- Technology

- Digital Textile Printing Market

Digital Textile Printing Market Size, Share, and Growth Forecast, 2025 - 2032

Digital Textile Printing Market by Printing Technology (Direct-to-Fabric (DTF) / Direct-to-Garment (DTG), Sublimation / Dye-Sublimation, Reactive Ink Printing, Pigment Ink Printing, Acid Ink Printing, and Other Technologies), Ink Type ( Reactive Ink, Acid Ink, Disperse Ink / Sublimation Ink, Pigment Ink, and Other Specialty Inks.), Fabric Type, Application and Regional Analysis for 2025 - 2032

Digital Textile Printing Market Size and Trends Analysis

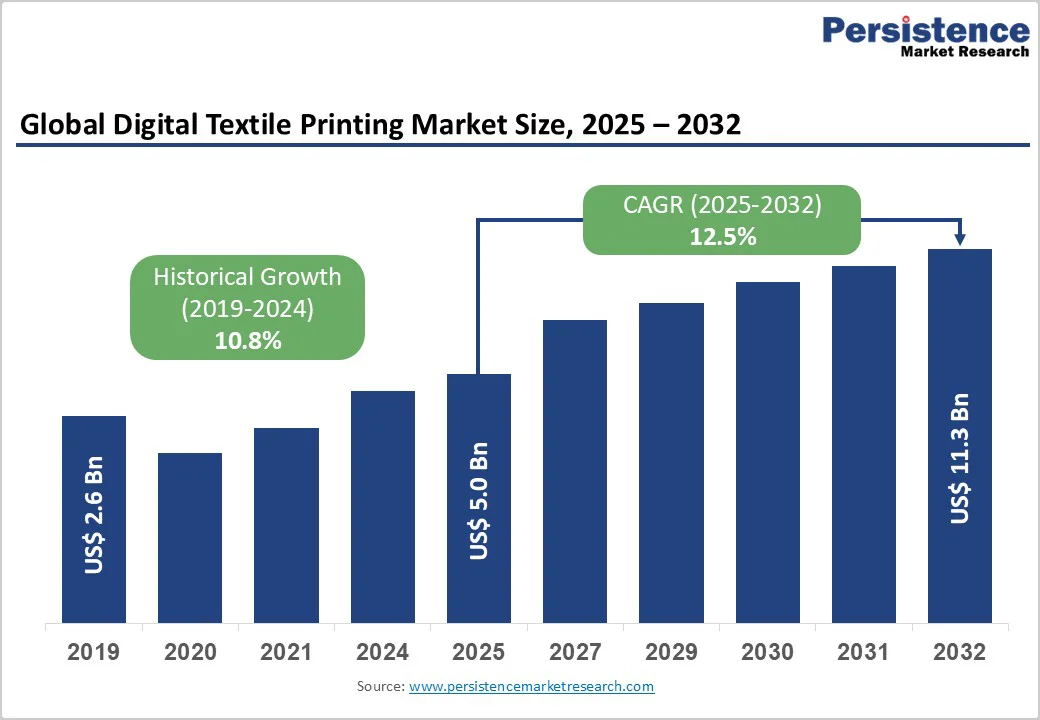

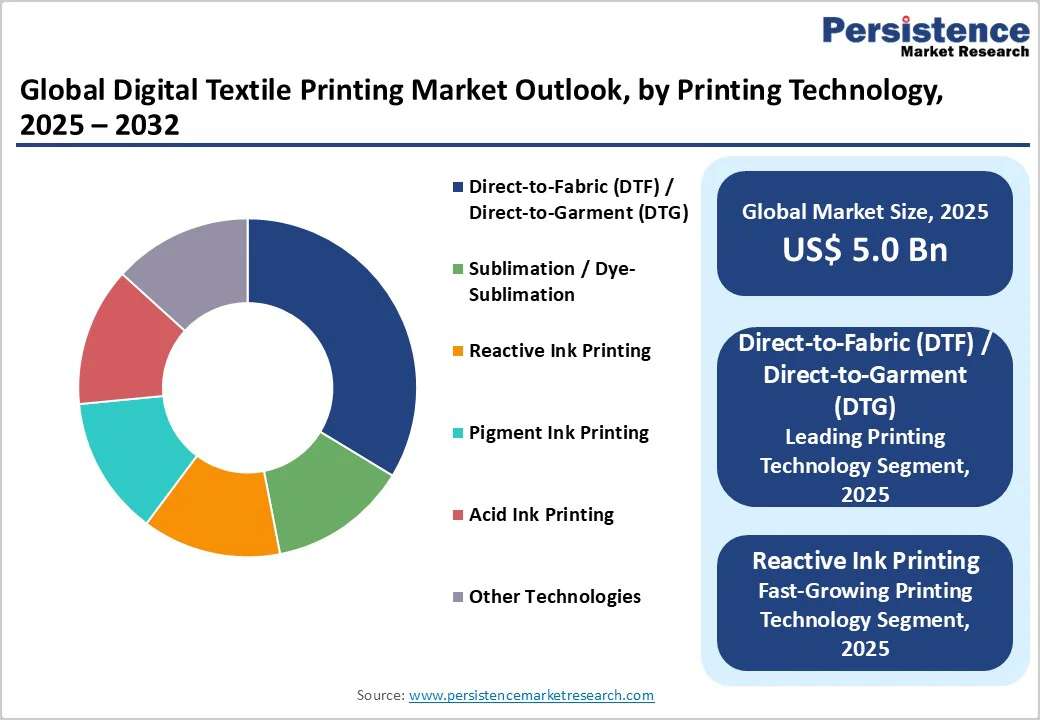

