- Automotive Components & Materials

- Automotive MCU Market

Automotive MCU Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Automotive MCU Market by Product Type (8-bit, 16-bit, 32-bit, 64-bit), Application (ADAS and Basic Safety, Body, Comfort, and Vehicle Lighting, Infotainment Components, Powertrain Components), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles), and Regional Analysis from 2026 to 2033

Automotive MCU Market Share and Trends Analysis

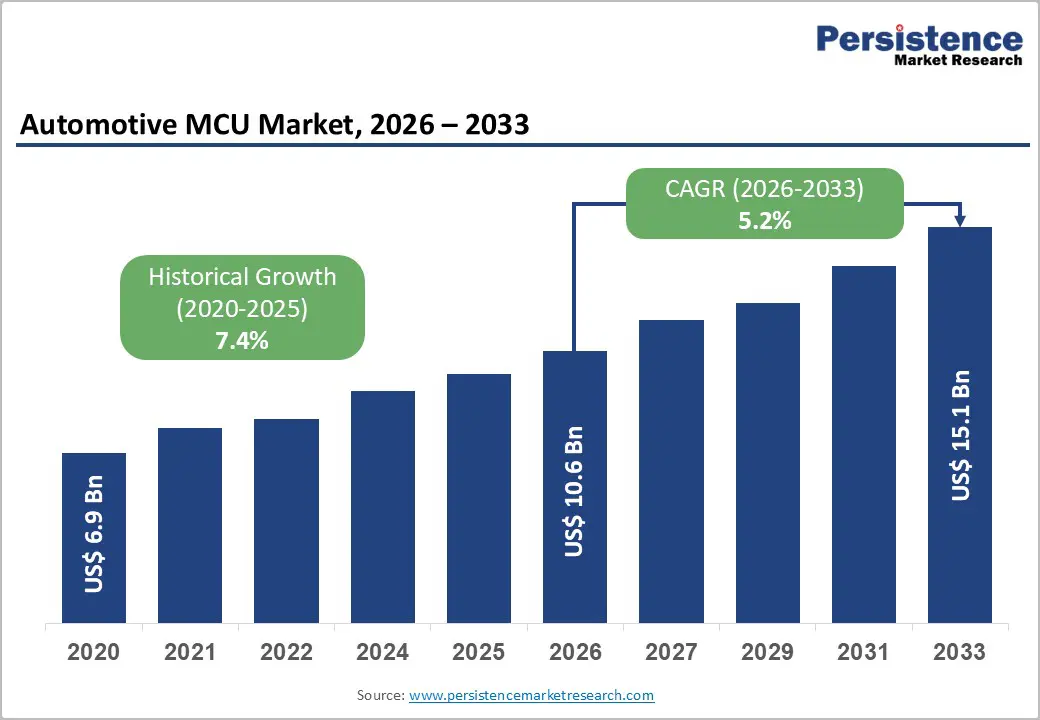

The global automotive mcu market size is projected at US$10.6 billion in 2026 and is projected to reach US$15.1 billion by 2033, growing at a CAGR of about 5.2% between 2026 and 2033.

Rising semiconductor content per vehicle, especially for electrified powertrains and ADAS, is steadily lifting MCU demand. Regulatory mandates on safety and emissions are accelerating the penetration of electronic controls in both mass-market and premium vehicles. Rapid growth in Asia Pacific production volumes, alongside premium infotainment and body electronics in North America and Europe, underpins medium-term expansion.

Key Industry Highlights:

- The Automotive MCU market is projected to grow from about US$10.6 billion in 2026 to roughly US$15.1 billion by 2033, at an estimated CAGR of 5.2% over the period.

