- Processed Food

- Butter Market

Butter Market Size, Trends, Share, Growth, and Regional Forecast, 2025 - 2032

Butter Market by Nature (Organic, Conventional), by Form (Spreadable, Non-Spreadable), by Industry, by Distribution Channel, and Regional Analysis from 2025 - 2032

Butter Market Share and Trends Analysis

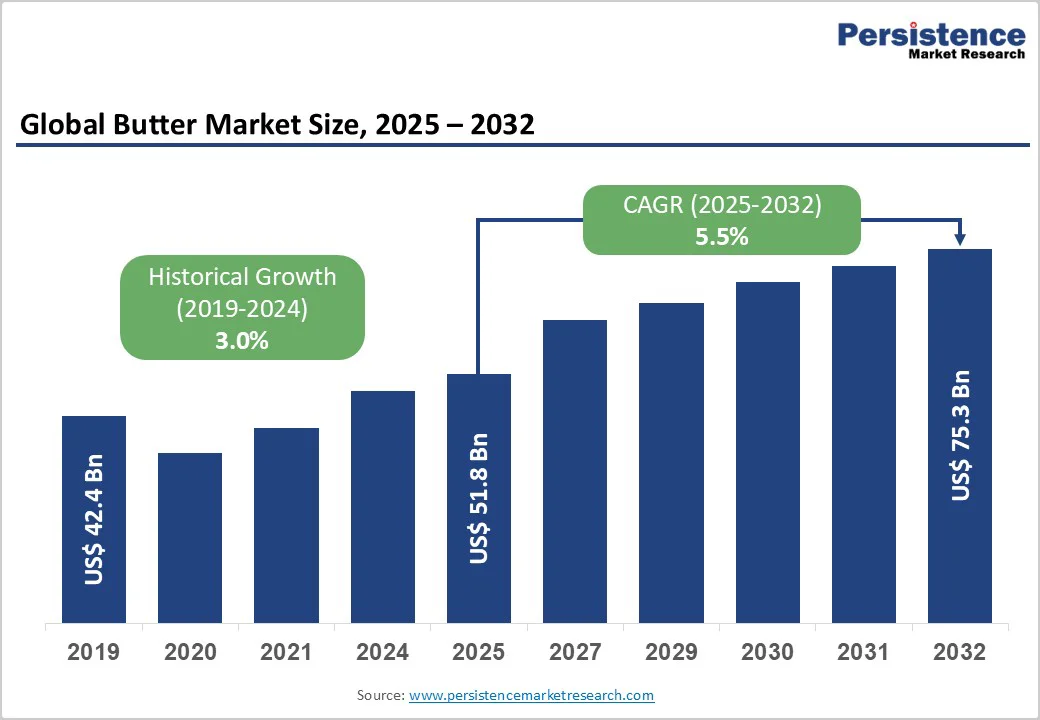

The global butter market size is likely to be valued at US$51.8 billion in 2025 and is projected to reach US$75.3 billion at a CAGR of 5.5% during the forecast period from 2025 to 2032.

The market is witnessing steady growth driven by rising demand for natural and premium dairy products, as well as expanding bakery and confectionery applications. Consumers are increasingly favoring clean-label and minimally processed foods, boosting butter’s appeal over margarine and artificial spreads. Additionally, the surge in home baking trends and the popularity of traditional cuisines are strengthening consumption across both developed and emerging economies.

Key Industry Highlights:

- Artisanal bakeries, patisseries, and premium dessert chains increasingly prefer real butter over substitutes for authentic texture and flavor. Hence, the popularity of the bakery and confectionery industry significantly boosts butter demand.

- The emergence of plant-based diets has led to rapid innovation in vegan butter alternatives made from coconut, almond, and soy oils.

