- Energy Storage Solutions

- Energy Transition Market

Energy Transition Market Size, Share, and Growth Forecast, 2025 - 2032

Energy Transition Market By Solution Type (Renewable Energy, Others), Technology (Energy Storage Systems, Others), End-user Sector (Residential, Commercial, Utility Scale, Power & Utility, Transportation, Industrial, Others), and Regional Analysis for 2025 - 2032

Energy Transition Market Share and Trends Analysis

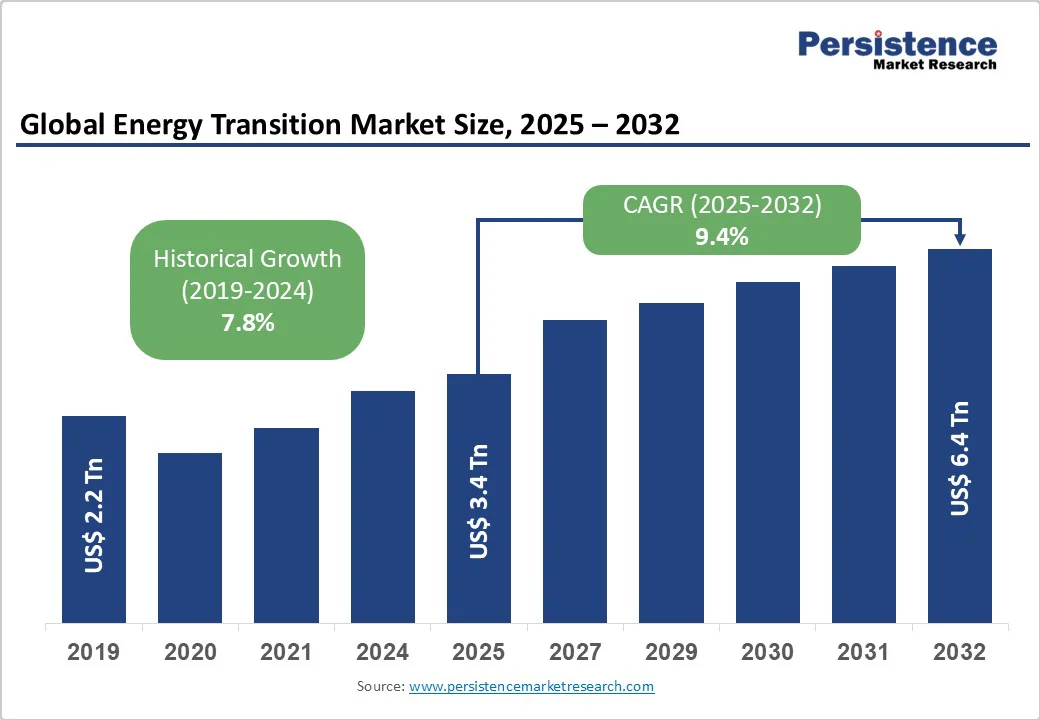

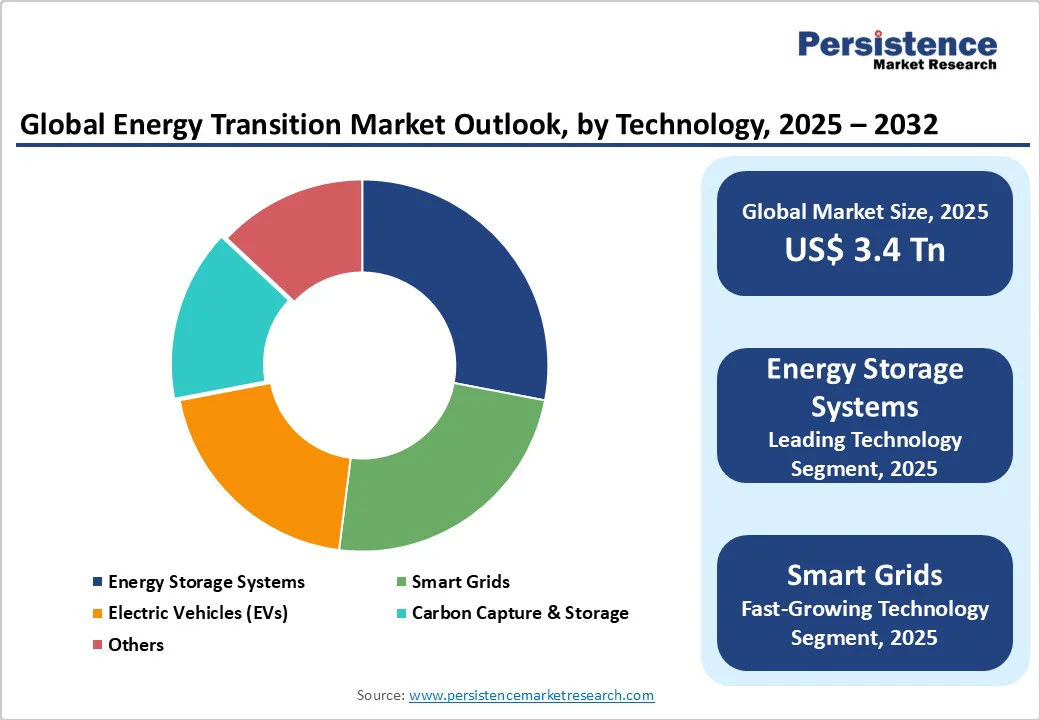

The global energy transition market size is likely to be valued at US$3.4 trillion in 2025. It is estimated to reach US$6.4 trillion by 2032, growing at a CAGR of 9.4% during the forecast period 2025−2032, driven by intensifying climate policies and rapidly declining costs of renewable technologies.

Structural energy shifts are driven by net-zero mandates covering over 70% of the global GDP by 2030 and US$1.3 trillion in annual corporate clean energy procurement. Advances in solar, wind, storage, and green hydrogen are cutting costs and accelerating adoption, fueling major capital flows into decarbonization and infrastructure.

Key Industry Highlights

- Dominant Solution Type: The renewable energy solution category is expected to lead in 2025; hydrogen solutions will exhibit the highest growth at 28% CAGR through 2032.

- Leading Technology: Energy storage is set to lead the technology segment, with about 28% market share in 2025, while smart grids are expected to grow the fastest during 2025-2032.