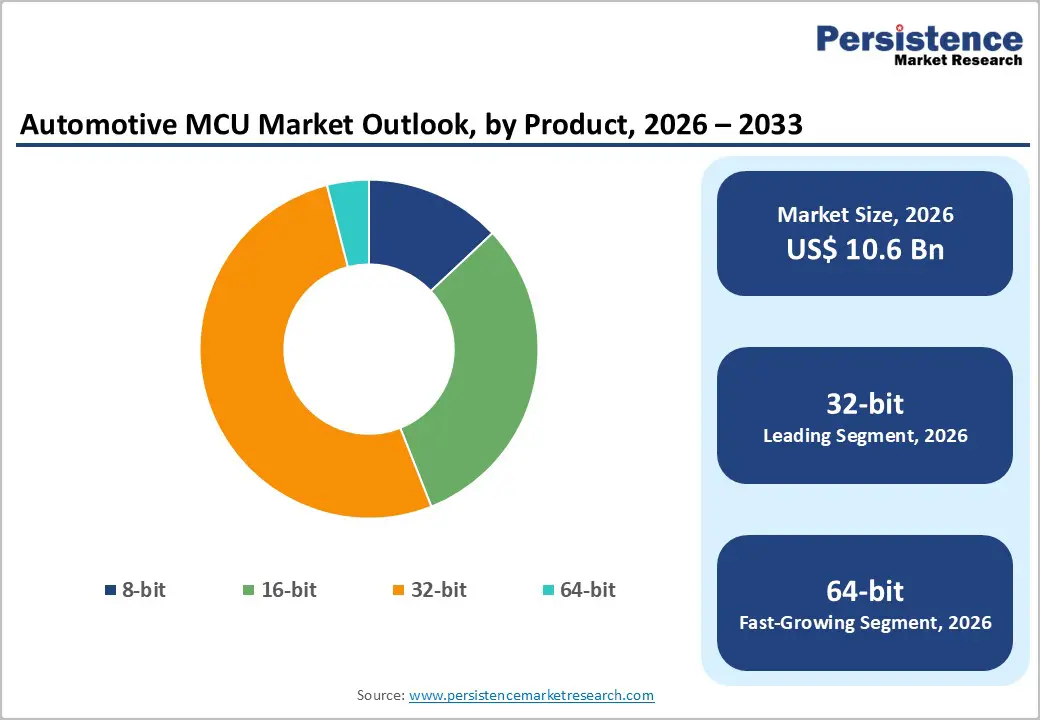

- 32-bit MCUs dominate with about 52% share, while 64-bit devices expand at approximately 8.5% CAGR as domain and zonal architectures scale.

- Body, Comfort, and Vehicle Lighting holds around 38% share, whereas ADAS and Basic Safety applications grow near 9.7% CAGR, driven by global safety mandates.

- Passenger Cars contribute roughly 45% of revenue, while Electric Vehicles show the fastest MCU demand growth at about 9% CAGR.

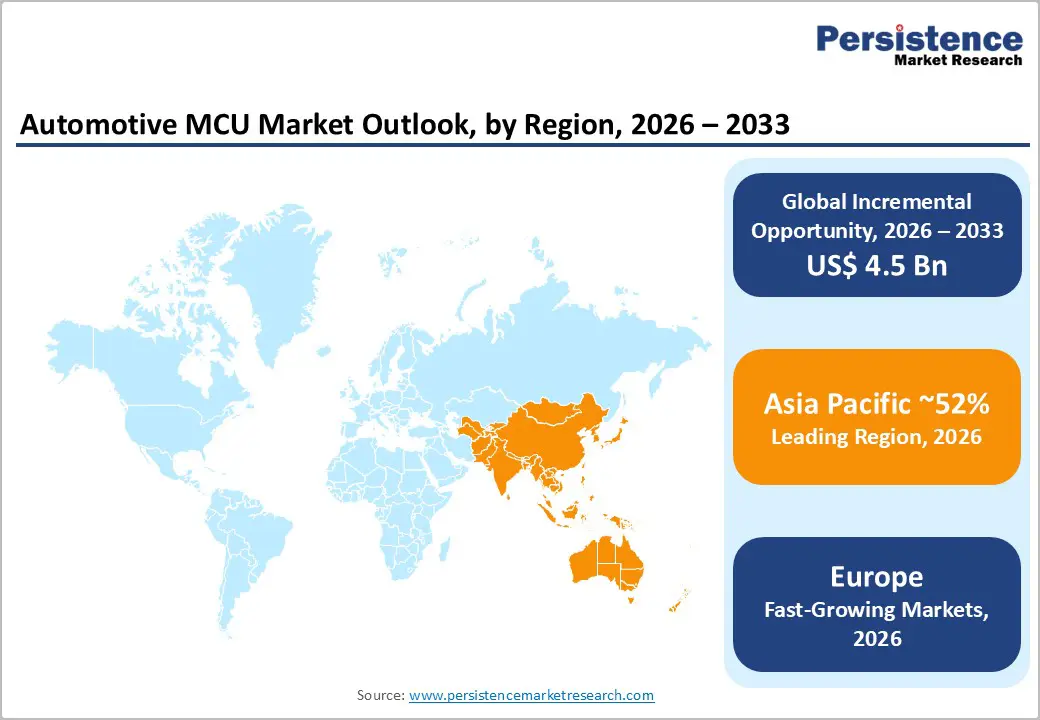

- Asia Pacific leads with around 52% regional share and is the fastest growing market, while Europe accounts for approximately 23.1% of global revenue.

