- Medical Devices

- Intra-aortic Balloon Pump Market

Intra-aortic Balloon Pump Market Size, Share, Growth, and Regional Forecast, 2025 to 2032

Intra-aortic Balloon Pump Market by Product Type {Intra - Aortic Balloon Pump (IABP) Console, Intra - Aortic Balloon Pump (IABP) Catheters, Accessories & Consumables}, Indication (Cardiogenic Shock, Heart Transplant, Acute Coronary Syndrome, Others), End-user (Hospitals, Ambulatory Surgical Centers, Others), and Regional Analysis from 2025 to 2032

Intra-aortic Balloon Pump Market Share and Trends Analysis

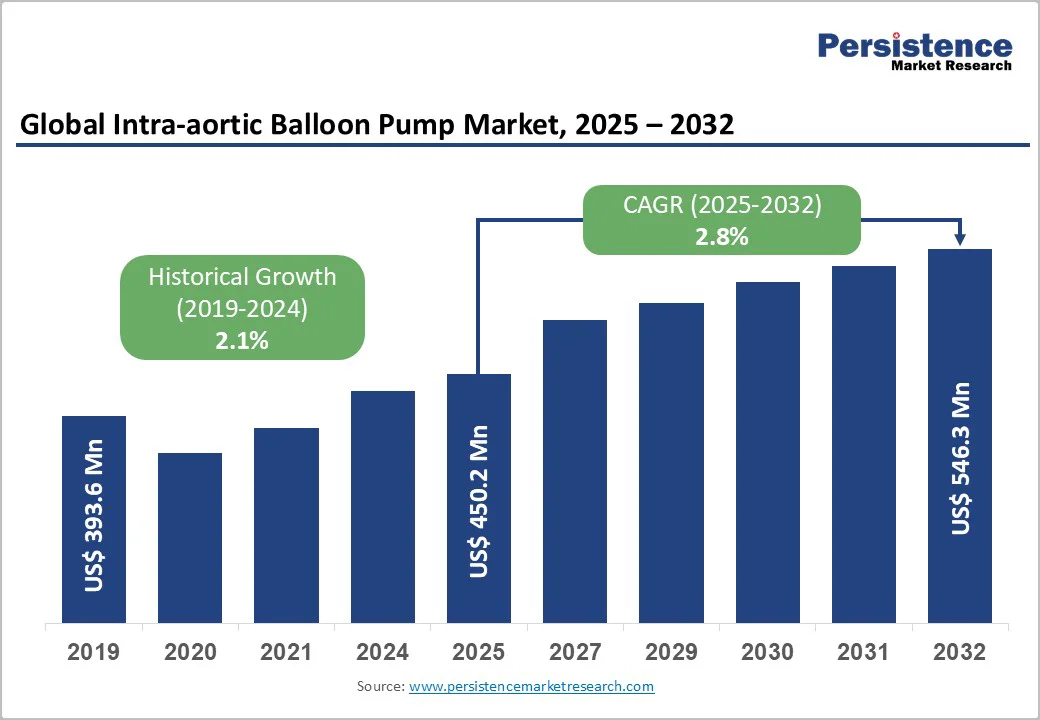

The global intra-aortic balloon pump market size is valued at US$450.2 million in 2025 and projected to reach US$546.3 million at a CAGR of 2.8% during the forecast period from 2025 to 2032.

The global intra-aortic balloon pump Industry is growing steadily due to rising cardiovascular disease cases, increased use in cardiogenic shock, and advancements in console and catheter technologies. North America leads with a robust cardiac care infrastructure. At the same time, the Asia Pacific is the fastest-growing region, driven by healthcare investments, expanding cardiac centers, and improved awareness of mechanical circulatory support.

Key Industry Highlights

- Leading Region: North America, holding nearly 40.5% market share in 2025, driven by advanced cardiac care infrastructure, high procedure volumes for cardiogenic shock and acute coronary syndrome, and strong presence of major IABP manufacturers

- Fastest-Growing Region: Asia Pacific, propelled by rising cardiovascular disease prevalence, expanding tertiary cardiac centers, and increased healthcare investments in China, India, and Japan

- Investment Plans: Europe, focusing on upgrading cardiac ICUs, increasing access to mechanical circulatory support systems, and supporting clinical collaborations to enhance IABP adoption across major hospitals

- Dominant Product: IABP Catheters, capturing nearly 51.4% market share, owing to their single-use nature, recurring procedural demand, and continuous improvements in fiber-optic and biocompatible materials

| Global Market Attributes | Key Insights |

|---|---|

| Global Intra-aortic Balloon Pump Market Size (2025E) | US$ 450.2 Mn |

| Market Value Forecast (2032F) | US$ 546.3 Mn |

| Projected Growth (CAGR 2025 to 2032) | 2.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 2.1% |

Market Dynamics

Driver - Growing use of IABP in Cardiogenic Shock Management

The use of the intra-aortic balloon pump (IABP) in managing cardiogenic shock (CS) is increasingly recognized as a key driver for the IABP market. A German national registry covering 2007-2017 documented an increase in CS incidence from 33.1 to 53.7 per 100,000 person-years, with hospital survival remaining at only ~41%.