The global digital textile printing market size is likely to value at US$ 5.0 billion in 2025 and is projected to reach US$ 11.3 billion, growing at a CAGR of 12.5% between 2025 and 2032.

The acceleration in growth momentum is driven by technological convergence in digital printing hardware, increasing adoption of sustainable production methodologies, and the fundamental restructuring of textile supply chains toward on-demand manufacturing models.

Key Industry Highlights:

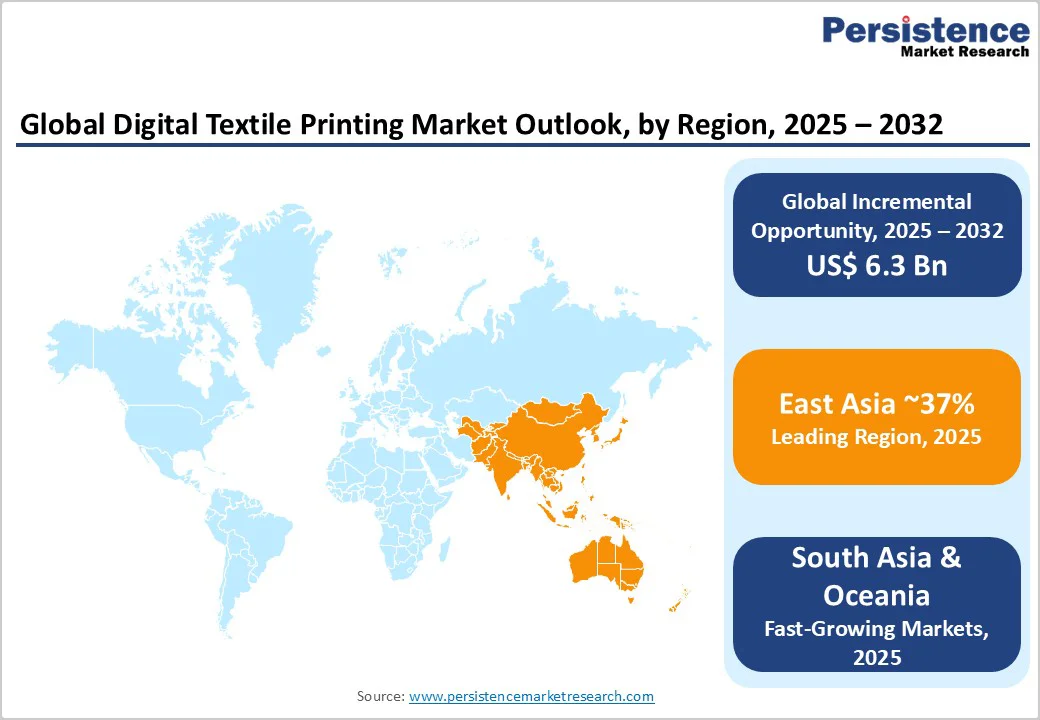

- East Asia dominated the global digital textile printing market with a 37% share in 2025, driven by China’s large-scale textile exports and adoption of eco-efficient digital printing under the “Made in China 2025” initiative.

