- Executive Summary

- Global Software Defined Security Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Manufacturing sector Outlook

- Global IT Spending Overview

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 – 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Software Defined Security Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Global Software Defined Security Market Outlook: Component Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Component Type, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Component Type, 2026-2033

- Software

- Services

- Market Attractiveness Analysis: Component Type

- Global Software Defined Security Market Outlook: Deployment Mode

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Deployment Mode, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Deployment Mode, 2026-2033

- On-Premises

- On-Premises

- Hybrid

- Market Attractiveness Analysis: Deployment Mode

- Global Software Defined Security Market Outlook: Security Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Security Type, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Security Type, 2026-2033

- Network Security

- Cloud Security

- Application Security

- Endpoint Security

- Identity & Access Management (IAM)

- Market Attractiveness Analysis: Security Type

- Global Software Defined Security Market Outlook: End Use Industry

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by End Use Industry, 2020-2025

- Current Market Size (US$ Bn) Forecast, by End Use Industry, 2026-2033

- BFSI

- Government & Defense

- Healthcare & Life Sciences

- IT & Telecom

- Manufacturing & Industrial

- Misc.

- Market Attractiveness Analysis: End Use Industry

- Global Software Defined Security Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Software Defined Security Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) Forecast, by Component Type, 2026-2033

- Software

- Services

- North America Market Size (US$ Bn) Forecast, by Deployment Mode, 2026-2033

- On-Premises

- On-Premises

- Hybrid

- North America Market Size (US$ Bn) Forecast, by Security Type, 2026-2033

- Network Security

- Cloud Security

- Application Security

- Endpoint Security

- Identity & Access Management (IAM)

- North America Market Size (US$ Bn) Forecast, by End Use Industry, 2026-2033

- BFSI

- Government & Defense

- Healthcare & Life Sciences

- IT & Telecom

- Manufacturing & Industrial

- Misc.

- Europe Software Defined Security Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) Forecast, by Component Type, 2026-2033

- Software

- Services

- Europe Market Size (US$ Bn) Forecast, by Deployment Mode, 2026-2033

- On-Premises

- On-Premises

- Hybrid

- Europe Market Size (US$ Bn) Forecast, by Security Type, 2026-2033

- Network Security

- Cloud Security

- Application Security

- Endpoint Security

- Identity & Access Management (IAM)

- Europe Market Size (US$ Bn) Forecast, by End Use Industry, 2026-2033

- BFSI

- Government & Defense

- Healthcare & Life Sciences

- IT & Telecom

- Manufacturing & Industrial

- Misc.

- East Asia Software Defined Security Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) Forecast, by Component Type, 2026-2033

- Software

- Services

- East Asia Market Size (US$ Bn) Forecast, by Deployment Mode, 2026-2033

- On-Premises

- On-Premises

- Hybrid

- East Asia Market Size (US$ Bn) Forecast, by Security Type, 2026-2033

- Network Security

- Cloud Security

- Application Security

- Endpoint Security

- Identity & Access Management (IAM)

- East Asia Market Size (US$ Bn) Forecast, by End Use Industry, 2026-2033

- BFSI

- Government & Defense

- Healthcare & Life Sciences

- IT & Telecom

- Manufacturing & Industrial

- Misc.

- South Asia & Oceania Software Defined Security Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Component Type, 2026-2033

- Software

- Services

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Deployment Mode, 2026-2033

- On-Premises

- On-Premises

- Hybrid

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Security Type, 2026-2033

- Network Security

- Cloud Security

- Application Security

- Endpoint Security

- Identity & Access Management (IAM)

- South Asia & Oceania Market Size (US$ Bn) Forecast, by End Use Industry, 2026-2033

- BFSI

- Government & Defense

- Healthcare & Life Sciences

- IT & Telecom

- Manufacturing & Industrial

- Misc.

- Latin America Software Defined Security Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) Forecast, by Component Type, 2026-2033

- Software

- Services

- Latin America Market Size (US$ Bn) Forecast, by Deployment Mode, 2026-2033

- On-Premises

- On-Premises

- Hybrid

- Latin America Market Size (US$ Bn) Forecast, by Security Type, 2026-2033

- Network Security

- Cloud Security

- Application Security

- Endpoint Security

- Identity & Access Management (IAM)

- Latin America Market Size (US$ Bn) Forecast, by End Use Industry, 2026-2033

- BFSI

- Government & Defense

- Healthcare & Life Sciences

- IT & Telecom

- Manufacturing & Industrial

- Misc.

