- Media & Entertainment

- AI in Gaming Market

AI in Gaming Market Size, Share, and Growth Forecast, 2026 - 2033

AI in Gaming Market by Product Type (Game Development & Design, Non-Player Character (NPC) Behavior, Others), Application (NPCs & Digital Humans, AI-generated Content Creation, Others), Technology, Platform, and Regional Analysis for 2026 - 2033

AI in Gaming Market Size and Trends Analysis

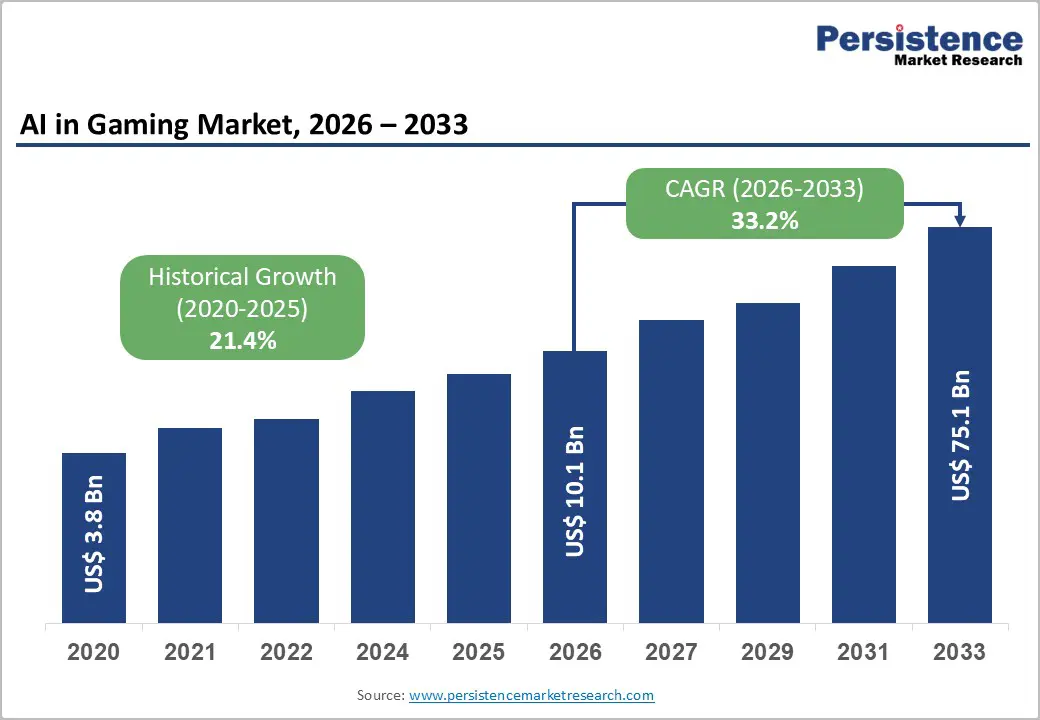

The global AI in gaming market size is likely to be valued at US$10.1 billion in 2026 and is expected to reach US$75.1 billion by 2033, growing at a CAGR of 33.2% between 2026 and 2033, driven by the rapid integration of AI across game development pipelines, real-time gameplay systems, and player engagement frameworks, enabling studios to improve production efficiency and deliver more adaptive gaming experiences.

The increasing use of AI in content generation, NPC behavior modeling, and live-service optimization is accelerating adoption across both AAA publishers and independent developers, reinforcing AI as a core component of modern game design.

Key Industry Highlights:

