- Medical Devices

- Automated Optical Imaging Market

Automated Optical Imaging Market Size, Share, and Growth Forecast, 2026 – 2033

Automated Optical Imaging Market by Technology Type (2D Imaging, 3D Imaging), Application (Medical Diagnostics, Industrial Inspection, Research and Development), End-user (Healthcare, Electronics, Automotive, Aerospace), and Regional Analysis for 2026 – 2033

Automated Optical Imaging Market Size and Trends Analysis

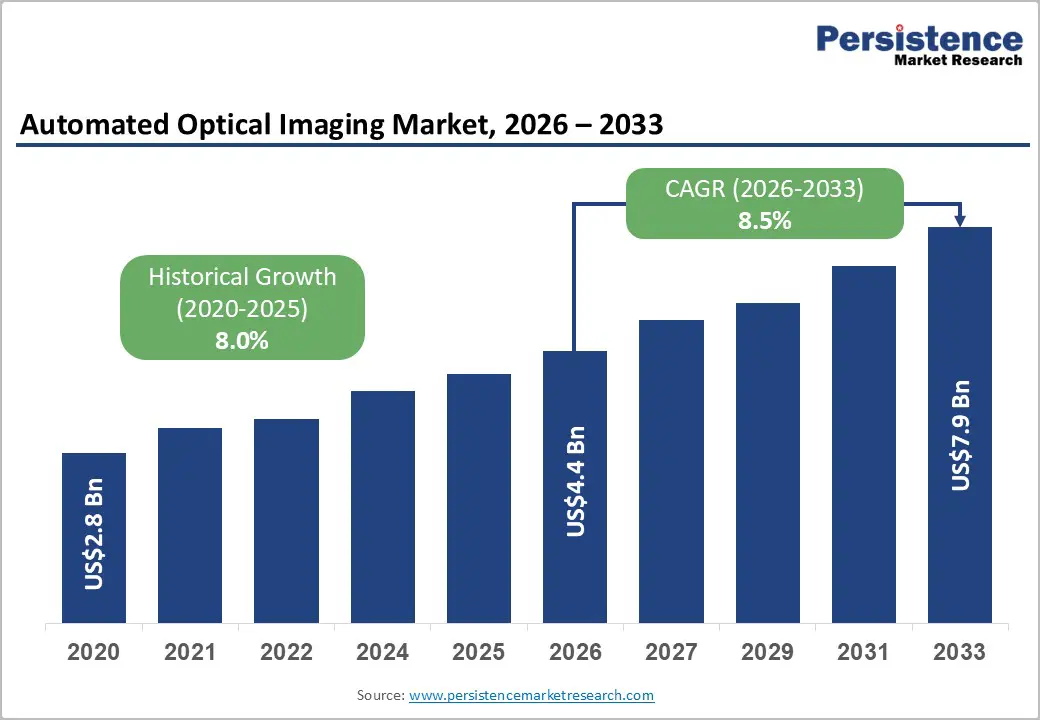

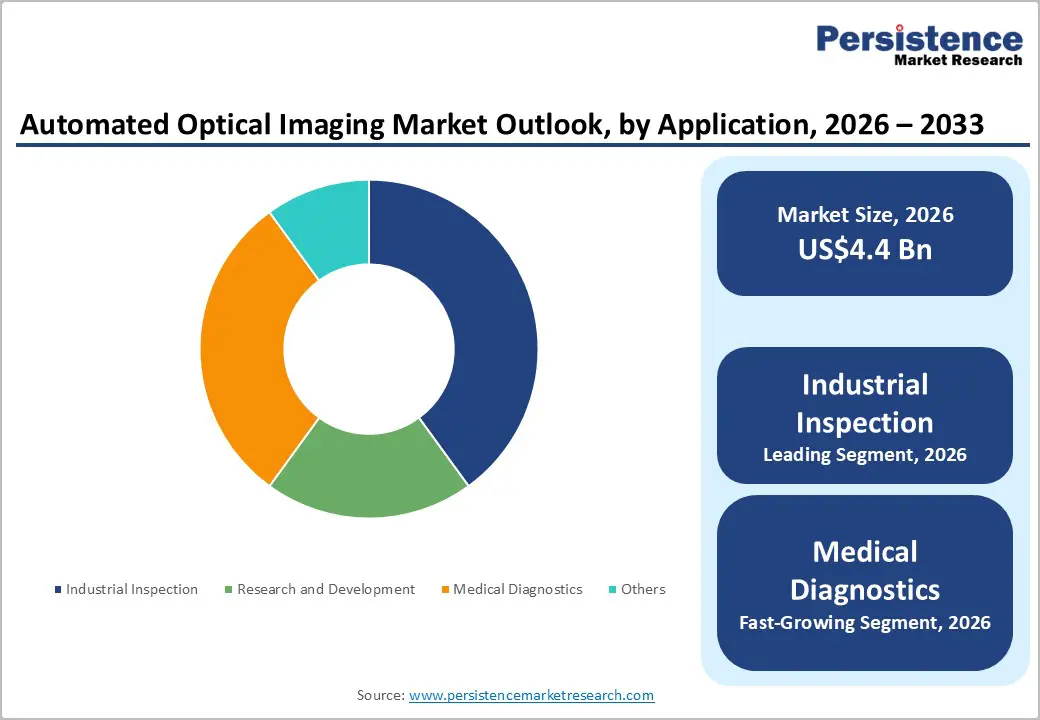

The global automated optical imaging market size is likely to be valued at US$4.4 billion in 2026 and is expected to reach US$7.9 billion by 2033, growing at a CAGR of 8.5% during the forecast period from 2026 to 2033, driven by the increasing adoption of high-precision imaging systems across medical diagnostics, semiconductor and electronics manufacturing, and advanced research and development applications.

Technological advancements, including high-resolution 2D and 3D imaging, hyperspectral imaging, and AI-driven image analysis, are enabling non-contact and non-invasive visualization, which improves accuracy and efficiency across critical processes. The rising demand for automation in industries such as healthcare, electronics, automotive, and aerospace is propelling market expansion, as organizations increasingly seek real-time, reliable imaging solutions for monitoring, inspection, and research purposes. The trend toward miniaturized devices, complex components, and intricate microstructures is reinforcing the need for sophisticated imaging systems capable of capturing detailed structural and functional information.

Key Industry Highlights:

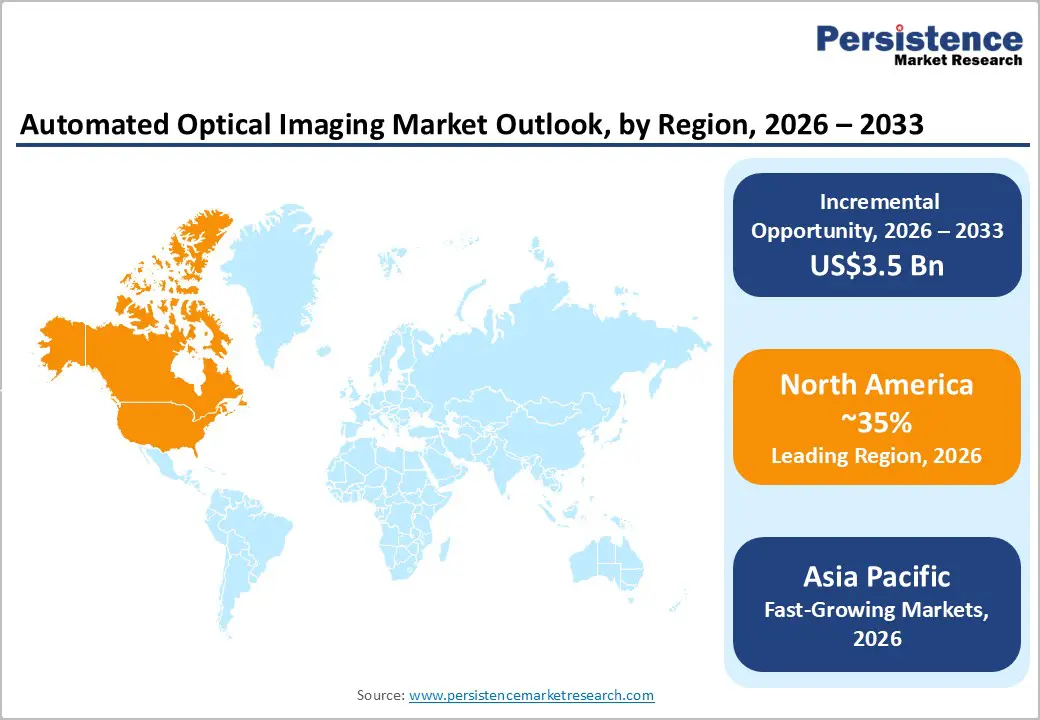

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by the U.S. with strong R&D, healthcare, and automotive adoption, and supportive regulations.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by strong electronics manufacturing, 5G adoption, and government support in countries such as China and India.

- Leading Technology Type: 2D Imaging is projected to represent the leading technology type in 2026, accounting for 60% of the revenue share, driven by its cost-effectiveness, established use in standard processes, and widespread deployment in high-volume production lines.

- Leading Application: Industrial inspection is anticipated to be the leading application, accounting for over 45% of the revenue share in 2026, supported by high-volume electronics manufacturing, automation mandates, and extensive use in PCB and semiconductor quality control.

| Key Insights | Details |

|---|---|

|

Automated Optical Imaging Market Size (2026E) |

US$4.4 Bn |

|

Market Value Forecast (2033F) |

US$7.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Technological Advancements in Imaging Systems

Recent advancements in optical imaging technology have significantly enhanced the precision, resolution, and speed of automated imaging systems. High-resolution 2D and 3D imaging, hyperspectral techniques, and advanced sensor designs allow for detailed visualization of microstructures, electronic components, and biological tissues. Integration of AI and machine learning algorithms enables automated defect detection, pattern recognition, and predictive analysis, reducing errors and increasing throughput. These innovations support diverse applications across medical diagnostics, semiconductor manufacturing, and research laboratories.

Automated optical imaging now incorporates multi-dimensional imaging and adaptive optics, allowing real-time data acquisition and volumetric analysis. Emerging technologies such as digital holography and fluorescence imaging enhance contrast and depth perception, critical for both industrial and medical applications. Coupled with faster image processing platforms, these systems reduce inspection times while improving accuracy. The evolution toward compact and portable imaging devices also expands adoption in point-of-care diagnostics, on-site research, and high-volume production environments.

Increasing Focus on Non-Invasive and High-Precision Applications

There is a growing demand for non-invasive imaging techniques in medical diagnostics, particularly in ophthalmology, oncology, and cardiology, where patient comfort and minimal intervention are priorities. Automated optical imaging systems provide precise, high-resolution data without physically altering the sample or patient, making them ideal for longitudinal studies and continuous monitoring. High-precision imaging is crucial in electronics and semiconductor industries, where even microscopic defects can impact performance.

The focus on high-precision applications extends to research and development laboratories, where accurate imaging of biological samples, microelectronics, and nanomaterials is critical. Integration with AI and machine learning enables precise measurement, anomaly detection, and predictive modeling, reducing manual intervention and improving reproducibility. In industrial and healthcare contexts, these capabilities support regulatory compliance, efficiency, and innovation, enabling organizations to optimize workflows while maintaining superior quality.

Barrier Analysis - Integration Complexity and Skill Gaps

Automated optical imaging systems often require sophisticated integration with existing manufacturing lines, laboratory setups, and data management platforms. The complexity of configuring imaging hardware, software analytics, and AI algorithms necessitates highly skilled personnel for installation, calibration, and maintenance. Many organizations face skill gaps, particularly in advanced imaging techniques and machine learning-based image analysis, limiting seamless adoption. Integrating multi-dimensional imaging systems with industrial automation or medical devices also poses technical challenges, including software compatibility, sensor alignment, and workflow customization, which can delay deployment and increase operational costs.

