- Medical Devices

- Non-invasive Prenatal Testing (NIPT) Market

Non-invasive Prenatal Testing (NIPT) Market Size, Share, and Growth Forecast, 2025 - 2032

Non-invasive Prenatal Testing (NIPT) Market By Technology (Next-Generation Sequencing (NGS), Others), Application (Trisomy Detection, Microdeletion Detection, Sex Chromosome Aneuploidy Detection, Others), End-user (Diagnostic Laboratories, Others), and Regional Analysis for 2025 - 2032

Non-invasive Prenatal Testing (NIPT) Market Share and Trends Analysis

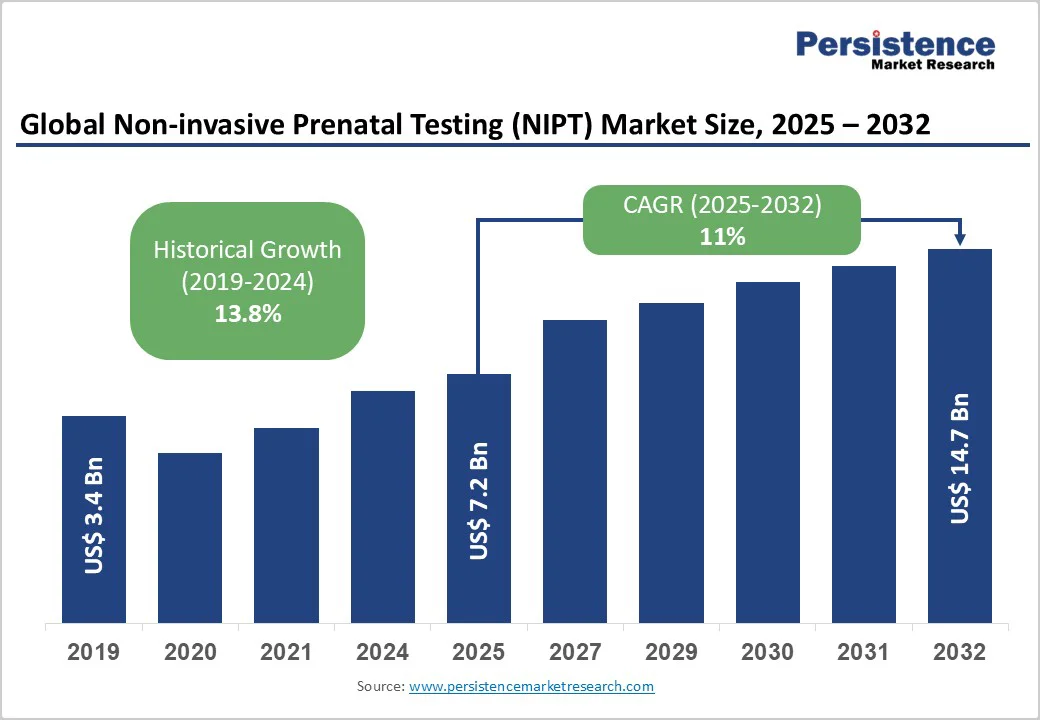

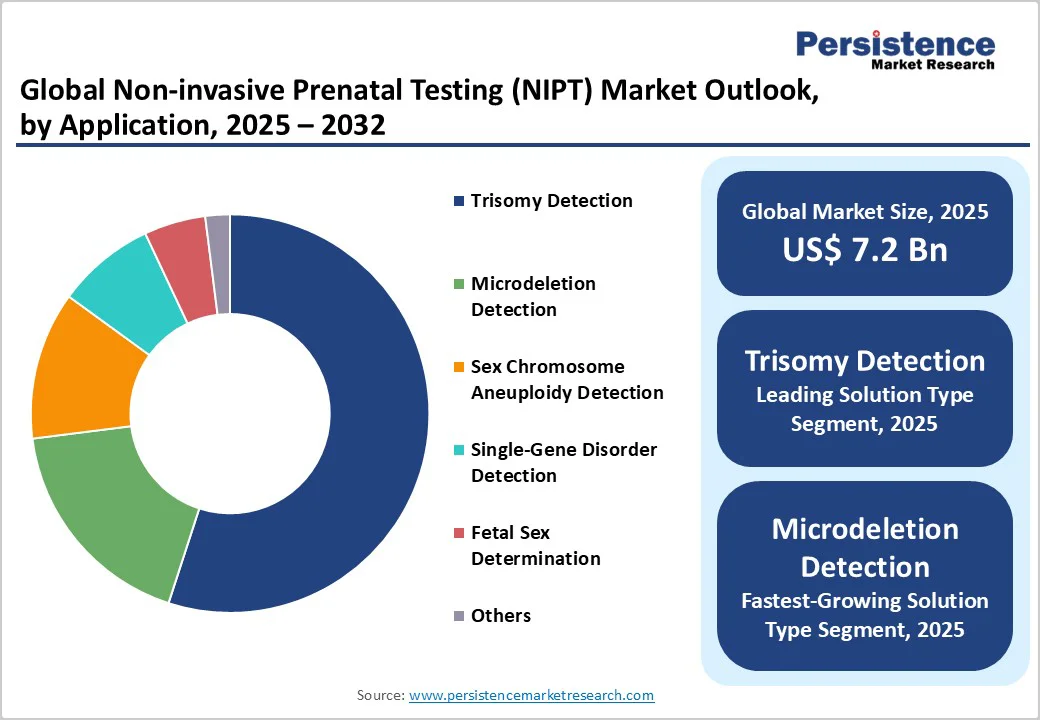

The global non-invasive prenatal testing (NIPT) market size is likely to be valued at US$7.2 Billion in 2025, and is estimated to reach US$14.7 Billion by 2032, growing at a CAGR of 11% during the forecast period 2025 - 2032, driven primarily by an escalating demand for enhanced prenatal diagnostics, spurred by advancements in next-generation sequencing (NGS) technologies, which improve detection accuracy and broaden test applicability.