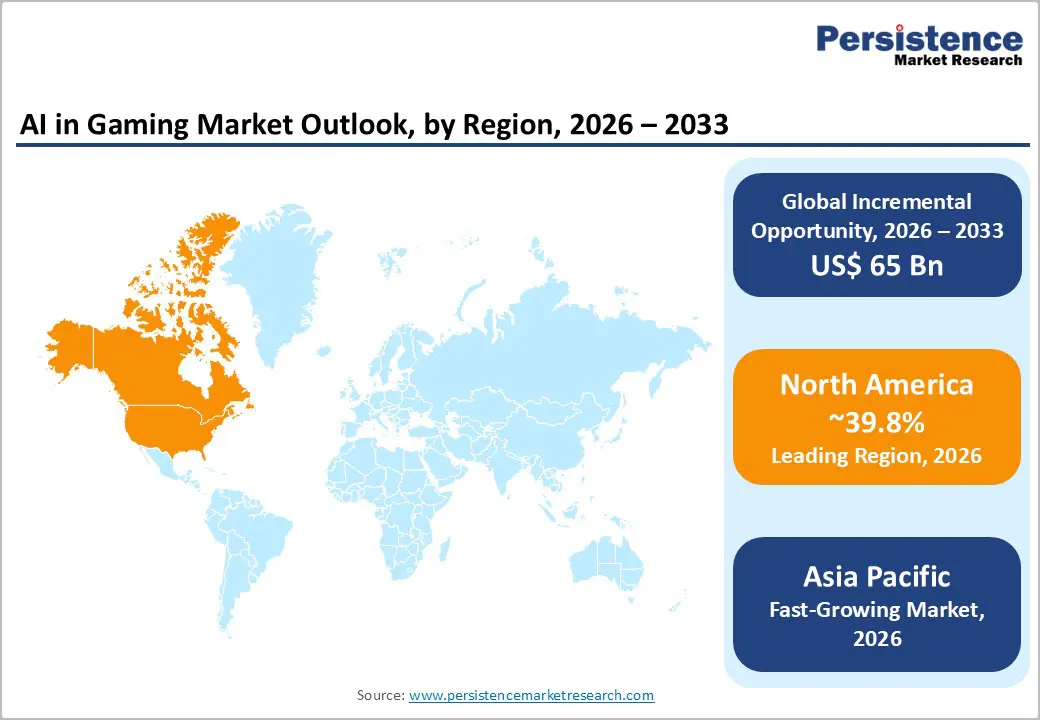

- Leading Region: North America is projected to account for approximately 39.8% of the market share, driven by the strong presence of major technology providers, advanced AI infrastructure, and high adoption across game development ecosystems.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by rapid mobile gaming adoption, expanding digital infrastructure, and increasing AI integration by regional publishers.

- Investment Plans: Industry investments are increasingly focused on AI-driven game development, cloud gaming platforms, and immersive technologies, with companies allocating significant budgets toward generative AI, neural rendering, and real-time personalization capabilities to enhance scalability and reduce production costs.

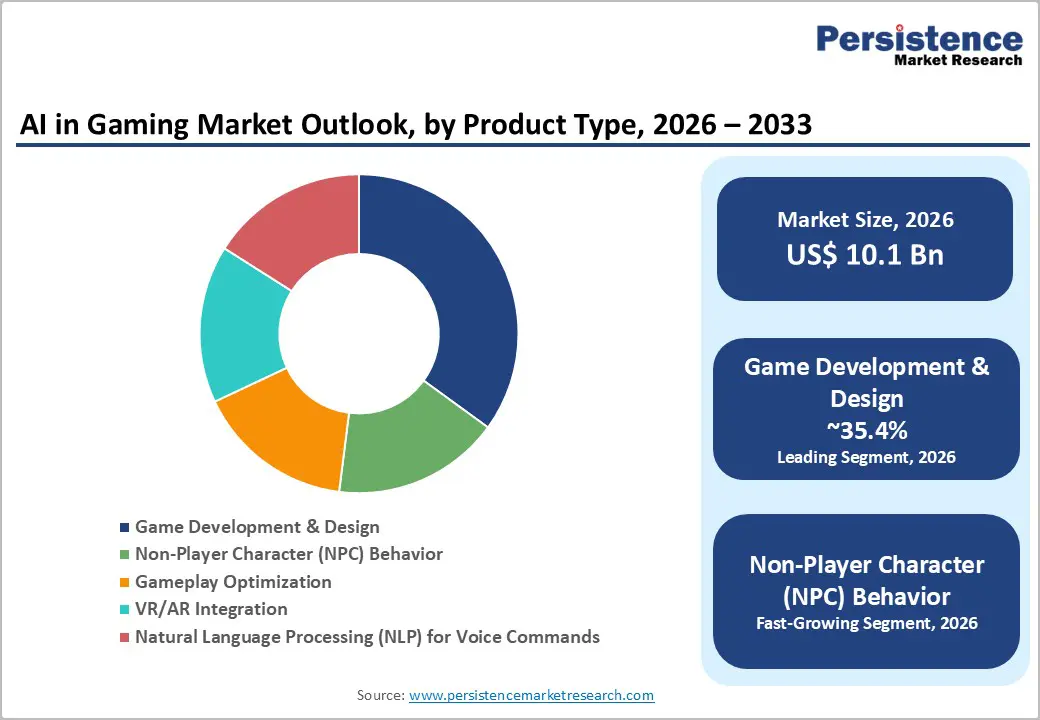

- Dominant Product Type: The game development and design segment is expected to lead, holding an anticipated market share of approximately 35.4%, due to widespread use of AI in asset creation, coding assistance, and workflow automation.