Training and workforce development remain critical, as end-users must understand both the operational and analytical aspects of imaging systems. Inadequate expertise can result in suboptimal performance, misinterpretation of data, and reduced return on investment. Ensuring interoperability between new imaging systems and legacy equipment is a persistent challenge for manufacturing and research facilities. Addressing these integration and skill-related hurdles requires targeted training programs, robust technical support, and simplified system interfaces.

Supply Chain Constraints and Component Availability

The production of automated optical imaging systems depends on critical components such as high-resolution sensors, specialized lenses, precision optics, illumination modules, and processing units. Supply chain disruptions, shortages of semiconductors, or delays in specialized optical materials can significantly impact manufacturing schedules and system availability. Limited access to these components can increase costs, lengthen lead times, and restrict market expansion. The reliance on a few key suppliers for advanced sensors and optics exposes the market to geopolitical and logistical risks, particularly in regions with heavy electronics manufacturing or medical imaging demand.

Rapid technological evolution necessitates constant sourcing of next-generation components to maintain competitive performance. Any bottleneck in the supply of high-quality lenses, imaging sensors, or AI-compatible processors can delay product launches and affect customer adoption. Companies may face challenges in scaling production for large-volume deployments in electronics or healthcare, limiting responsiveness to market demand. Mitigating supply chain constraints through diversified sourcing, strategic partnerships, and inventory management is crucial for sustaining growth and ensuring that automated optical imaging solutions remain available for critical industrial and medical applications.

Opportunity Analysis - 3D Imaging Convergence with IoT

The convergence of 3D automated optical imaging with IoT-enabled platforms offers significant opportunities for real-time monitoring, remote analysis, and predictive maintenance across industries. High-resolution 3D imaging integrated with connected devices allows for continuous data acquisition, automated anomaly detection, and intelligent workflow optimization. In manufacturing, IoT-enabled imaging facilitates real-time quality control, predictive analytics, and seamless integration with smart factory systems.

Beyond industrial applications, 3D imaging with IoT integration supports healthcare, research, and logistics by enabling remote diagnostics, cloud-based image processing, and collaborative analysis across geographies. IoT connectivity allows stakeholders to access imaging data in real-time, improving decision-making speed and accuracy. The combination of volumetric imaging, AI analytics, and networked communication creates opportunities for predictive modeling, personalized diagnostics, and automated R&D workflows.

Unmet Needs in Medical and R&D Applications

Medical and research sectors continue to face unmet imaging needs for high-resolution, non-invasive, and multi-modal analysis. Diseases such as cancer, retinal disorders, and cardiovascular conditions require precise visualization at micro and macro scales, while drug discovery and material sciences demand reproducible, high-fidelity imaging tools. Automated optical imaging systems capable of addressing these unmet needs can provide significant value by enabling early detection, improved experimental accuracy, and enhanced data-driven insights.

The rising emphasis on personalized medicine, preclinical studies, and advanced material characterization amplifies the demand for sophisticated imaging solutions. Laboratories and hospitals seek imaging systems that reduce human error, enable longitudinal studies, and integrate with AI-driven analytics for predictive insights. By addressing these unmet needs, companies can expand market penetration, develop specialized solutions, and differentiate themselves from traditional imaging providers. The combination of innovation, precision, and automation positions automated optical imaging as a strategic enabler for healthcare and R&D sectors, unlocking substantial growth opportunities.

Category-wise Analysis

Technology Type Insights

2D imaging is expected to lead the automated optical imaging market, accounting for approximately 60% of revenue in 2026, driven by cost-effectiveness, established applications in electronics manufacturing, and widespread deployment across high-volume production lines. 2D systems excel in capturing surface-level details and identifying structural irregularities with simpler setups, making them ideal for standard PCB and semiconductor monitoring. For example, in electronics manufacturing, companies such as Canon Inc. utilize 2D imaging cameras to inspect high-density printed circuit boards for surface defects, soldering issues, and assembly irregularities.

