- Automotive Components & Materials

- Automotive Mufflers Market

Automotive Mufflers Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Mufflers Market by Component (Reactive Muffler, Absorber Muffler, Hybrid Muffler), Material (Stainless Steel, Carbon Fiber, Aluminum, Titanium), Vehicle Type (Passenger Cars, Two-Wheeler, Light Commercial Vehicles, Heavy Commercial Vehicles), and Regional Analysis for 2026 - 2033

Automotive Mufflers Market Size and Trend Analysis

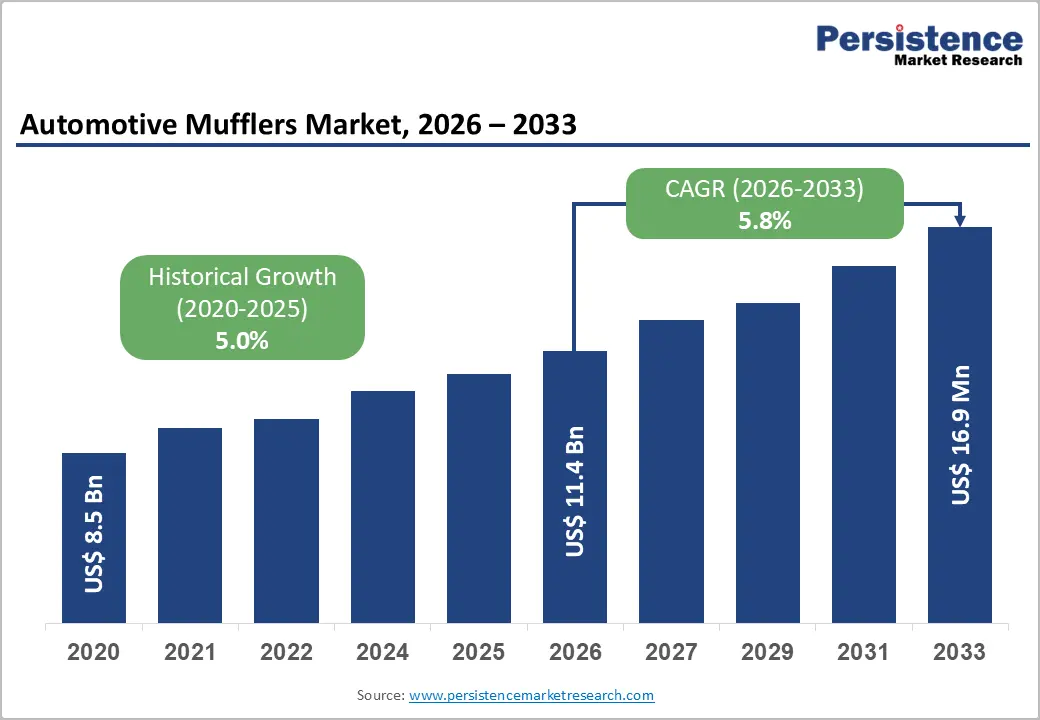

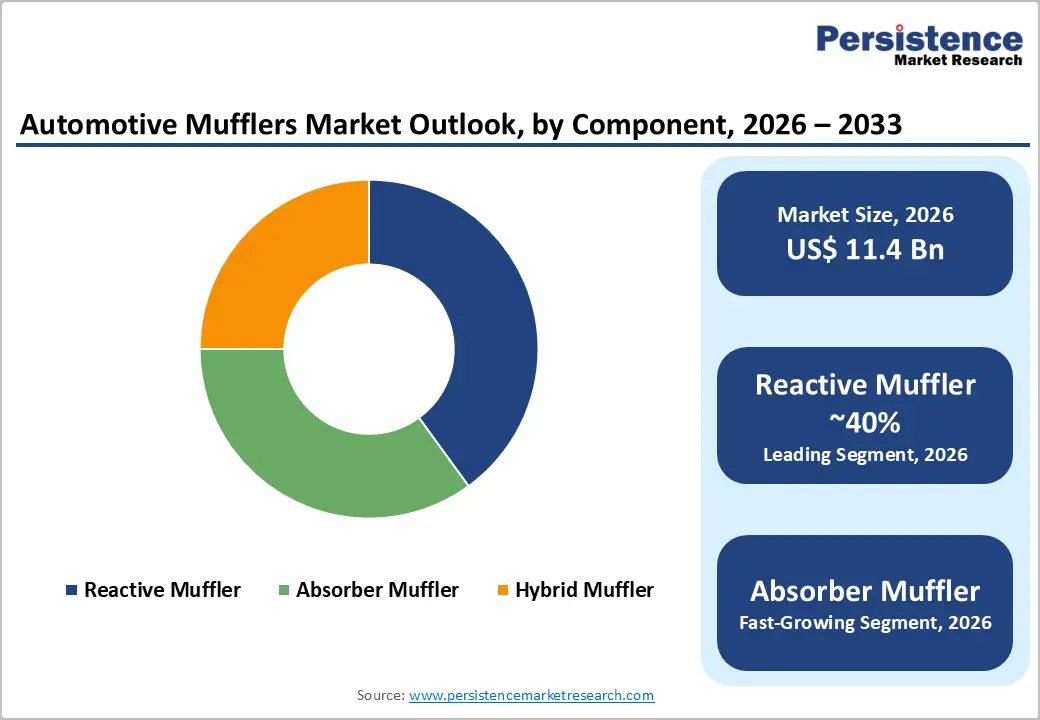

The global automotive mufflers market size is valued at US$ 11.4 Bn in 2026 and is projected to reach US$ 16.9 Bn by 2033, growing at a CAGR of 5.8% between 2026 and 2033.

Robust market expansion is underpinned by three converging forces: tightening global emission and noise legislation, sustained growth in internal combustion engine (ICE) vehicle production, especially across the Asia Pacific and accelerating demand for lightweight, high-performance exhaust silencing solutions.