- Europe accounted for 23% of the global market, led by Italy’s premium textile manufacturing base, representing 36% of regional industry turnover and strong sustainability-driven regulations.

- North America captured 20% market share in 2025, supported by reshoring initiatives, EPA-led sustainability standards, and modernisation investments exceeding $22 billion in advanced textile production.

- Direct-to-Fabric and Direct-to-Garment printing technologies led with 33% market share, favoured for high versatility, production efficiency, and rapid customisation in apparel manufacturing.

- The apparel and fashion segment dominated with 42% market share in 2025, fueled by the growing demand for personalised, sustainable, and fast fashion solutions supported by digital printing.

- Natural fibres held the largest fabric share at 48%, driven by high consumer preference for cotton-based textiles in apparel and home furnishing applications.

- Blended fabrics emerged as the fastest-growing segment, offering enhanced durability, comfort, and sustainability across fashion and industrial textile categories.

- Soft signage and promotional materials represented the fastest-growing application segment, propelled by expanding demand for lightweight, reusable display solutions in events, retail, and advertising sectors.

| Global Market Attributes | Key Insights |

|---|---|

| Digital Textile Printing Market Size (2025E) | US$ 5.0 Bn |

| Market Value Forecast (2032F) | US$ 11.3 Bn |

| Projected Growth (CAGR 2025 to 2032) | 12.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 10.8% |

Market Dynamics

Drivers - Sustainability Mandates and Water Conservation Imperatives

Digital textile printing addresses critical environmental challenges inherent in conventional textile manufacturing by fundamentally reducing water consumption by up to 90% compared to traditional rotary screen-printing processes.

The U.S. Environmental Protection Agency has documented that traditional textile dyeing and printing operations consume approximately 10,000 litres of water per kilogram of cotton fabric, generating substantial contaminated wastewater discharge.

Digital printing employs inkjet technology to apply dyes directly onto fabric substrates, eliminating large dye bath requirements and extensive post-treatment rinsing procedures. In 2024, the U.S. textile industry employed approximately 471,046 workers with total shipments reaching $63.9 billion, while simultaneously investing $22.3 billion between 2013 and 2022 in modernisation initiatives, including digital printing facilities and circular economy infrastructure focused on textile waste recycling.

The European Union's Eco-design for Sustainable Products Regulation, approved in July 2024, mandates that textiles placed on the market must incorporate at least 50% recycled materials by 2024, with 20% prepared for reuse, creating regulatory tailwinds for water-efficient digital printing adoption.

India's textile sector, contributing 2% to GDP and employing over 45 million people, has witnessed the Ministry of Textiles increase budget allocation by 19% to Rs. 5,272 crore (US$607 million) for FY 2025-26, prioritising sustainable manufacturing technologies.

These combined policy frameworks and environmental imperatives are propelling digital printing adoption as manufacturers seek to comply with stringent wastewater discharge norms while maintaining production efficiency.

On-Demand Production and Fast Fashion Ecosystem Integration

The transformation of apparel retail through e-commerce platforms has fundamentally restructured production workflows, with digital textile printing enabling print-on-demand business models that eliminate inventory risk and overproduction waste.

The U.S. Census Bureau reported e-commerce retail sales reached $291.6 billion in Q2 2024, representing 16% of total retail sales with 6.7% year-over-year growth. Digital printing technology allows fashion brands to produce smaller quantities across multiple design variations, rapidly restocking high-performing items while minimising markdown exposure on slower-moving inventory.

India's apparel market, projected to expand at a 10% CAGR to reach US$2.3 billion by 2030, exemplifies this shift, with digital spending in the fashion sector increasing 12% year-over-year as brands leverage customization capabilities.