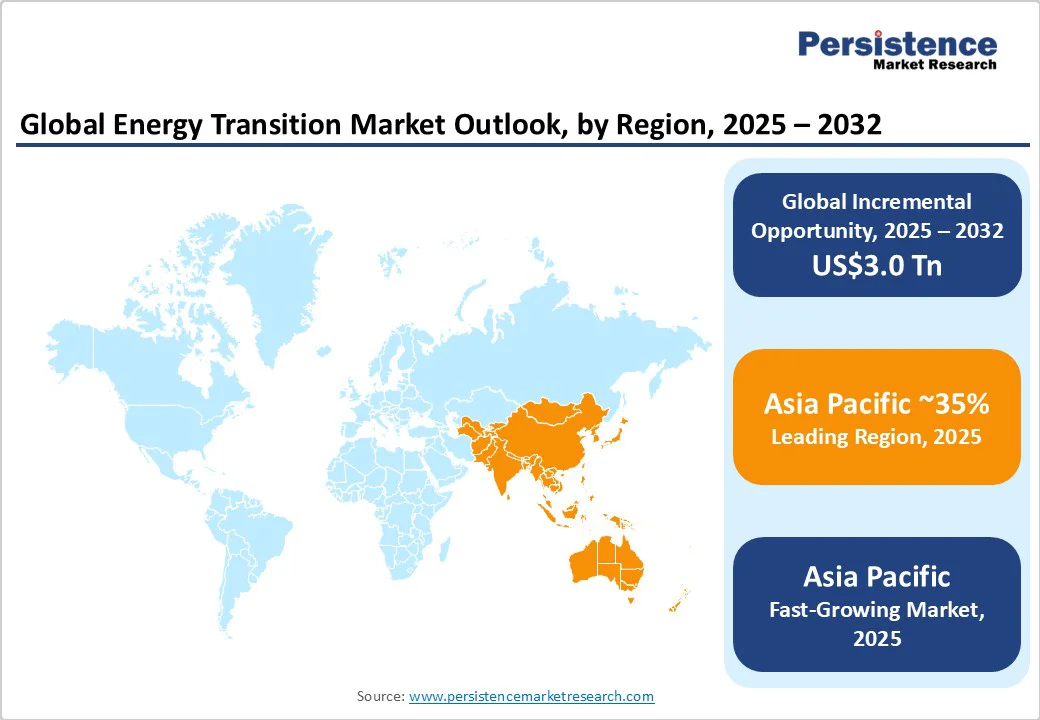

- Leading and Fastest-growing Region: Asia Pacific is anticipated to hold a 35% share with approximately 11.5% CAGR, propelled by China’s solar targets and regional manufacturing advantages.

- Leading Application Segment: Utility-scale applications are likely to account for 48% of the market share in 2025, while transportation leads growth with a 22% CAGR through 2032.

- September 2025: The UAE-based Global South Utilities (GSU) inaugurated a 50 MW solar farm in Chad, supporting the country’s efforts to reduce dependence on fossil fuels and fostering investment in solar infrastructure in emerging African markets to advance sustainable development goals.

| Key Insights | Details |

|---|---|

|

Energy Transition Market Size (2025E) |

US$3.4 Tn |

|

Market Value Forecast (2032F) |

US$6.4 Tn |

|

Projected Growth (CAGR 2025 to 2032) |

9.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Policy and Regulatory Acceleration

Governments worldwide are accelerating decarbonization policies, with frameworks such as the Green Deal of the European Union (EU), the U.S. Inflation Reduction Act (IRA), and China’s carbon neutrality goals driving transformative market conditions. Collectively covering over 70% of global emissions, these initiatives are setting aggressive renewable energy capacity additions, expecting a 25% annual increase in clean energy auctions. Carbon pricing is implemented in 55 jurisdictions, encompassing 22% of global emissions, thereby enhancing the investment environment for low-carbon technologies. The resultant policy-driven funding, exceeding US$600 billion annually, is de-risking projects and facilitating long-term power purchase agreements, enabling the market to grow with greater investor confidence and greater access to financing.

Technology Cost Declines and Performance Improvements

Technological innovations and economies of scale continue to lower costs and improve the performance of critical technologies. Solar photovoltaic system costs have decreased by 85% over the last decade, while onshore wind costs have decreased by 56%, enhancing their competitiveness against fossil fuels. Lithium-ion battery costs have been declining around 12% annually, reaching approximately US$124/kWh and propelling grid-scale energy storage capacity to new highs. Electrolyzer efficiency gains have cut green hydrogen production costs by nearly 50% over the past two years, bringing prices down to US$3.20/kg and unlocking widespread applications in transportation and industry. These advancements are catalyzing new applications and expanding market boundaries through 2032.

Barrier Analysis - Grid Infrastructure and Integration Challenges

Renewable energy deployment is outpacing grid capacity, causing major bottlenecks. In 2024, global grid investments hit US$180 billion, only half of what is needed for full renewable integration. Transmission congestion cuts generation efficiency by up to 12% and raises capital costs by 5-7%. In parts of the U.S., interconnection wait times have surged 90%, delaying projects by an average of 18 months. These challenges heighten financing risks, driving demand for solutions such as grid-forming inverters and advanced demand-side management.

Supply Chain Constraints and Commodity Price Volatility

Supply chain disruptions and volatility in raw materials constrain energy transition growth. Lithium, nickel, and cobalt prices have fluctuated over 35% annually amid geopolitical risks. Lithium carbonate rose from US$7,000/ton in 2022 to US$25,000/ton in 2024, cutting battery margins by 8-12%. Lead times for key components such as inverters now reach 24 months, delaying projects and raising working capital needs by US$50 million per GW. Strategic sourcing and long-term contracts are essential for managing risks and protecting profitability.