- Leading Application: The NPCs and digital humans segment is expected to dominate with around 28.6% market share, as AI-driven character realism and interactive storytelling remain central to enhancing player engagement and retention.

DRO Analysis

Driver - AI-Driven Production Efficiency and Cost Optimization

AI has transitioned from a niche capability to a core production tool in game development workflows. A large majority of developers now use AI for automating repetitive processes such as asset tagging, bug detection, and script generation. Industry surveys indicate that over 90% of developers have adopted generative AI tools, with a significant proportion leveraging them for code generation and automated testing. This shift is critical because modern game development involves rising production budgets and longer development cycles.

AI reduces iteration time, minimizes manual testing requirements, and enables faster content deployment in live-service environments. The impact is particularly strong for large publishers managing multi-year development pipelines, where even incremental efficiency gains translate into substantial cost savings and improved time-to-market performance.

Technological Advancements in Machine Learning and Generative AI

Rapid advancements in machine learning, generative AI, and neural rendering technologies are significantly expanding AI’s role in gaming. AI systems now support procedural content generation, dynamic gameplay adaptation, animation synthesis, and physics simulation, making them integral across multiple stages of development and gameplay. Reinforcement learning frameworks enable more realistic and adaptive NPC behaviors, while generative models assist in creating textures, environments, and dialogue. These innovations extend AI adoption beyond engineering teams to include design, creative, quality assurance, and live operations functions. As a result, AI spending is becoming embedded across the entire game lifecycle, increasing its strategic importance for both production efficiency and user experience enhancement.

Restraint Analysis - Intellectual Property and Regulatory Uncertainty

Despite strong growth potential, intellectual property (IP) and regulatory challenges remain significant barriers to market expansion. Current legal frameworks in major markets do not fully address the ownership of AI-generated content, creating ambiguity around authorship and rights protection. In several jurisdictions, content generated entirely by AI may not qualify for copyright protection, raising concerns for publishers relying on generative tools.

At the same time, emerging regulatory frameworks impose compliance requirements on transparency, data use, and accountability, increasing operational complexity. These uncertainties can delay adoption, particularly among large publishers that must manage legal risks across multiple markets and ensure compliance with evolving global standards.

Opportunity Analysis - Expansion of AI-Generated Content Creation

AI-generated content represents one of the most scalable and commercially viable opportunities in the gaming industry. Studios are increasingly adopting AI tools for procedural environment creation, character design, dialogue generation, and localization, enabling them to produce high-quality content at lower cost and faster speeds. This is especially valuable for live-service games that require frequent updates and new content releases to maintain player engagement.

Smaller studios and independent developers benefit significantly, as AI reduces reliance on large creative teams and lowers barriers to entry. As AI models continue to improve, their ability to generate game-ready assets is expected to enhance productivity and drive broader adoption across the industry.

Growth of Immersive and Cloud-Based Gaming Ecosystems

The expansion of virtual reality (VR), augmented reality (AR), and cloud gaming platforms is creating new opportunities for AI integration. AI enhances these platforms by enabling real-time personalization, adaptive gameplay, intelligent matchmaking, and latency optimization. As network infrastructure improves and cloud gaming adoption increases, AI will play a critical role in delivering seamless, low-latency experiences.

Immersive gaming environments also require advanced AI systems to manage complex interactions and dynamic environments, further driving demand. This convergence of AI with next-generation gaming platforms is expected to unlock new revenue streams and expand the addressable market.

Category-wise Analysis

Product Type Insights

Game development and design are anticipated to account for approximately 35.4% of the market share in 2026. This dominance is driven by the extensive use of AI in asset creation, level design, animation, coding assistance, and workflow automation. AI tools are increasingly embedded within game engines such as Unity Technologies and Epic Games, enabling faster iteration and improved productivity. Studios use AI to streamline complex processes, such as environment generation and bug detection, thereby reducing development timelines and operational costs.