Digital textile printing's ability to deliver complex, multi-colored designs without screen preparation or setup costs enables brands to respond to trend cycles in real-time, compressing lead times from 60-plus days for trans-Pacific shipments to 20 days for nearshore digital production facilities.

Technological Advancement in Printing Hardware and Ink Formulations

Innovation in printhead technology, automation systems, and specialised ink chemistry has elevated digital textile printing from experimental applications to industrial-scale production capability.

Modern digital textile printers integrate advanced automation, including smart printhead protection systems, constant temperature control, and intelligent water-saving belt cleaning mechanisms that enhance production efficiency and print quality consistency. High-speed single-pass printers have emerged as transformative technology, with production capacities reaching 1,080 square meters per hour while maintaining photorealistic resolution and colour accuracy.

The development of one-step pigment printing systems, exemplified by technologies that eliminate pre-treatment and post-treatment requirements, has reduced energy consumption by 75% and processing time by consolidating multiple production stages into unified workflows. Between 2023 and 2024, over 70 new digital textile printer models were launched globally, reflecting intense competitive innovation in equipment capabilities.

Ink formulation advancements have yielded eco-certified pigment inks with ECO PASSPORT certification, demonstrating compliance with OEKO-TEX standards while delivering superior wash fastness, light fastness, and soft hand-feel characteristics demanded by premium fashion markets.

Restraint - Capital Investment Requirements and Operational Cost Structures

The transition from conventional to digital textile printing necessitates substantial capital expenditure for specialised equipment, with high-speed industrial digital printers representing significant upfront investment barriers, particularly for small and medium-sized textile manufacturers.

While digital printing eliminates screen engraving costs and setup time, variable costs per printed meter remain higher than conventional rotary screen printing for long production runs, creating economic thresholds where traditional methods maintain cost advantages.

Maintenance requirements for digital printheads, specialised ink procurement, and technical operator training add operational complexity and recurring cost obligations. The initial investment hurdle is compounded by the need for ancillary infrastructure, including colour management systems, pre-treatment application equipment for certain fabric types, and quality control protocols to ensure consistent output across production batches.

Opportunity - Expansion in Technical Textiles and Industrial Applications

Digital printing enables functionality-enhanced textile production for automotive, aerospace, healthcare, and construction applications requiring specialised performance characteristics, including flame retardancy, antimicrobial properties, and high-tenacity construction.

India's mobiltech textile market, serving automotive applications, is projected to grow from US$2.32 billion in FY25 to US$4.57 billion by FY33, at an 8.84% CAGR, fueled by the adoption of electric vehicles and innovations in sustainable materials.

Digital printing technology facilitates rapid prototyping and customization of technical textile products, enabling manufacturers to develop application-specific solutions for medical-grade fabrics, protective workwear, and high-performance sportswear without extensive tooling investments.

Circular Economy Integration and Textile Waste Valorisation

The global textile industry generates approximately 92 million tons of waste annually, with less than 10% currently recycled in circular economy systems, representing $150 billion in lost material value.

Digital printing technologies support circular economy frameworks by enabling print-on-demand production models that minimise overproduction waste, facilitate rapid prototyping without material-intensive sampling, and allow economically viable small-batch manufacturing of customised products.

The European Union's strategy for sustainable and circular textiles, targeting 2030 compliance where textiles must be durable, recyclable, and produced responsibly, creates regulatory drivers for circular production systems.

Category-wise Analysis

Printing Technology Segment Insights

Direct-to-Fabric and Direct-to-Garment printing technologies commanded 33.0% of the global digital textile printing market in 2025, establishing dominance through versatility, production efficiency, and quality output capabilities.

DTG Printing employs specialised inkjet technology to apply full-colour designs directly onto garments, enabling complex photographic reproduction and gradient colour transitions unachievable through traditional screen-printing methods.

Technology eliminates minimum order quantity constraints, supporting personalised custom apparel production economically viable for single-unit orders through print-on-demand business models.

Water-based pigment inks utilised in DTG applications reduce environmental impact by 40% compared to screen printing while producing soft-to-touch prints with excellent wash fastness properties.

