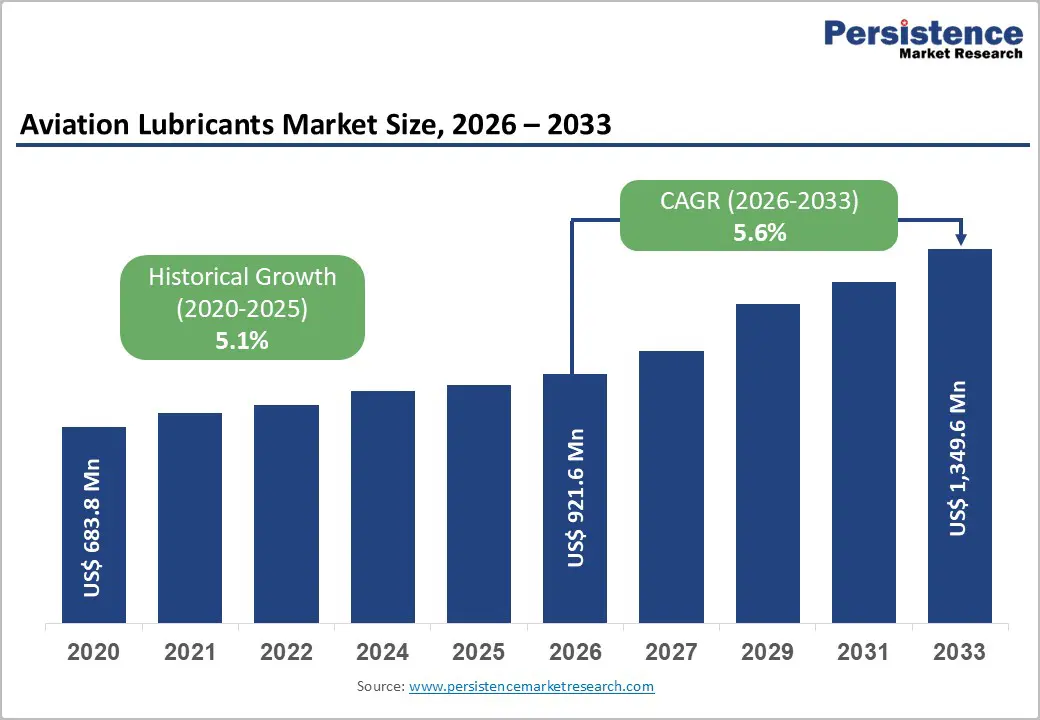

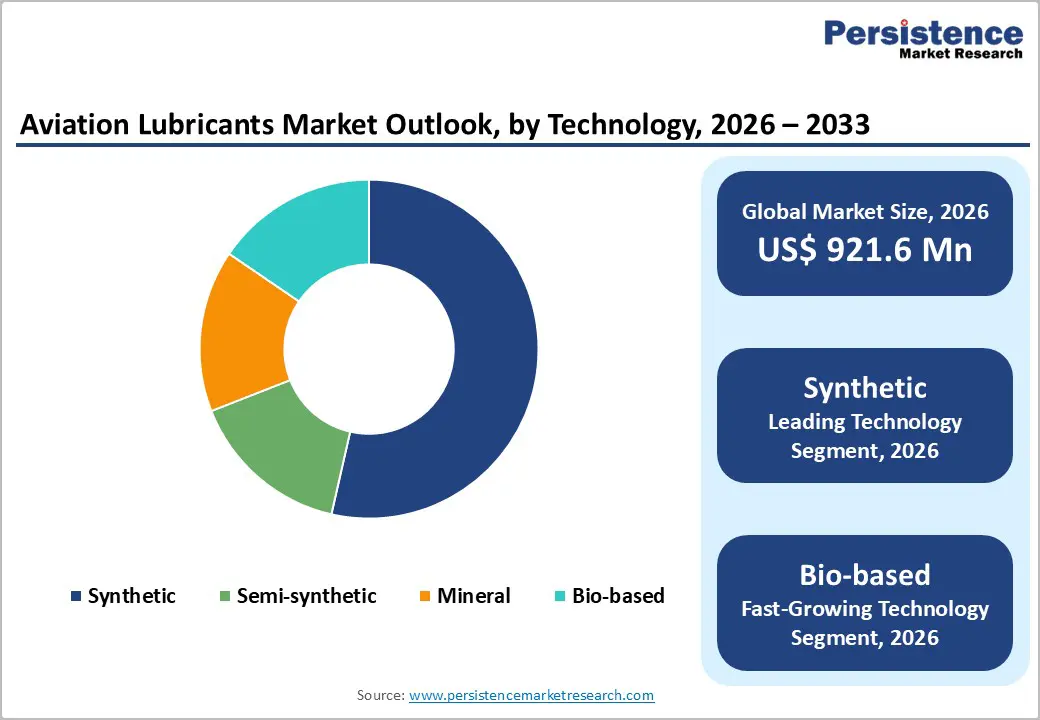

The global aviation lubricants market size is expected to reach US$ 921.6 million in 2026 and is projected to reach US$ 1,349.6 million by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

The market is driven by a robust recovery in global air travel demand, a rapidly expanding aircraft fleet, and stringent regulatory standards mandating high-performance lubrication solutions. According to IATA, global air passenger traffic exceeded 4 billion travelers in recent years, directly elevating engine utilization and lubricant consumption cycles. The accelerating shift toward advanced synthetic formulations, necessitated by next-generation turbofan engines (GTF/LEAP) that operate at thermal extremes above 240°C, further reinforces consistent demand for specialized aviation lubricants across both commercial and defense aviation segments.

Key Industry Highlights:

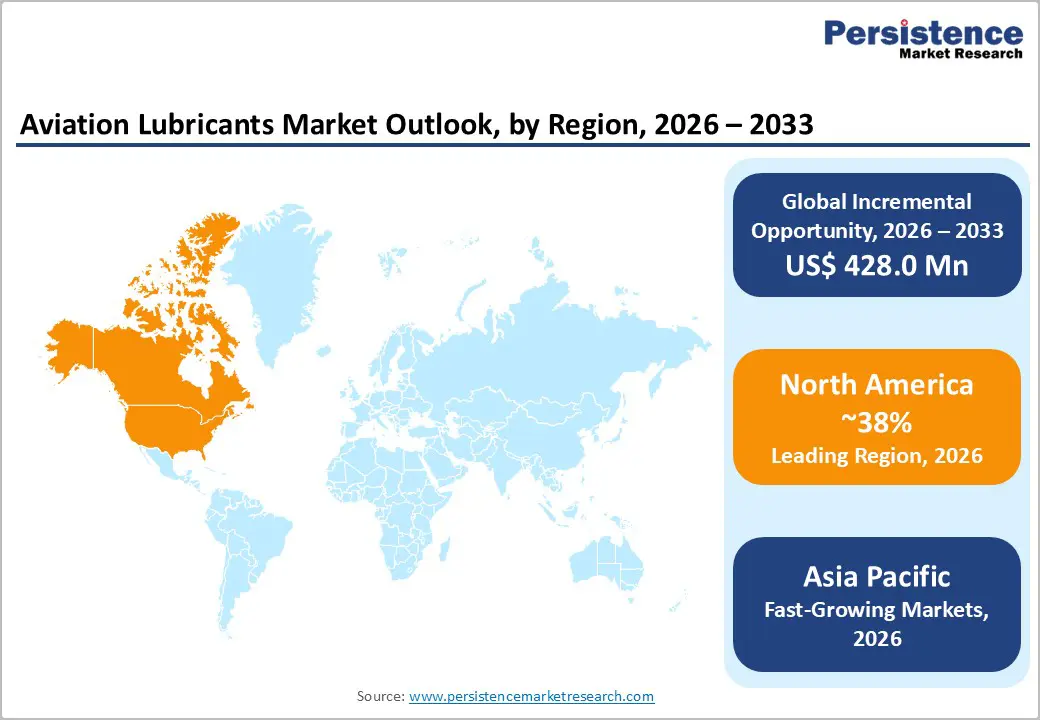

- Leading Region: North America dominates the global Aviation Lubricants market with approximately 38% market share in 2025, driven by the world's largest commercial and military aviation sector, a dense MRO network, and rigorous FAA regulatory frameworks mandating advanced lubricant performance standards.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market in Aviation Lubricants, propelled by China's 18.7% passenger traffic growth in 2024, India's fleet expansion, and ASEAN aviation infrastructure investments, collectively driving the region toward the highest CAGR during 2026 - 2033.

- Dominant Product Segment: Engine Oil is the dominant product type segment, capturing approximately 55% market share in 2025, underpinned by mandatory replacement cycles of every 600-1,000 flight hours and the critical role of turbine oils in next-generation commercial and military aircraft engines.

- Fastest Growing Segment: Bio-based lubricants are the fastest-growing technology segment, recording approximately 12% adoption growth between 2023 and 2025, driven by ICAO's CORSIA mandates and the EU's ReFuelEU Aviation Regulation, compelling airlines to shift to sustainable lubrication solutions.

- Key Opportunity: A key market opportunity lies in the MRO-driven demand surge across Asia Pacific's expanding fleet of over 8,500 commercial aircraft, offering high-growth potential for synthetic and bio-based lubricant manufacturers who can establish certified supply chains and long-term OEM partnerships in the region.

| Key Insights | Details |

|---|---|

| Aviation Lubricants Market Size (2026E) | US$ 921.6 Million |

| Market Value Forecast (2033F) | US$ 1,349.6 Million |

| Projected Growth CAGR (2026 - 2033) | 5.6% |

| Historical Market Growth (2020 - 2025) | 5.1% |

Market Dynamics

Drivers - Surging Global Air Traffic and Fleet Expansion Fueling Lubricant Demand

