- Industrial Machinery

- Air Separation Unit Market

Air Separation Unit Market Size, Share, and Growth Forecast 2026 - 2033

Air Separation Unit Market by Product Type (All Gaseous product, All Liquid Product, Combined Liquid and Gas Product), Process (Cryogenic, Non-Cryogenic), Gas Type (Nitrogen, Oxygen, Argon), Industry (Healthcare & Medical, Industrial processes, Steel & Metallurgy, Chemical and Petrochemical, Wastewater Treatment, Food & Beverage, Oil and Gas, Misc.), and Regional Analysis, 2026 - 2033

Air Separation Unit Market Size and Trend Analysis

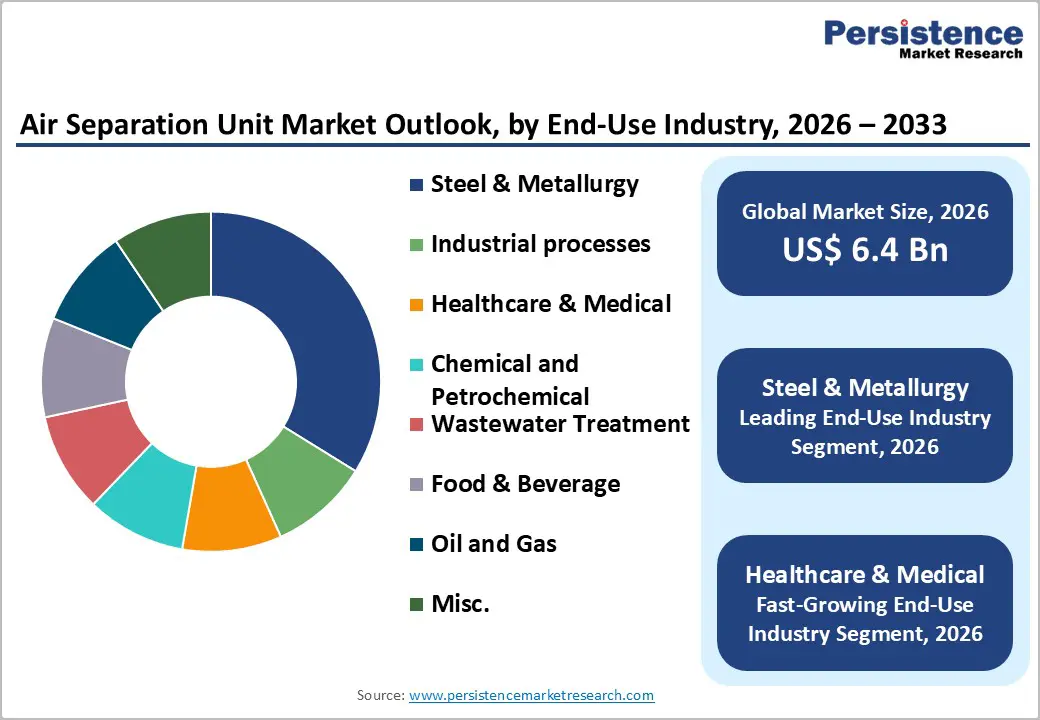

The global air separation unit market size is expected to be valued at US$ 6.4 billion in 2026 and projected to reach US$ 8.8 billion by 2033, growing at a CAGR of 4.3% between 2026 and 2033.

This sustained growth is driven by escalating demand for high-purity industrial gases across critical sectors, including steel manufacturing, healthcare delivery systems, and chemical processing. The World Steel Association reported total global crude steel production of 1,882.6 million tonnes in 2024, with oxygen essential for blast furnace operations and basic oxygen steelmaking, while the expanding semiconductor manufacturing sector requires ultra-pure nitrogen for production.