- North America’s Automotive MCU demand is expected to grow at about 3.7% CAGR, supported by EV programs and advanced infotainment penetration.

- Recent strategic moves include launches of AI-capable automotive MCUs, EV-focused powertrain controllers, and portfolio-expanding acquisitions among top suppliers.

| Key Insights | Details |

|---|---|

| Automotive MCU Market Size (2026E) | US$ 10.6 Billion |

| Market Value Forecast (2033F) | US$ 15.1 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.2% |

| Historical Market Growth (2020 - 2025) | 7.4% |

Market Dynamics Analysis

Drivers - Growing Penetration of ADAS and Safety Electronics

Global regulators increasingly mandate advanced driver assistance features such as automatic emergency braking, lane-keeping assistance, and stability control, all of which rely on high-performance MCUs for sensor fusion, actuation, and diagnostics. The safety and ADAS application segment in automotive electronics is expanding at double-digit growth rates, with some studies indicating CAGRs above 13% for safety MCU use in the second half of the decade. This regulatory-driven, non-discretionary adoption structurally raises MCU content per vehicle, supporting sustained unit and value growth through 2033. Safety and ADAS MCU demand is expanding faster than the broader automotive semiconductor market as Level 2 and Level 2+ driver-assistance systems become standard across mid-range and high-volume vehicle platforms globally. Increasing penetration of radar, camera, and sensor-fusion architectures requires higher processing capability and functional safety compliance, accelerating deployment of advanced automotive-grade microcontrollers.

Electrification of powertrain and EV volume growth

The rapid shift toward hybrid and battery electric vehicles requires significantly more MCUs per vehicle to manage battery, inverter, thermal systems, on-board charging, and advanced energy management. Many national and regional decarbonization policies, including zero-emission vehicle targets in Europe, North America, and China, are pushing EV and plug-in hybrid penetration higher through 2030. As a result, the automotive MCU market increasingly tracks EV production growth, with EV-related control units forming one of the most attractive multi-year demand pools for suppliers. Electrified vehicles integrate sophisticated battery management systems, motor control units, and power electronics that require reliable high-performance microcontrollers for real-time monitoring and system optimization. Increasing EV model launches across global OEM portfolios, along with expanding charging ecosystems and supportive incentives, are further accelerating semiconductor content growth within electric powertrain

Restraints - Supply chain volatility and semiconductor capacity constraints

The sector remains exposed to cyclical and shock-driven wafer supply constraints, as demonstrated by the 2020–2022 global chip shortage, when production disruptions in foundries and packaging plants curtailed MCU availability for automakers. OEMs and Tier-1s were forced to temporarily idle assembly plants and reschedule programs, highlighting reliance on a concentrated set of MCU suppliers. Such structural vulnerabilities create pricing volatility, lengthen design cycles, and incentivize risk-averse sourcing strategies that can delay platform transitions.

Pricing pressure and commoditization in lower-end MCUs

While high-end automotive MCUs command premium pricing, 8-bit and 16-bit devices used in basic body or legacy applications face intense competition and erosion. Large OEMs increasingly leverage scale to compress per-unit costs, and new regional players introduce low-cost alternatives, particularly in Asia. This dynamic squeezes margins in traditional segments, forcing incumbents to continuously optimize die size and process nodes or exit some low-value tiers, limiting overall profitability growth.

Opportunity - Shift toward 64-bit and domain/zonal architectures

The move from distributed ECUs toward centralized domain and zonal architectures creates an opportunity for higher-performance 32-bit and 64-bit MCUs with richer memory, security, and networking features. As OEMs re-platform electronics to support software-defined vehicles, demand for these advanced controllers could represent a multi-billion-dollar incremental opportunity by the early 2030s, particularly in premium and upper-mid segments. Suppliers that align portfolios with zonal control, high-speed networking, and over-the-air upgradability stand to capture outsized value. Modern vehicles integrate networked body control modules, LED lighting systems, zonal controllers, and rich infotainment platforms, all of which depend on 32-bit and 64-bit MCUs for performance and connectivity. Asia Pacific’s dominance in vehicle production and strong consumer demand for connected and feature-rich cars are driving growth in electronic content per unit, with the region accounting for close to half of global automotive microcontroller demand, strengthening long-term growth potential.