- Conventional butter remains dominant due to lower production costs, wider retail availability, and strong usage in bakery, confectionery, and foodservice sectors.

| Key Insights | Details |

|---|---|

|

Butter Market Size (2025E) |

US$51.8 Bn |

|

Market Value Forecast (2032F) |

US$75.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.0% |

Market Dynamics

Driver - Increasing Adoption of Clarified Butter Worldwide

Clarified butter, commonly known as ghee, is witnessing remarkable global adoption beyond its traditional South Asian roots. In recent years, it has gained immense popularity across Western markets as consumers embrace holistic nutrition and functional foods. On heating, it reaches a high smoke point that makes it a preferred choice for high-temperature cooking, keto diets, and paleo lifestyles. Moreover, it contains conjugated linoleic acid (CLA) and fat-soluble vitamins, which are associated with improved digestion, immunity, and heart health. Its long shelf life and rich, nutty flavor further enhance its appeal among chefs and health enthusiasts alike. The growing recognition of clarified butter as a clean, lactose-free, and nutrient-dense dairy fat positions it as a premium, versatile alternative within the expanding global butter market.

Restraints - Rising Vegan and Lactose-Free Consumer Base

The global transition toward plant-based and lactose-free diets is posing a substantial challenge to traditional butter consumption. A growing segment of consumers, particularly in North America and Europe, is actively reducing dairy intake due to ethical, environmental, and digestive health concerns. This shift is being reinforced by younger demographics and flexitarians who associate non-dairy alternatives with wellness, sustainability, and animal welfare.

As a result, nut-, soy-, and coconut-based spreads are capturing shelf space once dominated by conventional butter. The market is witnessing rapid innovation in vegan formulations that replicate butter’s texture and flavor using fermentation and fat-blending technologies. Consequently, dairy butter producers face pressure to adapt their portfolios and sustainability credentials to remain competitive in evolving consumer landscapes.

Opportunity - Expansion in the Vegan and Plant-Based Butter Category

The premium and organic butter segment is gaining significant traction as consumers increasingly prioritize health, sustainability, and ethical sourcing. Certified organic, non-GMO, and fair-trade butters appeal to high-end consumers willing to pay a premium for quality and transparency.

These products not only offer superior nutritional value but also align with growing environmental and social responsibility trends, including sustainable farming and ethical labor practices. Brands can differentiate through unique certifications, traceable supply chains, and artisanal processing techniques, thereby building strong trust. Additionally, this segment caters to niche markets such as gourmet baking, clean-label snacks, and wellness-focused meal kits, making it a high-potential growth avenue in the global butter market.

Category-wise Analysis

By Nature Insights

The conventional butter segment dominates the global market due to its wide availability, cost efficiency, and established supply chains. Produced using standard dairy farming methods, it caters to the mass consumption needs of households, bakeries, and foodservice industries, where consistency and affordability are key. Its strong retail presence across supermarkets and convenience stores further boosts sales. In contrast, organic butter faces limitations, including higher production costs, limited organic milk supply, and premium pricing, restricting its reach to niche consumers. However, as health-conscious and sustainability-driven consumers rise, organic variants are witnessing steady growth. Still, conventional butter remains the market leader because it aligns with the price-sensitive and large-volume demand structure that sustains the global dairy economy.