- Middle East & Africa Software Defined Security Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) Forecast, by Component Type, 2026-2033

- Software

- Services

- Middle East & Africa Market Size (US$ Bn) Forecast, by Deployment Mode, 2026-2033

- On-Premises

- On-Premises

- Hybrid

- Middle East & Africa Market Size (US$ Bn) Forecast, by Security Type, 2026-2033

- Network Security

- Cloud Security

- Application Security

- Endpoint Security

- Identity & Access Management (IAM)

- Middle East & Africa Market Size (US$ Bn) Forecast, by End Use Industry, 2026-2033

- BFSI

- Government & Defense

- Healthcare & Life Sciences

- IT & Telecom

- Manufacturing & Industrial

- Misc.

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Palo Alto Network

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Intel Corporation

- EMC

- Hewlett Packard Enterprises

- Catbird

- Symantec

- Cisco Systems

- Fortinet

- Vmware

- Palo Alto Network

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Hardware & Software IT Services

- Software Defined Security Market

Software Defined Security Market Size, Share, and Growth Forecast, 2026 - 2033

Software Defined Security Market by Component Type (Software, Services), Deployment Mode (On-Premises, Cloud-Based, Hybrid), Deployment Mode (Cloud-Based, On-Premises), Security Type (Network Security, Cloud Security, Application Security, Endpoint Security, Identity & Access Management (IAM), End Use Industry (BFSI, Government & Defense, Healthcare & Life Sciences, IT & Telecom, Manufacturing & Industrial, Misc.) and Regional Analysis for 2026 - 2033

Software Defined Security Market Size and Trends Analysis

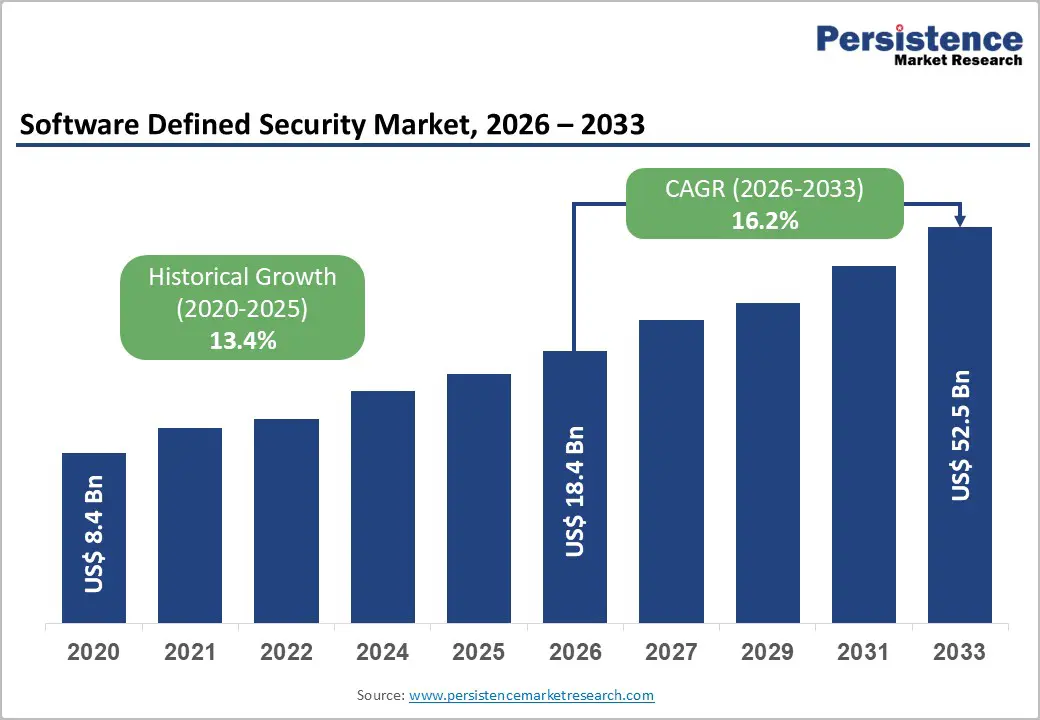

The global software-defined security market size was valued at US$ 18.4 billion in 2026 and is projected to reach US$ 52.5 billion by 2033, growing at a CAGR of 16.2% between 2026 and 2033. This substantial expansion is driven by the transition from hardware-centric security architectures to software-based, programmable security frameworks that provide centralized policy management, automated threat response, and seamless scalability across distributed IT environments.