Regulatory milestones such as the European Union's Euro 7 standard (effective November 2026) and the U.S. Environmental Protection Agency (EPA) multi-pollutant light-duty standards (effective model year 2027) compel automakers and Tier 1 suppliers to invest in next-generation muffler architectures, boosting bill-of-materials value and sustaining the market's upward trajectory.

Key Market Highlights

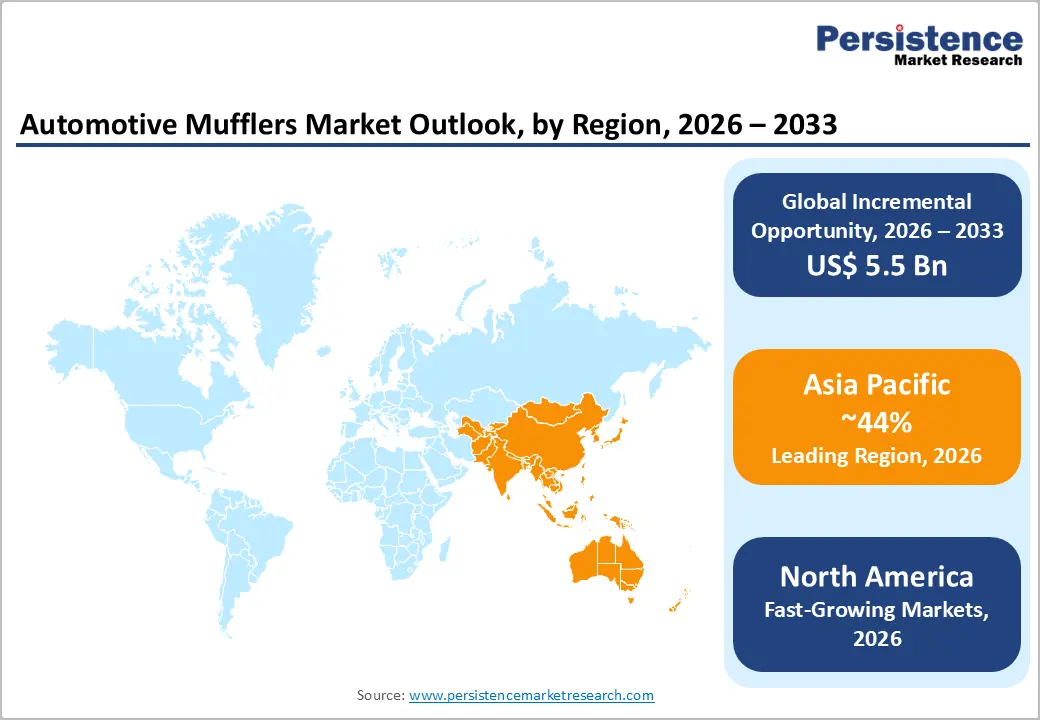

- Leading Region: Asia Pacific dominates the global automotive mufflers market, accounting for over 44% of revenue, driven by China and India's expansive vehicle production, tightening emission norms, and well-established Tier 1 supplier ecosystems offering manufacturing cost advantages.

- Fastest-Growing Region: Asia Pacific is also the fastest-growing region, with China registering a CAGR of approximately 8.1%, driven by the planned transition to the China VII emission framework and strong growth in two-wheeler and passenger car production across ASEAN economies.