By Industry Insights

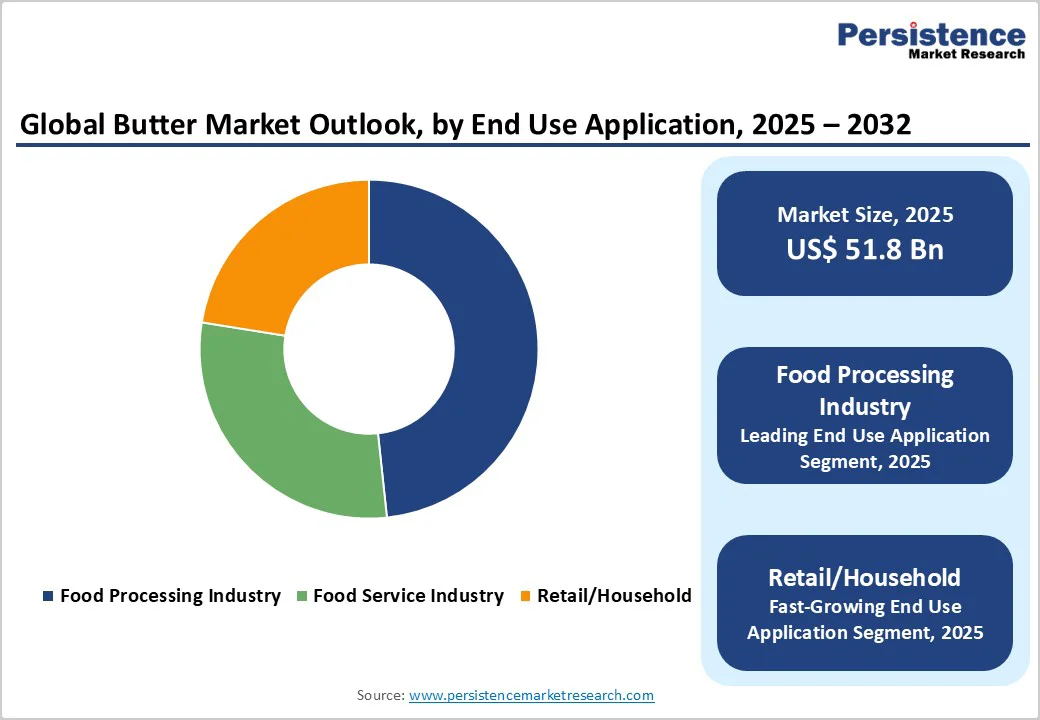

The food processing industry dominates the butter market as it serves as a core ingredient in bakery, confectionery, snacks, and ready-to-eat product formulations. Butter’s functional properties-such as enhancing flavor, texture, and moisture retention-make it indispensable for large-scale food manufacturing. Major industrial users include biscuit, chocolate, and frozen dessert producers, which require butter in bulk quantities. Its widespread use in processed and packaged foods across both developed and emerging economies sustains demand. Conversely, the Food Service Industry (restaurants, hotels, bakeries) contributes a moderate share, while Retail/Household consumption is growing due to premium and flavored butter varieties but remains smaller than the massive industrial demand driven by global food manufacturing trends.