The exponential rise in global air passenger traffic is one of the most powerful catalysts for the aviation lubricants market. According to ACI World and ICAO projections, global air passenger traffic is expected to reach approximately 9.8 billion by 2025, reflecting one of the strongest growth trajectories in modern aviation history. This surge has directly elevated flight hours, component utilization, and lubricant replenishment cycles. Both Airbus and Boeing combined to deliver over 1,100 aircraft in 2024, with the Airbus backlog reaching a record 8,658 aircraft. Modern commercial aircraft require lubricant replacement every 600-1,000 flight hours, creating a perpetual, recurring demand base across the global commercial fleet of more than 26,000 operational aircraft.

Stringent Regulatory Standards and Technological Advancements in Synthetic Lubricants

Regulatory bodies such as the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA) impose rigorous performance standards for aviation lubricants, including compliance with MIL-PRF-23699 and SAE AS5780 specifications. The FAA's Part 33 regulations govern detailed certification processes for turbine engine oils, compelling manufacturers to invest heavily in advanced formulations. These regulatory pressures, combined with the growing adoption of next-generation GTF and LEAP engines, which demand lubricants with superior thermal-oxidative stability, have accelerated the development of high-performance synthetic lubricants. Airlines increased synthetic oil procurement by approximately 25% between 2023 and 2025, reflecting the industry-wide transition toward enhanced lubrication solutions that extend maintenance intervals and reduce operational costs.

Restraints - Volatility in Crude Oil and Base Oil Prices

Aviation lubricants are primarily derived from petroleum-based base oils, making the market highly susceptible to crude oil price volatility. Base oil prices have historically fluctuated by up to 25% annually, directly affecting lubricant production costs and manufacturers' profit margins. This price instability creates significant challenges in maintaining stable pricing strategies, particularly for smaller or regional lubricant suppliers who lack the scale to absorb cost shocks. For large airlines operating on thin margins, unpredictable lubricant procurement costs can disrupt maintenance budgets and long-term supply contracts, potentially slowing adoption of premium formulations.