In this cohort, among patients receiving mechanical circulatory support, those treated with IABP had a survival rate of 49.5%. Separately, in real-world data from acute coronary syndrome complicated by CS, mortality ranged from 50-80%.

The convergence of rising CS prevalence and the need for haemodynamic support systems underpins growing demand for IABP devices, driving market growth through increased procedural volume, hospital investment, and replacement of older support technologies.

Restraints - High Procedural and Maintenance Costs

High procedural and maintenance costs represent a significant restraint for the intra-aortic balloon pump (IABP) market, limiting adoption in cost-sensitive hospitals, particularly in emerging economies. Data from the IABP SHOCK II trial in Germany indicated that the average total cost for patients receiving IABP support was €33,155 ± 14,593, compared with €32,538 ± 14,031 for control patients, with the IABP device itself contributing approximately €760 ± 174.

In countries like India, device-related hospital costs for IABP procedures typically range from USD 5,500 to 8,500, whereas in Singapore, overall procedural costs can reach USD 25,000 to 45,000, reflecting high operational and device expenses.

Additional expenditures include consumables, catheter replacements, routine console maintenance, and staff training. These high costs create barriers for smaller hospitals and restrict widespread implementation in developing regions, making budget constraints a critical factor restraining global IABP market growth despite rising cardiovascular disease prevalence and procedural demand.

Opportunity - Development of Next-Generation Fiber-Optic and Biocompatible Catheters

The development of next-generation fiber-optic and biocompatible catheters is a compelling opportunity in the Intra-aortic Balloon Pump (IABP) market. For example, fiber-optic tipped catheters have demonstrated a 96% reduction in device-related perfusion call-outs (17 vs 1) and a 94% drop in sub-optimal timing (55/98 vs 2/94) when compared with conventional fluid filled transducers.

A case report described an 8 French (Fr) catheter with fiber-optic sensing, capable of safely providing 50 cc of volume displacement, expanding access to more patients. The fiber optic sensors also offer high-fidelity arterial pressure measurements unaffected by electromagnetic interference, compared to traditional systems.

These improvements in accuracy, miniaturization (eg, 6 Fr catheters for smaller patients) and biocompatible coatings (reducing vascular complications) promise broader adoption, reduced complication rates, and potential market expansion into smaller centers and emerging markets.

Category-wise Analysis

By Product Type, Intra-Aortic Balloon Pump (IABP) Catheters dominate the Intra-aortic Balloon Pump Market

The Intra-Aortic Balloon Pump (IABP) Catheters dominate the market with a 51.4% share in 2025, due to their single-use nature and high procedural turnover. Each IABP procedure, whether for cardiogenic shock or high-risk PCI, requires a new balloon catheter, driving consistent recurring demand. Clinical data show that 40 cc catheters are used in approximately 80-85% of PCI cases requiring IABP support.

Unlike consoles, which are capital equipment with multi-year lifespans, catheters are disposable, contributing the majority of recurring revenue. Advances in catheter design, including smaller French sizes, improved biocompatible materials, and fiber-optic sensing, further encourage replacement and upgrades.

These factors, combined with the growing prevalence of cardiovascular diseases and procedural volumes, make IABP catheters the largest revenue-generating product type, accounting for nearly half of the market.

By Indication, Cardiogenic Shock is gaining traction due to high incidence, urgent support needs, and improved survival rates.

Cardiogenic shock (CS) dominates the market because it represents the most urgent and frequent indication for mechanical circulatory support. Data from Germany between 2007 and 2017 show that the incidence of CS increased from 33.1 to 53.7 per 100,000 person-years, reflecting a growing patient population in need of hemodynamic stabilization.

Overall hospital survival for CS remains low, around 40.2%, highlighting the clinical need for supportive devices. Among patients requiring mechanical circulatory support, IABP is widely used due to its relative ease of deployment, lower complication rates, and ability to provide immediate counter pulsation.

Studies show survival rates of 49.5% with IABP versus 30-35% with alternative devices in select populations. The rising prevalence of CS and established clinical adoption make this indication the largest revenue contributor in the IABP market

Regional Insights

North America Intra-aortic Balloon Pump Market Trends

North America dominates the global market with 40.5% share in 2025, due to the high prevalence of cardiovascular diseases, well-established healthcare infrastructure, and favorable reimbursement policies. In the U.S., approximately 6.7 million adults suffer from heart failure, projected to reach 8.7 million by 2030, highlighting the growing need for hemodynamic support.