Asia Pacific manufacturing and EV expansion

Asia Pacific accounts for the largest regional share in automotive microcontrollers, supported by high vehicle output in China, Japan, South Korea, and India and aggressive EV promotion policies. With regional microcontroller markets expected to grow at high single- to low double-digit CAGRs across automotive and industrial applications, incremental addressable demand for automotive MCUs in the Asia Pacific alone could reach several billion dollars over the next decade. Localized production and ecosystem partnerships can help global suppliers tap this volume profitably. Rapid expansion of electric-vehicle manufacturing hubs, rising domestic OEM production, and strong semiconductor supply-chain investments are further reinforcing the region’s importance in automotive electronics. Growing adoption of advanced driver assistance systems, connected vehicle technologies, and electrified powertrains across Asia Pacific markets is increasing microcontroller demand per vehicle, creating significant long-term opportunities for both global and regional semiconductor suppliers.

Category-wise Analysis

Product Insights

The 32-bit product type currently leads the Automotive MCU market with an estimated share of around 52%, reflecting its balance of performance, cost, and power efficiency for mainstream automotive body, powertrain, and infotainment applications. OEMs favor 32-bit architectures for scalable software development and compliance with evolving functional safety and cybersecurity requirements, especially in global vehicle platforms targeting multiple regions over long lifecycles.

The 64-bit segment is the fastest growing within product types, advancing at an estimated CAGR of about 8.5% as automakers migrate toward domain and zonal architectures with higher compute needs. Demand is particularly strong in ADAS, autonomous driving, and high-end infotainment, where memory bandwidth, security, and over-the-air update capability is critical.

Application Insights

Body, comfort, and vehicle lighting represent the leading application segment, accounting for roughly 38% of the Automotive MCU market, driven by broad penetration across all vehicle classes and trim levels. Typical use cases include body control modules, HVAC, seat and mirror adjustment, window lifters, smart lighting, and entry systems, all of which rely on cost-optimized but increasingly networked MCUs to deliver comfort and efficiency improvements at scale.

The ADAS and Basic Safety segment is the fastest growing, with MCU demand expanding at an estimated CAGR of around 9.7% as safety regulations tighten worldwide and advanced assistance features cascade into mass-market segments. Growth stems from mandatory features such as autonomous emergency braking, lane support, and advanced airbag systems, as well as OEM-driven differentiation through higher-level ADAS packages.

Vehicle Type Insights

Passenger Cars are the leading vehicle type, contributing roughly 45% of global Automotive MCU revenue, reflecting their dominant share of global production and higher average electronic content than many commercial vehicles. Mid-size and premium passenger models, in particular, integrate multiple MCUs for body control, infotainment, safety, and powertrain, making them a core volume and value engine for MCU suppliers.

Electric Vehicles represent the fastest-growing vehicle segment, with MCU demand estimated to grow at a close to 9% CAGR, supported by robust EV sales trajectories in China, Europe, and North America. Each EV typically requires additional MCUs for battery management, inverter control, charging systems, and thermal management, significantly increasing content per vehicle versus internal-combustion platforms.

Regional Market Insights

North America Automotive MCU Market Trends

North America represents a sizable share of the Automotive MCU market, anchored by the United States’ leadership in software-defined vehicle concepts, advanced infotainment, and high-electronic-content pickup/SUV platforms. The region benefits from strong semiconductor design capabilities and close collaboration between Tier-1s and global MCU suppliers on next-generation ADAS and connectivity solutions. Market value is projected to expand at a CAGR of around 3.7% from 2026 to 2033, supported by EV rollout, safety mandates, and premium trim mix in light trucks.

Growth is reinforced by U.S. industrial and CHIPS-related policies that incentivize domestic semiconductor investment, enhancing supply chain resilience for automotive customers. Competitive dynamics feature leading global MCU vendors partnering with North American OEMs on long-term platform roadmaps, with opportunities in centralized E/E architectures and over-the-air upgradable control units.

Europe Automotive MCU Market Trends

Europe commands roughly 23.1% of the global Automotive MCU market, driven by strong production in Germany, France, Spain, and the U.K., and by a concentration of premium brands with high electronics content. EU-wide safety and emissions regulations, including Euro 7 and the General Safety Regulation, accelerate the adoption of advanced powertrain control, ADAS, and cybersecurity-compliant MCUs. European OEMs’ shift toward centralized architectures and software platforms further increases the strategic importance of high-end MCUs in regional supply chains.