Key Industry Highlights:

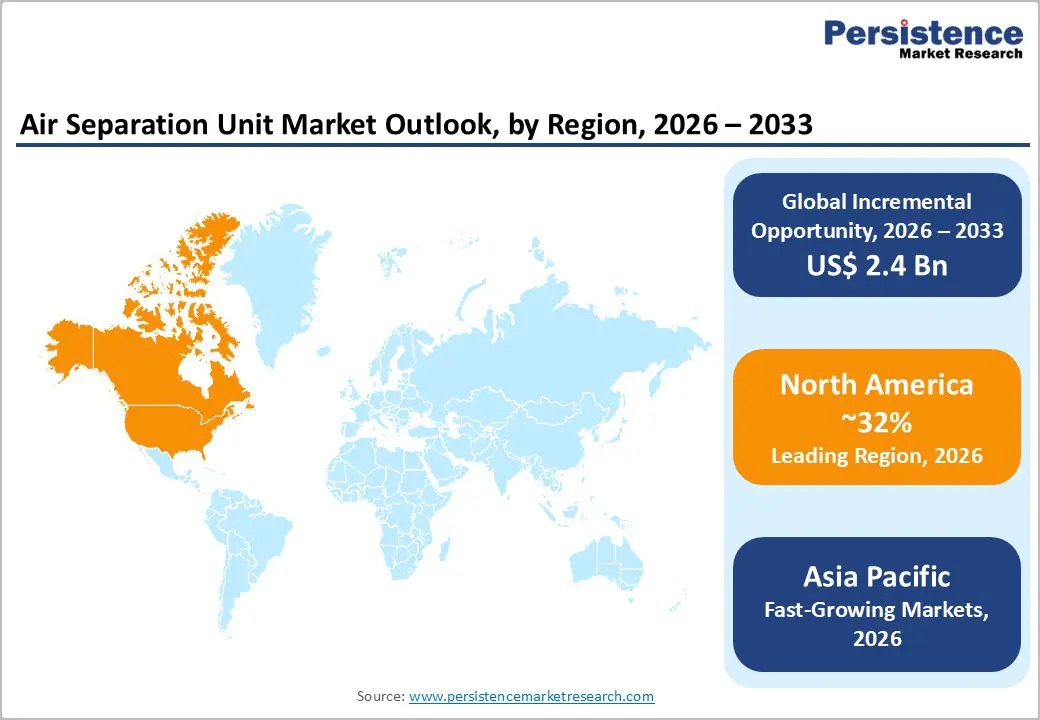

- Fastest Growing Region: Asia Pacific maintains the fastest regional growth trajectory with a projected CAGR of 5.8% from 2026-2033, fueled by China’s massive steel production base of 68.2 million tonnes monthly, India’s construction sector reaching US$ 1.4 trillion by 2025, and semiconductor manufacturing expansion supported by Production Linked Incentive schemes attracting investments from Apple and Samsung.

- Dominant Technology Segment: Cryogenic process technology dominates with approximately 68% market share in 2025, preferred for high-purity gas production exceeding 99.999%, large-scale capacity of 2,000-3,500 tonnes daily, and proven operational reliability supporting continuous industrial operations across steel mills, chemical facilities, and electronics manufacturing complexes.

- Leading Gas Type Segment: Nitrogen is the largest gas type segment, capturing 41% market share in 2025, driven by ubiquitous industrial applications, including chemical processing, inerting operations, modified-atmosphere food packaging, electronics manufacturing, cleanroom environments, and metal heat-treatment processes requiring oxygen-free atmospheres across diverse manufacturing sectors.

- Dominant Industry Segment: Steel & Metallurgy constitutes the dominant Industry with 35% market share in 2025, reflecting fundamental oxygen requirements for blast furnace operations, which consume 40-60 cubic meters per tonne of steel. Global crude steel production of 1,882.6 million tonnes in 2024 has created sustained demand for integrated air separation unit installations.