Lengthy Certification Timelines and High Barriers to Entry

Bringing a new aviation lubricant to market requires extensive testing and certification processes, typically lasting between 18 and 36 months and incurring considerable regulatory compliance costs. The FAA and EASA require comprehensive compatibility testing against OEM specifications for engine components, hydraulic systems, and airframe elements. These requirements represent a formidable barrier for new entrants and smaller innovators seeking to introduce novel bio-based or synthetic formulations. Additionally, specialized handling and storage requirements add 15-20% to distribution costs, further constraining the profitability of market expansion, especially in emerging or remote aviation markets.

Opportunities - Rise of Bio-Based and Eco-Friendly Aviation Lubricants Under CORSIA and Green Aviation Mandates

The implementation of the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) by ICAO is compelling the aviation industry to adopt environmentally sustainable products, creating a significant commercial opportunity for bio-based lubricant manufacturers. Bio-based and eco-friendly lubricants recorded approximately 12% growth between 2023 and 2025, while sustainability-oriented formulations captured nearly 15% of new product launches in 2024. The EU's ReFuelEU Aviation Regulation is further pushing European aviation stakeholders toward greener alternatives. Leading players such as Shell plc and TotalEnergies SE are actively investing in biodegradable turbine oils and renewable-feedstock lubricants. The global bio-lubricants market is projected to grow at a CAGR of 14.16% through 2035, signaling immense headroom for aviation-specific bio-based formulations in the coming years.

Asia Pacific Fleet Expansion and MRO Infrastructure Growth: Unlocking New Demand Horizons

The Asia Pacific region presents one of the most compelling growth opportunities for aviation lubricant market participants, driven by rapid fleet expansion, increasing disposable incomes, and massive investments in aviation infrastructure. China's aviation market recorded an 18.7% increase in passenger numbers in 2024 compared to 2023, according to IATA, while India's booming domestic aviation market continues to attract fleet additions by carriers such as IndiGo and Air India. The region hosts more than 8,500 commercial aircraft and over 15,000 general aviation aircraft, all of which require regular lubricant provisioning. As the region's MRO sector scales up to accommodate these growing fleets, demand for engine oils, hydraulic fluids, and greases is expected to grow at nearly double the global average CAGR, presenting a lucrative window for both multinational and regional lubricant manufacturers.

Category-wise Analysis

Product Type Insights

Engine oil is the dominant product type in the Aviation Lubricants market, accounting for approximately 55% of total market share in 2025. This dominance is attributed to the critical role engine oil plays in ensuring turbine and piston engine reliability, reducing metal-to-metal contact, and dissipating heat generated during extreme operational cycles. Modern turbofan engines, which represent the majority of the global commercial fleet, require engine oils capable of maintaining thermal stability above 240°C and resisting oxidative degradation under pressures exceeding 5,000 psi. Regular replacement intervals of 600-1,000 flight hours ensure a recurring, high-volume demand. Global commercial aviation fleet lubricant consumption exceeds 320 million liters annually, with engine oils accounting for the largest volume, reinforcing their leadership across the OEM and MRO value chain.

Technology Insights

Synthetic lubricants represent the leading technology segment in the Aviation Lubricants market, commanding approximately 55% market share in 2025. Their dominance is rooted in superior performance characteristics, including exceptional thermal-oxidative stability, low volatility, and minimal deposit formation, that align with the demanding specifications of next-generation GTF and LEAP turbofan engines. Airlines increased procurement of high-performance synthetic oils by 25% between 2023 and 2025, reflecting a decisive industry shift away from mineral-based formulations. Key synthetic types, such as polyalphaolefin (PAO)-based lubricants and synthetic esters, which comply with MIL-PRF-23699 and SAE AS5780 standards, are now used in nearly 46% of modern aircraft. Bio-based lubricants are the fastest-growing technology segment, benefiting from CORSIA mandates and rising sustainability priorities across global airlines.