For instance, AI-assisted procedural generation has been widely used in large-scale open-world games to create expansive environments with reduced manual effort, while automated QA systems help identify bugs during development cycles. The segment’s leadership reflects the industry’s focus on optimizing production pipelines, where AI delivers immediate and measurable efficiency gains.

NPC Behavior is projected to be the fastest-growing segment, supported by increasing demand for immersive and interactive gameplay experiences. AI-powered NPCs can adapt to player actions, learn from interactions, and exhibit realistic behaviors, significantly enhancing engagement. Advances in reinforcement learning and behavioral modeling allow developers to create dynamic game worlds where characters respond intelligently to changing scenarios.

For example, games like Red Dead Redemption 2 and The Elder Scrolls V: Skyrim showcase evolving NPC interactions that enhance realism and player immersion. This capability is particularly valuable in open-world and role-playing games, where player immersion is a key success factor. As player expectations continue to evolve, investment in NPC intelligence is expected to accelerate, especially with the integration of generative AI for dialogue and behavior modeling.

Application Insights

NPCs and Digital Humans are anticipated to hold approximately 28.6% of the market share in 2026, making them the largest application segment. This segment directly impacts the player experience layer, where AI enhances realism, storytelling, and interactivity. Digital humans powered by AI enable lifelike animations, natural dialogue, and emotional responsiveness, making games more engaging and immersive. For instance, AI-driven character systems in games like Cyberpunk 2077 demonstrate advanced facial animation and behavioral realism, while emerging AI companions in narrative-driven games are redefining player interaction. For developers, this application offers dual benefits: improving gameplay quality and increasing player retention and monetization opportunities.

AI-generated content creation is expected to be the fastest-growing application segment, driven by the need for rapid content production and continuous game updates. AI tools enable procedural generation of environments, characters, and narrative elements, significantly reducing development time. This is particularly important for live-service games, where frequent updates are essential to maintain user engagement. For example, games like No Man's Sky use procedural generation techniques to create vast universes, while studios increasingly leverage generative AI tools for concept art and level design prototyping.

The ability to generate content at scale allows developers to experiment with new concepts, personalize gameplay experiences, and respond quickly to player feedback, reinforcing this segment’s strong growth trajectory.

Regional Insights

North America AI in Gaming Market Trends

North America is expected to be the largest regional market, accounting for approximately 39.8% of the market share in 2026. The region’s leadership is driven by the presence of major gaming and technology companies such as Microsoft, NVIDIA, Electronic Arts, and Unity Technologies, alongside advanced technological infrastructure and strong investment in AI research and development.

U.S. AI in Gaming Market Trends

The U.S. dominates the regional market, contributing the majority of revenue due to its concentration of leading publishers, cloud providers, and AI innovators.

Key growth drivers include high adoption of AI technologies, robust funding for innovation, and a mature gaming ecosystem. The region benefits from strong collaboration between technology firms and gaming companies. For example, Microsoft introduced its generative AI model “Muse” to support gameplay ideation and development workflows, while NVIDIA continues to expand its RTX ecosystem with AI-powered neural rendering tools that enhance real-time graphics and character realism. Similarly, Electronic Arts has integrated AI across game testing, animation, and content creation pipelines, improving efficiency and reducing production timelines.

Investment activity remains strong, with companies focusing on AI integration, cloud gaming, and immersive technologies. The expansion of cloud gaming platforms by Microsoft through Xbox Cloud Gaming and AI-driven graphics innovation from NVIDIA is reshaping how games are developed and delivered. These developments reinforce North America’s leadership by enabling scalable, high-performance gaming experiences while accelerating the adoption of AI across the value chain.

Europe AI in Gaming Market Trends

Europe represents a significant and steadily growing market, supported by a strong base of developers and an established gaming ecosystem. Key countries such as Germany, the United Kingdom, France, and Spain play a central role in driving regional growth, with major companies like Ubisoft and CD Projekt contributing to innovation in AI-driven game development. A defining characteristic of the European market is its regulatory environment, particularly the implementation of the EU AI Act, which emphasizes transparency, accountability, and ethical AI usage. While these regulations introduce compliance requirements, they also create a structured framework that encourages responsible innovation.

U.K. AI in Gaming Market Trends

The U.K. is expected to play a leading role in AI-driven game development and innovation, supported by a mature gaming industry and strong venture capital activity. Companies such as Ubisoft (with major studios in the U.K.) and other local developers are actively adopting AI for NPC behavior modeling and automated content generation. The U.K. government’s focus on AI as a strategic sector, combined with a highly skilled workforce, has accelerated adoption across both AAA studios and independent developers, making it a key contributor to regional growth.