- Key Opportunity: Hydrogen economy development presents transformative opportunities, with Linde committing over US$ 400 million to air separation units supporting low-carbon ammonia production, while semiconductor expansion requiring ultra-high-purity nitrogen above 99.9999% and renewable energy integration capabilities position advanced ASU technologies for substantial growth in emerging clean energy and high-technology manufacturing markets.

| Key Insights | Details |

|---|---|

| Air Separation Unit Market Size (2026E) | US$ 6.4 billion |

| Market Value Forecast (2033F) | US$ 8.8 billion |

| Projected Growth CAGR (2026 - 2033) | 4.3% |

| Historical Market Growth (2020 - 2025) | 4.6% |

Market Dynamics

Drivers - Surging Demand from Steel and Metallurgy Industries Requiring High-Purity Oxygen

The steel and metallurgy sectors are the dominant drivers of global air separation unit demand, with oxygen serving as an indispensable component of modern steelmaking operations. According to the World Steel Association, global crude steel production reached 1,882.6 million tonnes in 2024, with Asia and Oceania producing 106.3 million tonnes in December 2024 alone, a 9.0% increase from December 2023. Oxygen is critical for combustion, decarburization, and metallurgical operations in blast furnaces and basic oxygen furnaces, positioning air separation units as vital infrastructure components in integrated steel mills worldwide.

India demonstrated remarkable growth, with crude steel production of 14.8 million tonnes in December 2025, up 10.1% year over year, reflecting expanding capacity requirements for industrial gas supply systems. As steel manufacturers increasingly adopt sustainable production practices and transition toward electric arc furnace technologies, investment in advanced air separation unit technologies designed to improve productivity while reducing energy consumption intensity has accelerated significantly. The integration of ASUs with steel facilities ensures a reliable, continuous supply of oxygen at specifications required for consistent metallurgical performance, eliminating dependency on merchant gas supply chains and reducing operational costs over facility lifecycles.

Expanding Healthcare Infrastructure and Medical Oxygen Production Requirements

The healthcare and medical sector has emerged as a strategic driver of air separation unit deployment, particularly for the production of medical-grade oxygen, which is essential for hospital operations and emergency care systems. Air Liquide announced in September 2024 that it had secured a long-term contract with Wanhua Chemical Group in Yantai, China, and invested over US$ 60 million to acquire and operate an air separation unit, demonstrating the commercial viability of dedicated ASU installations.

The healthcare industry’s emphasis on improving public health infrastructure and ensuring reliable oxygen supply capability has intensified following global pandemic experiences, with India’s construction sector expected to reach US$ 1.4 trillion by 2025, according to the National Investment Promotion and Facilitation Agency, driving parallel investments in hospital infrastructure and medical gas distribution systems. Medical oxygen production requires stringent purity specifications and continuous availability, compelling healthcare systems to invest in dedicated air separation units rather than relying solely on liquid oxygen deliveries from centralized production facilities.

Restraints - High Capital Expenditure and Extended Payback Periods for ASU Installations

The air separation unit market faces significant adoption barriers stemming from substantial upfront capital investment requirements and extended project payback timelines. Establishing air separation unit facilities involves complex, specialized equipment, including cryogenic distillation columns, multi-stage compressors, heat exchangers, and purification systems, all of which demand significant engineering expertise and precision manufacturing capabilities. Linde’s August 2025 announcement to invest US$ 100 million in an air separation plant in Brownsville, Texas, to support SpaceX operations underscores the magnitude of capital commitments required for single-facility deployments.

The cryogenic distillation process operates at extremely low temperatures, requiring minus 196 degrees Celsius for nitrogen separation and minus 183 degrees Celsius for oxygen separation, which necessitate sophisticated insulation systems, refrigeration infrastructure, and energy management capabilities that substantially elevate project costs beyond those of conventional industrial equipment. Small and medium-sized industrial operations often cannot justify the investment economics given typical payback periods of 7 to 10 years under normal operating conditions, particularly when alternative gas supply arrangements, such as cylinder delivery or liquid bulk systems, provide operational flexibility without a capital commitment. This capital-intensity barrier becomes particularly acute in emerging markets, where access to project financing, technical expertise, and long-term gas offtake contracts remains constrained.