The market's momentum reflects the critical need for agile security solutions addressing cloud migration, network virtualization, zero-trust implementation, and the proliferation of software-defined infrastructure across enterprises. As financial institutions, telecommunications operators, and government agencies adopt software-defined networking (SDN) and network functions virtualization (NFV), organizations are prioritizing programmable security platforms that deliver unified visibility, dynamic policy enforcement, and automated security orchestration across hybrid and multi-cloud environments.

Key Industry Highlights:

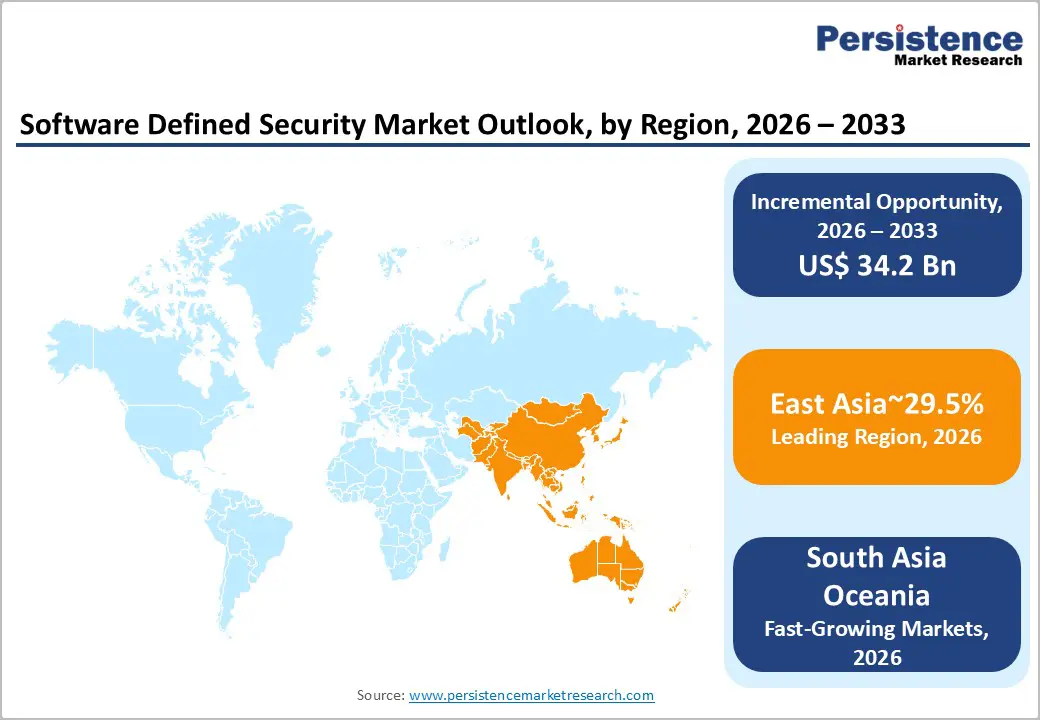

- Regional Leadership: East Asia leads the global Software-Defined Security Market with 29.5% share, supported by accelerating 5G deployments, telecom network virtualization, and large-scale digital infrastructure modernization.

- Strong North American Presence: North America holds 21% share, driven by strong cybersecurity spending, zero-trust adoption, cloud migration, and the presence of leading SDS technology vendors.

- High-Growth European Market: Europe accounts for 23% share and continues expanding due to strict data protection regulations, secure multi-cloud adoption, and enterprise digital transformation initiatives.

- Leading Component Segment: The Software segment dominates with 58.4% share, enabled by shifts toward programmable security controls, NFV/SDN integration, and centralized policy orchestration.

- Fastest-Growing Component Segment: The Services segment is the fastest-growing, driven by consulting, implementation, managed security, and integration services that support complex cloud-first and hybrid architectures.