- Dominant Segment: Passenger Cars dominate the Vehicle Type segment with approximately 59% market share, supported by high global production volumes and the expanding hybrid vehicle fleet requiring more sophisticated and thermally resilient muffler architectures.

- Fastest Growing Segment: The Hybrid Muffler segment is the fastest growing component category, benefiting from the global proliferation of hybrid and PHEV vehicles that demand specialized exhaust silencing solutions capable of managing variable engine load profiles and extended durability requirements.

- Key Market Opportunity: The key market opportunity lies in developing lightweight, active noise-control, and hybrid-compatible muffler technologies, as Euro 7 and equivalent global emission regulations mandate higher-performance, longer-lifecycle exhaust components, significantly expanding the bill-of-materials value per vehicle.

| Key Insights | Details |

|---|---|

| Automotive Mufflers Market Size (2026E) | US$ 11.4 Billion |

| Market Value Forecast (2033F) | US$ 16.9 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.8% |

| Historical Market Growth (2020 - 2025) | 5.0% |

DRO Analysis

Market Growth Drivers

Stringent Global Emission and Noise Regulations Driving Advanced Muffler Adoption

The regulatory landscape has emerged as the single most powerful demand catalyst for automotive mufflers. The European Union's Euro 7 regulation (EU Regulation 2024/1257) mandates that from November 2026, all newly type-approved light-duty cars and vans meet harmonized NOx limits of 60 mg/km and extends vehicle emissions compliance requirements to a lifecycle of up to 10 years or 200,000 km, twice the duration required under Euro 6.

Simultaneously, the U.S. EPA has finalized multi-pollutant standards for model year 2027 vehicles, targeting a 50% reduction in NOx and a 40% reduction in particulate matter from light-duty vehicles. These mandates require OEMs to integrate higher-efficiency reactive, absorber, and hybrid muffler configurations, significantly increasing the per-vehicle content value and driving volume demand among Tier 1 exhaust component suppliers.

Surging Global Vehicle Production and Expanding Aftermarket Replacement Demand

The structural growth of the global automotive manufacturing base continues to underpin demand for mufflers. According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production grew by 5% in the first quarter of 2024 compared with the same period in 2023, driven by a recovery across key producing nations. Simultaneously, the aging of the global fleet, with average fleet age reaching 12.2 years in the United States and 11.8 years in Europe during 2024, generates durable aftermarket demand for muffler replacements.

As emissions inspection regimes tighten and older ICE vehicles require frequent exhaust component upgrades to remain compliant, suppliers with broad distribution networks and diversified product portfolios are well positioned to capture recurring replacement revenue throughout the forecast period.

Market Restraints

Accelerating Electrification of the Automotive Fleet

The rapid transition toward battery electric vehicles (BEVs) poses a structural headwind to long-term muffler demand. Since BEVs generate no combustion exhaust, they eliminate the need for traditional exhaust silencing components. According to the International Energy Agency (IEA), global electric car sales surpassed 14 million units in 2023a 35% year-on-year increase.

Furthermore, the EU's ban on the sale of new ICE passenger cars and vans from 2035 signals a definitive long-term contraction in the addressable ICE vehicle base, progressively constraining OEM muffler procurement volumes in mature markets over the latter part of the forecast horizon.

Volatility in Raw Material Costs Compressing Manufacturer Margins

Stainless steel, the dominant material used in automotive muffler manufacturing, is subject to significant price volatility tied to nickel market dynamics. Nickel-alloy surcharges fluctuated between US$ 15,000 and US$ 22,000 per tonne during 2024, directly elevating the cost of muffler production.

Smaller manufacturers with limited hedging capacity are particularly exposed, as input cost swings erode profitability and restrict the ability to invest in product innovation. The qualification timeline for alternative low-nickel alloys, while gaining research momentum, remains lengthy, limiting near-term relief for the industry.

Market Opportunities

Hybrid Vehicle Proliferation Creating Demand for Specialized Thermal Management Mufflers

The global shift toward hybrid and plug-in hybrid electric vehicles (PHEVs) presents a significant near-term growth opportunity for muffler manufacturers. Hybrid powertrains operate under intermittent engine loads and variable exhaust temperatures, demanding specialized muffler architectures capable of managing complex thermal and acoustic profiles. Automotive suppliers are actively responding to this need.