Expanding reimbursement in key markets, including the U.S. and Europe, is improving accessibility, while rising maternal age worldwide is boosting the test uptake.

The shift from high-risk to universal screening and broader adoption of expanded genetic panels are driving market growth and reshaping competition in prenatal diagnostics.

Key Industry Highlights

- Leading Technology: Next-generation sequencing (NGS) dominates, set to capture approximately 60% of the market share due to its comprehensive genomic coverage, high accuracy, and scalable throughput.

- Leading & Fastest-growing Applications: Trisomy detection is slated to hold about 54% of the NIPT market revenues in 2025, with microdeletion and single-gene panels growing fastest at around 17.5% CAGR during 2025 - 2032.

- Leading & Fastest-growing End-users: Diagnostic laboratories are likely to have approximately 60% share in 2025, while hospitals are expected to grow the fastest at 14% CAGR through 2032.

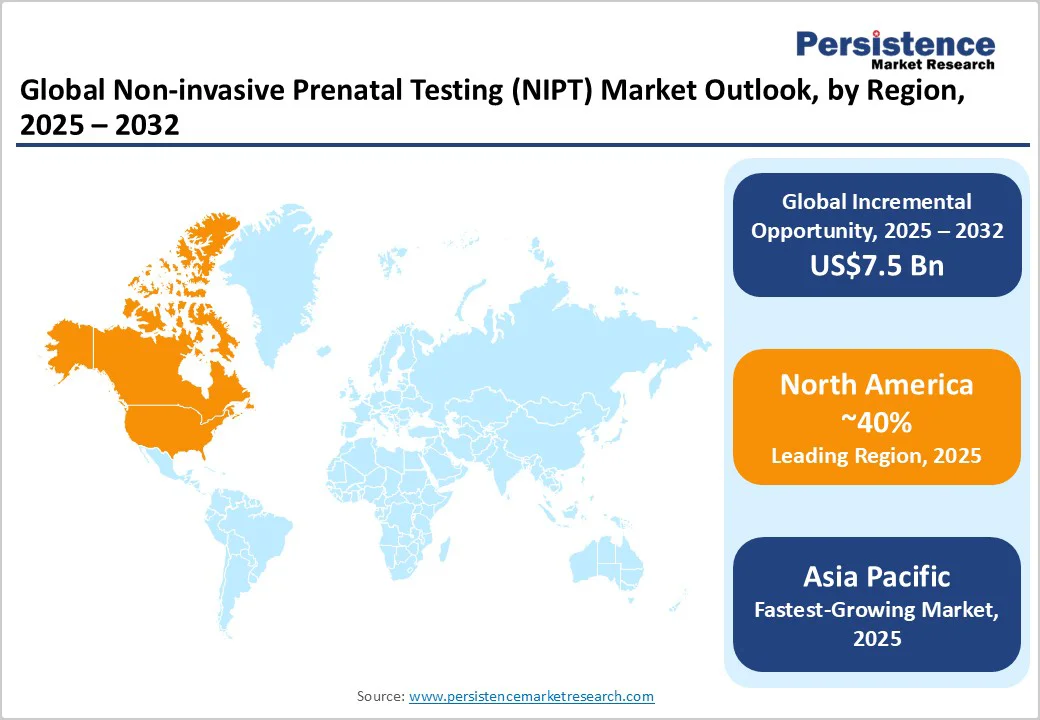

- Dominant Region: North America is set to lead with a 40% market share in 2025 due to favorable reimbursement and innovation ecosystems.