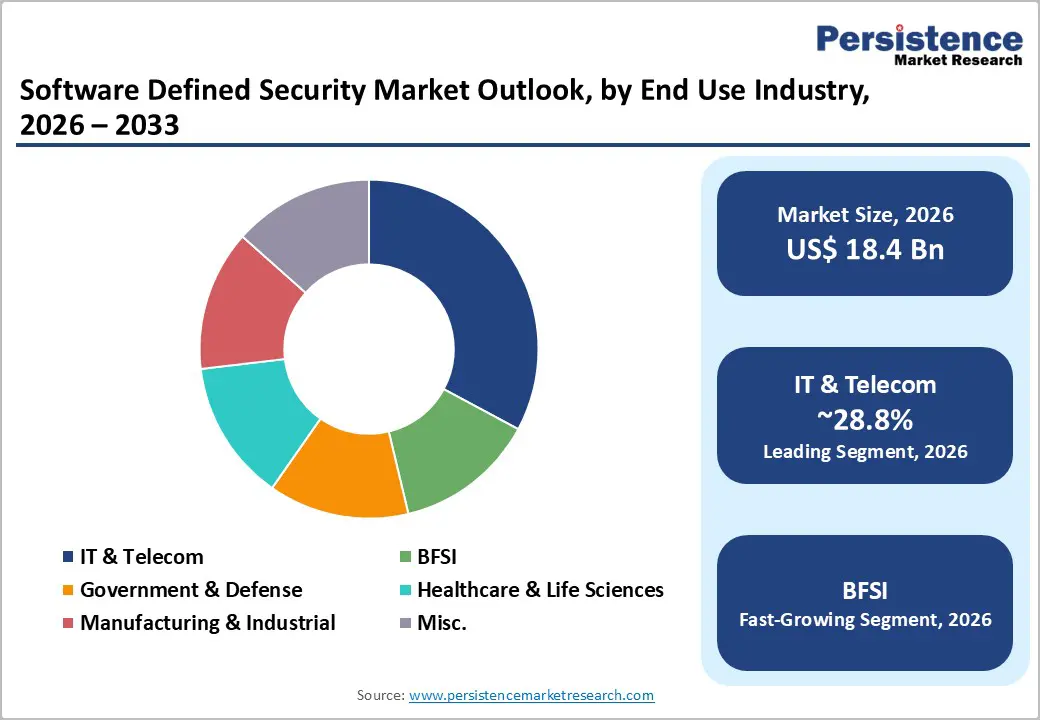

- Leading End-Use Sector: IT & Telecom leads with 28.8% share, reflecting heavy reliance on virtualized network functions, private 5G rollouts, SDN/NFV adoption, and automated cybersecurity policy enforcement.

| Report Attribute | Details |

|---|---|

|

Software Defined Security Market Size (2026E) |

US$ 18.4 Bn |

|

Market Value Forecast (2033F) |

US$ 52.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

16.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

13.4% |

Market Dynamics

Growth Drivers

Telecommunications Infrastructure Modernization and 5G Network Deployment

The rapid modernization of telecommunications infrastructure and deployment of 5G networks fundamentally drives the Global Software Defined Security Market as operators transition from proprietary hardware appliances to virtualized, software-based security functions protecting complex network architectures. India's telecom sector exemplifies this transformation, with a subscriber base of 1.21 billion and tele-density of 86.09 PERCENT as of June 2025, while internet subscribers reached 979 million. Broadband adoption accelerated sharply over the last decade, expanding from 149.75 million connections in 2016 to 979 million in 2025, supported by 4G and rapidly expanding 5G networks, with 5G already contributing nearly a quarter of total wireless data usage in FY25.

Gross telecom revenue rose from US$ 39.22 billion in FY24 to US$ 43.42 billion in FY25, with cumulative FDI inflows reaching US$ 40.07 billion between April 2000 and March 2025. According to ITU estimates, global internet usage expanded rapidly, reaching around 6 billion users in 2025, up from 60 percent in 2020, with nearly 1.3 billion people coming online between 2020 and 2025. This unprecedented connectivity expansion, combined with large-scale 5G rollouts, fibre expansion under BharatNet, rising tower fibreisation, and data consumption surges, necessitates software-defined security architectures enabling dynamic policy enforcement, automated threat detection, and centralized security management across virtualized network functions, substantially benefiting the Global Software Defined Security Market.

Financial Services Digital Asset Protection and Regulatory Compliance

The exponential growth and digitalization of financial services sectors globally create critical demand for software-defined security architectures protecting increasingly valuable digital assets while ensuring regulatory compliance across complex, distributed financial systems. India's banking, financial services, and insurance (BFSI) sector expanded 50 times in market capitalization to reach US$1 trillion in 2025, now contributing 27 percent to the country's GDP.