Investment trends in Europe focus on AI-driven innovation, cross-border collaboration, and digital transformation initiatives. For example, Sony Interactive Entertainment, with strong operations across Europe, continues to invest in AI-enhanced gaming experiences for its PlayStation ecosystem, while studios such as CD Projekt are incorporating AI tools to enhance open-world storytelling and character behavior. These developments highlight how European companies are balancing regulatory compliance with innovation, positioning the region as a key contributor to the global AI in gaming market.

Asia Pacific AI in Gaming Market Trends

Asia Pacific is set to be the fastest-growing region, driven by rapid expansion across China, Japan, South Korea, India, and Southeast Asia. The region benefits from a large and growing player base, strong mobile gaming adoption, and increasing investments in digital infrastructure.

China AI in Gaming Market Trends

China is expected to be the largest gaming market in the region, with companies such as Tencent and NetEase leading AI adoption. These companies use AI for player behavior analysis, matchmaking optimization, anti-cheat systems, and procedural content generation. Their large-scale multiplayer ecosystems provide vast datasets, enabling continuous improvement of AI-driven systems and reinforcing China’s leadership in AI-powered gaming operations.

Japan AI in Gaming Market Trends

Japan is anticipated to be a key player in high-quality, narrative-driven gaming, with companies like Square Enix and Bandai Namco Entertainment exploring AI applications in storytelling, character development, and animation. AI is increasingly used to enhance emotional realism and interaction within games, aligning with Japan’s focus on immersive and story-rich gaming experiences.

The primary growth drivers across Asia Pacific include high smartphone penetration, expanding connectivity, and strong demand for interactive entertainment. Governments and private sector players are investing heavily in AI research, gaming infrastructure, and digital ecosystems, creating favorable conditions for market expansion.

Competitive Landscape

The global AI in gaming market is moderately fragmented, with a mix of global technology providers, game publishers, and specialized AI solution vendors. Leading companies maintain strong positions through advanced technology capabilities, extensive intellectual property, and established distribution networks. While no single player dominates the market, competition is intensifying as companies expand their AI capabilities and invest in innovation.

Recent developments highlight a strong focus on AI innovation, partnerships, and infrastructure expansion. Companies are investing in generative AI models for gameplay ideation, forming strategic collaborations to accelerate content creation, and establishing dedicated AI research centers. Technology providers are also introducing advanced tools for neural rendering and real-time character generation, enabling more immersive gaming experiences. Key players are focusing on innovation, platform integration, and market expansion. Strategies include embedding AI into development tools, leveraging cloud platforms for scalability, and enhancing player engagement through personalization. Companies are also investing in proprietary data and AI models to strengthen competitive differentiation.

Key Industry Developments

- In October 2025, Electronic Arts announced a strategic partnership with Stability AI to co-develop AI-driven tools for content creation, focusing on accelerating 3D environment generation and improving production workflows for game developers.

- In January 2026, NVIDIA introduced DLSS 4.5 and Multi Frame Generation 6X at CES 2026, leveraging transformer-based AI models to enhance image quality, improve frame rates, and deliver smoother high-refresh-rate gaming experiences.

Companies Covered in AI in Gaming Market

- NVIDIA

- Microsoft

- Tencent

- Sony Interactive Entertainment

- Electronic Arts

- Unity Technologies

- Epic Games

- Ubisoft

- Take-Two Interactive

- Advanced Micro Devices (AMD)

- Intel

- NetEase

- Bandai Namco Entertainment

- Square Enix

- Roblox Corporation

Frequently Asked Questions

The global AI in gaming market is valued at US$10.1 billion in 2026.

The AI in gaming market is projected to reach US$75.1 billion by 2033.

Key trends include the growing use of generative AI for content creation, the increasing deployment of AI-driven NPCs and digital humans, the expansion of cloud gaming platforms, and the rising integration of AI in game testing, personalization, and live-service optimization.

The game development and design segment leads the market with an anticipated share of approximately 35.4%, driven by the widespread adoption of AI for asset creation, coding assistance, and workflow automation.

The AI in gaming market is expected to grow at a CAGR of 33.2% between 2026 and 2033.

Some of the major players include NVIDIA, Microsoft, Electronic Arts, Unity Technologies, and Tencent.