Aircraft Type Insights

Commercial aviation is the leading aircraft type segment in the Aviation Lubricants market, representing approximately 55% of total market share in 2025. This segment's dominance is underpinned by the sheer scale of the global commercial fleet, exceeding 26,000 operational aircraft, and the high-frequency maintenance schedules inherent to commercial operations. According to OAG data, high-frequency routes such as Jeju-Seoul handled over 13.2 million passengers in 2024, with shorter stage lengths and higher flight frequencies accelerating component wear and lubricant consumption. Commercial operators maintain strict ICAO- and EASA-mandated maintenance protocols, ensuring systematic, high-volume procurement of engine oils, hydraulic fluids, and greases across global airline fleets, further cementing commercial aviation's leadership in the overall market.

End-user Insights

The MRO (Maintenance, Repair & Overhaul) segment is the dominant end user in the Aviation Lubricants market, holding approximately 60% of total market share in 2025. The aftermarket nature of MRO ensures persistently high lubricant consumption, as aircraft components operate under extreme thermal and mechanical stress, necessitating frequent lubricant replenishment and replacement. More than 54% of global MRO facilities have shifted to long-life lubricants, reducing maintenance downtime by approximately 17%. The U.S. alone has approximately 9,000 commercial aircraft requiring consistent MRO-linked lubricant servicing. As aircraft prices are high and purchase frequency is low, lubricant consumption in MRO significantly outpaces OEM first-fill demand, making the aftermarket a structurally larger and more stable segment for aviation lubricant market participants.

Regional Insights

North America Aviation Lubricants Market Trends and Insights

North America leads the global Aviation Lubricants market with approximately 38% market share for aviation lubricants, driven by the world's largest and most active commercial and military aviation ecosystem. The United States alone accounts for approximately 80% of the regional demand and approximately 35% of global consumption. With over 9,000 commercial aircraft, 21,000 general aviation aircraft, and approximately 13,000 military aviation assets, the U.S. generates consistent, high-volume lubricant demand. The U.S. Air Force executed approximately 1.03 million flying hours in 2024 and allocated a budget for 1.09 million hours in 2025, reinforcing sustained military lubricant consumption.

From a regulatory and innovation standpoint, the FAA's Part 33 certification requirements and updates to ASTM D4059 specifications for turbine engine oils have compelled manufacturers to invest in advanced synthetic formulations. The FAA Reauthorization Act of 2024 and related mandates on extended oil drain intervals are accelerating the transition to synthetic lubricants across the region. Major OEMs such as Boeing and Lockheed Martin, combined with a dense network of certified MRO centers, create a deeply integrated lubricant supply ecosystem, making North America a critical innovation hub for the global aviation lubricants industry.

Europe Aviation Lubricants Market Trends and Insights

Europe is the second-largest regional market for aviation lubricants, supported by a robust commercial fleet, a well-established MRO infrastructure, and strong regulatory compliance frameworks. The region recorded over 7 million annual commercial flights, each requiring regular lubricant replenishment across engine oil, grease, and hydraulic fluid categories. The United Kingdom, Germany, France, Spain, and Italy collectively host over 450 certified MRO centers conducting approximately 90,000 maintenance operations annually. NATO military fleets, comprising more than 6,500 aircraft across member states, generate additional demand for high-performance specialty lubricants.

The EU's ReFuelEU Aviation Regulation and EASA's ongoing alignment with ICAO CORSIA standards are compelling European operators to prioritize sustainable formulations. Bio-based lubricant adoption grew an estimated 14% between 2023 and 2025 across European markets, and synthetic lubricants represent approximately 58% of regional consumption. France benefits significantly from the Airbus manufacturing hub and a 4.0% CAGR trajectory for its national aviation lubricants sector through 2035, while Germany is projected to grow at 4.5%, supported by aerospace innovation leadership.