In January 2024, Tenneco Inc. launched an integrated thermal management system specifically designed to maintain optimal exhaust temperatures in hybrid and conventional vehicles, improving catalyst light-off performance under low-load conditions. Globally, hybrid vehicle sales continue to climb, with Toyota prioritizing hybrid models as a bridge technology. This sustained ICE-hybrid phase supports per-unit muffler content growth and positions companies investing in high-performance hybrid-compatible exhaust silencing solutions at a competitive advantage through the forecast period.

Lightweight Material Innovation and Active Noise Control Technologies Opening New Revenue Pockets

Advances in lightweight materials and active noise cancellation (ANC) exhaust technology offer meaningful avenues for market participants to expand revenue and differentiate product portfolios. In February 2024, FORVIA (Faurecia) unveiled a lightweight exhaust manifold made from a high-strength aluminum alloy to reduce system mass while preserving durability, directly addressing automakers' fuel economy and CO2 targets.

Meanwhile, active noise control mufflers that electronically attenuate specific frequency bands are gaining traction with OEMs as consumer preference for cabin quietness intensifies. Titanium and carbon fiber muffler variants are also attracting premium segment interest due to their exceptional weight-to-strength ratios. Suppliers that combine material science leadership with ANC capability stand to command higher value-added content per vehicle and secure long-term OEM platform wins.

Category-wise Analysis

Component Insights

Among the three primary component types, reactive mufflers lead, accounting for approximately 36% of global automotive muffler market revenue. Reactive mufflers leverage internal chambers and baffles to reflect and cancel sound waves across a broad frequency spectrum, delivering superior noise attenuation at varying engine output levels without introducing significant exhaust back-pressure penalties.

This acoustic and thermodynamic versatility makes them the preferred choice among OEMs for passenger-car and light-commercial-vehicle applications. Their compatibility with both conventional ICE and hybrid powertrain configurations further supports adoption. Continuous improvements in chamber geometry design, acoustic modeling, and corrosion-resistant material integration have enhanced their efficiency and durability, reinforcing their dominance in original equipment fitment and the growing aftermarket replacement segment globally.

Material Insights

Stainless steel is the dominant material segment in the automotive mufflers market, accounting for approximately 39% of revenue. Its pre-eminence is attributable to an outstanding combination of properties critical to long-term muffler performance: superior corrosion resistance, high-temperature tolerance, mechanical strength, and formability for complex exhaust geometries.

Grade 409 and 439 ferritic stainless steels are widely specified for cold-end applications, while austenitic grades such as 304 and 316L are used for higher-heat hot-end sections. Stainless steel's compatibility with advanced hybrid muffler designs and its alignment with stringent environmental regulations requiring durable emission-control components over extended lifecycles of up to 200,000 km under Euro 7 mandates further cements its leadership in OEM and aftermarket channels.

Vehicle Type Insights

Passenger cars constitute the leading vehicle type segment, accounting for approximately 59% of total automotive mufflers market revenue. The sheer volume of passenger car production globally, driven by rising urbanization, expanding middle-class populations in Asia Pacific, and continued rollouts of ICE and hybrid models, anchors this segment's dominance.

High-volume automotive platforms manufactured by Toyota, Volkswagen Group, Hyundai Motor Group, General Motors, and Ford collectively drive robust OEM procurement of passenger car muffler assemblies. Concurrently, stricter urban noise pollution ordinances and emissions inspection requirements across Europe, North America, and China are accelerating aftermarket replacement demand in this vehicle category. Hybrid passenger car volume growth further enhances per-unit muffler content value, supporting segment revenue outperformance.

Regional Analysis

Asia Pacific Automotive Mufflers Market Insights

Asia Pacific is the largest regional segment, commanding over 44% of global automotive exhaust systems market share, with China and India driving outsized growth. China leads the region with a CAGR of approximately 8.1%, propelled by its planned transition from China VI to China VII emission norms and the massive scale of domestic vehicle production. In India, the prospective introduction of BS-VII norms is prompting suppliers to develop next-generation exhaust silencing systems underscored by Tenneco Inc.'s showcase at SIAT 2026 of a diesel engine emission control system with BS-VII readiness.

The broader ASEAN sub-region is also gaining strategic importance. In October 2023, Purem AAPICO, a joint venture between AAPICO Hitech and Eberspächer, opened a new exhaust system production facility in Rayong, Thailand. Asia-based suppliers benefit from local-content mandates and economies of scale that compress unit costs and enhance export competitiveness, reinforcing the region's dominant position in global muffler manufacturing and supply chains.