Harmonized regulatory frameworks across EU member states support consistent electronics specification, facilitating platform reuse and long production cycles for MCU programs. Investment opportunities are strongest in EV-related control systems, zonal controllers, and safety-critical MCUs certified to stringent functional safety standards.

Asia Pacific Automotive MCU Market Trends

Asia Pacific is the leading and fastest-growing region, holding around 52% of global Automotive MCU demand, with China, Japan, South Korea, and India serving as both major vehicle production hubs and semiconductor consumption centers. Automotive microcontroller use benefits from large-scale manufacturing ecosystems, rapid EV proliferation, and increasing fitment of ADAS and connected infotainment even in mid-tier models. Regional policies promoting new energy vehicles and domestic semiconductor capacity further support medium-term growth.

The region’s manufacturing advantages include dense supplier clusters, competitive labor costs, and government support for advanced electronics and microcontroller design centers, especially in China and India. Investment opportunities are concentrated in localized MCU production, partnerships with regional OEMs and Tier-1s, and platform solutions optimized for cost-sensitive but feature-rich vehicles.

Competitive Landscape

Leading Automotive MCU suppliers pursue innovation-led strategies centered on higher-performance, functionally safe, and cybersecurity-hardened MCUs, while simultaneously optimizing cost structures for high-volume platforms. Key differentiators include long-term supply reliability, deep OEM and Tier-1 partnerships, scalable software ecosystems, and support for domain/zonal architectures and software-defined vehicles. Emerging business models emphasize platform-based families, over-the-air updatable firmware, and closer integration of MCUs with power, networking, and sensor front-ends.

Strategic Developments:

- In January 2024, NXP Semiconductors introduced a new family of automotive-grade MCUs with integrated AI acceleration to enhance real-time decision-making for ADAS and body applications, supporting higher system integration and safety performance.

- In March 2024, Renesas Electronics launched a high-performance automotive MCU platform targeting autonomous driving and advanced safety controllers, enabling higher computing density with functional safety and cybersecurity features for future vehicle architectures.

- In June 2024, STMicroelectronics entered a collaboration with a leading automotive Tier-1 supplier to co-develop next-generation powertrain control MCUs, focusing on higher efficiency for hybrid and battery electric vehicles and tighter integration with inverter and battery systems.

- In September 2024, Infineon Technologies announced the acquisition of a smaller MCU manufacturer to broaden its automotive-grade microcontroller portfolio, strengthen its position in high-end safety applications, and deepen relationships with global OEMs.

- In 2025, multiple top automotive MCU suppliers expanded 28 nm and below production capacity and design support centers in Asia Pacific, aiming to secure supply, shorten design-in cycles, and align portfolios with regional EV and ADAS growth.

Companies Covered in Automotive MCU Market

- NXP Semiconductors

- Renesas Electronics Corporation

- Infineon Technologies AG

- Texas Instruments Incorporated

- Microchip Technology Inc.

- STMicroelectronics NV

- ON Semiconductor

- Toshiba Corporation

- Analog Devices, Inc.

- Cypress Semiconductor (Infineon)

- Silicon Laboratories

- GigaDevice Semiconductor

- AutoChips / SemiDrive

- BYD Semiconductor

- Rohm Semiconductor

Frequently Asked Questions

The Automotive MCU Market is expected to reach about US$10.6 billion in 2026 and approximately US$15.1 billion by 2033, reflecting steady value growth as electronic content per vehicle rises.

The market is driven by increasing ADAS and safety mandates, accelerating vehicle electrification, and rising electronics content in body, comfort, lighting, and infotainment systems across global passenger and commercial fleets.

Between 2026 and 2033, the Automotive MCU Market is projected to grow at a CAGR of around 5.2%, underpinned by higher MCU content in EVs and advanced driver assistance applications.

Key opportunities lie in 64-bit and high-end 32-bit MCUs for domain/zonal architectures, ADAS and autonomous driving controllers, and Asia Pacific EV and high-content vehicle production growth.

Major players include Infineon Technologies, NXP Semiconductors, STMicroelectronics, Texas Instruments, Renesas Electronics, Microchip Technology, ON Semiconductor, Analog Devices, Toshiba, Silicon Labs, and other players, which collectively shape technology and supply dynamics.