Life insurance AUM reached US$ 693 billion and mutual fund AUM rose to US$ 844 billion by March 2025, with gross NPAs falling from 5.8 percent in FY22 to 2.2 percent in FY25 and credit costs reducing from 1.3 percent to 0.4 percent.

The European financial and insurance activities sector generated €0.9 trillion in value added in 2022 and employed nearly 5 million people across almost 867,000 enterprises, while the European banking sector held total assets of €43.6 trillion in 2023, with loans outstanding at €26.8 trillion and deposits at €17.3 trillion.

China's banking and insurance sectors demonstrated robust growth, with total banking assets reaching RMB 467.3 trillion, up 7.9 percent year-on-year as of Q2 2025, and insurance assets growing 9.2 percent to RMB 39.2 trillion. This massive financial asset concentration, combined with digital transformation initiatives, real-time payment systems like Brazil's PIX, and the transition from legacy systems to API-first architectures, necessitates programmable security frameworks enabling automated policy enforcement, dynamic threat response, and centralized security orchestration across distributed financial ecosystems, driving sustained demand within the Global Software Defined Security Market.

Market Restraining Factors

Organizational Skill Gaps and Software-Defined Security Expertise Deficiencies

The shortage of cybersecurity professionals with specialized expertise in software-defined networking, security automation, policy orchestration, and programmable security architectures constrains market adoption and implementation effectiveness. The information and communication services sector in the EU, which generated approximately €667 billion in value added and employed nearly 7.2 million people in 2022, demonstrates high productivity with apparent labour productivity reaching €92,800 per person employed, yet faces persistent talent competition for specialized software-defined security roles.

Organizations struggle to recruit personnel capable of designing, implementing, and managing software-defined security environments that integrate network virtualization, security orchestration, automated policy enforcement, and dynamic threat response mechanisms, limiting adoption rates particularly among enterprises lacking established DevSecOps practices or security automation capabilities.

Key Market Opportunities

Private 5G Networks and Enterprise Wireless Security Requirements

The deployment of private 5G networks across industrial, manufacturing, healthcare, and enterprise environments presents transformative opportunities for the global software-defined security market by enabling comprehensive protection of mission-critical wireless infrastructure, edge computing environments, and distributed IoT ecosystems. On February 26, 2024, Palo Alto Networks launched end-to-end Private 5G security solutions in collaboration with partners including Celona, NVIDIA, and NTT DATA, enabling organizations to deploy, manage, and secure private 5G networks while integrating AI, Zero Trust, and software-defined security capabilities to protect mission-critical traffic and distributed cloud-native environments.

India's telecom sector's rapid expansion, with wireless services accounting for over 96% of total subscriptions led by Reliance Jio and Bharti Airtel, and data consumption surging with 5G contributing nearly a quarter of total wireless data usage, demonstrates the scale of wireless infrastructure requiring protection. The European defence industry's turnover of €183.4 billion in 2024, reflecting a 13.8 percent year-on-year increase, includes substantial investments in secure communications infrastructure and operational technology networks.

Private 5G networks enable ultra-reliable low-latency communications for industrial automation, remote healthcare, smart manufacturing, and critical infrastructure operations, each requiring software-defined security architectures providing network slicing security, edge security orchestration, zero-trust network access, and automated threat response capabilities protecting distributed wireless environments, creating substantial addressable opportunities within the Global Software Defined Security Market.

Quantum-Resistant Security Architecture Deployment

The emergence of quantum computing threats and the critical need for quantum-resistant cryptographic protection create significant opportunities for the Global Software Defined Security Market through the deployment of post-quantum cryptography, quantum-safe communications, and adaptive security architectures, preparing enterprises for the post-quantum computing era.

On August 14, 2025, Palo Alto Networks launched enterprise-wide quantum security readiness solutions, including next-generation software firewalls, Secure Access Service Edge (SASE) enhancements, and quantum-optimized hardware, providing organizations with automated, scalable, and AI-driven protections across multicloud environments, strengthening software-defined security and zero-trust architectures.