Kornit Digital's Apollo system with integrated curing technology and Epson's SureColor F-series printers exemplify advanced DTG platforms achieving production speeds under five minutes per custom t-shirt while maintaining photorealistic print quality.

The technology's applicability across cotton, polyester, and blended fabric compositions, combined with single-operator production workflow automation, positions DTF/DTG as the preferred solution for fashion brands, promotional merchandise, and print-on-demand service providers.

Reactive ink printing represents the fastest-growing technology segment within digital textile printing, distinguished by chemical bonding between reactive dyes and natural fibre molecules during steaming fixation processes.

Fabric Type Segment Insights

Natural fibres commanded 48.0% of the global digital textile printing market in 2025, reflecting consumer preferences for breathable, comfortable textile products and the extensive application of cotton, silk, linen, and wool in apparel and home textile categories. Cotton production, estimated at 7.2 million tonnes (~43 million bales of 170 kg each), projected by 2030 in India alone, ensures abundant raw material availability for natural fibre textile manufacturing.

Blended fabrics represent the fastest-growing fabric type segment, driven by performance characteristics combining natural fibre comfort with synthetic fibre durability, wrinkle resistance, and easy-care properties.

Application Segment Insights

The apparel and fashion segment dominated the global digital textile printing market with 42.0% share in 2025, reflecting the fashion industry's adoption of digital printing for rapid design iteration, customisation capabilities, and sustainable production methodologies.

Digital printing enables faster production cycles compared to traditional screen printing by eliminating screen setup processes, allowing fashion brands to compress lead times and adapt quickly to emerging trends in the fast-moving fashion industry.

The sustainable fashion movement, with 94.6% of consumers expressing willingness to pay premiums for eco-friendly options, drives the adoption of water-efficient digital printing technologies, reducing environmental impact while maintaining high-quality output. Fashion applications benefit from digital printing's ability to reproduce complex, detailed, multi-colored designs without limitations of traditional methods, supporting brand differentiation through unique visual content.

The ASEAN digital textile printing market, dominated by clothing with over 40% share, exemplifies regional concentration in apparel applications, with Direct-to-Garment technology capturing more than 38% of the Japanese market demand for highly qualitative custom prints satisfying stringent fashion requirements.

Soft signage and promotional materials emerged as the fastest-growing application segment, propelled by demand for lightweight, portable, reusable fabric-based display solutions across retail, events, exhibitions, and outdoor advertising.

Regional Insights and Trends

East Asia Digital Textile Printing Market Trend

East Asia commanded 37% of the global digital textile printing market in 2025, driven by China's position as the world's largest textile manufacturer, holding over 41% of global textile and apparel exports. China's "Made in China 2025" initiative promotes intelligent manufacturing systems, including high-speed textile printers, while the Ministry of Ecology and Environment enforces stricter wastewater discharge norms, pushing textile factories toward digital printing adoption.

Major textile production clusters in Zhejiang and Guangdong provinces are accelerating printer adoption, responding to twin pressures of environmental regulations and automation incentives. Japan's digital textile printer market is propelled by R&D in smart textiles and industrial fabrics supported by the National Institute of Advanced Industrial Science and Technology, with government programs encouraging university-industry collaboration for advanced materials and printing innovations.

North America Digital Textile Market Trends

North America held 20% of the global digital textile printing market in 2025 The U.S. textile printing market, holding a dominant regional position in 2024, benefits from sustainability emphasis and supply chain agility as the Office of Textiles and Apparel reports a steady rise in domestic textile production supported by nearshoring strategies and reshoring of fashion supply chains. American print houses increasingly adopt pigment ink systems and direct-to-garment technologies to minimise water use and chemical discharge, responding to EPA-led environmental standards.

The U.S. textile industry employed approximately 471,046 workers in 2024, with total shipments reaching $63.9 billion, remaining the world's second-largest exporter of textile-related products with combined fibre, textile, and apparel exports totalling $28 billion in 2024.

Investment of $22.3 billion between 2013-2022 in new plants and equipment focused on modernisation, automation, and circular economy initiatives, including recycling facilities, demonstrates a commitment to technology adoption.