Opportunity Analysis - Green Hydrogen Export Corridors

Green hydrogen production and export are emerging as a high-growth market segment, projected to expand from US$2 billion in 2024 to US$25 billion by 2032, growing at an astounding CAGR of 34%. Strategic initiatives in Australia, Chile, and the Middle East are leveraging abundant solar and wind resources to scale electrolyzer facilities to exceed 1 GW in capacity. Developing hydrogen export infrastructure to key European and Asian markets offers an estimated US$10 billion revenue potential by 2030. These developments not only accelerate decarbonization but also open new supply chains, benefiting engineering, procurement, & construction (EPC) contractors, utilities, and commodity traders positioned in the hydrogen ecosystem.

Distributed Energy Resources (DER) Aggregation

The DER aggregation market offers significant revenue growth, expanding from an estimated US$8 billion in 2024 to US$32 billion by 2032, with a CAGR of around 18%. Aggregators combine residential solar, battery storage, and flexible demand assets into virtual power plants (VPPs), providing grid services and reliability enhancements. Regulatory frameworks in advanced markets such as California and Germany are incentivizing market participation, generating ancillary service revenues averaging US$150/kW annually, which reflect internal rates of return (IRRs) of 12% for asset owners. As utility business models evolve, energy service companies can monetize these capabilities through white-labeled software platforms and outcome-based service contracts, diversifying revenue streams and enhancing customer engagement.

Segmentation Analysis

Solution Insights

Renewable energy is expected to continue to dominate the solution category, with an approximate 62% market share estimated for 2025, driven primarily by solar power, which alone accounts for roughly 35%. Wind energy contributes approximately 18%. These segments are benefiting from substantial cost reductions and supportive governmental policies globally. Hydrogen-based solutions are projected to be the fastest-growing segment over 2025–2032, signaling rapid technology adoption and emerging infrastructure investments. The outstanding growth of hydrogen is driven by the scaling of electrolyzer capacity and the expansion of fuel-cell applications, especially in the transport and industrial sectors.

Technology Insights

Energy storage systems represent the leading technology segment, set to hold an estimated 28% of the market share in 2025, underpinning grid stability and facilitating the integration of renewables. This market is supported by 20 GW of annual battery installations globally, with a growing emphasis on utility-scale and behind-the-meter storage projects. Smart grids are rapidly gaining adoption and are expected to exhibit the fastest growth from 2025 to 2032. Investments in digital grid modernization, such as IoT sensors, AI-enhanced demand forecasting, and advanced metering infrastructure, are enabling utilities to optimize grid operations and improve the integration of variable renewable energy sources.

End-user Sector Insights

Utility-scale deployments are expected to dominate in 2025, capturing an estimated 48% of energy transition market revenue share, driven by economies of scale and institutional investment appetite for large-scale solar and wind projects. These assets benefit from mature financing mechanisms and established power purchase agreements (PPAs). The transportation sector is also anticipated to lead growth, registering an approximate 22% CAGR between 2025 and 2032. This expansion is propelled by the electrification of commercial fleets, extensive rollouts of electric vehicle charging infrastructure, and growing adoption of hydrogen fuel-cell vehicles, representing a critical end-user market for clean energy technologies.

Regional Insights

North America Energy Transition Market Trends

North America is estimated to command a 31% share of the market share in 2025, with projected growth through 2032. The U.S. leads globally with approximately 25% of renewable energy installations, driven by the comprehensive incentives provided under the Inflation Reduction Act (IRA), which allocates US$369 billion in tax credits and grants for clean energy investments.