Intensive Energy Consumption and Operational Cost Pressures

Air separation units represent extremely energy-intensive industrial processes, with electricity costs comprising the dominant component of operating expenses throughout facility lifecycles. The cryogenic separation process requires substantial compression energy to achieve the pressure differentials necessary for fractional distillation, while maintaining ultra-low temperatures demands continuous refrigeration power input. Air Liquide’s financial disclosures indicate plans to increase capital expenditure to EUR 5.0-6.0 billion annually in 2025-2026, partly to address energy transition considerations, reflecting industry awareness that operational efficiency improvements are essential for maintaining competitive positioning.

Electricity price volatility creates uncertainty for air separation unit operators, particularly those operating under fixed-price gas supply contracts where cost escalation cannot be passed through to customers, compressing profit margins and reducing investment returns. In regions lacking stable, low-cost power infrastructure, the economics of air separation units become unfavorable compared to alternative gas supply configurations.

Opportunity - Hydrogen Economy Development Driving Large-Scale Oxygen Demand Growth

The global transition toward hydrogen as a clean energy carrier presents transformative opportunities for air separation unit manufacturers and operators, as oxygen is an essential input for multiple hydrogen production pathways. Linde committed over US$ 400 million in June 2025 to build the largest air separation unit in the Mississippi River corridor for low-carbon ammonia production, supplying oxygen and nitrogen for the 1.4 million metric tonnes ammonia plant operated by Blue Point Number One, a joint venture between CF Industries, JERA, and Mitsui & Co. Hydrogen production through steam methane reforming requires large-scale oxygen supply for gasification processes, while water electrolysis applications necessitate high-purity gas separation capabilities, positioning air separation units as critical infrastructure enabling hydrogen economy development.

The European Commission is required to review technological development in bio-based plastic packaging by February 12, 2028, with potential implications for chemical feedstock production that requires industrial gas inputs. Furthermore, integrating air separation units with renewable energy projects, such as wind and solar farms, facilitates on-site gas production, enhancing overall project efficiency while aligning with sustainability commitments. Market participants who successfully develop air separation unit solutions that incorporate energy storage, grid-balancing capabilities, and hydrogen production integration will secure substantial competitive advantages in emerging clean energy markets.

Semiconductor and Electronics Manufacturing Expansion Requiring Ultra-High Purity Nitrogen

The semiconductor and electronics manufacturing sector offers exceptional growth opportunities for specialized air separation unit technologies capable of producing ultra-high-purity nitrogen, an essential ingredient for production processes. According to Invest India, the electronics market valuation in India reached US$ 101 billion as of March 2023, with ambitious targets to reach US$ 300 billion by 2025-2026, driven by the Production-Linked Incentive schemes attracting substantial investments from major global players, including Apple and Samsung.

Semiconductor fabrication processes require nitrogen purity levels exceeding 99.9999% to prevent oxidation and contamination during photolithography, chemical vapor deposition, and wafer cleaning operations, compelling manufacturers to invest in dedicated air separation unit installations with advanced purification capabilities rather than relying on merchant nitrogen supply. China, Japan, South Korea, and Taiwan continue expanding semiconductor production capacity to support artificial intelligence, 5G technology deployment, and consumer electronics manufacturing, creating sustained demand for industrial gases across electronics clusters.

The Ministry of Electronics and Information Technology in India has spearheaded initiatives, including the Scheme for Promotion of Manufacturing of Electronic Components and Semiconductors (SPECS), to create world-class infrastructure and encourage investment in high-value components. Air separation unit manufacturers that develop modular, compact designs optimized for cleanroom environments while maintaining ultra-high purity specifications will capture significant market share in this rapidly expanding segment, characterized by stringent quality requirements and premium pricing.

Category-wise Analysis

Product Type Insights

Combined liquid and gas production systems account for approximately 52% of the air separation unit market, driven by their operational flexibility and diversified revenue streams. These integrated systems enable simultaneous pipeline supply of gaseous oxygen and nitrogen alongside liquid production for merchant distribution. This dual-output capability enhances asset utilization and allows operators to balance long-term contracts with spot market opportunities. The ability to adjust the product mix between liquid and gaseous forms supports demand fluctuations, maintenance cycles, and emergency supply needs. Such configurations are particularly advantageous in large industrial clusters where multiple customers require varying gas volumes and purity levels from a single integrated facility.