Financial services sectors managing massive digital assets, with China's banking assets reaching RMB 467.3 trillion and European banking assets totaling €43.6 trillion, face critical quantum computing threats to the cryptographic systems that protect transaction integrity, customer data, and regulatory compliance. Defense and aerospace sectors, with the U.S. A&D industry generating $995 billion in total business activity and European A&D achieving €325.7 billion turnover, require quantum-resistant security protecting classified information, command and control systems, and strategic communications infrastructure.

Organizations implementing quantum-ready software-defined security architectures can proactively address quantum computing threats, ensure cryptographic agility enabling rapid algorithm updates, and maintain security effectiveness as quantum computing capabilities advance, positioning quantum security as a critical growth opportunity within the Global Market.

Category-wise Analysis

Component Type Insights

Software dominates the global software-defined security market, with 58.4% market share in 2026, reflecting a fundamental shift from hardware-based security appliances to programmable, virtualized security functions delivered through software platforms. This segment encompasses security orchestration platforms, virtual firewall software, software-defined perimeter solutions, network security virtualization, and cloud-native security applications enabling centralized policy management, automated threat response, and seamless scalability across distributed environments.

The software segment's leadership position stems from the transition to cloud-native architectures, containerized application deployments, and microservices-based software development, all of which require programmable security controls integrated into DevSecOps workflows. On June 10, 2025, Cisco announced advancements in its Software Defined Security approach with the Hybrid Mesh Firewall and Universal Zero Trust Network Access (ZTNA), integrating zero-trust, AI workload protection, and enhanced policy management into the network to secure hybrid and AI-driven environments. Organizations adopting software-defined security platforms benefit from reduced hardware dependencies, simplified security policy deployment, and enhanced agility responding to evolving threat landscapes through automated software updates and policy modifications.

Services represent the fastest-growing component of the Global Software Defined Security Market, encompassing professional consulting, implementation support, security orchestration services, managed security operations, and continuous optimization services that address the complexity of transitioning from traditional to software-defined security architectures. The services segment's rapid expansion reflects the specialized expertise required to design software-defined security frameworks, integrate programmable security controls with existing infrastructure, and optimize security automation workflows.

End Use Industry Insights

IT & Telecommunications commands the largest end-user share of the Global Software Defined Security Market at 28.8% in 2026, reflecting the sector's fundamental reliance on software-defined networking, network function virtualization, and programmable infrastructure that require comprehensive security integration. Telecommunications operators pioneered software-defined networking adoption, transitioning from proprietary hardware to virtualized network functions enabling dynamic service provisioning, automated network management, and cost-optimized infrastructure operations.

Banking, Financial Services, and Insurance (BFSI) is the fastest-growing end-user segment in the software-defined security market, driven by accelerated digital transformation, real-time payment system deployments, cloud migration initiatives, and stringent regulatory compliance requirements that require programmable, centralized security architectures. The sector's rapid adoption reflects the critical need for dynamic security policy enforcement, automated threat response, and unified security management across increasingly distributed financial services ecosystems.

Regional Insights and Trends

North America Market Trend

North America represents 21% of the software-defined security market, characterized by advanced software-defined networking adoption, mature cybersecurity markets, substantial enterprise cloud migration, and concentrated presence of leading software-defined security vendors and sophisticated early-adopter customers. The region benefits from established zero-trust security frameworks, widespread adoption of security orchestration platforms, and proactive investment in next-generation security architectures supporting hybrid and multi-cloud environments.

On January 7, 2025, Intel introduced its Adaptive Control Unit (ACU U310) and whole-vehicle platform at CES 2025, accelerating software-defined vehicle innovation by consolidating multiple real-time, safety-critical, and cybersecure functions into a single chip, demonstrating North America's leadership in software-defined technology development. On August 14, 2025, Palo Alto Networks launched enterprise-wide quantum security readiness solutions, including next-generation software firewalls and SASE enhancements, providing organizations with automated, scalable, and AI-driven protections across multicloud environments.

North America's competitive landscape features established software-defined security platforms, robust venture capital supporting security automation innovation, collaborative partnerships between cloud providers and security vendors, and sophisticated enterprise customers driving demand for advanced software-defined security capabilities, positioning the region for continued innovation leadership and strong market growth through advanced threat protection, security automation, and quantum-resistant security deployments.

East Asia Market Trend

East Asia dominates the software-defined security market with a 29.5% share, driven by massive telecommunications infrastructure investments, rapid 5G deployment, substantial financial services digitalization, and government-led initiatives promoting software-defined networking and network function virtualization across critical infrastructure sectors. The region's market leadership reflects strategic emphasis on technology sovereignty, domestic platform development, and comprehensive protection of software-defined infrastructure supporting digital economy initiatives.