North America Automotive Mufflers Market Insights

North America represents one of the most mature yet persistently significant markets for automotive mufflers, anchored by robust vehicle parc volumes and a stringent regulatory environment. The U.S. Environmental Protection Agency (EPA)'s finalized multi-pollutant light-duty standards, targeting a 50% NOx reduction and a 40% particulate matter reduction, effective from model year 2027, necessitate technologically advanced muffler assemblies across both OEM and aftermarket channels. The aging U.S. fleet, averaging 12.2 years, fuels consistent aftermarket replacement cycles for mufflers, catalytic converters, and exhaust pipes.

The regional innovation ecosystem is characterized by active R&D investment from major players. In October 2024, Flow master launched the Signature Series premium truck exhaust range for major light-pickup models, tapping growing consumer enthusiasm for high-performance aftermarket muffler solutions.

Europe Automotive Mufflers Market Insights

Europe's automotive mufflers market is being significantly shaped by the bloc's comprehensive emission and decarbonization policy framework. The landmark EU Regulation 2024/1257 (Euro 7))which enters force for new light-duty vehicle type approvals from November 2026 and mandates 10-year / 200,000 km emissions durability compliance, requires fundamentally re-engineered muffler and exhaust aftertreatment architectures. Germany remains the dominant European market, hosting global muffler manufacturers including Friedrich Boysen GmbH & Co. KG and Eberspächer, and accounting for the largest share of European OEM vehicle output.

France and the U.K. further reinforce regional demand through vehicle fleet renewal incentives and progressive urban low-emission zones. In November 2023, Eberspächer commenced production at a dedicated 7,000-square-meter facility manufacturing exhaust gas after-treatment systems. The European Automobile Manufacturers' Association (ACEA) projects that fleet renewal, driven by Euro 7 compliance and accelerating electrification, will reduce the number of older, high-emitting vehicles, sustaining replacement-component demand over the medium term.

Competitive Landscape

The global automotive mufflers market exhibits a moderately consolidated structure, with a handful of large multinational Tier 1 suppliers primarily Tenneco Inc., FORVIA (Faurecia), Eberspächer, and Friedrich Boysen GmbH & Co. KG commanding significant OEM platform relationships. Leading companies pursue growth through technology differentiation in lightweight materials, acoustic engineering, and thermal management integration, while simultaneously expanding geographic footprints via joint ventures particularly in Asia Pacific.

Emerging business model trends include aftermarket digital platforms and direct-to-consumer performance exhaust channels. R&D priorities are centred on hybrid-compatible muffler architectures, active noise control systems, and advanced material qualification for ultra-long durability compliance under Euro 7 and equivalent global standards.

Key Developments:

- In January 2025, Tata Motors and Hindustan Petroleum Corporation introduced co-branded “Genuine DEF” diesel exhaust fluid across 23,000 HPCL stations and 2,000 Tata Motors outlets.

- In October 2024, Flowmaster launched the Signature Series premium truck exhaust line for major light-pickup models.

Companies Covered in Automotive Mufflers Market

- Tenneco Inc.

- Onyxautosilencer

- Friedrich Boysen GmbH & Co. KG

- THUNDER

- Bosal International N.V.

- Eminox

- The Dinex Group

- Faurecia (FORVIA)

- BENTELER International

- Yutaka Giken Co., Ltd.

- Eberspächer

- Munjal Auto Industries Limited

Frequently Asked Questions

The global Automotive Mufflers market is valued at US$ 11.4 Bn in 2026 and is projected to reach US$ 16.9 Bn by 2033, growing at a CAGR of 5.8% during the forecast period.

Market growth is primarily driven by tightening global emission and noise legislation including the EU's Euro 7 regulation (effective November 2026) and U.S. EPA multi-pollutant standards (model year 2027)alongside continued global vehicle production growth, ageing fleet replacement cycles, and the proliferation of hybrid vehicles requiring specialised exhaust silencing architectures.

Reactive mufflers are the leading component segment, accounting for approximately 36% of market revenue. Their ability to attenuate a broad sound frequency spectrum, compatibility with both ICE and hybrid powertrains, and consistent compliance with global noise and emission regulations drive their dominant OEM and aftermarket fitment rates.

Asia Pacific is the leading region, accounting for over 44% of global automotive exhaust systems market share. The region benefits from the world's largest vehicle production bases in China, India, Japan, and ASEAN, strengthening local-content mandates, and progressively tightening emission norms that sustain strong per-unit muffler content value.

Key players operating in the global Automotive Mufflers market include Tenneco Inc., FORVIA (Faurecia), Eberspächer (Purem by Eberspächer), Friedrich Boysen GmbH & Co. KG, Bosal International N.V., BENTELER International, Yutaka Giken Co., Ltd., The Dinex Group, Eminox, Munjal Auto Industries Limited, Onyxautosilencer, and THUNDER, among others.