Process Insights

Cryogenic air separation accounts for approximately 68% of the market share, reflecting its superior scalability and ability to deliver ultra-high-purity gases. By utilizing differences in boiling points among atmospheric gases, cryogenic distillation achieves purity levels suitable for steelmaking, healthcare, chemicals, and electronics applications. The technology supports large-capacity installations capable of producing thousands of tonnes per day, making it ideal for integrated industrial complexes requiring continuous and reliable supply. Its long-established operational track record, strong engineering base, and well-developed maintenance ecosystem reduce risk compared to alternative technologies. These advantages reinforce cryogenic systems as the preferred solution for large-scale industrial gas production worldwide.

Gas Type Insights

Nitrogen accounts for around 41% of the air separation unit market, supported by its broad applicability across industries. Its inert characteristics make it essential for chemical processing, petrochemicals, electronics manufacturing, and food packaging. Nitrogen is widely used for reactor inerting, pipeline purging, tank blanketing, and pressure transfer operations. In the food sector, it supports modified atmosphere packaging to extend shelf life and preserve product quality. Semiconductor and electronics manufacturing require ultra-high purity nitrogen for precision fabrication processes. The diversity of nitrogen applications across multiple industrial sectors ensures relatively stable demand, reducing exposure to cyclical fluctuations concentrated in a single Industry.

Industry Insights

Steel and metallurgy hold approximately 35% of the air separation unit market share, reflecting the sector’s heavy reliance on oxygen in primary and secondary steelmaking processes. Oxygen injection enhances combustion efficiency in blast furnaces and facilitates impurity removal in basic oxygen furnaces, directly linking steel production volumes to industrial gas demand. Even as electric arc furnace technology expands, oxygen remains critical for decarburization and slag management. Additionally, specialty steel production requires argon for inert atmosphere protection during refining. The continuous, high-volume gas requirements of steel plants favor dedicated onsite air separation units, reinforcing the sector’s dominant position in overall market demand.

Regional Insights

North America Air Separation Unit Market Trends and Insights

North America represents a mature and technologically advanced air separation unit (ASU) market, supported by established industrial infrastructure and strict regulatory oversight. Strong activity in steel, petrochemicals, refining, aerospace, and energy transition projects sustains demand for oxygen and nitrogen supply systems. Environmental and process safety regulations, particularly in the United States, impose stringent operational and design standards, encouraging the adoption of highly efficient and digitally monitored ASU technologies.

The region is also witnessing rising investments in low-carbon hydrogen and ammonia projects, where large-scale ASUs are essential for integrating oxygen supply. Industrial gas majors continue expanding onsite and merchant production capacities to strengthen supply resilience and serve clean energy initiatives. Advanced manufacturing hubs along the Gulf Coast and Midwest further facilitate deployment of high-capacity cryogenic units. Overall, stable industrial demand combined with decarbonization investments positions North America as a strategically important and innovation-driven ASU market.

Europe Air Separation Unit Market Trends and Insights

Europe is a technologically sophisticated ASU market characterized by stringent environmental standards and strong decarbonization commitments. Mature industrial bases in Germany, France, Italy, and the Benelux region sustain steady demand from steel, chemicals, refining, and manufacturing sectors. European Union regulations governing pressure equipment, emissions, and industrial safety significantly influence plant design, efficiency benchmarks, and operational compliance requirements. The region is increasingly aligning ASU investments with green steel, hydrogen economy, and renewable energy integration projects, creating new growth avenues beyond traditional industries.

Major industrial gas companies operate extensive pipeline networks connecting large-scale air separation facilities to industrial clusters, ensuring supply reliability and optimized asset utilization. Additionally, sustainability initiatives and carbon reduction targets are accelerating the modernization of existing plants toward energy-efficient and low-emission configurations. Europe’s combination of regulatory rigor, technological expertise, and clean energy leadership continues to shape the deployment of advanced ASUs across the region.