- Fastest-growing Regional Market: Asia Pacific is the fastest-growing regional market with an estimated 15% CAGR during 2025 - 2032, driven by healthcare expansion in China and India.

- Key Constraint: Supply chain and regional regulatory complexities limit scalability in emerging markets, necessitating decentralized procurement strategies and regional partnerships.

| Key Insights | Details |

|---|---|

| Non-invasive Prenatal Testing (NIPT) Market Size (2025E) | US$7.2 Bn |

| Market Value Forecast (2032F) | US$14.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 11% |

| Historical Market Growth (CAGR 2019 to 2024) | 13.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expanding Reimbursement Frameworks Facilitating Broad Adoption

Reimbursement coverage expansion is significantly propelling the NIPT market growth. Regulatory bodies such as the Centers for Medicare & Medicaid Services (CMS) in the U.S. have broadened coverage to include average-risk pregnancies, boosting potential patient pools from approximately 6 million to over 15 million annually. This policy shift has corresponded with an increase in test utilization rates, effectively transforming market economics.

Parallel developments have occurred in Europe, where the inclusion of non-invasive prenatal testing by the National Health Service (NHS) of the U.K. into national antenatal programs has elevated market penetration. These reimbursement advancements have bolstered the capacity of healthcare providers to offer NIPT with minimal out-of-pocket expense, which is pivotal in securing payer buy-in and provider recommendation. Consequently, reimbursement expansions can catalyze investments in technology innovation, genetic counseling services, and partner networks, positioning market participants to capture scalable growth.

Supply Chain Vulnerabilities Constraining Market Scalability in Underserved Regions

Global supply chain constraints, particularly pertaining to proprietary assay reagents and NGS instrument components, pose a critical barrier impacting market scalability. The dependence on a narrow supplier base increases vulnerability to trade policy shifts and pandemic-related challenges, disproportionately affecting emerging and remote markets where procurement agility is limited.

The European Federation of Biotechnology highlights regulatory fragmentation across European Union (EU) member states, further complicating centralized supply fulfillment and increasing direct costs for smaller end-users such as independent clinics. To mitigate these structural headwinds, strategic initiatives including nearshoring production, diversifying supplier portfolios, and strengthening inventory management systems are essential for maintaining operational continuity and supporting anticipated regional expansions in Southeast Asia and Latin America.

Attractive Avenues in Expanded NIPT Panels Addressing High-Value Clinical Needs

The rapid expansion of expanded NIPT panels incorporating microdeletion syndromes and single-gene disorder detection presents a lucrative and actionable market opportunity. Regulatory bodies across the U.S., Germany, and China have recently endorsed the inclusion of syndromes such as DiGeorge (22q11.2 deletion), Cri-du-chat, and monogenic disorders in routine screening panels, thus broadening clinical utility and payer acceptance.

These advanced panels meet growing patient demand for comprehensive assessments and personalize prenatal care by identifying inherited and de novo mutations earlier in pregnancy. Industry leaders are investing substantially in targeted NGS methodologies and AI-powered bioinformatics to enhance detection sensitivity and reporting efficiency, facilitating clinical adoption. This development is enabling integration with genetic counseling services and digital health applications, opening diverse avenues for commercial differentiation, payer engagement, and patient-centric care model innovations.

Category-wise Analysis

Technology Insights

Next-generation sequencing (NGS) continues to dominate the NIPT market landscape, set to command an estimated 60% market share in 2025. This leadership is driven by its superior genomic coverage and ability to deliver comprehensive chromosomal and subchromosomal anomaly detection, making it the preferred technology platform for diagnostic laboratories and specialty prenatal centers.

NGS platforms have demonstrated scalable throughput with reduced turnaround times, supporting large-volume testing that aligns with increasing prenatal screening demands worldwide. The technology has also benefited substantially from declining sequencing costs and enhanced bioinformatics tools, both of which have reinforced accuracy and decreased error rates.

The fastest-growing technology segment in the forecast period from 2025 to 2032 is anticipated to be bioinformatics and data analytics solutions, projected to grow at a CAGR of approximately 18%. This surge is largely attributed to the increasing complexity of genetic data, which demands sophisticated analytical platforms capable of managing large datasets while providing clinically actionable insights.