3D imaging is likely to represent the fastest-growing segment, supported by its advanced capabilities in volumetric analysis, height measurement, and reduced false calls for complex assemblies. The technology supports high-precision evaluation of solder joints, microelectronic components, and intricate structures that 2D imaging cannot fully capture. For example, Zeiss Group implements 3D imaging systems in semiconductor wafer inspection to accurately detect micro-defects and ensure uniformity across high-density chips. Rising miniaturization trends and the need for precise component verification are encouraging manufacturers to transition toward 3D systems.

Application Insights

Industrial inspection is projected to lead the market, capturing around 45% of the revenue share in 2026, supported by the dominance of electronics manufacturing, particularly in PCB and semiconductor quality control. Automated optical imaging systems are widely used for real-time defect detection, surface and component verification, and process monitoring in high-volume lines. For example, Keyence Corporation provides imaging solutions for SMT (surface mount technology) production lines, enabling automated detection of misaligned components and soldering defects. The combination of high throughput, integration with manufacturing execution systems, and compatibility with existing production lines reinforces the segment’s leadership.

Medical diagnostics is likely to be the fastest-growing application, driven by non-invasive imaging advantages, increasing chronic disease prevalence, and AI integration for improved accuracy. Automated optical imaging systems enable precise visualization of anatomical structures and pathological conditions in ophthalmology, oncology, and cardiology without invasive procedures. For example, Cirrus HD-OCT is used in ophthalmology to capture detailed retinal images, improving early detection of eye diseases. The integration of AI algorithms assists in anomaly detection and predictive analysis, improving diagnostic efficiency and reducing manual interpretation errors.

Regional Insights

North America Automated Optical Imaging Market Trends

North America is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by strong innovation ecosystems, advanced manufacturing adoption, and increasing demand across the healthcare and electronics sectors. In the U.S. and Canada, significant investments in research and development, particularly in semiconductor fabrication and medical diagnostics, increase demand for automated imaging technologies that deliver high?resolution visualization and precision analytics. The regulatory environment, anchored by stringent quality and safety standards, encourages the adoption of automated optical imaging solutions that ensure compliance and enhance operational reliability.

In healthcare and medical diagnostics, North America’s demand for automated optical imaging is rising due to aging populations and increased screenings for chronic diseases. For example, Carl Zeiss Meditec Inc. has expanded its U.S. portfolio of optical coherence tomography (OCT) and confocal imaging systems used in ophthalmology and neurology, enabling clinicians to visualize microstructures with exceptional clarity and support early disease intervention. Across electronics and semiconductor manufacturing, companies are adopting high?throughput 3D optical imaging platforms to inspect increasingly miniaturized components, where traditional methods fall short.

Europe Automated Optical Imaging Market Trends

Europe is likely to be a significant market for automated optical imaging, due to the rapid adoption of high?precision imaging technologies across medical diagnostics, industrial manufacturing, and research sectors. Countries such as Germany, the U.K., France, and the Netherlands are investing heavily in automation and digitalization, particularly within automotive and electronics industries where quality control and micro?level visualization are critical. Regulatory emphasis on safety standards and conformity assessment, such as CE marking and MDR for medical devices, reinforces demand for reliable imaging solutions that help companies meet stringent compliance requirements.

In the healthcare domain, Europe’s aging population and rising prevalence of chronic diseases underpin the expanding deployment of automated optical imaging systems in hospitals and diagnostic centers. For example, Leica Microsystems GmbH has expanded its presence in the European market with high?resolution confocal and multiphoton imaging platforms used in both clinical pathology and biomedical research. These systems provide detailed visualization of tissue samples and cellular structures, improving diagnostic accuracy and research outcomes.

Asia Pacific Automated Optical Imaging Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by strong electronics manufacturing, increasing automation adoption, and rising demand for precision imaging across medical, automotive, and semiconductor sectors. Key manufacturing hubs such as China and Taiwan are investing in advanced automated imaging systems to support high?volume production environments and complex component inspection. Integration of artificial intelligence and machine vision is enabling real?time anomaly detection and predictive analytics, enhancing production efficiency.