Region-wise Insights

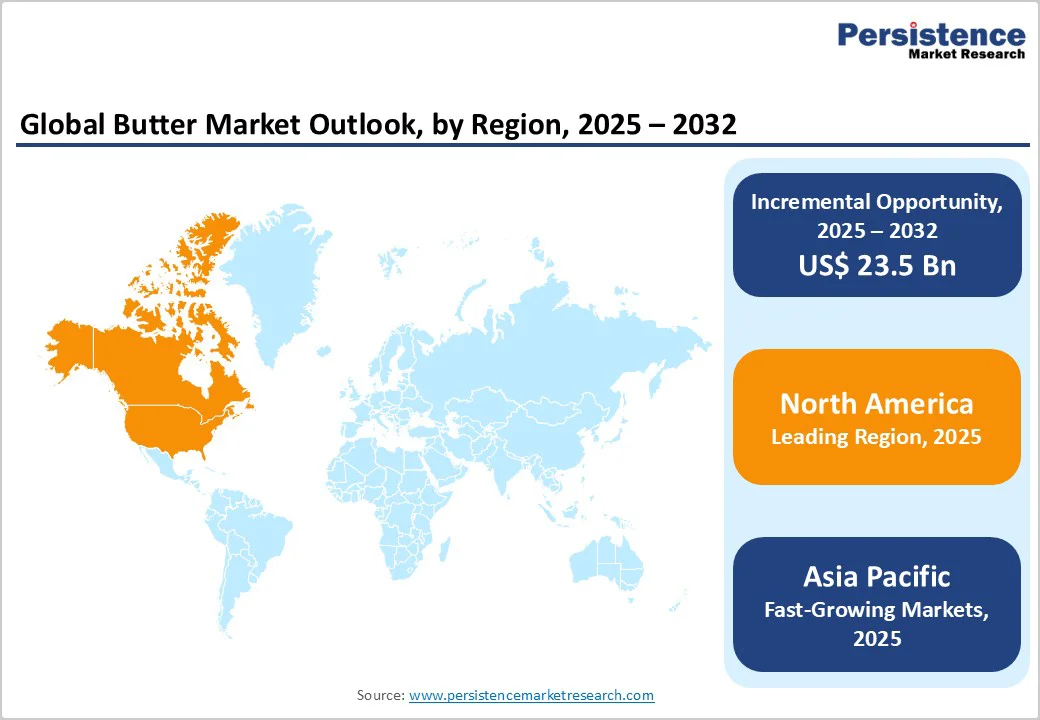

North America Butter Trends

North America, particularly the United States, leads the global butter market, driven by strong consumer preference for natural dairy fats over margarine and plant-based spreads. The region benefits from high per capita butter consumption, advanced dairy processing infrastructure, and a robust food manufacturing base. Growth is fueled by the expanding bakery, confectionery, and ready-to-eat sectors, where butter remains a key ingredient. The rise of artisanal and grass-fed butter varieties reflects consumers’ growing interest in clean-label, high-quality, and locally sourced products. Moreover, the U.S. dairy industry’s focus on product innovation, such as flavored, whipped, and cultured butters, is reinforcing market expansion. Favorable trade policies and premium exports to Europe and Asia further strengthen North America’s leading position in the global butter landscape.

Asia Pacific Butter Market Trends

The Asia Pacific butter market is emerging as the fastest-growing regional segment, propelled by rising urbanization, Western dietary influence, and expanding bakery and confectionery industries. Countries like India, China, and Japan are witnessing surging demand for butter in both household and industrial applications. Increasing disposable incomes and the popularity of ready-to-eat and café-style bakery foods are fueling market expansion. Local dairy cooperatives and global brands are investing in value-added butter variants, including unsalted, flavored, and organic options, to cater to evolving consumer preferences. Moreover, the growth of the foodservice sector and quick-service restaurants is accelerating butter usage in everyday cooking and baking. Improved cold-chain infrastructure and digital retail penetration are further strengthening the Asia Pacific’s role as a key emerging butter market.

Competitive Landscape

The butter market’s competitive landscape is defined by intense rivalry between large-scale dairy producers, regional cooperatives, and emerging niche brands. Competition centers on product differentiation, quality, and innovation, with growing emphasis on organic, grass-fed, and flavored butter varieties. Companies are investing heavily in automation, cold-chain logistics, and digital retail channels to strengthen their market presence. Rising consumer awareness of health, purity, and sustainability is driving firms to adopt eco-friendly packaging and ethical sourcing practices.

Key Industry Developments:

- In October 2025, Savor developed animal-free fats that chemically matched real dairy fats but had lower CO2 emissions, water consumption, and land use than their agricultural counterparts. Starting with water and either carbon dioxide or methane, the food-tech firm used a thermal process to synthesize fatty acid molecules, which were then assembled into fats such as milkfat and butter.

Companies Covered in Butter Market

- Royal FrieslandCampina N.V

- Fonterra Co-operative Group Limited

- Groupe Lactalis S.A.

- Arla Foods amba

- Amul (GCMMF)

- Dean Foods Co

- Saputo Inc.

- OMSCO

- Dairy Farmers of America

- Other

Frequently Asked Questions

The global market is projected to be valued at US$51.8 Bn in 2025.

Rising demand for natural and clean-label products as consumers shift away from artificial spreads and margarine.

The global market is poised to witness a CAGR of 5.5% between 2025 and 2032.

Growth in plant-based and vegan butter alternatives, appealing to flexitarian and lactose-intolerant consumers.

Royal FrieslandCampina N.V, Fonterra Co-operative Group Limited, Groupe Lactalis S.A., Arla Foods amba, Amul (GCMMF), and others.