AI integration is enabling automated variant interpretation, risk stratification, and predictive modeling, thereby reducing human error and accelerating diagnostic workflows. Cloud-based platforms are facilitating data sharing, remote reporting, and real-time monitoring, which have been critically important during periods of healthcare disruption and geographic expansion.

Application Insights

Trisomy detection is likely to hold approximately 55% of the non-invasive prenatal testing market revenue share in 2025. This dominance is underpinned by well-established clinical guidelines endorsing universal screening for trisomies 21, 18, and 13, coupled with high detection sensitivity often exceeding 99%.

Health systems in key markets, including the U.S., the U.K., and Germany, prioritize trisomy screening in their maternal health programs, supported by payer reimbursement and high patient awareness. Clinical emphasis on early detection for better pregnancy management and decision-making reinforces sustained demand within this application area.

Microdeletion and single-gene disorder detection segments are forecast to experience the highest CAGR during 2025 - 2032, reflecting their rapid adoption in clinics and reference labs responding to a growing demand for broader genetic insights.

Technological improvements in targeted sequencing and bioinformatics have enabled earlier and more accurate detection of rare syndromes, such as DiGeorge and Cri-du-chat, which are now being integrated into standard NIPT panels.

Increasing patient-driven demand for comprehensive genetic information and personalized prenatal care is expanding panel offerings, while payers are gradually recognizing the cost-effectiveness of extensive prenatal diagnosis to reduce the long-term burden of genetic disorders.

End-user Insights

Diagnostic laboratories are expected to control the largest market share, estimated at 60% in 2025. The leadership of these facilities is attributable to their economies of scale, established payer contracts, and operational infrastructure capable of processing high test volumes efficiently.

Large reference lab organizations have strengthened their market dominance through strategic acquisitions, capital investments in automated sequencing platforms, and expansion of bundled services, including genetic counseling.

These labs provide essential quality assurances through CLIA and CAP certifications, meeting stringent regulatory and clinical validation standards critical for payer acceptance. Their centralized model facilitates competitive pricing and rapid dissemination of testing services, serving a broad geographic and demographic patient base.

On the other hand, hospitals are anticipated to be the fastest-growing end-users through 2032. This growth is fueled by expanding insurance coverage policies and the integration of non-invasive prenatal testing into routine prenatal care protocols within both public and private hospital systems.

Hospitals leverage their direct patient access and multidisciplinary care coordination to enhance prenatal screening offerings. Investments in hospital-based laboratory infrastructure and specialized clinical teams are enabling faster turnaround and more comprehensive prenatal diagnostics.

Regional Insights

North America Non-invasive Prenatal Testing (NIPT) Market Trends

At about 40%, North America is set to dominate the non-invasive prenatal testing market share in 2025, largely driven by the United States, which alone captures more than a third of the global market.

This dominance is supported by a robust reimbursement framework, notably the expansion of CMS coverage to include average-risk pregnancies, increasing the potential test pool sizably. The U.S. regulatory environment is characterized by rigorous oversight by the Food and Drug Administration (FDA) for genetic test validation and an active innovation ecosystem that fosters rapid technology adoption.

Increased maternal age and strategic collaborations between diagnostic firms and healthcare providers to embed NIPT into gestational care pathways are also playing a major role in regional market growth. Competitive positioning is contingent on investments in AI-powered diagnostics and data management platforms.

Regulatory harmonization efforts between the FDA and CMS are also streamlining market entry for novel tests, while investment focus remains on infrastructure upgrades and geographic expansion within rural U.S., where testing is currently underpenetrated.

Europe Non-invasive Prenatal Testing (NIPT) Market Trends

Europe is projected to hold approximately 30% of the NIPT market share by 2025, with Germany, the U.K., France, and Spain contributing heavily. The high adoption rates in Germany and the U.K. are a result of targeted public health initiatives, widespread payer acceptance, and population screening programs. Regulatory harmonization efforts through bodies such as G-BA and NICE have promoted greater standardization of reimbursement policies and clinical practice guidelines, which are positively influencing volume growth.

Multinational test providers have been known to collaborate closely with regional labs and academic institutions to validate novel NIPT panels and enhance service offerings. The regional market benefits from well-established supply chains and a strong emphasis on robust clinical evidence generation. Investment trends highlight digital transformation initiatives, particularly the integration of genetic counseling platforms with laboratory information systems. Market growth is further supported by an increased uptake in Eastern European countries seeking to close diagnostic gaps through government funding programs.

Asia Pacific Non-invasive Prenatal Testing (NIPT) Market Trends

Asia Pacific is slated to be the fastest-growing regional market for non-invasive prenatal testing, expected to expand at a CAGR of about 15% from 2025 to 2032, and secure approximately 22% of the global market by 2025. China is the principal driver with proactive regulatory reforms by the National Medical Products Administration (NMPA), government incentives promoting indigenous technology manufacturing, and aggressive use of AI to improve sequencing accuracy and throughput in metropolitan hospitals.