Asia Pacific Air Separation Unit Market Trends and Insights

Asia Pacific is the fastest-growing ASU market, driven by rapid industrialization, expanding steel production, semiconductor manufacturing growth, and large-scale infrastructure development. China and India remain central to regional demand due to massive steel output and construction activity, which directly correlate with oxygen consumption. Simultaneously, the expansion of electronics and semiconductors across China, Taiwan, South Korea, Japan, and India is fueling demand for ultra-high-purity nitrogen.

Government-led industrial policies, manufacturing incentives, and infrastructure programs are accelerating capacity additions across chemicals, energy, and heavy industries. The region also benefits from competitive manufacturing costs and expanding technical expertise, enabling both domestic ASU deployment and export-oriented equipment production. Safety regulations in developed markets, such as Japan, ensure operational reliability and adherence to quality standards. With ongoing urbanization and industrial diversification, the Asia Pacific continues to emerge as both the largest consumption hub and a strategic production center for air separation technologies.

Competitive Landscape

The air separation unit (ASU) market demonstrates moderate consolidation, with a limited number of global industrial gas companies holding significant market share due to their technological expertise, large-scale manufacturing capabilities, and long-term customer contracts. The market structure favors high entry barriers, driven by capital intensity, engineering complexity, and strict regulatory compliance requirements. As a result, competition is primarily concentrated among established players with integrated global operations and strong balance sheets.

Business strategies center on improving cryogenic efficiency, reducing energy consumption, and deploying modular plant designs that lower capital costs and shorten installation timelines. Companies increasingly incorporate digital monitoring, automation, and predictive maintenance tools to enhance reliability and reduce downtime. Long-term build-own-operate (BOO) agreements remain a dominant commercial model, enabling suppliers to secure stable revenue streams while minimizing customer investment risk. Additionally, strategic investments are aligned with clean energy, hydrogen, and low-carbon industrial projects, positioning suppliers as infrastructure partners in global decarbonization initiatives.

Key Developments:

- June 2025: Linde announced a long-term agreement with Blue Point Number One, investing more than US$ 400 million to build the largest air separation unit in the Mississippi River corridor providing oxygen and nitrogen for 1.4 million metric tonnes low-carbon ammonia production, strengthening its Gulf Coast industrial gases infrastructure.

- August 2025: Linde broke ground on a US$ 100 million air separation plant at Brownsville’s North Industrial Park, Texas, to supply liquid oxygen and nitrogen for SpaceX’s Starship program, reducing delivery distance from over 500 miles to less than 50 miles and creating 15 direct jobs with above-average wages.

- September 2024: Air Liquide secured a long-term contract with Wanhua Chemical Group in Yantai, China, investing over US$ 60 million to acquire and operate an air separation unit plus liquefied argon production unit for Industrial Merchant markets across Shandong province, expanding Asian market presence.

Companies Covered in Air Separation Unit Market

- Air Liquide S.A.

- Linde AG

- Messer Group GmbH

- Air Products and Chemicals, Inc.

- Taiyo Nippon Sanso Corporation

- Praxair, Inc.

- Oxyplants

- AMCS Corporation

- Enerflex Ltd

- Technex Ltd.

- Ranch Cryogenics

- Daesung Industrial Co., Ltd.

- Air Water Inc.

- Yingde Gases Group Co., Ltd.

- Inox Air Products Private Limited

- Universal Industrial Gases, Inc.

- Cryotec Anlagenbau

- Kaifeng Air Separation Group

- Sichuan Air Separation Plant Group

- NIKKISO

Frequently Asked Questions

The global air separation unit market is expected to reach US$ 6.4 billion in 2026.

Demand is driven by steel production, healthcare infrastructure, and semiconductor manufacturing.

Asia Pacific leads, with the fastest growth driven by China and India.

Opportunities include hydrogen economy development, semiconductor expansion, and renewable energy integration.

Major players include Air Liquide, Linde, Air Products, Messer Group, Taiyo Nippon Sanso, Praxair, Inox Air Products, Yingde Gases, and Universal Industrial Gases.