Around one million percutaneous coronary interventions (PCI) are performed annually, many in high-risk patients who benefit from IABP use. The region’s extensive network of tertiary cardiac centers, advanced catheterization labs, skilled interventional cardiologists, and strong insurance coverage for device-assisted procedures drives adoption. Combined, these factors make North America the leading market for IABP systems, both in procedural volume and revenue.

Asia Pacific Intra-aortic Balloon Pump Market Trends

The strong growth of the Asia Pacific region in the intra-aortic balloon pump (IABP) market is closely tied to its escalating cardiovascular disease (CVD) burden. In 2019, over half of all global CVD deaths occurred in Asia, rising from 5.6 million in 1990 to 10.8 million in 2019. Furthermore, within this region, CVDs accounted for roughly 40 % of all deaths in the Western Pacific region and nearly 25 % in South East Asia in 2021.

These high and growing rates drive demand for advanced cardiac support devices like IABPs, as greater numbers of acute cardiac events and interventional procedures create the clinical need. At the same time, improving healthcare infrastructure and device adoption in Asia Pacific support faster market uptake compared with mature regions.

Europe Intra-aortic Balloon Pump Market Trends

Europe remains an important market region due to its substantial cardiovascular disease burden, mature healthcare infrastructure, and active inter-hospital collaborations. Annually, about 60,000 - 70,000 cases of cardiogenic shock are diagnosed across Europe. In a pan-European survey including 47,407 patients undergoing percutaneous coronary intervention, 7.9% had STEMI-related cardiogenic shock; only 25% of those received IABP support.

The presence of advanced tertiary cardiac centres, widespread adoption of mechanical circulatory support protocols, and coordinated research networks (e.g., across Germany, France, and the UK) enhances both demand and evidence generation. Consequently, Europe plays a key role in IABP device utilization, product innovation and market growth.

Competitive Landscape

The global intra-aortic balloon pump (IABP) market is growing as hospitals increasingly adopt advanced, image-guided, non-invasive therapies. Key manufacturers focus on precision, targeting accuracy, and real-time monitoring.

Rising cardiovascular disease prevalence, particularly acute heart failure and myocardial infarction, alongside expanding hospital infrastructure and trained specialists in the Asia Pacific and Europe, is boosting adoption. Improved clinical outcomes and supportive government health initiatives further accelerate global market growth.

Key Industry Developments:

- In August 2025, the EU CE-Mark was reinstated for the Cardiosave Intra-Aortic Balloon Pump, allowing the device to resume marketing and distribution across European markets. This regulatory approval confirmed the device met all required safety and performance standards. The reinstatement enabled hospitals and clinicians to continue using the Cardiosave IABP for critical cardiac support, improving patient care in acute heart failure and high-risk cardiac procedures.

- In April 2025, Teleflex received FDA 510(k) clearance for its AC3 Range™ Intra-Aortic Balloon Pump (IABP). This approval allows the company to market and distribute the device in the U.S., enhancing treatment options for patients requiring mechanical circulatory support. The AC3 Range™ IABP is designed to improve hemodynamic support, offering clinicians advanced features for precise cardiac assistance during critical care and surgical procedures.

- In February 2025, Teleflex announced its intent to separate into two independent publicly traded companies. The move aimed to create focused entities, allowing each to concentrate on its core business areas, medical devices and specialty products. The separation was intended to enhance operational efficiency, strategic growth, and shareholder value by enabling more targeted investment and innovation within each new company.

Companies Covered in Intra-aortic Balloon Pump Market

- Teleflex Corporation

- Getinge

- Zeon Corporation

- Tokai Medical Products Inc.

- SENKO MEDICAL INSTRUMENT Mfg. CO., LTD.

- InterValve Inc.

- Insightra Medical, Inc.

- Abiomed Inc.

- Terumo Corporation

- Boston Scientific Corporation

- Edwards Lifesciences Corporation

- Others

Frequently Asked Questions

The global intra-aortic balloon pump market is projected to be valued at US$ 450.2 Mn in 2025.

Rising cardiovascular disease prevalence, increasing cardiac interventions, technological advancements in IABPs, and expanding hospital infrastructure drive the global market.

The global intra-aortic balloon pump market is poised to witness a CAGR of 2.8% between 2025 and 2032.

Expanding healthcare infrastructure in Asia Pacific, growing geriatric population, rising awareness of acute cardiac support, and adoption of advanced IABPs.

Teleflex Corporation, Getinge , Zeon Corporation, Tokai Medical Products Inc., SENKO MEDICAL INSTRUMENT Mfg. CO., LTD., InterValve Inc.