According to ITU estimates, global internet usage reached around 6 billion users in 2025, with Asia-Pacific accounting for a substantial share of this growth. The region's telecommunications modernization, combined with smart city initiatives, industrial IoT deployments, and cloud computing adoption across manufacturing, finance, and government sectors, creates substantial demand for software-defined security solutions.

East Asia's competitive advantages include government support for indigenous software-defined networking platforms, substantial R&D investments in network virtualization technologies, collaborative ecosystems connecting telecommunications operators with security vendors, and strategic initiatives promoting software-defined infrastructure across critical sectors, positioning the region for sustained market leadership through comprehensive digitalization initiatives and technology localization strategies through 2033.

Europe Market Trend

Europe accounts for 23% of the software-defined security market, supported by stringent cybersecurity regulations, comprehensive data protection frameworks, collaborative defense initiatives, and mature telecommunications infrastructure undergoing extensive virtualization and software-defined networking transitions. The region's market characteristics reflect strong regulatory enforcement, technology-sovereignty priorities, and established partnerships among telecommunications operators, financial institutions, and software-defined security providers.

The European financial and insurance sector generated €0.9 trillion in value added and employed nearly 5 million people across almost 867,000 enterprises in 2022, demonstrating high productivity with a wage-adjusted labor productivity ratio of 236.1 percent. The European banking sector held total assets of €43.6 trillion in 2023, with loans outstanding at €26.8 trillion and deposits at €17.3 trillion, undergoing structural transformation with the number of credit institutions falling to 5,304, driven by digitalization and efficiency-focused restructuring. This consolidation accelerates adoption of software-defined security architectures enabling centralized policy management, automated compliance monitoring, and unified security operations across multi-bank networks.

Competitive Landscape

The global software-defined security (SDS) market is consolidated in nature, dominated by a few leading players offering comprehensive and integrated solutions for network security, zero trust, and AI-driven threat mitigation. Palo Alto Networks holds a strong position with its next-generation firewalls, private 5G security offerings, and cloud-native SDS capabilities, catering to enterprises across multiple verticals. Cisco Systems leverages its Hybrid Mesh Firewall and Universal ZTNA solutions, embedding security into network infrastructure while integrating AI-powered detection and response, reinforcing its market leadership.

Intel Corporation drives innovation in software-defined security for automotive and industrial applications through adaptive control units and secure compute platforms. Symantec focuses on enterprise-grade endpoint and network security, enhancing its SDS portfolio with integrated management consoles and authentication services.

Key Industry Developments

- On August 14, 2025, Palo Alto Networks launched enterprise-wide quantum security readiness solutions, including next-generation software firewalls, Secure Access Service Edge (SASE) enhancements, and quantum-optimized hardware, providing organizations with automated, scalable, and AI-driven protections across multicloud environments, strengthening software-defined security and zero-trust architectures.

- On June 10, 2025, Cisco announced advancements in its Software Defined Security approach with the Hybrid Mesh Firewall and Universal Zero Trust Network Access (ZTNA), integrating zero-trust, AI workload protection, and enhanced policy management into the network to secure hybrid and AI-driven environments.

Companies Covered in Software Defined Security Market

- Palo Alto Network

- Intel Corporation

- EMC

- Hewlett Packard Enterprises

- Catbird

- Symantec

- Cisco Systems

- Fortinet

- Vmware

- SANS Institute

Frequently Asked Questions

The global Software Defined Security Market is projected to be valued at US$ 18.4 Bn in 2026.

The BFSI segment is expected to account for approximately 26.3% of the Global Software Defined Security Market by End Use Industry in 2026.

The market is expected to witness a CAGR of 16.2% from 2026 to 2033.

The Software Defined Security Market is driven by rapid telecom modernization and 5G deployment, rising digital financial assets, and growing regulatory compliance needs across highly connected digital ecosystems.

Key opportunities in the Software Defined Security Market stem from private 5G network deployments and emerging quantum-resistant security architectures enabling secure, programmable, and future-proof protection for distributed enterprise environments.

Key players in the Software-Defined Security Market include Palo Alto Networks, Cisco Systems, VMware, Fortinet, Hewlett Packard Enterprise (HPE), and Symantec.