Market growth in Japan is propelled by clinical trial validations supporting early NIPT adoption, while in India, it is being driven through public-private partnerships and tiered pricing strategies targeting urban and peri-urban hospitals. ASEAN countries are accelerating adoption facilitated by healthcare infrastructure investments and regional capacity-building initiatives.

The regional competitive environment features both domestic leaders and multinational entrants capitalizing on the cost advantages of manufacturing and scaling operations. Investment flows prioritize lab infrastructure build-out in tier-two and tier-three cities, supply chain optimization, and integration of tele-genetic counseling services to broaden prenatal care access. Regulatory convergence with World Health Organization (WHO) standards is enhancing cross-border market integration and investor confidence.

Competitive Landscape

The global non-invasive prenatal testing (NIPT) market exhibits a moderately consolidated structure, headlined by top firms including Illumina, Natera, Roche, LabCorp, Quest Diagnostics, and Eurofins Scientific. High entry barriers stem from intensive R&D investment, regulatory compliance, and payer relationships, creating a competitive moat for incumbent players.

While consolidation is prevalent at the global level, fragmentation persists regionally due to localized testing providers, emerging technology vendors, and bespoke clinical service models.

Competitive strategies focus on integrating proprietary consumables with sophisticated bioinformatics, expanding genetic counseling offerings, and geographic expansion to emerging markets. The landscape is also shaped by strategic acquisitions and alliances that aim to leverage multi-omic data integration and enhance service comprehensiveness, effectively positioning these firms as preferred partners in the prenatal diagnostics ecosystem.

Key Industry Developments

- In August 2025, Natera launched Fetal Focus, a new noninvasive prenatal test that screens fetal DNA from maternal blood for cystic fibrosis and three other inherited single-gene conditions, achieving over 90% accuracy in preliminary trials. This test is especially useful when the baby's father is unavailable for genetic testing. Supported by the EXPAND trial involving about 1,300 pregnant women, Fetal Focus detects recessive conditions such as cystic fibrosis, spinal muscular atrophy, and hemoglobinopathies, providing critical prenatal information without invasive procedures.

- In June 2025, NHS England announced plans to introduce universal DNA screening for all newborns in England in order to assess risk factors for hundreds of diseases and conditions. The initiative, which leverages genomic sequencing and AI analytics, aims to shift healthcare from reactive treatment to preventative intervention. The program has been described as a major step in public-health strategy, though critics raise concerns about consent, data security, oversight, and potential psychological impacts of early genetic risk labelling.

- In February 2025, an article in Nature revealed that researchers successfully treated a child in utero for the first time for the rare genetic motor-neuron disorder spinal muscular atrophy Type 1 by administering a gene-targeting drug to the fetus during late pregnancy. Now nearly three years old, the child shows no signs of the condition, which is often fatal in early infancy. The intervention marks a milestone in prenatal gene therapy, raising hopes for earlier treatment of inherited neuromuscular diseases and prompting broader discussions about fetal medicine, long-term monitoring, and patient-selection criteria.

Companies Covered in Non-invasive Prenatal Testing (NIPT) Market

- Illumina, Inc.

- Natera, Inc.

- F. Hoffmann-La Roche Ltd.

- Laboratory Corporation of America Holdings (LabCorp)

- Quest Diagnostics Incorporated

- Eurofins Scientific

- BGI Genomics Co., Ltd.

- Myriad Genetics, Inc.

- PerkinElmer, Inc.

- Thermo Fisher Scientific Inc.

- Annoroad Gene Technology Co., Ltd.

- Berry Genomics Co., Ltd.

- Agilent Technologies, Inc.

- Ariosa Diagnostics, Inc.

- Invitae Corporation

Frequently Asked Questions

The non-invasive prenatal testing (NIPT) market size is projected to reach US$7.2 Billion in 2025.

Heightening demand for enhanced prenatal diagnostics and rapid advancements in next-generation sequencing (NGS) technologies are driving the market.

The non-invasive prenatal testing (NIPT) is poised to witness a CAGR of 11% from 2025 to 2032.

Widening reimbursement policies in key markets, rising average maternal age globally, the transition from high-risk to universal pregnancy screening protocols, and growing clinical adoption of expanded genetic panels are key market opportunities.

Illumina, Natera, and F. Hoffmann-La Roche are some of the key players in the non-invasive prenatal testing (NIPT) market.