In the healthcare and advanced technology segment, increasing clinical needs for high?resolution, non?invasive imaging are driving investment in sophisticated optical imaging platforms. For example, Canon India Pvt. Ltd. has deployed advanced optical imaging solutions in medical and industrial settings across Asia Pacific, offering high?precision imaging for applications ranging from diagnostic support in ophthalmology to detailed visualization in semiconductor wafer inspection. These deployments underscore increasing confidence in automated optical imaging systems to improve diagnostic accuracy and support stringent quality control processes.

Competitive Landscape

The global automated optical imaging market exhibits a moderately fragmented structure, driven by the coexistence of large multinational imaging manufacturers, specialized machine vision firms, and emerging AI?enabled solution providers. Market growth is supported by increasing demand across medical diagnostics, electronics manufacturing, and advanced research applications, prompting firms to innovate in high?resolution hardware, 3D imaging capabilities, and smart analytics software. Regional players in Asia Pacific and Europe are gaining ground by offering cost?effective systems tailored to local manufacturing needs, while established brands maintain leadership through deep technical expertise and comprehensive service networks.

With key leaders including Zeiss Group, Olympus Corporation, Nikon Corporation, Leica Microsystems, Keyence Corporation, Basler AG, Cognex Corporation, Omron Corporation, Teledyne Technologies Incorporated, Canon Inc., and Sony Corporation, the market reflects both breadth and depth in product offerings. These players compete through continuous product development, strategic partnerships, and expansion of after?sales support, emphasizing features such as enhanced resolution, faster processing speeds, and machine?learning powered image analysis.

Key Industry Developments:

- In March 2026, Perimeter announced that its Claire AI?enabled optical imaging system received FDA approval, marking a major milestone for intraoperative imaging in breast cancer surgery. The system provides high?resolution, real?time imaging during surgical procedures, helping surgeons assess tumor margins and potentially reduce the need for repeat surgeries. This approval underscores the growing importance of automated optical imaging combined with artificial intelligence in clinical environments, particularly for complex diagnostic and procedural applications.

- In March 2026, Imaris unveiled Imaris 11, an advanced automated image analysis platform that enhances reproducibility and workflow automation for biomedical imaging data. Designed for research and clinical laboratories, this platform supports high?throughput automated processing of imaging datasets, improving efficiency in areas such as 3D visualization, segmentation, and quantitative analysis of biological structures. The new release reflects broader trends in the market toward software?driven automation and AI?assisted interpretation of optical imaging data.

- In June 2025, NIDEK Co., Ltd. launched the RS?1 Glauvas Optical Coherence Tomography (OCT) device, an advanced automated optical imaging system designed for retinal and glaucoma diagnostics in high?volume clinical practices. The RS?1 Glauvas offers high?speed imaging with up to 250?kHz scan rate, wide and deep area capture, and deep learning?based analytics that enhance image clarity, streamline workflows, and improve diagnostic confidence for retinal vascular diseases.

Companies Covered in Automated Optical Imaging Market

- Zeiss Group

- Olympus Corporation

- Nikon Corporation

- Leica Microsystems

- Keyence Corporation

- Basler AG

- Cognex Corporation

- Omron Corporation

- Teledyne Technologies Incorporated

- Canon Inc.

- Sony Corporation

Frequently Asked Questions

The global automated optical imaging market is projected to reach US$4.4 billion in 2026.

The automated optical imaging market is primarily driven by growing demand for high-precision, non-invasive imaging in healthcare and research applications.

The automated optical imaging market is expected to grow at a CAGR of 8.5% from 2026 to 2033.

Key market opportunities in the automated optical imaging market include integration of AI and 3D imaging for advanced diagnostics, expanding use in non-invasive medical applications, and adoption in research and clinical laboratories for high-throughput imaging.

Zeiss Group, Olympus Corporation, Nikon Corporation, Leica Microsystems, and Keyence Corporation are the leading players.