Asia Pacific Aviation Lubricants Market Trends and Insights

Asia Pacific is the fastest-growing region with the highest projected CAGR during 2026-2033, driven by unprecedented fleet expansion, rising middle-class travel demand, and escalating defense aviation investments. China's aviation market saw a 18.7% increase in passenger volumes in 2024 relative to 2023, according to IATA, while handling approximately 730-741 million travelers during the same period. India's aviation lubricants sector is expected to expand at a CAGR of 6.0%+ through 2033, supported by a growing domestic fleet and strategic investments in MRO capabilities under the government's UDAN (Ude Desh ka Aam Nagrik) regional aviation connectivity scheme.

Japan, South Korea, and the ASEAN bloc are further amplifying demand through fleet modernization and airport capacity expansion programs. The Asia Pacific region hosts more than 8,500 commercial aircraft and over 15,000 general aviation aircraft. Air travel growth rates in the region are nearly double the global average, attracting heightened attention from global lubricant manufacturers. Companies such as China Petroleum & Chemical Corporation (Sinopec) and AVI-OIL India [P] Ltd are strategically positioned to cater to this accelerating regional demand for specialized aviation lubricants.

Competitive Landscape

The global Aviation Lubricants market exhibits a semi-consolidated structure, with a few large multinational energy and specialty chemical companies accounting for a substantial portion of global supply while several regional producers serve niche or localized demand. Leading suppliers maintain strong market positions through well-established aviation brands, extensive distribution networks, and long-standing relationships with aircraft manufacturers, airlines, and maintenance service providers.

Competitive strategies primarily focus on securing long-term supply agreements with OEMs and MRO operators, alongside sustained investment in high-performance synthetic formulations designed to meet evolving aviation safety and efficiency standards. Companies are also expanding research in bio-based and low-carbon lubricant technologies to align with aviation decarbonization goals. Digitalization is emerging as an important differentiator, with lubricant condition monitoring, predictive maintenance solutions, and AI-driven performance analytics gaining traction. Additionally, mergers, acquisitions, and strategic partnerships are being pursued to strengthen global supply chains, expand product portfolios, and increase presence in rapidly growing aviation markets across the Asia Pacific and the Middle East.

Key Developments:

- January, 2024: Shell plc signed a long-term agreement with Air Europa to supply AeroShell aviation lubricants, including engine oils, greases, and fluids, for the airline’s Boeing 737 and 787 Dreamliner fleet and associated maintenance operations.

- June, 2025: NYCO unveiled TURBONYCOIL® 940 SE, a new synthetic turbine oil developed after a decade of research to deliver high thermal and oxidation stability while incorporating safer additive technologies for modern aircraft engines.

Companies Covered in Aviation Lubricants Market

- Shell plc

- Exxon Mobil Corporation

- BP p.l.c.

- TotalEnergies SE

- NYCO S.A.

- Eastman Chemical Company

- LANXESS Corporation

- Radco Industries, Inc.

- The Chemours Company FC, LLC

- DuPont de Nemours, Inc.

- Aerospace Lubricants, Inc.

- Eni S.p.A.

- China Petroleum & Chemical Corporation (Sinopec)

- AVI-OIL India [P] Ltd

- Phillips 66 Company

- FUCHS Group

- Chevron Corporation

- Nye Lubricants, Inc.

- Lukoil Aviation

Frequently Asked Questions

The global Aviation Lubricants market is estimated to reach US$ 921.6 million in 2026, supported by recovering air travel demand, expanding aircraft fleets, and increasing use of high-performance synthetic and bio-based lubricants.

Key demand drivers include rising global air passenger traffic, expanding aircraft production backlogs, stringent aviation safety regulations, and increasing defense aviation spending.

North America leads the Aviation Lubricants market, accounting for around 38% of global demand, supported by a large aviation fleet, strong MRO infrastructure, and strict regulatory standards.

A major growth opportunity lies in Asia Pacific’s rapidly expanding aviation sector and the rising adoption of sustainable bio-based aviation lubricants.

Key players include Shell plc, ExxonMobil, TotalEnergies, BP, NYCO, Eastman Chemical Company, Chemours, DuPont, LANXESS, and Phillips 66.