Canada's advancing hydrogen strategy and Mexico’s expanding renewable auctions complement the regional profile. The regulatory environment is advancing initiatives to alleviate interconnection backlogs and prioritize grid resilience. The competitive landscape features dominant utilities such as NextEra Energy and renewables-focused developers, supported by a robust innovation ecosystem and US$45 Billion in private equity infusions.

Europe Energy Transition Market Trends

Europe is projected to hold a 29% market share by 2025. Germany is a key driver, having added 35 GW of renewable capacity in 2024, complemented by the U.K.’s leadership in offshore wind and France’s nuclear asset extensions. Regulatory alignment via the EU’s REPowerEU and Fit-for-55 initiatives is facilitating cross-border grid projects and harmonizing renewable subsidies.

The market features leading utilities such as Enel and EDF, which are pivoting to green hydrogen and battery storage solutions. Capital markets have supported the transition with US$63.5 billion in sustainable debt issuances, underlining strong investor confidence in offshore wind and regional interconnectors.

Asia Pacific Energy Transition Market Trends

Asia Pacific commands the largest regional share of the energy transition market, estimated to reach 35% through 2032. China's ambitious goal of 1 TW of solar capacity by 2030, Japan’s development of its hydrogen supply chain, and India’s target of 500 GW of renewables are propelling regional growth. Manufacturing cost advantages for photovoltaic modules and electrolyzers further bolster competitiveness.

Regulatory drivers include China's national carbon market and India’s renewable purchase obligations, which stimulate domestic demand and vertically integrated supply chains. The market structure is dense with local engineering, procurement, and construction players, while global technology firms are entering through joint ventures. Investment volumes exceeded US$80 Billion in 2024, fueling transmission upgrades and battery gigafactory constructions.

Competitive Landscape

The global energy transition market exhibits moderate consolidation, with the top five players, NextEra Energy, Ørsted, Enel, EDF, and Iberdrola, collectively accounting for about two-fifths of market revenues. These players have been strategically utilizing large asset portfolios, integrated service offerings, and technological innovation to maintain a competitive advantage.

The remainder of the market is served by a fragmented array of regional developers, EPC contractors, and technology entrants, especially within nascent segments such as green hydrogen and distributed energy resources aggregation. The overall market structure encourages strategic partnerships and acquisitions as companies seek scale and diversification.

Key Industry Developments

- In July 2025, SEforALL partnered with NTPC to create an energy transition roadmap aligned with India's net-zero and energy security goals. NTPC is advancing clean energy through green hydrogen, floating solar, battery storage, pumped hydro, and carbon capture, aiming to reach 60 GW of renewables by 2032. The partnership reinforces India’s role in balancing growth with bold climate action.

- In June 2025, Getech and Sound Energy launched HyMaroc, a joint venture to tap Morocco’s hydrogen and helium reserves. Leveraging the country’s strong solar and wind resources, the initiative aims to boost renewable hydrogen production, support regional energy security, and position Morocco as a key player in the global hydrogen economy.

- In June 2025, the U.K.’s Crown Estate announced a £400 million investment in offshore wind over two years to boost renewable capacity. The funding will accelerate infrastructure development, support net-zero goals, and reinforce the Crown Estate’s commitment to sustainable energy and offshore innovation.

Companies Covered in Energy Transition Market

- NextEra Energy

- Ørsted A/S

- Enel S.p.A.

- EDF

- Iberdrola

- Shell plc

- BP p.l.c.

- Siemens Energy

- Tesla

- Vestas

- BYD

- Brookfield Renewable

- JERA

- Adani Green Energy

Frequently Asked Questions

The energy transition market is projected to reach US$3.4 Trillion in 2025.

Intensifying climate policies and rapidly declining costs of renewable technologies are driving the market.

The energy transition market is poised to witness a CAGR of 9.4% from 2025 to 2032.

Structural shifts in energy systems propelled by government mandates targeting net-zero emissions, technological advancements in solar photovoltaics, wind, battery storage, and green hydrogen, and significant capital flows toward decarbonization solutions are key market opportunities.

NextEra Energy, Ørsted, and Enel are some of the key players in the energy transition market.