Europe Digital Textile Printing Market Trends

Europe accounted for 23% of the global digital textile printing market share in 2025, characterised by strong sustainability regulatory frameworks and premium textile manufacturing concentration. The European textile industry recorded EUR 170 billion turnover in 2023, employing approximately 1.3 million people across 197,000 companies, with production focused on high-value segments including technical textiles and premium clothing.

Italy dominates European textile activities with 24% of employment, 36% of industry turnover, and 30% of exports, positioning it as the central hub for European textile manufacturing. The European Commission's Ecodesign for Sustainable Products Regulation, approved July 2024, mandates products to be durable, reusable, and incorporate recycled materials, with Digital Product Passport requirements expected to be finalised by mid-2025, creating a traceability infrastructure.

The Corporate Sustainability Due Diligence Directive requires fashion and textile brands to develop due diligence policies identifying human and environmental impacts throughout value chains, with phased implementation from 2027-2029 based on company size and turnover thresholds.

Competitive Landscape

The global digital textile printing market is largely oligopolistic with a consolidated core of technology-intensive companies and a fragmented long tail of regional specialists and OEMs. A handful of leaders, Kornit Digital Ltd., Seiko Epson Corporation, Durst Group, Mimaki Engineering Co., Ltd., and Roland DG dominate innovation, proprietary inks, and industrial-scale solutions, setting high entry barriers.

Smaller companies and local OEMs compete on niche applications, cost and service flexibility, keeping the market dynamic. Intense R&D, strategic partnerships, and after-sales service differentiate winners, while volume contracts with apparel and home-textile brands reinforce the incumbents’ positions. Overall, market power is concentrated but evolving as new ink and substrate technologies lower some barriers.

Key Industry Developments:

- In October 2025, Kornit Digital Ltd. announced that UK-based Snuggle expanded its fleet to nine Kornit Atlas MAX PLUS direct-to-garment systems, enabling production of over 24,000 pieces daily and quadrupling capacity since 2017. This development highlights the growing adoption of advanced digital textile printing technologies for on-demand, high-quality apparel production, reinforcing Kornit’s leadership in sustainable and scalable digital textile solutions.

- In September 2025, MS Printing Solutions and JK Group, subsidiaries of Dover Corporation, launched the new MP Series of multi-pass printers for digital textile printing. The series introduces advanced performance features, including enhanced durability, modular architecture, and support for multiple ink types, catering to fashion, sportswear, and direct-to-fabric applications. This launch underscores Dover’s commitment to innovation, speed, and sustainability in digital textile printing technologies.

Companies Covered in Digital Textile Printing Market

- Kornit Digital Ltd.

- Dover Corporation

- Roland DG / Roland DGA

- Seiko Epson Corporation

- Durst Group

- Mimaki Engineering Co., Ltd.

- Konica Minolta, Inc.

- MUTOH HOLDINGS CO., LTD.

- SPGPrints B.V.

- Electronics For Imaging, Inc.

- DCC Print Vision LLP

Frequently Asked Questions

The global Digital Textile Printing Market is projected to be valued at US$ 5.0 Bn in 2025.

The Direct-to-Fabric (DTF) / Direct-to-Garment (DTG) segment by Printing Technology is expected to hold around 33% market share in 2025, driven by its versatility, efficiency, and ability to deliver high-quality custom prints for fashion, apparel, and on-demand production needs.

The market is poised to witness a CAGR of 12.5% from 2025 to 2032.

The growth of the Digital Textile Printing Market is driven by rising demand for sustainable, on-demand printing solutions and advancements in high-speed inkjet and pigment-based technologies.

Key market opportunities in Digital Textile Printing include expansion in technical textiles and industrial applications, enabling advanced solutions for automotive, healthcare, and construction sectors; and circular economy integration, which focuses on textile waste valorisation, compatibility with recycled fibres, and supporting sustainable on-demand production models to meet evolving regulatory and consumer demands.

The top key market players in the global Digital Textile Printing Market include Kornit Digital Ltd., Dover Corporation, Seiko Epson Corporation, Mimaki Engineering Co., Ltd., Durst Group, Roland DG Corporation, Konica Minolta, Inc., and Electronics for Imaging, Inc.